This week's Quarterly Survey of Business Opinion (QSBO) from the New Zealand Institute of Economic Research made for sober reading.

The bit that really jumped out at me was this;

A net 25% of firms reduced their headcount during the quarter, the highest proportion since the Global Financial Crisis in 2007, and another 10% expect to lay off staff next quarter.

The volume of companies saying they're laying off staff suggests unemployment's rising, possibly significantly. The last official Statistics NZ reading showed an unemployment rate of 4.3%, or 134,000 people, as of March. The June quarter data will be out on August 7.

The QSBO has been running since 1961 and is described as New Zealand’s longest-running business opinion survey, querying about 4,300 firms quarterly.

Here's a cross section of other indicators suggesting the economy's in a tailspin.

Credit bureau Centrix says company liquidations in May were the highest for a May month in a decade. The value of new residential building construction work consented fell $3.3 billion in the year to May as the average asking price of homes listed for sale falls and the volume of properties listed for sale rises. And retail spending fell for a fourth consecutive month in May.

Meanwhile, the Reserve Bank (RBNZ) next reviews monetary policy next week, July 10. So what chance it lowers the Official Cash Rate (OCR) from 5.50% where it has been since May 2023? Or even hints a reduction is coming soon?

Not great.

Since inflation surged from 2021, with Consumers Price Index (CPI) inflation peaking at 7.3% - its highest level in 30+ years - in June 2022, the inflation fighting RBNZ has been under siege.

That's because its monetary policy mandate tasks the RBNZ with keeping annual CPI inflation between 1% and 3% over the medium term, with a focus on keeping future inflation near the 2% mid-point.

For the March year Statistics NZ had the CPI at 4%, down from 4.7% in December. The June year CPI will be out on July 17, which the RBNZ expects to weigh in at 3.6%. The CPI measures changes in the prices paid by households for goods and services.

This trend of falling inflation and a starkly weakening economy might suggest the RBNZ can take its foot off the monetary policy pedal. BNZ Head of Research Stephen Toplis, is certainly of this view. Following the QSBO he published a note headlined; ‘QSBO says inflation beaten,’ adding;

“In our humble opinion, today's NZIER Quarterly Survey of Business Opinion screams: cut rates sooner rather than later.”

However, taking the RBNZ's musings on inflation literally, it wants to see the whites of 2% inflation's eyes before any OCR cut is made. The RBNZ hierarchy has also been striving hard to avoid signalling an OCR cut is around the corner, to avoid precipitating a pick-up in economic activity, potentially adding petrol to the inflation flame. The RBNZ doesn't want egg on its face.

Witness the recent speech from RBNZ Chief Economist Paul Conway. Its title was The road back to 2% inflation. That follows one from Governor Adrian Orr in February with the title The Monetary Policy Remit and 2% inflation. Orr said;

The Reserve Bank believes that the current 2% mid-point inflation target remains appropriate for New Zealand.

“2% continues to strike the right balance between the costs and benefits of inflation,” Mr Orr says. “A focus on 2% appears to be consistent with an ‘optimal’ level of inflation.”

“In the long-term, an inflation target centred on 2% is more likely to mean continued growth and steady jobs, supporting the prosperity and wellbeing of everyone,” he says.

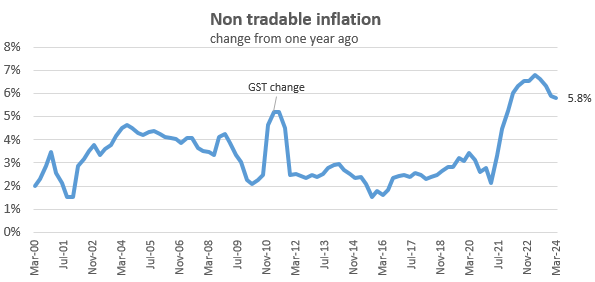

The non-tradable dilemma

The big CPI inflation challenge for some time now has been what's known as non-tradable inflation. This is the changes in prices for goods and services less exposed to international competition and more influenced by domestic factors. Think insurance costs, local government rates, rents, construction costs, and cigarette and tobacco inflation.

March year CPI inflation had tradable inflation, featuring imported goods such as petrol, down to 1.6%, with non-tradeable inflation at 5.8%.

