By Gareth Vaughan

My article on Wednesday, on a UK assessment of quantitative easing (QE), was based on a Bank of England paper citing a range of other papers and reports on QE. Given the ongoing debate in New Zealand on whether QE is exacerbating wealth and income inequality, one of these other papers is worth a closer look.

This paper is entitled; Quantitative (displ)easing? Does QE work and how should it be used next time? It comes from the London-based Resolution Foundation, which describes itself as an independent think-tank focused on improving the living standards of those on low-to-middle incomes.

The paper notes that a common criticism of the Bank of England’s QE, first launched in 2009, is that the lion’s share of the benefits have gone to the already wealthy. (The paper was published before COVID related QE launched in 2020).

This inequality concern, highlighted by rising house and share market prices, has also emerged in New Zealand since the Reserve Bank of New Zealand (RBNZ) embarked on QE last March. In response to this Governor Adrian Orr said in December the RBNZ will probe the impact of loose monetary policy on inequality.

The Resolution Foundation paper, authored by Joseph E. Gagnon, Jack Leslie, Fahmida Rahman and James Smith, says this concern is not without substance. This it argues, is especially as QE is found to work to a large extent by boosting asset prices, suggesting it disproportionately helps wealthy asset holders.

"But this is only a partial view of the impact of QE and it does not take into account the wider effects on the economy. A more complete analysis of the impact of QE shows a more nuanced picture: by design, QE increases wealth (via rising asset prices) which has the largest effect on the already wealthy."

"But counterbalancing macroeconomic effects (via changes to inflation, employment and wages) increases income more evenly across the distribution. Before turning to new analysis which quantifies the distributional impact of QE, it is important to clarify the channels through which QE impacts the welfare of UK households," the paper says.

Below are the detailed wealth and income effects outlined in the paper.

Wealth effects:

• Changes in financial wealth. Purchases of government bonds pushes up bond prices and through the portfolio rebalancing mechanism, increases the price of other financial assets. This increases the wealth of those holding these financial assets.

• Changes in property wealth. Financial asset price rises will spill over into increasing property prices and thus property wealth for those owning a house.

• Inflation effect. QE raises the level of inflation which, in real terms, reduces the value of loans and the value of assets held in nominal amounts (e.g. current accounts). This effectively redistributes net wealth from savers towards borrowers.

Income effects:

• Employment effect. QE supports economic activity – reducing the output gap – and therefore raises the employment level, increasing wellbeing for workers who would not have been employed in the absence of QE.

• Wage effect. Improved macroeconomic conditions lead to a tighter labour market, pushing up on wage growth.

QE shouldn't have long-term effects on asset prices or economic activity apart from helping smooth economic fluctuations and thus reducing the drag on potential economic output, the paper argues.

Figure 3 from the Resolution Foundation paper below shows the estimated impact of QE, from the first three channels detailed above, on average net wealth for each net wealth decile. According to this, about 40% of the aggregate boost to wealth from changes in financial asset prices, property prices, and inflation went to families in the highest wealth decile, while only 12% of the benefit went to the bottom half.

"This reflects the already highly skewed wealth distribution in the UK (around 50% of total wealth is held by the highest wealth decile): a rise in asset prices directly benefits those already holding those assets. In other words, the changes in asset prices scale the existing value of wealth, meaning that the proportional impact is more constant than the absolute effect."

"But the types of asset held by families in each wealth decile do affect the aggregate impact somewhat: those holding proportionally more financial assets are advantaged more by QE than those with larger property wealth, based on the Bank of England’s estimates of the changes in financial and property asset prices," the paper says.

The paper goes on to say that the wealth effects should unwind when QE is withdrawn.

"Policy makers originally envisaged QE to be a short-term measure and therefore judged that the ‘real world’ impact of these temporary changes in wealth would be small. However QE stimulus has been used for a much longer period than originally envisaged [in the UK], meaning wealth changes will not only feel more permanent but in some cases very directly feed into lasting effects on the real economic position of households."

This, it argues, will happen in three main ways.

"First, it is more expensive to buy assets (e.g. housing) which will prevent some people from purchasing them over time. Second, when QE is unwound and asset prices move back to their underlying value, those who purchased assets at the higher price will lose out. And third, pre-existing owners of assets are able to sell them at the higher price and realise a higher level of consumption," the paper says.

