Dairy co-operative Fonterra has issued a second profit upgrade in little more than two weeks and is now forecasting that earnings could be somewhere in the region of a third more than earlier indicated.

And the co-op has released more details on the planned sale of its consumer brands, given the name 'Mainland Group'.

Fonterra now says earnings for the 2025 financial year will be between 55c and 75c a share - up from a previous forecast range of just 40c to 60c. If you take the mid-point of those two forecast ranges it gives an initial forecast of 50c a share and now, with the latest forecast the figure is 65c - that's a 30% hike.

The latest upgrade from Fonterra comes on the heels of a February 21 upgrade in which it had said it expected earnings to be in the "upper half" of that previously forecast 40c-60c range.

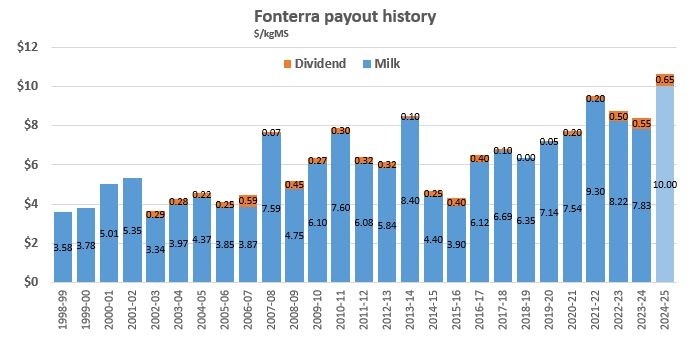

The quick-fire profit upgrades are notable that they come amid a season in which Fonterra appears likely to pay a record farmgate milk price of around $10 per kilogram of milk solids.

In the past Fonterra's profits have tended to suffer when the milk price for farmer shareholders is high - because the milk price is a significant part of Fonterra's cost base. Therefore, a high milk price, while good for farmers directly, can knock Fonterra's earnings.

Apparently not this year though.

The upgrade comes ahead of half-year earnings to be announced on Thursday, March 20.

Fonterra chief executive Miles Hurrell told NZX it’s pleasing to see the co-op delivering strong earnings performance alongside a $10.00 per kgMS forecast farmgate milk price midpoint, "which is a great outcome for farmer shareholders".

"As we have finalised preparation of our interim results, and looked at the balance of the year ahead, we are pleased to confirm an upgrade in our full year forecast earnings range," Hurrell said.

"This upgrade reflects the underlying strength of our core Ingredients business and the resilience in our Consumer channel, which is contributing to a robust result for businesses in the divestment perimeter.

"Our Consumer channel has shown good volume and margin growth while recovering the higher Farmgate Milk Price this season," Hurrell said.

The co-op’s dividend policy is to pay out between 60-80% of full year earnings, with up to 50% of the full year dividend to be paid at the time of the half-year result.

At the same time as issuing its latest profit upgrade, Fonterra has released materials for roadshow meetings, starting on Monday (March 10) with potential investor groups as part of the divestment process for its global Consumer and associated businesses.

The co-op is keeping its options open between either a trade sale of the newly-styled 'Mainland Group' or an initial public offering (IPO) followed by a stock exchange listing.

The roadshow meetings are being held in New Zealand, Australia and Asia, and will be led by Mainland Group CEO-elect René Dedoncker and CFO-elect Paul Victor.

