Long term international government bond benchmark interest rates have an outsized impact on New Zealand.

Sure, the OCR rules for very short term rates. But it is the longer maturities that set the yield benchmarks. These longer rates are how commercial property is valued, how corporate equities are assessed, and how currency relativities are set.

This is where we are at present:

| Govt bond yields | 2 yrs | 5 yrs | 10 yrs |

| % | % | % | |

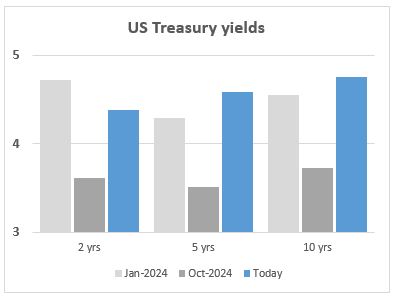

| US | 4.38 | 4.58 | 4.76 |

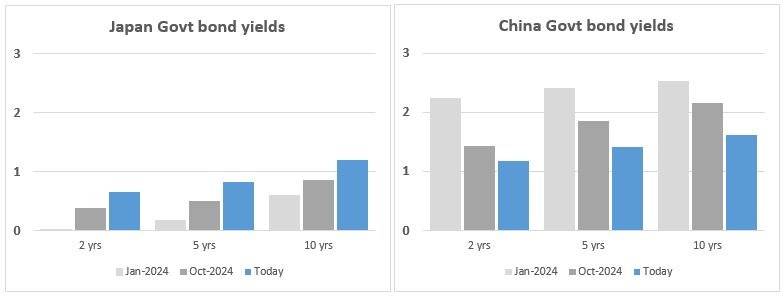

| Japan | 0.65 | 0.82 | 1.20 |

| China | 1.18 | 1.42 | 1.62 |

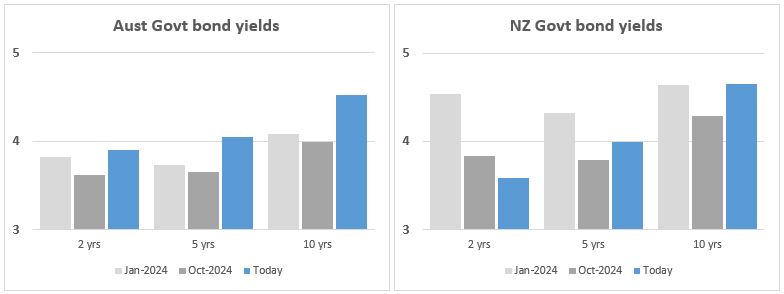

| Australia | 3.90 | 4.05 | 4.53 |

| New Zealand | 3.59 | 3.99 | 4.65 |

Things have changed rather quickly over the past three or so months.

This is where we were on October 1, 2024

| Govt bond yields | 2 yrs | 5 yrs | 10 yrs |

| % | % | % | |

| US | 3.61 | 3.51 | 3.73 |

| Japan | 0.39 | 0.50 | 0.86 |

| China | 1.43 | 1.86 | 2.16 |

| Australia | 3.62 | 3.65 | 3.99 |

| New Zealand | 3.83 | 3.79 | 4.29 |

And this is where we were at the start of 2024.

| Govt bond yields | 2 yrs | 5 yrs | 10 yrs |

| % | % | % | |

| US | 4.72 | 4.29 | 4.55 |

| Japan | 0.01 | 0.18 | 0.59 |

| China | 2.24 | 2.41 | 2.52 |

| Australia | 3.82 | 3.73 | 4.08 |

| New Zealand | 4.54 | 4.32 | 4.64 |

A number of things stand out here. Worth noting are ...

- the unwinding of the US inversions

- the speed of change up in the past 90 days of US rates, post-election

- NZ rates have moved from a premium to the US, to a discount to the US

- how far and fast the Chinese rates have fallen recently

- how far and how fast the Japanese rates have risen recently

- Australian rate have risen, but only modestly.

With rates moving this fast, it is bound to affect us. Even without the geopolitical pressures, these shifts are important from a Kiwi point of view because ...

- Australia owns 90% of our banking system, and the way they look at returns (through their yield perspective) impacts us. (If yields rise there more than here, it might push down the value of bank shares. And to mitigate that, bank boards will start looking for even bigger profits.)

- Japan and China are two of the world's major creditor nations. While we don't source much capital from them, Australia and the US does, and their situations are moving in opposite directions, and this too will affect the availability and pricing of the offshore borrowing we do.

- the US financial markets are where most of our foreign funds are directly sourced, or at least priced.

Interestingly, New Zealand benchmark bond yields are no longer at a premium to equivalent Australia rates across the shorter end of the tenors. And our relationship to the US has taken a major change. We are pivoting and even though our 10 year is back to where it was a year ago, it is now in a new rising trend.