It also points out that the asset price impact of QE isn't the ultimate objective of the policy. However, it's often is the only issue considered when discussing QE's distributional effects.

"QE’s macroeconomic effects on output, inflation and the labour market are often overlooked. The increase in asset prices and falls in real interest rates from QE should boost economic growth and reduce any output gap. This will result in lower unemployment and therefore higher wage growth via a tighter labour market. Together these effects will boost average labour income."

Figure 4 below highlights the effect of QE on average annual incomes, split by net income decile.

Here the paper notes the benefits are much more evenly distributed via income than the wealth effects were and, as a proportion of income, help the bottom half the most.

"This is driven by the fact that QE is estimated to have increased employment more at the bottom of the income distribution than the top. The aggregate result of this is that the macroeconomic effect will reduce, rather than increase, income inequality. This is in contrast to the asset price effect, which appears to increase absolute wealth gaps (and be broadly neutral in relation to relative wealth inequality). The income effect is also progressive when split by wealth decile, meaning that families not benefiting from higher asset prices are partially compensated by the income effect," the paper says.

"Having this rounded picture of the distributional impact of QE in mind is crucial to policy makers both evaluating the policy, but also considering what wider policies might best sit alongside any future use of QE. More controversy over the looseness of monetary conditions should also not be a surprise after such a long period."

"In many ways, the deeper issue is that QE is conflated in the public mind with a secular decline in interest rates of all kinds – one that preceded the [global] financial crisis and appears to be continuing," the paper says.

"The challenge is that with policy rates still close to all-time lows in many countries ... QE will almost certainly be asked to play a key role in supporting the economy in future. So having a well-articulated plan for using it is essential, and a key part of that plan must be ensuring that QE can be used in a transparent way that eases the pressure on central banks to refrain from using it."

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

30 Comments

In New Zealand a lot of small business lending is guaranteed by a house. This makes it hard to separate stimulus packages and the property market.

Two key points:

1) The argument that supposed benefits of QE pass through to the lower deciles within the population is essentially a trickle down argument - the trickle down argument has been around in some cohorts of economists (on the right of politics) for more than 50 years and probably longer.

2) The analysis is essentially rear vision mirror stuff from pre-COVID times. The current level of global QE is of a totally different quantum.

Keith W

1) The argument that supposed benefits of QE pass through to the lower deciles within the population is essentially a trickle down argument - the trickle down argument has been around in some cohorts of economists (on the right of politics) for more than 50 years and probably longer.

Exactlty:

In March 2017, former Treasury and Federal Reserve (Fed) official, Peter R. Fisher, delivered a speech at the Grant’s Interest Rate Observer Spring Conference entitled Undoing Extraordinary Monetary Policy.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1…

Correct Keith, but would like you to compare NZ country size, from population & economic point of view to the next door neighbour OZ. The speed and amount of QE magnitude. Which does really raise a question, apart from the other obvious 'knee jerks' measures such as OCR, LVR and the rest.

It is different quantum but the devil is in details.

Be more worried about why they’re doing it so quickly and so much, than the effects it’s having.

Ask yourself, what’s got them so scared? 300 PHD’s down there all got spooked over something.

At this juncture it might be judicious to introduce some old analysis in respect of central bank capture of economists.

Priceless: How The Federal Reserve Bought The Economics Profession

That describes the economics profession and why we should not take much notice of them. As economist Prof Bill Mitchell who after more than forty years in the profession describes economists as suffering from groupthink.

Groupthink is a phenomenon that occurs when a group of well-intentioned people makes irrational or non-optimal decisions spurred by the urge to conform or the belief that dissent is impossible. The problematic or premature consensus that is characteristic of groupthink may be fueled by a particular agenda—or it may be due to group members valuing harmony and coherence above critical thought.

https://www.psychologytoday.com/nz/basics/groupthink

treadlightly... yes and with our cancel CULTure movement moving full steam ahead this will only be exacerbated.

Surely with the length of time that QE has been running in some countries we should be able to measure some of these supposed effects. there should be no doubt now whether it creates inflation raises wages or any of these other beneficial effects that have been touted. But really the only measurable effects we seem to see is rising asset prices and rising inequality. Surely it's time to say hey you're not actually succeeding in getting the things you want from this action maybe it's time to stop.

Indeed: Future Stimulus Math

What a load of crock! PROOF that economists are either stupid/useless, or blatant QE supporter/liars.

