New Zealand's inflation rate is still expected to fall below 3% by year end, but persistently high shipping costs provide "some upside risk", ASB economists say.

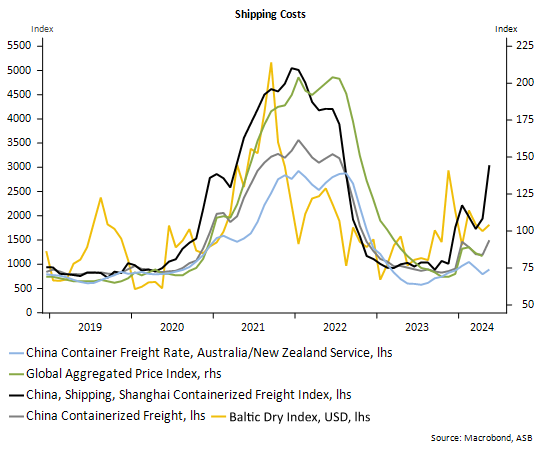

In a note on shipping costs, ASB senior economist Mark Smith says the run up in shipping costs has been swift – with a trebling in some rates in recent months.

Smith says unlike the surge in shipping costs during the pandemic, the latest rise appears to have been predominantly supply-driven. Current drivers include shipping disruptions in the Red Sea (Gaza conflict related) and Panama Canal (low water levels).

"The impact of higher shipping rates will depend on how persistent the uplift in shipping costs is - the longer that shipping rates remain elevated, the greater the potential impacts are. There is considerable uncertainty over how long shipping rates will hold up for, as this will depend on how tensions in the Middle East play out," Smith says.

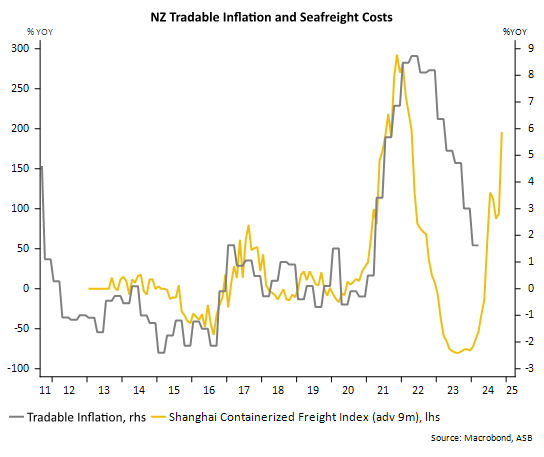

Smith says there is a lag of about six-to-nine months to retail prices in NZ, but the relationship is not exact.

"If shipping costs hold up, the concern is that this could boost tradable goods prices in NZ, reducing the likelihood of annual CPI inflation falling below 3% by year end. This could delay RBNZ [Reserve Bank] rate cuts," Smith says.

After inflation began to soar in 2021 the RBNZ reacted by forcing the Official Cash Rate up from just 0.25% to 5.5%, where it is now. This has led to higher mortgages and subsequently reduced spending and a significantly dampened economy. The RBNZ aims for inflation within a 1% to 3% range. As measured by the Consumers Price Index (CPI), inflation was 4% for the March quarter. The RBNZ is forecasting that CPI inflation will be 2.9% by the end of 2024.

Smith says there are good reasons to expect "a considerably more modest inflation impact" in New Zealand from the latest shipping cost rises than during the pandemic rises.

"Freight is only one of the costs impacting consumer prices and firm profitability. Labour cost pressures (which usually constitute a larger portion of firm costs] look to be cooling.

"Our view is that the price and cost impacts from higher shipping rates will be considerably more isolated than in the 2021/22 episode and will not drive a generalised rise in inflation that the RBNZ will have to offset with tight monetary settings."

Smith still expects annual NZ CPI inflation to fall below 3% by year end, but concedes that persistently high shipping costs provide "some upside risk".

However, weak retail demand in New Zealand and the likelihood that retail inventory levels are high will mitigate the short-term impacts on NZ economic activity and inflation.

"There is limited scope for NZ firms to push through cost increases onto beleagured consumers, with high consumer resistance to accepting higher retail prices.

"Firms look to be under extreme margin pressure. Cost cutting in other areas and efforts to drive greater efficiencies (rather than price rises) could result as margins are rebuilt.

"Labour incomes are expected to be under pressure (job cuts and modest wage rises could be the result as firm’s trim costs).

"In other words, higher shipping costs are an adverse cost shock that will further crimp NZ and global household demand, one way or another.

"This will eventually weigh on NZ core inflation. The next move in the OCR will be down," Smith says.

6 Comments

Made a list of what new durable goods we need for the rest of 2024.

Here it is:

If you have the cash on hand buy everything you need now before South China sea lanes are shut down

Let's say I rely on $1000 of stuff per week. $300 of that stuff is bought from other countries by wholesalers. Wholesalers have costs and a margin to make for their owners, so they sell their stuff to the retailers that I buy from - who add another mark-up to cover their costs and margin. Let's say that operating costs and margins for those wholesalers and retailers are broadly stable (which they are).

