Fletcher Building [FBU] is a difficult collection of building related businesses to efficiently manage in its current form, analysts with investment services firm Forsyth Barr say.

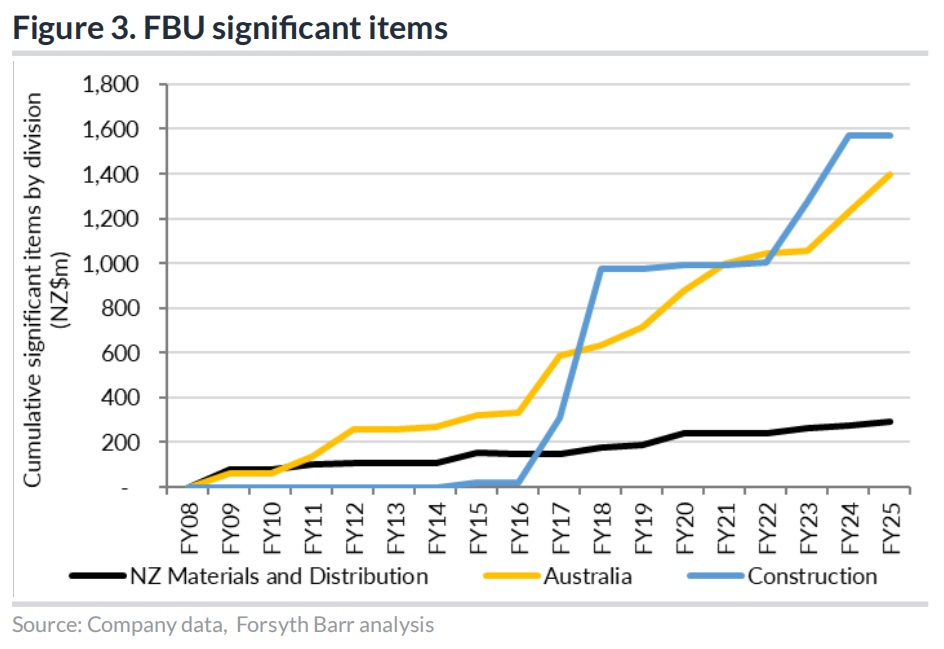

And they say that after completion of the current capital raise, over the course of the past decade Fletcher will have raised $1.5 billion in capital from shareholders and sold $1.8 billion in assets, in order to fund $2.6 billion of 'significant items' and losses.

Fletcher went into a trading halt on NZX on Monday as it announced the capital raise, of $700 million, to pay down debt.

On Tuesday the company announced it had completed the first part of the capital raising, from institutional shareholders, and had taken in just under $600 million. The shares then resumed trading as the offer to remaining shareholders was launched. The Fletcher price spiked about 8% to just under $3 as the market reacted to news of the successful capital raising.

In a research note on the capital raising Forsyth Barr senior analyst, equities, Rohan Koreman-Smit and analyst, NZ equities, Paul Laxton Koraua, said while the capital raise was unsurprising, given elevated gearing, volatile trading conditions, and an incoming management team, it had come sooner than they expected.

"The new CEO is a week away from beginning his tenure, and the company just told investors that it was comfortable with its balance sheet at its FY24 result in late August," they said.

"FBU did state that the operating environment remains challenging, and that it has increased its cost out target [to $180 million] as a result."

The analysts say they see value in the NZ core of the business, and the upcoming strategic review is (another) opportunity to refocus the business.

"But the investment case is clouded by continued cash flow drag from the Construction and Australia divisions."

However, NZ demand should improve as interest rates are cut.

The analysts say the capital raise allows more time for Fletcher's new management team to undertake a full strategic review and evaluation of the portfolio of businesses.

"We expect this to be completed within the first half of next calendar year."

They say "capital partnering" within the residential division - that the company had discussed doing when announcing its annual result last month - "remains an option but this is not a quick process".

