By David Chaston

Earlier this morning, jobs numbers out of the US came in higher than markets were expecting.

The US non-farm payrolls report showed that there were 280,000 more people employed in May than April. Data for February and March were revised higher, data for April was revised down by a tiny bit.

The American unemployment rate ticked higher to 5.5% as more people were encouraged back into the labour force. Their participation rate - anemic by New Zealand standards - ticked higher to 62.9%.

The proportion of the working age population that is employed, which some economists consider a bellwether of how the economy is performing, rose to 59.4%. It is the highest point since the US recovery began six years ago.

But most importantly, wage growth rose and is now +2.3% higher than in the same month a year ago. It was up +0.3% month-on-month. Both measures were above market expectations.

This data has implications for New Zealand.

Firstly, the giant US economy is the engine of the world economy and consumer trends there drive investment decisions everywhere. Expanding employment shows that the weather and strike reduced first quarter result is an aberration.

Secondly, the US Fed will no doubt see this data as supportive for a rate hike when they meet on Thursday, June 18.

Today, an influential Fed spokesperson said that ending balance sheet reinvestment would be tightening and they want to get rates above zero before ending reinvestment.

The same spokesperson essentially dismissed the IMF's recent call to delay raising rates. But he also said the rise in employment and wages might be because they are going through a poor patch with productivity; that is, more people are being employed than output can sustain in the intermediate term.

A rising US official interest rate will give the RBNZ some cover to hold rates here and possibly turn the recent economist chatter around to be thinking about the potential for higher rates here too at some point.

Rising rates will have a 'brutal' impact on the value of bonds, and bond losses in investment portfolios will become more likely. That could extend the rush to equity investment. Higher yields and interest rates will work to restrain asset values, and that includes in the property sector.

Thirdly, the US dollar rose on the news. That means that the New Zealand dollar fell against the greenback. The NZD closed today in New York at 70.4 USc, its lowest level since mid 2010.

It was over 88 USc less than a year ago.

A fast retrenchment in the value of the New Zealand dollar will raise inflation in the tradable sector and cease to counter the higher price rises we have regularly seen in the non-tradables sector. A turnaround in inflation could come quite quickly if our dollar stays down or goes even lower. The problem for the RBNZ is that they may react too late to restrain a rapidly rising price level.

But rising inflation and a 'house price problem' can both be addressed with monetary policy by raising the official interest rate. That would also be more palatable given the underlying economy is performing strongly at present.

But banks and their economists won't like it. And neither would 'property investors' which these days seems to be everyone who owns a house. So the usual chorus will rise to oppose even the suggestion. The loudest voices will want the unsustainable party to continue. RBNZ policy makers however seem to be the types who can look through the self-interest expressed in the media and have shown some clearer signs recently that they are prepared to take on the banks even if it is pretty tentative.

Cheap money distorts most economic decisions, both public ones and even more pronounced, private ones. Those distortions are everywhere you look and especially in Auckland.

More expensive money will be hard on some businesses important to New Zealand. That is especially true of dairying and recent dairy conversion. The recent fall in prices is bringing stress to such enterprises. But the bald truth is that over-borrowing for farming is never a good idea given the commodity cycles they go through. So a cleanout is coming and keeping the cost of money cheap to minimise the inevitable restructuring pain in one sector seems pointless.

Get our daily currency email by signing up here:

Daily exchange rates

Select chart tabs

28 Comments

Hmmm -the deafening silence of disapproval?

I accept the outcomes but not necessarily the causes of rising interest rates.

The disquieting evidence of illiquidity in fixed income markets is ever evolving.

Unexpected culprits include Apple Inc.

All four of Australia’s biggest banks, heavily reliant on offshore debt markets, have sent representatives to Reno, Nevada, where Apple’s money-management unit, Braeburn Capital Inc., is based, according to people with knowledge of the trips. Read more here and here

When taking account of financial risks in 2015 it is almost convention that there are bubbles, with rather unnerving complacency about it all. That suggests in some ways the whole idea of bubbles has changed since the first one under eurodollars showed up in 1985 (junk bonds), before the dot-coms were even floated. It seems as if there is an almost cease-fire of sorts about it, namely that everyone seems to accept that financial imbalances are part of the landscape and thus promise no defectors so long as that seems a reasonable position. Read more

Lobbyists at work and how multi-nationals tax-gymnastics never sleep

They want it both ends of the stick - coming and going - now a repatriation tax-holiday

Companies including Apple, Google and pharmaceutical giant Pfizer Inc. have been lobbying Congress for two years to approve a repatriation holiday that would allow them to transfer overseas profits to the U.S. and pay a tax levy that is lower than the current rate.

I fail to see why the US Govn doesnt just tax them the full rate now. Oh wait its a banana republic with bought Pollies.