Things are still on the move. It seems unlikely this is where these yields will be mid-2025 or the end of 2025.

The purpose of this review is to establish the benchmarks of where we start in 2025, and show how we got there from 2024.

Got a perspective on these shifts? Share it in the comment section below.

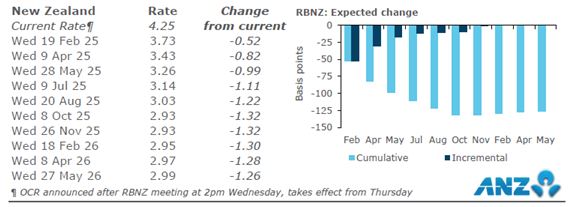

And for completeness, here are the current financial market pricing expectations for the OCR in 2025.

26 Comments

Always amazes me the comment count on property and interest rate articles but when you get to the underlying treasury influences that have market led forecasts there is a lack of knowledge.

Why? Reckon that's on track with the ratio of macroeconomists vs real estate agents in the country

Or, more generally speaking, with how much exposure average Joe has to the real estate movements vs macroeconomic policies

Also, it's a matter of complexity. Jane sold a house down the road for a 400k premium is much easier to comprehend than why the Japanese bonds have risen in the past 12 months

For the last 40 years, all you needed to know was that interest rates were dropping, and money kept getting cheaper. Inflation wasn’t even part of the conversation, no need for the average person to care about macro. But if rates keep trending up from August 2020 and the long end of the yield curve keeps rejecting cash rate cuts like it has since September 2024, we might be entering a new cycle, breaking away from the secular bond bull market. I feel bad for the FHBs who jumped in at the peak, but no sympathy for the spruikers caught in last year’s bull trap.

I think you and I are signing from a very similar sheet of music here. My warning back in late 2021-2022 to people was that it appeared that the US 10 year was breaking out of a 40 year trend of falling interest rates - and this could has a profound impact on everything they thought they knew about investing (primarily in bonds and property - nobody really talks about stock pricing on here anyway). Getting rich off property the last 40 years has been easy as interest rates went from all time highs to all time lows. No real need to worry about timing..just buy and get 7-10% annual returns. I personally don’t think current prices in property can hold if interest remain steady/flat, let alone rise again from here. Current prices are based upon interest rates being cheaper in the future than they are now. But in my interpretation of the 10 year yield is saying mortgage rates could well be higher in the future than they are now - so be extremely careful about taking on too much debt as the cost of that debt could keep rising, not falling (ie the opposite of what everybody’s experience paying off a mortgage the last 40 years).

Yes, I agree with everything you said. Bond market yields are currently reaching levels last seen between 2008 and 2011. A 5% 10y yield is approaching crisis territory for the US, UK, Australia and New Zealand, while for Japan, it's likely around 2% (which is approaching quickly). Jamie Dimon and Stanley Druckenmiller have both talked about the potential of the US 10y yield hitting 7%. That wouldn’t crush most Americans fixed for 30-years, but it would crush us here in NZ.

Yeah the chart looks there could be a lot of upside to come in the 10 year yield ie breaking out a lot higher - but who knows what may happen in terms of geopolitical events and central bank intervention/manipulation of markets the next 12 months. Either way it looks like we’re are again in a rock/hard place position and once again trying to avoid taking our medicine for living beyond our means. Ie too much private debt relative to our GDP/incomes.

Good post, I_O.

But I'd council against considering house prices solely from an interest rate perspective. The basics of demand and supply must also be considered. Demand can be significantly influenced by interest rates, and supply to a lesser extent. However, the dynamics of the supply side have changed radically in the past 5-10 years. In my view, these changes on the supply side will have a much greater impact than interest rates for the next 20-30 years. IMO, property 'investors' expecting the past to repeat in terms of capital gains are going to be sadly mistaken.

Always amazes me the comment count on property and interest rate articles but when you get to the underlying treasury influences that have market led forecasts there is a lack of knowledge.

Yes indeed and hats off to David Chaston for this.

Aussie 10 yr up 3.46% over past 30 days. Off to the pub for a $20 pint.

High mortgage debt must be hampering the ability to raise taxes to service state debts. CEIC pegs total Aussie debt at 264% of GDP.

https://www.ceicdata.com/en/indicator/australia/total-debt--of-gdp

J. C.

But that is very modest when compared to all the others on that list. The EU for example, is shown as having total debt of 719% of GDP.

All rates are surely rising and rising hardcore!

My Bloomberg subscription, while expensive for the small fish I am, has great economic news/info!

https://www.bloomberg.com/markets/rates-bonds

I follow Bloomberg news too. I don't miss an episode of 'Bloomberg Real Yield'.

