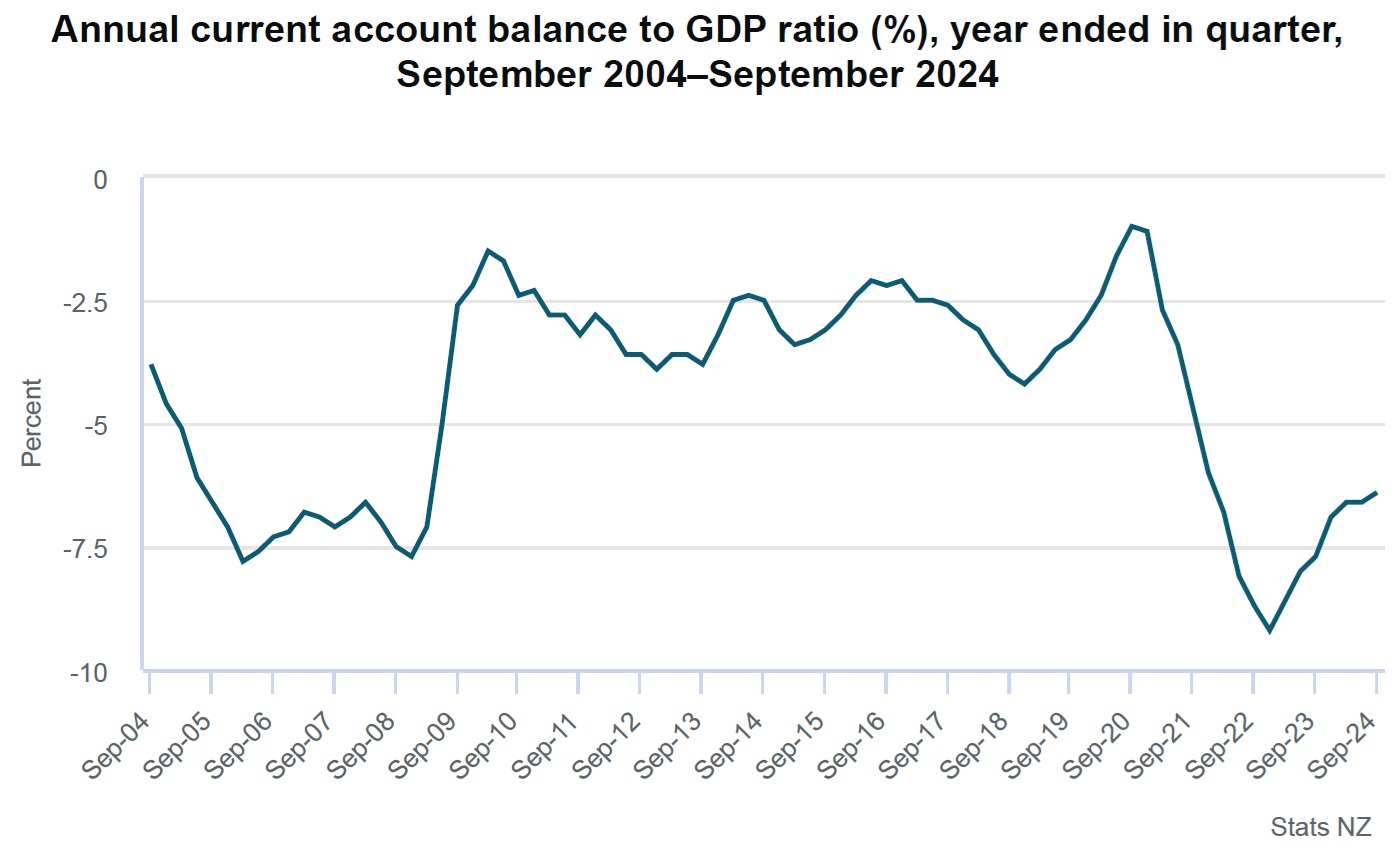

The deficit between what we earn overseas and what we spend as a country has narrowed - but still remains at a level described by economists as unsustainably wide.

Statistics NZ reports that in the 12 months to September our current account deficit was $27.0 billion, down from a revised $27.6 billion in the 12 months to June 2024.