Yes and its not the first time they've done, that either, under the rationale that they'd invest in their enterprises, increase payrolls, and fund further R&D, but the actual outcome of the 2004 tax repatriation scheme, was corporate management increased their own compensation, they fired US based workers, increased the offshoring of their operations, and reduced R&D investment.

For those unfamiliar with TISA and its implications, and wish to know more.

http://www.nakedcapitalism.com/2014/06/wikileaks-exposes-super-secret-r…

http://www.scoop.co.nz/stories/PO1506/S00028/wikileaks-tisa-dump-expose…

http://www.wsj.com/articles/SB10001424052970203633104576623771022129888

I wonder if the TISA (Transnational Agreement on Investment and Services), which NZ is party to and is conducted under even more secrecy, than the TPPA contains provisions related to changes in international corporate tax policy.

The IMF is warning the U.S. fed to hold off raising interest rates for the time being.

Meanwhile in NZ finance is comparatively expensive - what is the benefit of the drag iof high interest rates to every homeowner with a mortgage, every small business owner, every small orchard ist and farmer etc - what is the point of this self inflicted handicap compared to every other developed economy?

This is still not the right time to raise interest rates.

This is still not the right time to raise interest rates.

Seems as though reality has got ahead of your sentiments. Choose tab "1D" for evidence

"•We expect the RBNZ to leave the Official Cash Rate (OCR) unchanged at 7.75% on June 7"

Whoops - wrong year - 2007.

If on the other hand you choose 1M you can see we have had noise on the scale of the present "up"

Apart from that there still is little reason to raise the OCR to cure non-existant inflation, and some to drop it before we pop into deflation and a recession.

Apart from that there still is little reason to raise the OCR to cure non-existant inflation, and some to drop it before we pop into deflation and a recession.

C'mon - an increasing majority of New Zealanders have already gone backwards. Rate cuts from here soothe the avarice of the already wealthy, but nonetheless, indebted property speculators. The poor pay extraordinary rates of interest to secure access to meager pickings.

How true. Or should I say how sadly true.

Indeed,

a) "egalitarian" no more as money is sucked out by the financial parasites (of all walks of life). It seems we reward bankers, financial speculators and currency traders over real businesses and are quite happy to let them feed off us like carrion.

b) I noticed a letter from the bank putting up the CC rate by 1% or so. (see a))

c) Depositors whine that having enjoyed exceptionally high interest rates by standards in asia life isnt fair especially now the tide is going out and the OBR leaves them vunerable.

Who is to blame here? Enough NZers voted for JK's tax cuts in 2008 and against HC didnt they? and repeat this time and probably next time. Enough voters dont want their property speculation taxed and dont care about other NZers as long as they are OK. The ethos of Rogernomics has a lot to answer for and it will be answered I think. Not to mention the delusion across generations that we can grow for ever.

all the ducks are lining up for a sep Fed rate rise, the USD is also strengthening which since NZ is a high importer and we buy in USD will lead to inflation. also oil is stable and in a stable trading range so will no longer will add deflation. all the signs are for increasing fixed rates in about 3-6 months then it wll be interesting to those leveraged to high.

have a look at NZ,s richest man selling assets to reduce his debt loading and increase interest cover

Or the ducks may be shot before the hike

http://www.cnbc.com/id/102593779

Unfortunately most mortgage holders don't understand the risk that a Fed hike brings to them. At the moment theyre sucked in by talk of a RBNZ cut, which may or may not occur, and ignorant of the fact that if that cut(s) don't come in Jun/Jul, and if Sep is still looking likely for the Fed (although there's no guarantee of that despite the payroll figures on Friday), they'll likely very quickly lose their access to the current cheap longer-term fixed rates at a time when they're thinking OCR cuts will happen and will provide them lower with longer-term rates.

And I say potentially very quickly because the other thing that they dont understand is the massive illiquity developing in financial markets over the past year that will inevitably cause major market movements and volatity when events eventually do occur (e.g. a Fed hike) such that they will not have time to react and lock down their position - it is a concern. The smart money will be comfortably hedged, but many others wont

Grant, how is that likely to affect people already on "fixed" loans?

David, re: original article: "But banks and their economists won't like it. And neither would 'property investors' which these days seems to be everyone who owns a house."

the real danger is not so much the problems of 'property investors' but the results of (a) lower disposable income for 'owner-occupier investors', and (b) that if it's a market wide effect it is likely to result in lift in rental prices which are already out of step with wages in many locations.

Don't forget there are as many if not more 'savers' than 'borrowers', who will be more likely advantaged by higher rates than hurt by them. But the overall cost of higher rates may well be negative because those fewer borrowers took on obligations greater than savers salted away. But not by much.

Total borrowing by households and business is about NZ$355 bln, total bank balances are NZ$265 bln (excluding for foreigners). There are other savings - KiwiSaver/Funds NZ$87 bln, NZ Super Fund $40 bln etc. So overall its sort of in balance. The Government's borrowing is usually talked about in gross terms - NZ$70 bln - but in net terms is much lower than that.

