Retirement village operator Ryman Healthcare [RYM] is asking shareholders for about $1 billion - its second substantial capital raising in two years - as it looks to reduce debt to "reset" its balance sheet.

In February 2023 Ryman raised $902 million, which all went to extinguish US 'private placement' debt.

The $1 billion to be raised now, through a $313 million underwritten institutional placement and an approximately $688 million underwritten pro-rata accelerated non-renounceable entitlement offer, will reduce Ryman's gearing "to more prudent levels" within a range of 20-30%, below the previous 30-35% medium-term target, the company said.

"Ryman is taking decisive action to reset its balance sheet through a $1.0 billion equity raise to create a sustainable capital structure. This will enhance financial stability and resilience in the current market, and provide the platform to achieve improved performance and a return to growth over time," the company said.

The company's shares went into a trading halt on NZX on Monday to allow the raising to take place. The offer price is $3.05 per share compared with a market price on Friday of $4.31.

Ryman was founded in Christchurch in 1984 and owns and operates 49 retirement villages in New Zealand and Australia. Ryman villages are home to 15,300 residents, and the company employs 7,700 staff.

Ryman says the move will reduce net interest-bearing debt from $2.56 billion to $1.59 billion.

Regarding its lending arrangements, the company says it has agreement to amend its syndicated facility agreement.

It has received a waiver of interest cover ratio (ICR) covenant with testing to occur next at the 30 September 2026 test date at a lower covenant of 1.5x (on and from that date).

The company has extended $539 million of its banking facilities and has no near-term maturities.

Ryman says the capital raise provides flexibility to undertake and operational reset and manage the business to optimise cash generation.

The equity raise and future projected release of cash is "expected to provide headroom and capacity for a return to disciplined growth over time".

The board remains "committed to reviewing dividend policy prior to the end of FY26".

In the half-year to September 30 Ryman reported net profit after tax of $94.4 million, down 50% from $187.1 million in the first half of 2024.