Our deficit has therefore reduced to 6.4% of our GDP, down from 6.6% as of the June quarter.

Stats NZ said in the September 2024 quarter New Zealand’s seasonally adjusted current account deficit narrowed by $0.9 billion to $6.2 billion. The detail of this was:

- seasonally adjusted goods deficit narrowed to $1.9 billion

- seasonally adjusted services deficit narrowed to $397 million

- primary income deficit narrowed to $3.5 billion

- financial account recorded a net inflow of $2.1 billion.

The seasonally adjusted goods deficit narrowed by $0.7 billion to $1.9 billion, driven by a $0.8 billion fall in goods imports.

"In the September 2024 quarter, New Zealand imported fewer cars than last quarter. Also contributing to the fall was transport equipment imports with no defence aircraft imported, which were recorded in the June 2024 quarter," Stats NZ's international accounts spokesperson Viki Ward said.

"There was a higher volume of petrol imports in this quarter."

Goods exports decreased by $0.1 billion, driven by meat and casein.

While economists are expecting that our current account deficit will gradually shrink over time, the extent to which we are spending more than we earn in the world has attracted the attention of credit rating agencies, who have previously stressed that they want to see that deficit coming down or else it could cause our sovereign debt ratings to come under review.

The deficit hit a peak of 9.2% of GDP in 2022 and has been falling slowly since.