Bottom line: higher rates might hurt borrowers, but they probably won't hurt society overall much at all.

No doubt though, those paying extra interest will be more vocal than those receiving extra interest.

rents can only rise to the equivalent of ability to pay and numbers requiring properties. at the moment that is distorted due to government top ups and high immigration. you can reduce these two factors and rents would drop but no government wants its people living on the street and empty houses

Hi Cowboy, no they won't be affected and that was my point. However, that said, those that are fixed in the mortgage market are generally fixed into the much shorter terms (6mths - 2yrs), and not from my observation of the public's past history, from a great understanding of interest rates, but rather simply because its cheaper. Much like it was in reverse in 2007 before the crash when they were fixed in the longer terms for the same reason - greed, or desperation, is usually the norm. If I was a borrower I'd be staggered out 3-5yrs (longer if the banks provided it) as thats where you need to be from a risk management viewpoint - those that are vunerable (an increasing number), and don't manage risk, inevitably come a cropper.

And for those that think there isn't risk, but actually understand what the US Fed funds & US bond rates mean for our rates (unfortunately the two don't generally go hand in hand), should spend an hour viewing the attach link - it might actually mean they get to keep their house/farm/investment.

My outlook is quite the opposite. We've enjoyed unprecedented low interest rates during the current business cycle. Look at what has been achieved: GDP growth of around 3% which good but not great under under such easy conditions. Mortgage credit growth of around 5% which is considerably lower than one would expect under the current interest rate scenario.This is also exacerbated by low inflation and poor wage growth. So how will higher borrowing costs across the curve impact growth and credit expansion? It's likely de-levering will ensue and only one way it can go. Stick to the short end is my advice. Can't do much about the long end but look for Wheeler and co to look after the economy at the short end.

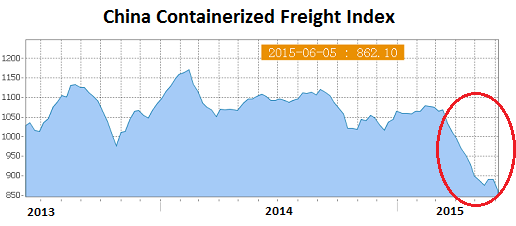

What about the implications of this?

http://wolfstreet.com/wp-content/uploads/2015/06/China-Containerized-Fr…

{kind=link}

http://wolfstreet.com/2015/06/05/china-containerized-freight-index-ccfi…

And the next article linked to as well;

http://wolfstreet.com/2015/06/05/get-used-to-selloffs-central-bankers-s…

I reckon within the fortnight we'll all know.

It's OK. The G7 meeting in Germany will solve the EU economic spiral, reset tthe world economies to pre-2008 conditions, normalise interest rates, return to growth as normal. All under control.

Not so fast on the jobs growth,

http://davidstockmanscontracorner.com/another-paint-by-the-numbers-frid…

"For instance, among the grand total of 280,000 new jobs reported for May, the entire goods producing sector—-construction, manufacturing, mining and energy—- accounted for just 6,000 or 2% of the gain. And that’s not just a monthly aberration. Employment in the most productive sector of the US economy has been shrinking for 15 years, and is still 2.4 million or 11% below its pre-recession level."

the rise in employment and wages might be because they are going through a poor patch with productivity

A shopkeeper has 10 customers spending $1000 each. A year later that same shopkeeper has 100 customers spending $100 each. He has the same turnover but has to hire more staff to handle the increase in customers.

That is a fall in productivity and a result of falling wages.

Others think the same.

Frankly, higher rates driven by an improving economy and a more aggressive Fed looking to head off inflation seem a little far fetched to me. I’ve been talking about this for years now but I’ll say it again; better growth isn’t happening as long as productivity and population growth are depressed. And higher inflation isn’t happening unless the dollar falls a lot harder than it has recently. The New Normal, the Great Stagnation or whatever you want to call it is here until we start to see some real investment that can pay off in better productivity gains. We are a long way from that right now. Read more

I went to this site

http://www.multpl.com/us-gdp-inflation-adjusted/table

and analysed this data.

What i ended up with was a 1yr, 5yr, 10yr, 15yr and 20yr graph of changes in economic growth.

The results were

The pace of growth in US GDP has been gradually declining for the past 70 years. Yes you heard correctly - for the past seventy years.

It is hard to pick short term changes to GDP but i recon that there is a better than 50% chance that US growth for 2015 will be close to 2.5%.

As the graph shows a steady decline for the past seventy years then i predict from that

America may only see 3% growth once in the next couple of years if they are lucky.

15 years from now America will be pushing to achive 2% growth

30 years time America will be pushing to see 1% growth

So any talk of FED rises is rubbish. But if they are foolish enough to try it will be just like the RBNZ and short lived.

OOpps

Ooops problem getting through on the internet

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.