But to what extent can the RBNZ even influence the prices of insurance, council rates and rents? Toplis is a sceptic, saying in January;

...non-tradables inflation is almost always higher than 2.0%. Since 2000 non-tradables inflation has averaged 3.3%. In the 95 quarters across this period annual non-tradables inflation has been 2.0% or below just six times. Four of those six quarters ended up sub 2.0% because of a big reduction in ACC levies that 'artificially' depressed the reading by around 0.6%."

"Given what is currently driving non-tradables inflation, it is highly unlikely monetary policy will be able to get it anywhere near 2.0% in the foreseeable future."

So what does the RBNZ itself say?

In a press conference after the RBNZ's February Monetary Policy Statement Orr said;

The Consumer Price Index is made up of many, many components. Once you start climbing down into the components monetary policy really doesn't impact any of them. It impacts indirectly the components of the CPI via spending, demand and supply. That's how it impacts on it...we do not set local authority rates, we do not set prices. We set the price of money which then determines over time willingness for people to hold it or not, spend or save, so it's that second round indirect impact.

As we get to the lower inflation parts there are some really persistent and challenging parts of that inflation picture and it just means that we may have to work harder to achieve the same outcome. But I would say it's no different to any other period.

The hardest component for us to manage is productivity. Low productivity means low nominal GDP growth before you get inflation pressures rising so if we had a higher productivity economy we would be able to deal with these relative prices much easier. But again that's in the hands of businesspeople, consumers, investors, government policy. We just control the price of money.

The chart below shows the rise and fall of non-tradable inflation since the start of this century.

'Inflation in these components will not peak until the third quarter'

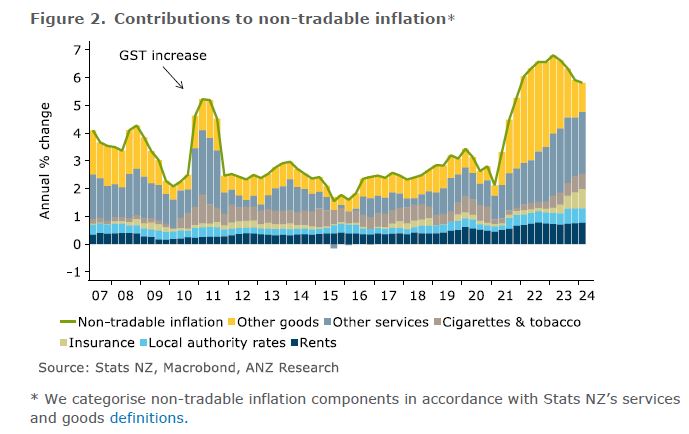

ANZ New Zealand economists Henry Russell and Sharon Zollner last month issued a helpful note, Non-tradable disinflation: a waiting game. They dig into insurance costs, local authority rates, cigarettes and tobacco inflation and rent inflation. Russell and Zollner note collectively the four account for 2.5 percentage points, or 44%, of the current annual non-tradable inflation of 5.8%. That has them punching well above their collective weight of less than a third of the non-tradable basket.

Russell and Zollner say;

"And on our forecasts, while other sources of non-tradable inflation retreat, inflation in these components will not peak until the third quarter. At that point it will be responsible for around 2.7 percentage points, or 54%, of total non-tradable inflation."

They add another recently emerged example of inflation persistence stems from the Commerce Commission announcing its draft decision to increase revenue limits for Transpower and local electricity distributors from the March quarter next year.

"The new revenue limits would result in an average annual increase of $180, +GST, to household power bills, adding roughly 0.25 percentage points to annual headline inflation and 0.45 percentage points to non-tradable inflation, all else equal."

The ANZ economists also note;

Since the initial inflation surge from March 2021, the cost of building a new home as measured in the CPI has increased around 36%. Dwelling insurance as measured in the CPI has increase by around 40% over the same period.

How about vehicle insurance? Since March 2021, vehicle insurance costs are up nearly 31%. Over the same period, vehicle prices have risen 7.3%, vehicle parts and accessories have risen 26%, and vehicle servicing and repairs have risen 18.8%.

The chart below, showing the contributors to non-tradable inflation, comes from ANZ.