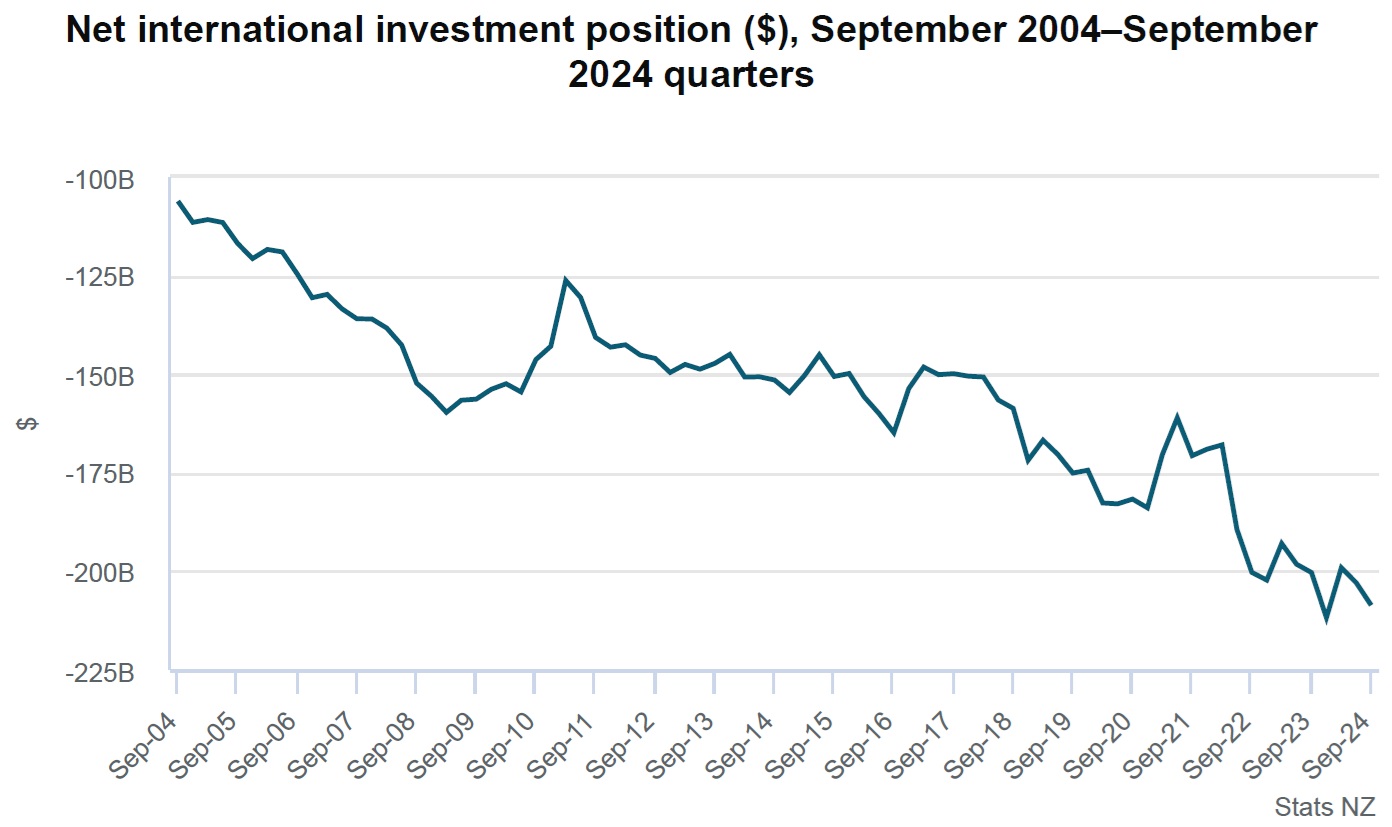

In terms of New Zealand 'net international investment' position - representing the difference between New Zealand’s financial assets and liabilities with the rest of the world - we continue to have a 'net liability position'.

At 30 September 2024, New Zealand’s net international investment liability position was $208.6 billion (49.5% of GDP), $5.7 billion wider than $202.9 billion (48.3% of GDP) as at 30 June 2024.

The widening of the net international investment liability position reflected New Zealand’s international liabilities increasing more than its assets.

In the September 2024 quarter, we borrowed more from overseas than we acquired in overseas financial assets.

"Increases in share prices along with borrowing from and lending to overseas largely contributed to New Zealand’s international liabilities reaching $613 billion, and assets reaching $405 billion, which were new highs," Ward said.

14 Comments

You can really see the affect of Covid. But why no recovery? Still no tourism?

I wonder how much closing Marsden Point will affect it going forward? Importing high cost refined fuel rather than cheaper crude oil

If that is the reason, surely the government would have known and stepped in.

.....you mean the net zero at all costs government?

Wow. A perfect example of 'reckons' - all leading to a non-answer and political bias in just 3 posts.

An interest.co.nz record?

Musk, eat your heart out. We can do better than "X".

"But why no recovery? Still no tourism?"

Seriously, Jimbo? Do you not read any news from overseas?

There hasnt been any good economic news for NZ Inc. that i can think of for quite some time

Just the increase in dairy payout for dairy famers that will flow though to the rest of the economy.

Step one is to get BOGS positive, that may come in time as our currency continues to be trashed.

Yes. It's one of the most pressing issues we have, yet very few comments here.

27 billion pa spending more than we earn is $100 per week for every man woman and child. The day of reckoning will come and it will be brutal.

Most Kiwis are naive enough to believe that more public infrastructure spending, lower interest rates or some other domestic policy lever can resuscitate our economy. In practice though, we can only export our way out of this mess. The current account balance is a lagging indicator of a nation's economic competitiveness.

If I were Luxon or Willis, I'd be very worried about the ongoing brain drain and how that could further trash our export sectors. Instead, they appear to be doubling down on unskilled immigration, which is the equivalent of pushing down on the accelerator minutes before the car is about to hit a brick wall.

Brain drain daughter arrived in NZ for xmas. The state and presentation of the populace shocked her within hours of landing. Loves NZ, sad for it and but won't be living here.

hi Beanie,

I have been pointing out that our currency will fall to accommodate the imported lifestyles our 'wealthy' demand for ages.

A falling currency is the 'release valve'. It has to get used. There is no other way.

Well, there is another way. I'll not bore everyone with yet more commonsense. I've done enough of that already.

Maybe if Kiwi 'investors' stopped borrowing money from overseas to buy low-returning, already built 'assets' we'd be a lot better off?

Maybe if Kiwis voted for a government that furthered our enormous & largely untapped ability to produce renewable energy - rather than importing it - we'd be a lot better off?

But no. Kiwis don't vote for this. They want tax cuts that others - including their children - will pay for.

Our problems start at home.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.