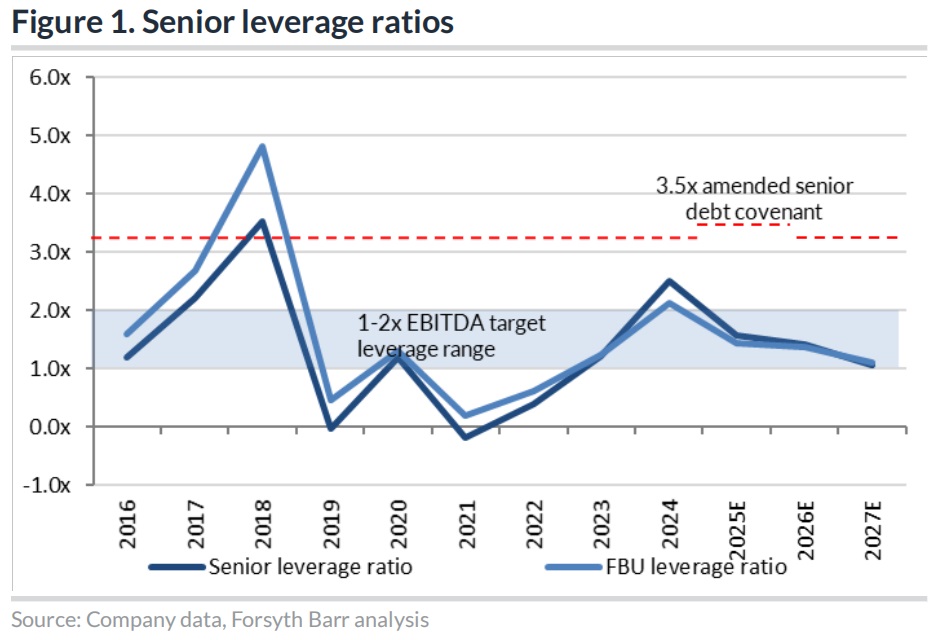

The analysts say Fletcher's elevated net debt "left little margin for error" to breach amended covenant ratios, but the capital raise does alleviate balance sheet concerns.

The analysts have adjusted the Fletcher financial forecasts (see below) for the impact of the capital raise and have assumed the proceeds are applied to debt reduction. They have lowered their 12-month "target price" for Fletcher to NZ$3.10 from NZ$3.60, "reflecting dilution from the equity raise".

14 Comments

I understand Auckland Airport the other day raised approx 11/2 billion for planned expansion. But I was surprised to read that Hawkins has the building contract.

So, did Fletcher's submit a tender at all? If not, why not? Were they even invited to tender? Or is it because they have lost all credibility in the infrastructure sector? And all that's left for them is residential construction, and even here they give the impression that they can only operate in the residential sector if they have a partnership with some other company.

These are interesting areas for a business journalist to explore.

In the old days we used to call the then Fletcher Challenge “the hungry lion.” Almost as if a modern times Greek tragedy come legend, the only motivation, direction, and sustainability was to keep hoovering up business after business, and then finally the whole damn shooting box has become the Hydra, doesn’t know it’s head from its tail.

They got out of vertical construction after the convention centre debacle. They don’t do that type of work anymore (no doubt they will start again soonish and the cycle will repeat).

Hawkins have been at airport 20+ years doing extensions etc. It's what big construction companies do. Say Vodafone wants to up grade its shops to One NZ but over a period of time the construction companies will take a loss on the first few to then get the contract to do the whole lot were they will mark up and hopefully make a profit on the last few.

Or they do it with an open book agreed profit margin right from the start, indexed to PPI and CPI at certain intervals.

Not every commercial arrangement has some nefarious profit gouging "long game" behind it.

They aren’t a difficult group of businesses to manage if the management was competent. Part of the problem is they keep listening to analysts and employing consultants!

LOL. You've worked there then? Herding drunk cats high on speed would be easier. (The 'components' just do whatever they want.)

The best thing for the Fletcher shareholders and the whole of NZ is for this bloated incompetent monopolist to be broken up and sold so that the parts can be run efficiently, competitively, productively and profitably. If kiwis are incapable of this, we would be better off if say the Japanese owned it.

Agreed, should have been broken up long ago. Tragic.

Such short memories. Fletchers was broken up a long time ago

Yeah but that was Building from Forests, Energy, investments in Peru etc etc. eeeeek

This was from the day (2000) - "The diverse Building division is to become a standalone publicly listed company, after its heavy mix of construction, steel, building products, concrete and housing businesses proved a stumbling block for a sale."

This is the present mess that remains 24 years later.

Rubbish

I've made the decision to quit FBU shares. I have been involved in at least two capital raising. Had enough. Good luck to all other shareholders.

FBU is like TEL. (Exclude them from a basket of shares on the NZSE and it performs heaps better.)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.