'King Canute'

Russell and Zollner say, in a glass-half-full view;

"This baked-in persistence (the impact of which is exacerbated by the unusual highs seen in CPI inflation), is very likely one of the reasons why monetary policy lags are proving longer this cycle."

"That’s preferable to the alternative explanation: that monetary policy isn’t working, either because of a change in the transmission mechanism or because the speed limit for the economy is lower than previously envisaged, as the RBNZ concluded in the May Monetary Policy Statement. That implies more pain is required, whereas this explanation implies that we just have to be patient."

The extent to which monetary policy impacts the likes of insurance, rates, rent and household power bills is highly debatable. In the words of Orr above it has an indirect impact. Insurance premiums are set by insurers facing rising costs from extreme weather and reinsurers, and whose shareholders want good returns. Rates are set by financially challenged councils, rents are determined within a broken housing market, and the Commerce Commission is allowing power bill increases to help fund needed network investment.

Speaking to Auckland University's Tim Hazledine last year, he questioned whether "King Canute in the Reserve Bank" had anything to do with falling inflation. Hazledine also offered a series of suggestions to help the RBNZ tackle inflation including; expanding the Commerce Commission's mandate so it becomes a price watch commission, holding tripartite pay talks between the Government, unions and employer groups, exploring an extension of the Pharmac model to source other products and services at lower prices from international suppliers, and reducing GST to 10% from 15%.

Meanwhile, Kiwibank's Jarrod Kerr has queried the ongoing feasibility of the 2% target. Kerr notes more extreme weather events, moves to decarbonise the economy, improving struggling or failing infrastructure, wars and geo-political tensions are all inflationary.

One thing is for sure. Debate will continue over the RBNZ's wielding of monetary policy and the impact of the central bank's blunt OCR tool. Especially if the economy continues weakening, the OCR is held at its current level, and non-tradable inflation remains stubbornly high.

In this scenario questions need to be asked as to whether current monetary policy settings, dating from the 1980s, are fit to serve New Zealanders today and their 21st century challenges.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

38 Comments

Great article

and reducing GST to 10% from 15%.

Yes, certainly the most promising and assured way to reduce non-tradeable inflation.

But government ideology regarding the introduction of capital/land taxes will put paid to any consideration of that.

Our broken tax system - broken for years and years and years - will continue to punish everyday workers.

On a less, or secondary action, the government could reduce the punitive taxes on tobacco products - again to the same end of reducing non-tradeable inflation. But, the tax income has become critical - often 'saving' the day in terms of flailing government revenues.

As unemployment creeps up, PAYE will reduce as well.

What is it about governments that refuse to address the things they do to exacerbate our decline?

Nice work Gareth.

Seems crystal clear now that monetary policy is not working. Yes, higher rates are crashing the economy, killing jobs etc... but the transmission through to moderating prices is not happening. Why?

If insurance companies want to restore profitability, they just can increase premiums. If local Govt needs to increase rates to tackle infra backlogs, pay higher debt-servicing costs, they just can increase rates. If wholesalers with market power want to restore profitability off the back of lower import costs, they just can. If lower demand affects profits, the big price-setting firms just can buy less stuff to sell, lay off staff, and maintain their prices / margins.

Add all of the above onto the basic fact that businesses are now paying $9bn per year more in interest than they were in 2022 - that's more than 4% of total household consumption expenditure. Did businesses have that money saved up somewhere for a rainy day, or might they be recovering those costs from their customers - you know, by charging higher prices?!?

My firm view now is that our uncompetitive markets mean that monetary policy is now pushing prices up more than the crash in demand is pulling them down. How far will we have to crash demand to reverse that?

I would understand if RBNZ just came out and said, 'sorry, we can't adjust rates despite things turning to custard because our currency would collapse'. But, I think they genuinely believe that what they are doing will reduce prices. But, then they have to - their whole existence is based on everyone believing that monetary policy works. It's crazy.

I'll end with a scary chart - a reminder that NZ is especially committed to causing a deep and painful recession. Our combination of high private debt levels (140%) and a relatively high interest rate (5.5%) means that the impact of monetary policy is way more fierce in NZ than anywhere else across the OECD. Only the US and Iceland have a similar combo - and US mortgages are protected by 30-year fixed rates, and the average house price in Iceland is $400k (less than half NZ).

Indeed, a scary chart.