The authors state this:

Here the paper notes the benefits are much more evenly distributed via income than the wealth effects were and, as a proportion of income, help the bottom half the most... This is driven by the fact that QE is estimated to have increased employment more at the bottom of the income distribution than the top. The aggregate result of this is that the macroeconomic effect will reduce, rather than increase, income inequality.

Yet, as noted on the graph above (i.e., the empirical 'proof' they provide for these claims): they state,

Income refers to net household income before housing costs

Do they think we're all stupid? Or do they think that as property/housing asset prices go through the roof, that landlords don't respond by increasing rents?

Certainly in the small sample I've modeled, rent price increases are averaging 13% above tenancy.govt.nz stats (based on bonds submitted in the past 6 months) and 23% above what is deemed affordable. That unaffordability shows households paying an average of $98/week more on rent than they can comfortably afford.

#rentcontrolnow (but you won't hear it from any orthodox economists)

I agree with u Kate, in regards to the findings of the report.. ( They should do a reort on the impact of the FIRE economy , on wealth inequality... https://www.scoop.co.nz/stories/HL1507/S00101/the-fire-economy-new-zeal… )

I disagree with u about rent controls... Have u pondered what the 2nd and 3rd higher order effect of rent controls might be..?

I'm not being critical of you, just asking a serious question.

I cant find anything that argues/shows that rent controls are a solution .. From what what I've read about rent controls,.. one of the higher order effects is that it reduces the private sector supply of rental homes, over time..

Price/Wage/Rent controls have been done often enuf in the past for one to see that the higher order effects are distortionary.

History shows that there is also a time and a place for such controls.... WW 2 was such a time...

Even germany , which has had a history of stable house prices and Rents , are having problems....

https://www.goethe.de/en/kul/mol/dos/liv/21251402.html#:~:text=In%20201….

Yes, I've read a lot about unintended consequences/higher order effects. Most rent controls are not applied universally (and many of the higher order consequences arise from this aspect of policy design) and the other main issue is what type of method (i.e., formula) is used to set rental prices.

My early modeling suggests provided NZ applies rent controls universally and uses RV as a basis for the rent control formula, higher order effects/unintended consequences are minimal. There still exists the question of how the new build market would respond to rent controls. Certainly, it seems the two-story townhouse type new build is presently the main build-to-let property coming on the market. However, my observation is that those properties are slow to let (based on price) and are aimed at a higher household income rental market - whereas our problems are with lower income households (i.e., those new and growing registrations for state housing places).

And even if private sector house building does slow as a result of rent controls - the government has the capacity to absorb all of those labour resources in its own house-building programme.

I'd suggest the Govt needs more than ..." the capacity to absorb".... sounds like an after thought.

A reduction of the pool of rental properties resulting from rent controls would be a serious disaster...

Govt would have to have the principal policy of creating an oversupply of houses and in partnership with that have rent controls as a medium term measure..

The possibility of rent controls reducing the number of available rentals should be a very serious concern..?? ( especially if the controls are brought in during a period of imbalance between supply/demand ).

When i consider higher order effects of policy... I ask the question.. "How will these rules be gamed? "

None of this addresses the question of affordable housing... ie. the cost of a new house. ( The irony is that it has been the unintended consequences of "controls/regulations" that have, largely, resulted in our current unaffordable housing situation )

This report has a short history of town planning controls , post ww2..

https://www.nzinitiative.org.nz/reports-and-media/reports/priced-out/do…

So the key higher order concern you have is a reduction in the number of private rental houses being available.

But the houses themselves don't disappear? They remain as dwellings in the overall national dwelling count. One would assume they would change from rental to owner-occupied - and government can introduce any number of policy incentives to get households into their own homes (i.e., rent-to-buy; conversion of private rental to state rental; public/private shared ownership; state loans at no interest for deposits, etc. etc.)

If rent controls increase the supply of houses available for sale in the market - that would have a cooling effect on prices.

Really, you are trying to argue at cross-purposes. We don't have a demand problem - we have a supply problem at the lower/affordable end of the housing/accommodation market.

PS thanks for the link - read it when it was first published. Same old, same old - that argument (planning is at fault) is the hamster wheel we need to get off.

Kate ...

Why is it that Govt has never aligned immigration policy with the ability to provide housing.?