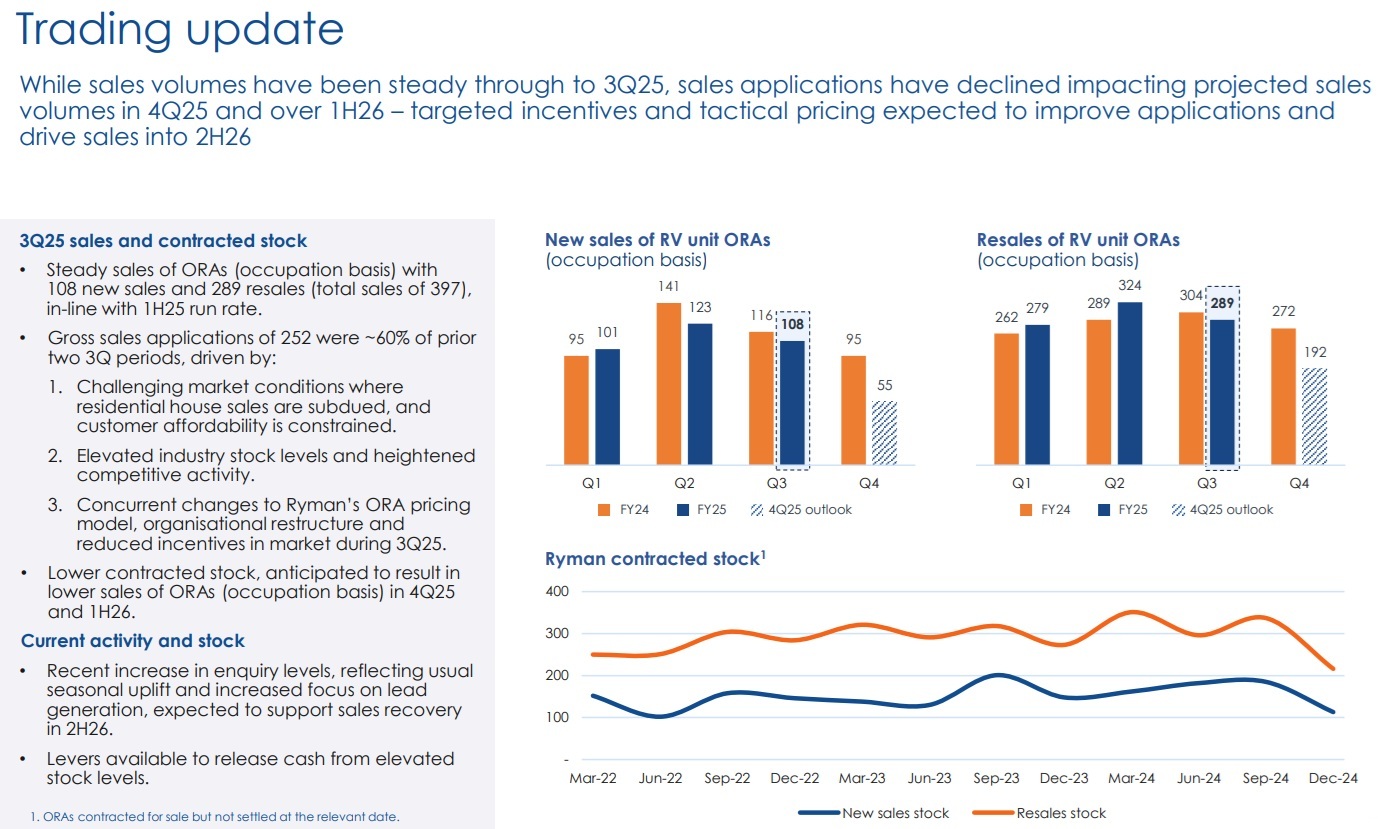

In a trading update with the capital raising material, Ryman said while sales volumes have been steady through to the thrid quarter of the March 2025 financial year, sales applications have declined "impacting projected sales volumes in 4Q25 and over 1H26". The company says "targeted incentives and tactical pricing" are expected to improve applications and drive sales into the second half of financial year 2026.

Ryman Chair Dean Hamilton says Ryman is "on a journey and have already made significant transformation progress over the past 12 months, including our Board, management and governance refresh, changes to our pricing model and moving to a functional structure".

"Resetting our balance sheet will support us to progress our business improvement programme further."

Ryman CEO Naomi James, who joined the company in November 2024, says that the business improvement programme is now "firmly focussed" on releasing cash from the business (over $500m target over the next three to five years), targeting sustainable business improvement ($100-150m target in annualised cash improvement through both revenue and cost opportunities over three to five years), and taking a disciplined approach to growth.

"We are transforming how we operate so that our residents continue to have the best experience in retirement living, with access to industry leading care. Our continuum of care model uniquely positions Ryman to meet the increasing demand for aged care in New Zealand and Australia, which is growing rapidly ahead of the supply available in both countries. Since joining Ryman, I have seen first-hand our unique value proposition in the market, which offers our residents access to the level of care they require as their needs change, giving families the confidence their loved ones will be looked after through their later years."

32 Comments

Oh Dear, imagine the headline if one of our banks seeks to reinforce their balance sheet.....

"imagine the headline if one of our banks seeks to reinforce their balance sheet....."

Some privately owned unlisted businesses without access to additional capital are going to face cash flow stress and be unable to survive in its current form, with significant impact for existing shareholders.

If Ryman was unlisted and did not have access to additional capital and support from existing shareholders, the company may have had significant cashflow stress and an entirely different outcome. In the event of debt default, the holders of the right to occupy would likely become unsecured creditors. Many customers may be unaware of this inherent credit risk. For some customers, the purchase of a right to occupy is the largest asset that they own (i.e amount receivable from Ryman). Several relatives are current customers and in this very situation.

Just because a company is listed, access to capital may still be unavailable - look at US listed Nikola which had a market value of US$27 billion at the peak. This is equivalent to NZ$47 bn, about 26% of the entire current market cap of NZ. Nikola just filed for bankruptcy.

Take some comfort for your relative. Retirement villages have a statutory supervisor and the Retirement Villages Act protects ORA holders. If the land under them is sold it can only by law be sold with the village continuing and the residents get to stay. Even if sold by a mortgagee same protection applies.

Just one more billion please. What could go wrong?

All the while sellers cannot get enough for their existing home to be able to afford to move in.

A rellie was hoping to chose between a Ryman apartment and another. The other was better so fully intends to go with it ( needs to sell first) but Ryman have since upped the price from $400k to $450.