Regarding the scary chart - perhaps if we didn’t allow our private debt to spike to 140% of GDP in the first place then we wouldn’t find ourselves in such a financially vulnerable position - hence my at times repetitive warnings about the hole we were digging ourselves (while being abused as a doom gloom merchant by those who were profiteering at the expense of the financial and social stability of the nation as a whole).

We’ve made our bed with financial ignorance, time to sleep in it. When you get to the position we’ve allowed ourselves to be in, there is no way out without significant pain somewhere in the economy - act like fools and reap the rewards of that behaviour (monetary policy, immigration, tax policy etc).

I agree. Although it is worth pointing out that the mistake was made over a 20 year period from 1989 when we powered our economy on credit money. Basically, NZ developed a massive crush on monetary policy, a fetish for Govt budget surpluses (enabled by private debt explosion), and a passion for selling off assets to rentiers. So, here we are.

Spot on. Both of you. And the overwhelming sentiment? "there is no way out without significant pain somewhere in the economy"

Agreed. NZ has run trade/current account deficits for many years now. If we're going to run low public debt under that scenario, then the private sector (which turns out to be mainly households) has to carry the debt that funds our ability to spend more than we earn.

It's amusing watching finance ministers of the past boasting about their fabulous balance sheet while households were continuing to tick up the necessary debt on their behalf. An irrelevant detail it seems.

Exactly this. Please feel free to work for treasury or rbnz!

The problem is that energy efficiencies are well on the way to flat-lining, and the cost of energy (albeit once-removed as in Transpower maintenance) is rising in real ECOE terms. And a lot of things are becoming scarcer, or harder to get.

So inflation wont ever go away, in fact it will inexorably increase.

And pushing on a piece of limp spaghetti, won't etc. etc...

Too much debt? Does that mean I have to sell the new Ranger, the high-end mountain bike and the jet-ski, and also cancel the house renovations and the four-week overseas holiday?

The other part of the dilemma is how the currency markets value the NZD if the RBNZ moves ahead of the Fed.

This Could Force the Fed to Cut Rates in July

Fed officials have repeatedly stated they are going to be patient before pivoting to rate cuts. But that would only be the case if the economy is actually strong and resilient. Should the labor market show signs of falling off dramatically, they'd cut their rates in a hurry. Today's macro data were filled with exactly those kinds of warning signs.

Theyve ignored the warning signs to date...as Snider frequently notes they are reactive after the event....and we are further ahead in the cycle than the US.

Regarding US employment:

‘This is an ominous sign

The unemployment rate has moved above its 36-month MA

Such a development has happened 10 prior times since 1952

Every single time, it ended in a recession

This time is NOT different’

https://x.com/gameoftrades_/status/1808853453776826855?s=46&t=MUwQeKa7M…

Similar result as inverted yield curve. Nz just experienced a double dip recession

The longer it takes to get non tradeable down to around 3% the bigger the economic mess will be. I'm interested to see what the RB does if non tradables stays high while unemployment sails past their forecast 5%.

A very real possibility at this point.

A guarantee at this point I'm afraid. The rapid increases in unemployment we are seeing now are the result of rate rises in early 2023. Monetary policy takes as long to 'work' on the downs as it does on the ups.

Some more data from the US re: inflation.

‘US consumers' average 5-10 year inflation expectations have spiked to 5.6%, the highest in 31 years.

This measure increased by ~2 percentage points in just a few months.

By comparison, median inflation expectations are around 3%, in-line with the readings seen over the last 3 years.

Meanwhile, CPI inflation has been above 3% for 38 consecutive months, the longest streak since the 1990s.

Inflation is still a major issue’

https://x.com/kobeissiletter/status/1808472776962924857?s=46&t=MUwQeKa7…

Hence why the 10 year treasury remains above %4.00

MikeM if the headline number is within range & we’ve got unemployment continuing to climb & the NZ economy tanking will Governor Orr just hang it all on the non tradeable number 😬

Surely annual CPI within target range is the goal…but, if I’m at the tote placing a punt…I’m putting it all on them absolutely f**king this up spectacularly 😂

Guess I won’t find that as funny when I’m picking my favourite bridge to live under though eh 🤦🏻♂️

I’ll be trolling it with you under the bridge when the one trick pony is still performing with no audience

The RBNZ in my view can have no impact on non Tradable inflation, if I am wrong please explain.