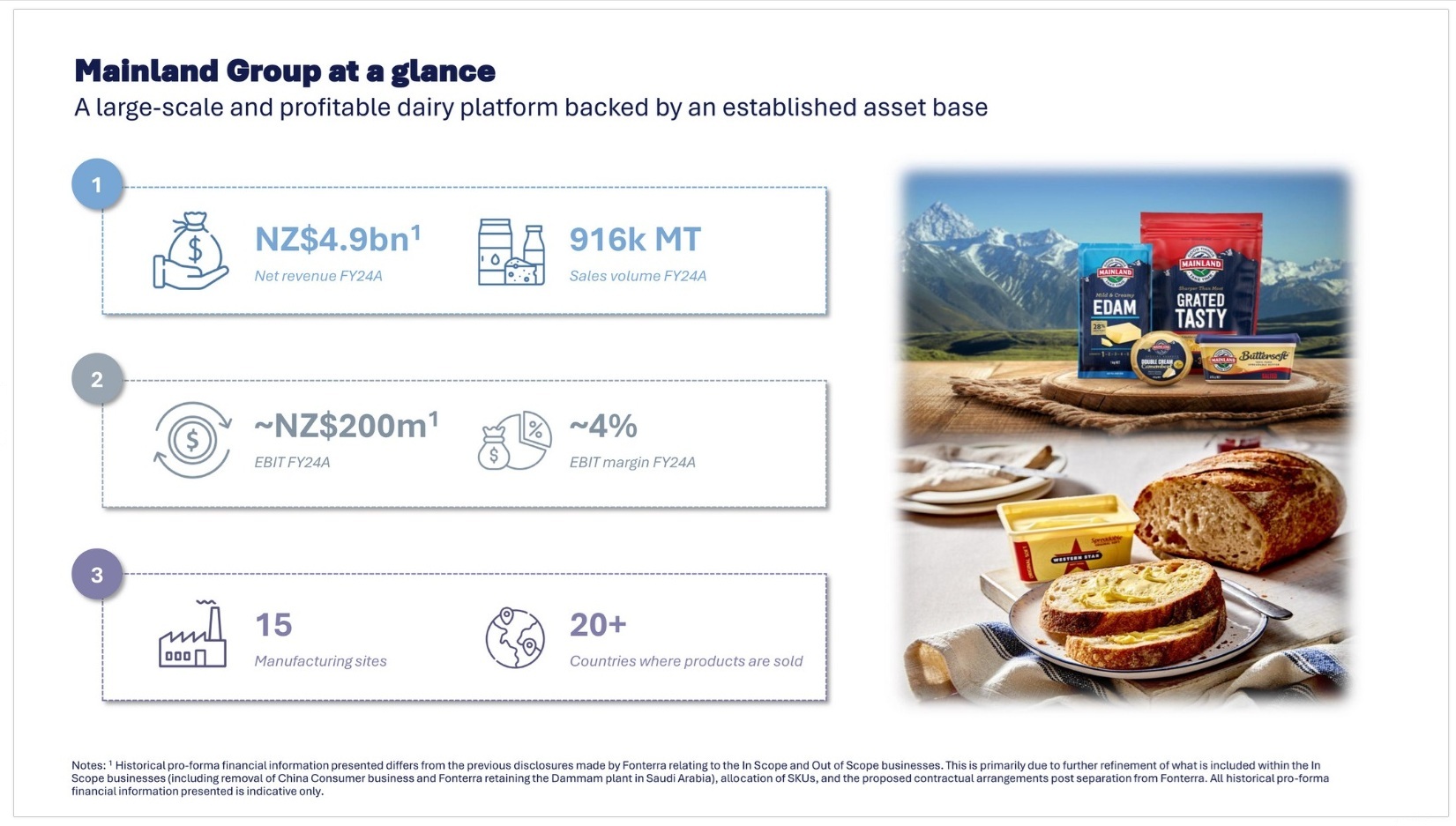

Fonterra first foreshadowed a potential sale of these assets last year. Included are household-name brands such as Mainland and Anchor, while there's also Fonterra Oceania and Fonterra Sri Lanka.

Hurrell says the roadshow meetings are an important step in the process of testing the merits and value of an IPO, which the Co-op is exploring as a divestment option alongside a trade sale.

"We are pleased to be making progress in both the potential trade sale and IPO processes and will continue to keep our farmer shareholders, employees and the market updated on milestones," he said

Fonterra "continues to target a significant capital return to be made to farmer shareholders and unit holders following the divestment".

It has been estimated Fonterra shareholders might reap as much as $3 billion - about $2 per share - from a successful sale of the businesses.

The roadshow materials released on Monday by Fonterra showed the assets up for sale made revenues of $4.9 billion in the 2024 financial year, up from $4.7 billion the year before. Earnings before interest and tax (EBIT) were $200 million in the 2024 financial year.

11 Comments

The Fonterra turnaround over the last five years is remarkable.

Will broader New Zealand now step up and invest to create a genuine international champion? That is the big question.

KeithW

This is getting quite rediculous. As the price of their raw material increases they are somehow making more money. So much the opposite of the previous 15 years.

If by 'ridiculous' you mean that it demonstrates how poorly the 'old Fonterra' was run for much of the first 20 years of its life, then I agree with you.

KeithW

Exactly what I meant.

There's probably even posts from me and others from way way back on interest pointing to exactly that, but it came up against a brick wall from shareholders at the time. I truly can not believe the change Miles Hurrell has wrought.

Don't forget the changes at Board level. My own opinion is that this is where the fundamental change occurred.

KeithW

So the assets they wish to sell returned maybe 6% on Capital. But the dividend is a 15% return on shares. (Figures in my head off cuff so hopefully not to far out).

This would be why they are selling them?

Fonterra will still be profitable without the consumer brands business.

These profits come from food service and related specialist ingredients.

My personal hope is that the proposed new 'Mainland' becomes a NZX listed consumer-focused company with a significant minority holding by Fonterra. I first wrote about that model close on 20 years ago.

My fear is that if corporate NZ does not step up right now then 'Mainland' will instead go the way of an overseas-owned trade sale.

KeithW

Fonterra will still be profitable without the consumer brands business.

These profits come from food service and related specialist ingredients.

How does Fonterra differentiate itself on food service and specialist ingredients? Is it because they're more efficient on the food service channel compared to the competitors? I know that in ASEAN they've trying to recruit from Puratos who are quite effective in the bakery channel. I'm guessing it will depend on how well they do this in China.

In part it is because this is their 'main business'. It is a sector where they are the 'big boys'. Also, there is cultural alignment in the way the company is run. This is a simple answer to a complex question. Fonterra's food service kitchen in Shanghai where they work with local chefs, and have done so for 15 years, is one such example. I have personally spent time in that particular kitchen including eating some of the test products onsite.

KeithW

Gotcha. I'm aware of the efforts in China and also aware of the intentions / past efforts in ASEAN re food service and ingredients. Europe less so but would think that mkt is more difficult to dominate. In the case of Vietnam, while the early establishment of the business model for food service has been superb, to some extent it seems far less entrepreneurial than perhaps it should be. As for other ASEAN markets, it's unclear. Perhaps replicating what's working in China should be looked at for other ASEAN mkts.

The turnaround in Fonterra performance is awesome to see.

I argued at the time that NZ Apple and Pear Marketing Board that morphed into ENZA should have pursued the get back to the knitting approach that Fonterra has pursued. The huge cost to orchardists for America's Cup sponsorship and Jules Verne round the world yacht races were great ego boosts for John McLiskie and Joe Pope but did not deliver to the orchardists in fruit value. That lead to throwing the baby out with the bath water rather than a deep look into how ENZA could be restructured to sharpen focus on grower returns - to my knowledge that navel gazing exercise was never undertaken. Instead deregulation was foisted on the industry in a calculated manner by which vested interests gained significant advantage through control of post harvest functions at the cost of everyday orchardists who were bloody good at growing the fruit international consumers desired and useless at marketing because that was something that they entrusted to NZAPMB/ENZA.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.