Dont u think this sort of stuff should be sorted before rent controls..?

Post 2010, when we have had some of the lowest levels of home building while we have had some of the highest levels of immigration.

If govt cant deal with basic things like this.... how will they be able to intelligently match supply/demand imbalances in the housing/rental mkt..??

Dont u think this sort of stuff should be sorted before rent controls..?

No. Because rent controls are needed based on the loose and ill-conceived immigration policies of the past. They (unaffordable rents) are the consequence of those policies and we have to now live with them and house the population at an affordable level. Sure, plan for the future as well, but our reality now is that rent controls are desperately and urgently needed due to past policy.

We can't send the population that never should have entered in the first place (due to our infrastructure/housing capacity constraints) back to where they came from. Nor can we deny returning NZers to opportunity to return home. Nor can the state build its way out of the present crisis fast enough. The need for rent control is now.

#rentcontrolnow.

Lies, damn lies, economists statistics.

They are probably correct Kate. After all going from unemployment to a wage will most likely increase your income a large percentage. You'll still have none to spare but a overpaid economist isn't likely to understand that nor care.

The other thing is their analysis was dependant on QE ending causing a drop in asset price. So in current practice their analysis is null and void.

"Wage effect. Improved macroeconomic conditions lead to a tighter labour market, pushing up on wage growth."

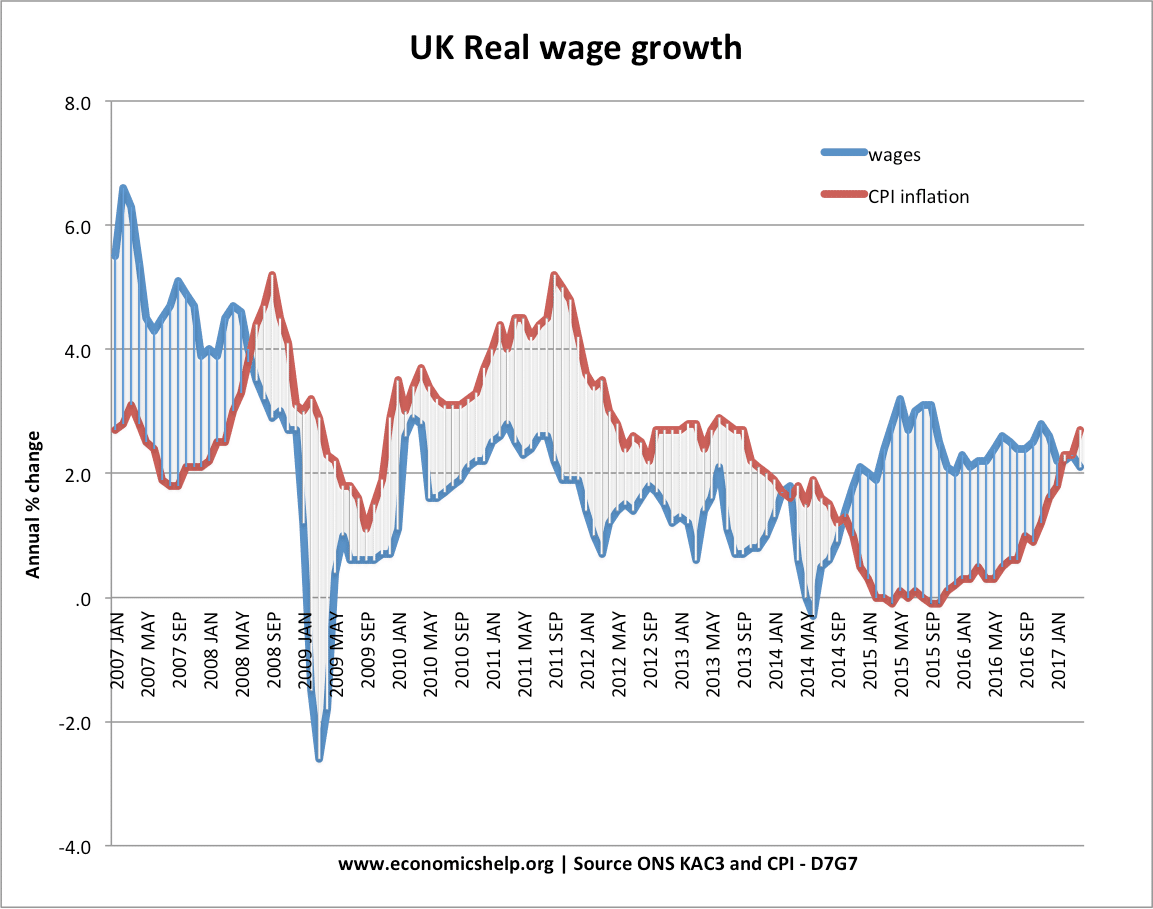

Total bulldust. https://www.economicshelp.org/wp-content/uploads/2015/10/uk-real-wags-0…

