By Infometrics economist Andrew Gawith Over the past two years the New Zealand dollar has trampolined spectacularly, plummeting almost 25% over the 12 months ended March 2009 and then rebounding 23% since then. Many exporters and importers are exasperated, while currency traders and economists have been made to look like chumps. But that won't stop them making currency forecasts; after all, some mug has to. Sorry, you won't get a currency pick in this column; the purpose is to look at the volatility of the currency, what has pushed it around over the past few years, the remarkable stability of the currency over the long-term, and the cost of currency volatility for investment and to economic growth.

By Infometrics economist Andrew Gawith Over the past two years the New Zealand dollar has trampolined spectacularly, plummeting almost 25% over the 12 months ended March 2009 and then rebounding 23% since then. Many exporters and importers are exasperated, while currency traders and economists have been made to look like chumps. But that won't stop them making currency forecasts; after all, some mug has to. Sorry, you won't get a currency pick in this column; the purpose is to look at the volatility of the currency, what has pushed it around over the past few years, the remarkable stability of the currency over the long-term, and the cost of currency volatility for investment and to economic growth.

The $NZ has definitely been more volatile over the past year or so. The standard deviation (a measure of how variable a series is) for the $US/$NZ exchange rate has increased significantly since mid-2008 and is around twice what it was for most of the 1990s. In simple terms, the daily fluctuations in the dollar have increased markedly with the $US/$NZ falling or rising from one day to the next by an average of 1% this year, compared to just 0.5% over most of the 1990s. Interestingly, the dollar has tracked the slumps and rebounds in the US stock market remarkably closely (see graph) suggesting financial markets' perception of risk has been the major factor driving our dollar. In the midst of the financial crisis investors rushed to what they perceived to be safe assets "“ fringe currencies such as the $NZ didn't rate so the currency fell almost as fast as share prices. However, as investors rediscovered their appetite for risk they ploughed back into exotic currencies and battered stocks. The $NZ and stock markets rose almost in lock step to the soothing sounds of recovery. But risk has not always been behind the wheel of the currency.  Prior to the credit crisis, it was interest rates "“ New Zealand rates were higher than in most other developed economies so smart people borrowed (in, say, Japan) where interest rates were negligible, and invested in New Zealand. The so-called carry trade was based on making money from the interest rate differential "“ a higher return on the funds invested than on the cost of funds borrowed. Simple stuff really. But the carry trade meant a big inflow of capital chasing our high interest rates and that capital inflow drove the $NZ higher, conveniently adding to the returns the smart people were getting. The $NZ is also part of the commodity currency club whose membership includes Australia, Canada and South Africa. The argument goes that economies producing old-economy commodities will do particularly well in a world increasingly dominated by raw-material hungry countries like China and India. And so it has proven to be over the last year or so "“ the Australian dollar has increased by around 45% against the $US and the Canadian dollar is up by 17%. Fundamentals like the balance of payments seem almost irrelevant to the exchange rate. New Zealand runs one of the largest current account deficits relative to GDP of any western economy and has done so for 40 odd years.

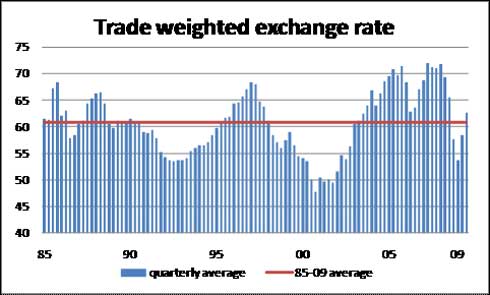

Prior to the credit crisis, it was interest rates "“ New Zealand rates were higher than in most other developed economies so smart people borrowed (in, say, Japan) where interest rates were negligible, and invested in New Zealand. The so-called carry trade was based on making money from the interest rate differential "“ a higher return on the funds invested than on the cost of funds borrowed. Simple stuff really. But the carry trade meant a big inflow of capital chasing our high interest rates and that capital inflow drove the $NZ higher, conveniently adding to the returns the smart people were getting. The $NZ is also part of the commodity currency club whose membership includes Australia, Canada and South Africa. The argument goes that economies producing old-economy commodities will do particularly well in a world increasingly dominated by raw-material hungry countries like China and India. And so it has proven to be over the last year or so "“ the Australian dollar has increased by around 45% against the $US and the Canadian dollar is up by 17%. Fundamentals like the balance of payments seem almost irrelevant to the exchange rate. New Zealand runs one of the largest current account deficits relative to GDP of any western economy and has done so for 40 odd years.  So we have a vague idea of what drives the currency, but where have such factors driven it to since it was floated in 1985? Well the short answer is.....nowhere. The trade weighted exchange rate has averaged 60.8 since 1985 "“ almost exactly the same as it was when the dollar was floated 24 years ago (61.79). That consistency hides some long periods when the currency was either below or above this long-term average, most recently above as a result of relatively high interest rates and more fundamentally a significant and sustained lift in the terms of trade. However, the data support the view that the real exchange rate tends to revert to fairly stable long term average, which suggests that as an economy we have made little or no progress over the last 25 years in lifting the value of what we produce. The volatility, or more correctly the large and sustained swings in the exchange rate have increased the risks associated with investing for our major export businesses "“ agriculture and tourism. The currency gyrations have also created havoc for many emerging manufacturing and high tech export businesses whose profits have swung wildly on the back of the yo-yoing dollar. Currency uncertainty is a killjoy for these industries. If we are serious about lifting New Zealand's growth rate and closing the gap with Australia, a more stable exchange rate is likely to be important in getting the required investment. Some countries, notably Brazil, have moved to discourage large speculative capital flows in an attempt to dampen the swings in their currencies. There may be other more fundamental policy responses that could help tame the swings. But short of going back to a fixed exchange rate, New Zealand businesses will have to rely on strategies (currency hedging, for example) to cushion the worst effects of the currency jumps and dives "“ the government won't come to their rescue anytime soon. ________________ * Infometrics is an economic information and forecasting company based in Wellington. To find out more, see its website here. This piece first appeared in the Dominion Post.

So we have a vague idea of what drives the currency, but where have such factors driven it to since it was floated in 1985? Well the short answer is.....nowhere. The trade weighted exchange rate has averaged 60.8 since 1985 "“ almost exactly the same as it was when the dollar was floated 24 years ago (61.79). That consistency hides some long periods when the currency was either below or above this long-term average, most recently above as a result of relatively high interest rates and more fundamentally a significant and sustained lift in the terms of trade. However, the data support the view that the real exchange rate tends to revert to fairly stable long term average, which suggests that as an economy we have made little or no progress over the last 25 years in lifting the value of what we produce. The volatility, or more correctly the large and sustained swings in the exchange rate have increased the risks associated with investing for our major export businesses "“ agriculture and tourism. The currency gyrations have also created havoc for many emerging manufacturing and high tech export businesses whose profits have swung wildly on the back of the yo-yoing dollar. Currency uncertainty is a killjoy for these industries. If we are serious about lifting New Zealand's growth rate and closing the gap with Australia, a more stable exchange rate is likely to be important in getting the required investment. Some countries, notably Brazil, have moved to discourage large speculative capital flows in an attempt to dampen the swings in their currencies. There may be other more fundamental policy responses that could help tame the swings. But short of going back to a fixed exchange rate, New Zealand businesses will have to rely on strategies (currency hedging, for example) to cushion the worst effects of the currency jumps and dives "“ the government won't come to their rescue anytime soon. ________________ * Infometrics is an economic information and forecasting company based in Wellington. To find out more, see its website here. This piece first appeared in the Dominion Post.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.