So, when wholesalers pay an extra 10% for the stuff they buy from other countries, what happens? Basically, I end up paying $330 for the stuff that used to cost me $300. So, my total costs go up by $30 to $1030 per week - a 3% increase on my total shopping basket. This is basically what happened in 2021/22, although import costs, which make-up one-third of our consumption, went up 27%!

So, what do I do hen prices rise? Maybe I compromise on some of my domestic spending - meals out etc, and spend a bit less on that more expensive imported stuff. Does the price of that imported stuff go down because demand falls 10%? Nope, the wholesaler just orders less of it.

Now, step back and think about what happens as the impact of those higher priced imports flow through the economy... companies pay more for their imported input goods, and charge more for their output goods. So, the price of domestically produced goods increases too. Workers then push for higher wages so that they can afford to live and eat - this moderately increases input costs and therefore prices too. Price rises basically propogate through the economy and will - without intervention - find a new absolute and relative level. Less will be spent on the discretionary things that have gone up in price or become unaffordable, more will be spent on non-discretionary things. Businesses will adjust, supply chains too etc etc.... and on we go. Until import costs com down again of course and then we will see another period of adjustment. Think about when we introduced / increased GST - look what happened afterwards.

Now add in to this simple self-levelling world the mighty RBNZ. They look at prices going up and decide that the answer is to increase business debt servicing costs and increase my $300 per week mortgage costs to $450 per week. Now I can buy even less stuff. Eventually, after 12 - 18 months of people getting poorer and poorer, enough people are poor enough to forego enough consumption that businesses without market power go bust, and thousands of jobs are lost. Now, finally, staff can be hired very cheaply, and prices rises moderate! Well, no, staff make-up around 10% of the costs of our huge wholesale and retail industry, and wages are pegged around the minimum wage. Moderating wage demands make sod all difference to the price of most of what we buy. While RBNZ have been reeking havoc, prices have been doing pretty much what they would have done without any intervention.

And that" $300 per week mortgage costs to $450 per week". What are you (second person, plural) going to do to mitigate that? I'll tell you. Roll your Debt exposure as short as possible and pray for a cut in the OCR to flow though to your future mortgage rate. Right? And those who have spare liquidity to lend out - what are they doing at the moment? Lending it out for as long as possible, for the same reason - any OCR cut will eat into future returns. And what if that is exactly the mirror image of what we should all be doing? What if we should all be borrowing long and lending short, because as you seem to be suggesting, much of 'what's coming' is not under the control of the RBNZ - it's external factors that are going to determine where our economy goes, not domestic. And under that scenario, the RBNZ is today trying it's best to 'get us ready' for what most see as improbable, if not impossible; a looming global rise in interest rates.

Problem is that dropping interest rates also causes another impact happening very visibly in Japan atm: currency depreciation. Any substantial difference between our interest rates and the USD will lead to similar issues around much more expensive imports.

Japan at least has a few more things to export than we do so the weaker yen helps them compete with China on this front. But in NZ we aren't quite so lucky.

The JPYUSD exchange rate is the most important macroeconomic indicator in the world today. The real problem NZ, Japan, and many if not most other countries are facing is that a truly insane amount of debt has been built up in the system after more than a decade of too low interest rates. This is on both the government side, business side, and household side. It just varies on the exact split by country. This absurd amount of debt (that makes debt levels during the GFC look like chump change) is now coming back to bite us as we seem to be in a far more inflationary global environment for a number of reasons.

Keep an eye on crypto. Whether you believe crypto is the future, a joke, or a scam, the crypto market is a great indicator to let you know how much liquidity is sloshing through the system still looking for a home. If the crypto market keeps going up we know that money is being created somewhere in the system. And at a time when most countries are trying to get a handle on inflation, the fact money is still being created somewhere is a strong indicator that it is only being done because the Fed feels it has no other choice.

The article is a bit misleading. Inbound rates to New Zealand have certainly not tripled in the last few months.

The blue line on the graph which is for AU and NZ combined ex China does show an uptick. Rates to Australia are higher than to NZ at the moment due to their demand for imported goods being above our anemic levels. From Jan to Jul the rate for a 40' container from main China ports to main NZ ports has increased 45%. The increase is mainly driven by the stronger demand for imported goods in Europe, Americas and Africa. Shipping rates from China to those countries have increased rapidly. But NZ importers are still only paying around a quarter of what they were paying during the covid peak. New Zealand just has to pay more now to justify the shipping lines continuing to allocate vessels and equipment to our trade lanes. If week demand continues they will reduce the vessel sizes on our trade. But this will have a flow on effect for exporters trying to get containers and space for their shipments out from NZ on those same vessels.

In short, 70% of New Zealanders have shut their wallets. The banks or the landlord get paid first and we try and live on the rest. You cant get blood from a stone.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.