You will note the UK started QE in 2009. Look at the graph. Prior to the GFC wage growth was running well above inflation. QE started and wage growth dropped to well below inflation. QE stopped in the UK in 2012, a couple of years after, wage growth flipped over again to be more than inflation (which is logical to me, as things take a while to "shake out"). In 2016 they started QE again, guess what happened? Yep, wage growth fairly quickly fell below inflation.

{kind=link}

These idiots are trying all they can to make QE seem less damaging than it is in a horrendously bad attempt at trying to appease the masses.

You can see the same thing playing out in the US: https://www.epi.org/nominal-wage-tracker/

Only difference with the US is Trump did something intelligent, handed out QE to the masses, rather than just to the already wealthy. Hence the huge jumps in recent times (about to jump again with Biden's $2T hand out).

According to the article; Wealth Effects- Third on the list is Inflation Effect- QE raises the level of inflation.

Well, not as conventionally measured by reference to Consumer Price Indexes. On that measure, QE has had no effect on inflation.

I see posts from Keith Woodford and Audaxes which in effect accuse central banks of promoting the trickle down effect of QE. I agree with them and find it disturbing that the banks should be promoting a long discredited neo-liberal theory.

Agree - and of course it is not only the banks but the government as well.

QE is just a swap of notes that earn interest (bonds / gilts) for notes that do not earn interest (cash). There is sod all evidence that QE does anything to boost the economy or prevent deflation - QE is basically welfare for the rich with toxic side-effects including property / share price bubbles that then have to be kept inflated.

I suspect that QE is really just a mechanism to allow Govt-owned Banks to lend money to the Govt (that owns it) without either being open about what they're doing. Imagine if the public found out that the Government is not actually *fiscally* limited and that it does not have to go into 'debt' to pay for new infrastructure, houses, services, etc.

You will be declared a heretic on this site for saying things such as this, just as I have been. My advise don't mention MMT.

Nothing wrong with discussing mmt.

Maybe one becomes a heritc when mmt is preahed like it is some kind of truth that will solve our problems.

Of course its not..

Its a set of ideas that brings together money printing and fiscal policy, in the name of full employment.

Like most ....isms, mmt has some good ideas...

Just my view.

I think MMT is a really useful model for understanding macroeconomics and Govt finance. It is 'preached' far too often though. My criticism of mainstream economics is that it is a dangerous pseudo-science. I used to spend my days at work modelling the flow of sewage through pipes - it was literally complex shit. When I started to explore mainstream economic models I was disgusted with how poorly conceived they were - reducing the analysis of complex systems to a few simple equations with completely unrealistic underpinning assumptions. Absolute madness that these models are still used to inform Govt policy.

I enjoyed the ‘literally complex shit’ line. I am no practising econ, but there has to be a place for simplifying assumptions and models in policy analysis - so long as there’s a place for criticising those assumptions and models, too. As for MMT, it is probably maligned as much by those who misrepresent it in their preaching as those who throw stones at it from a distance. MMT is not a suite of policies to be rolled out as some panacea. It is rather a clearer lens from which to see the fiscal capability of a government with monetary sovereignty.

Don't be sore treadlightly, you aren't a heretic and I doubt anyone here thinks so. Your robust debates with others have been a pleasure to read as they present a non traditional theory of how things work which I am sure has triggered much thought in commentators (it has in me!).

Thanks for that. I don't do it for my own benefit, but how can we be content with where mainstream economics is taking this country. Things are so bad for so many people it does make me cross that it doesn't need to be like that. How can we have people in this country who cannot afford food and don't have a house to live in.

"...when QE is unwound..."

LOL that's a good one

QE is wounding and will not be easy to unwound. Even BoE thinks so. They should know, they have the Original QE there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.