The current inexperienced govt continues to muddle around with silly little topics such as the non existent problem of potholes yet fundamental obsolete sectors such as council rates, banking, insurance, electricity need a change

Rates should be paid by central govt it’s only $14b per year that can be funded easily by consolidating all councils into one govt ministry saving $billions on multiple council costs, put company tax rate back to 33% & greater profits & gst revenue due to no rates paid by the populace, cut back the pointless military spending and voila councils & rates are paid & managed by central govt similar to education & health depts, no more dopey little council operators chasing up rates

Non tradeable inflation is a govt problem, not the RBNZ, and successive govts have failed to act:

a) local govt could be forced to put spending through socioeconomic cost / benefit assessments that are made publicly available in annual and 10-year plans, before local govt commits to any of the spending. This would force local govt to stop spending on low value vanity projects and force the spending towards projects with high returns. With more effectively directed spending the total spend should also moderate.

Also, most local govt areas are too small and many uneconomic. Amalgamation (mergers) would reduce the overhead and help keep costs down.

Furthermore, central govt should start paying rates on all crown land.

(Aside: interesting we add local govt rates into the CPI when they are a tax, but central govt taxes aren't in the CPI.)

b) the NZ insurance market is now a lot more concentrated. Central govt and ComCom need to address this.

c) construction costs (I presume excl land) - more competition in building supplies needed. Govt has moved a bit in this area.

Also, we build houses 1 by 1, each individually tailored which adds massively to the costs with no economies of scale. Away from NZ I've seen whole new subdivisions are made up of 4 or 5 standard designs only, and that's it. We would need some large companies with the capital to do this. We would also need much lower land prices so less capital is tied up buying it for development.

Good comment.

Councils are responsible for providing 25% of NZ's public services and infrastructure but earn less than 10% of total net government revenue.

The Lakes district Council is a great example where the tourism boom brings in billions for the central government but has left the local council more indebted than ever.

God help us, listen to Kerr ‘the current CPI is to low’ he and his follow bankers are the main problem, they got us here. The current OCR isn’t even high. Leave it as it is! Let the economy find its feet, sure there will be abit of pain (correction from the artificial drug induced high) but it’s what we need now.

That’s an ace idea alright

I think the basic problem here is that we allow us to be ripped off! By the gentailers who are making a 2.7B$ profit and leave any investment in the grid to be paid by the customers i.e everybody has to pay $180 more next year. By our supermarket duopoly; by our (Australian owned) insurers (Let me give you an example: I still own a property in The Netherlands and as most of you know most of it lies below sea level. My insurance premium overthere went up by 3.4% in 2022 and 4.1% in 2023) and there are many more who are ripping NZ off.

Maybe we should allways set the OCR to the non-tradable inflation. It would force us to seek solutions to our high non-tradable inflation and very inefficient markets and economical policies.

We might well see it as very positive that tradable inflation has subsided so rapidly which has allowed RBNZ some breathing room post-pandemic to "wait and see." This situation could have been much worse had commodities, manufactured good etc. not normalised.

I think RBNZ should raise acknowledging that under 2% they'll trim again. Give the market some general guidance regardless of forecasting.

How about we force the councils to fully open their books and become more efficient?

Clearly their costs are on a major increase.

More money is coming in due to more ratepayers with new infill housing yet they persist in their woke spending.

Surely one big cost to the nation could be slashed with a complete overhaul of health and safety of roading projects. The number of road cones, rented back to us by consulting businesses, is a massive, massive rort.

and reducing GST to 10% from 15%.

Once a tax is in and the price has increased, removing the tax does nothing. The market can pay it so the pricing will remain.

The price may drop for a week or two to highlight the decrease. But slowly and surely it will climb back up. Only difference is the govt tax take drops and private profitability increases.

Why does the rbnz wait so long after a CPI release to announce the OCR

It doesn’t. Only seems like a long time if you are getting desperate.

What I find really interesting is that ANZ jawbones more than RBNZ when it comes to claiming that the OCR can stay high well into the future. If you want an impartial assessment, don’t go to ANZ. They are analogous to CNN, trotting out the official narrative despite the evidence.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.