Wait until the old biddy gets unwell and is so emotionally attached the only option they want is the Ryman/Somerset Hospital Level Care. Financially brutal and mostly overlooked. In saying so, excellent service.

Is it really financially brutal compared to the only realistic alternative, which is buying in-home care? That could easily burn through $500,000 a year.

It wouldn't come to this if families were willing / able to take their parents into their homes.

Families dont have the energy or resources to look after elderly parents.

Most families are stretched mentally and time wise to pay their bills, buy a house and raise a family.

Once you are old enough to need help u better have a fat wallet or it's gonna be messy

I would have thought that if your parents were elderly you would be quite old too. The kids should have left home by then.

In the days past sure, but it's starting to shift or perhaps we're even in the middle of the change. More people are having kids later and more "kids" are staying at their parents for longer, a double whammy.

My father is 80, and all bar one of the children in our family are teenagers and still at school. The other is still living at home though. And they're expensive.

There is a form of elder abuse out there where the kids wont let the parents go to care (usually a single oldie). Instead they leave them to loneliness, poorly cared for and neglected in their home. The kids don't want them in their homes and they also don't want to loose their inheritance.

While pocketing their pensions.

Hardly surprising. Rymans business is property. Their business model relies on a continual increase in property values so they can sell occupancy at an ever increasing rate.

This model has come to an end.

Its actually far harder than that. They have to run a business to keep those properties tenanted. None of the other REITS have to do this.

And the business they have been running is getting smashed by an increasing cost base... and they are struggling to push that on to the oldies.

If the Retirement Villages are struggling now, you can imagine what they will be line in 15 years!

Its interesting that the retirement village model in Australia is totally different. They dont provide aged care facilities, and over-50s buy (and sell) their own home (so keeping any capital gains) while owners pay a ground rent for the land its on. The REIT (eg Stockland) makes money by doing nothing, and the rent gets paid regardless of whether the home is occupied or not. In many cases, the ground rent is paid by the Govt as pensioners are eligible for rental subsidies. Because its leasehold, there is no stamp duty payable.

And also book constant asset revaluations on all the property as house prices go up. This allows them to look profitable on paper, but in reality they are losing money. See their negative cashflow.

> on a journey and have already made significant transformation progress over the past 12 months

What are they transforming the business into, a butterfly?

No...it will be a tree. Orr already has the Kauri, maybe a pohutakawa?

It won't be a profitable rest home business anyway!

The NZ Property Ponzi cash machine is Kaput, Redundant and simply no longer the road to riches.

I know old folks who are spitting tacks, that they can no longer sell for "deserved 3 to 4x" their purchase price of 10 to 30 years ago......and pulling out of selling, their now mostly empty big house.

This crash has a while to roll yet, with some forced sellers are still to meet the market, to fund the Rymans life.

So existing shareholders have to stump up more cash or get scalped by the brokers who are doling out free money to their preferred clients, ain't capitalism a wonderful thing!

Existing shareholders simply bet on the wrong horse.

It was predictable

Looks more like a Donkey

All Sharesies account holders got an email inviting them to participate in the placement at a 29.2% discount from Friday's close.

Via Sharesies:

As a Sharesies investor, you can take part in the placement by applying for new shares at the fixed price of $3.05 NZD. This represents a 29.2% discount to Ryman’s closing price of $4.31 on the NZX on Friday, 21 February 2025.

Applications for shares in the placement need to be submitted through Sharesies before 4:30 PM today, Monday 24 February 2024. We know this is a tight turnaround, but that’s due to the nature of this type of offer.

This placement will be mainly targeting existing and new institutional shareholders, so please bear in mind that scaling is highly likely, and you may only receive some or even none of what you apply for.

Sounds like broker spruik of a blind, 3 legged mutt.

With the oldies, empty, distressed sale homes, no longer selling......the cash flood into the serviced villages is now a financially existential trickle....

"This represents a 29.2% discount to Ryman’s closing price of $4.31 on the NZX on Friday, 21 February 2025."

1) need to attract shareholders to subscribe

2) allow for share dilution (i.e. same sized pie being cut into smaller pieces)

Isn't a being in a rush one of the red flags to look out for?

Sharesies hasn’t seen a general decline - but look out!

I can see lots of their customers being mad with them as it all looked too easy.

I’m out of most shares probably till mid year and will have a further think then……..

It is good to see that the entire Management Team look new.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.