The NZD has keeps tumbling with every cut of the OCR while the US 10 year treasury goes up, this will create huge pressure on inflation and at some point the OCR will start climbing again to protect the NZD which has lost 15% in recent months. In my opinion the property market will see next phase of crash pick up speed in coming year

Yeah if the US 10 year goes through 5% and I was loaded to the eyeballs with mortgage debt here in Nz, I would be feeling extremely worried.

To me, if the US 10 year goes above 5% then people should go back and look at interest rates in the post depression/WW2 period ie the period following the last time we had a period of such low interest rates to see what might be possible.

It looks to me that the Fed could go back to rate hikes again at some point this year - not a forecast just a possibility that has generally been completely dismissed - just as my views were that the OCR could go up to 5 or more following COVID (was told this would be impossible as the economy and housing market would never survive ..but it happened and we survived).

The NZD is also dropping due to the strength of the USD, which is considered a safe haven. The DXY nearly hit 110 today, and the next stop could be 113. I'm not sure the US stock market can handle a dollar that strong, as it makes those stocks even more expensive compared to the rest of the world. You can see the S&P500 beginning to roll over. A weaker USD is needed if it's going to hit new highs.

NZ inflation + GDP growth is 2.2 + 0.6 = 2.8, and yet the 10 year NGB bond is 4.5%+.

NZ will have to either go into austerity, or will need to borrow more, and the NZ debt level will be much higher down the track.

And if the government takes on more debt and spends more in the economy that is generally inflationary which could see rates go higher again.

This is the rock and hard place, as the government needs to spend more money to stay the slow in velocity of money. They are flogging the near-dead horse thinking they can still squeeze a few strides out of it.

Within the treasury of all the NZ Based divisions of the Aussie banks (or in there parent) there are separate legal entities based in the UK and US used to issue bonds in that environment and manage the swap from these currencies back to NZD. They legally outsource funding this way., though they normally share their offices offshore, often sitting on the offshore trading floors of the banks.

The sole purpose is to access fixed term funding and roll over existing funding for NZ entity.

What happens offshore 100% impacts us and our rates.

The 2 year used to be the most popular rate, but I think if you now look duration will be shorter.

If the UK/US raise there overnight rate, it will impact NZ more then it has in the past due to this shorter duration

If everyone in NZ moved to 6 month fixed rates, we would be locked to the US/UK/Europe 6 month funding costs.... sure there is NZ term deposit funds but not enough to fund 360 billion.

Rock and hard place time, what you would probably see is offshore rise and no RBNZ rise and a falling NZD.

is this a case of survive until trump goes away? He wants Greenland for natural resources but also to enable and protect the northern shipping channel around the artic, global warming will make this passable before 2030 year round, and its safer then middle east shipping routes.... USA could move to Greenland based oil and gas, avoid middle east and having to buy via Saudi, at this point it could pull out of the middle east, saving billions such a different world then the last 50 years, this is a new world well removed from the bitter lake agreements where US would provide security to Saudis and in return Saudis would price oil in USD only.... Saudis IMHO have more to lose here.

Within the treasury of all the NZ Based divisions of the Aussie banks (or in there parent) there are separate legal entities based in the UK and US used to issue bonds in that environment and manage the swap from these currencies back to NZD. They legally outsource funding this way., though they normally share their offices offshore, often sitting on the offshore trading floors of the banks.

Interesting learning for but with a little thought this makes complete sense.

Thanks ITG!

You are a Gem.

Not the facts Oneroof would like out there.......

Then again, we all know the vested Onesyspoof interests are all about NZ housing market ponzi proliferation, at all and any costs.

The Onespoof writers, funders and REAs are in for on hell of a head ache come FY 2025.......as their "5 to 10% gains" rose tinted, vested interest, stupid groupthink gets them all another serious Black Eye.

Great comment on a top quality article.

It's nuts isn't it - the world is moving rapidly in a direction that is counter to shared interests and the US is going to try and take the role of playground bully - using monetary, fiscal, and military firepower to keep it's oligarchy rich and it's people compliant.

On the monetary side, it is worth noting that the US can keep rates high because (i) dollar hegemony allows continuous sizeable govt deficits and (ii) they have effectively insulated existing homeowners from rate rises. My view is that we should shift our homeowner mortgage debt onto the Govt balance sheet (as an asset) and fix rates for term for existing and new homeowners - just make it 4% forever (inflation target + 200pts). The current financialised housing market just doesn't work and constant rate changes cause instability and boom and bust cycles. If we need to reduce aggregate demand, just use the tax system so we can target the actual spenders.

Your view is an exceptionally good one. ;-)

It is a view that appeals, but what do you see as a consequence upon demand for NZD? If we remove the ability of international finance to benefit from our desire to outbid each other on real estate will they be so inclined to fund our persistent trade imbalance?....I suspect not and the adjustment, while beneficial in the long run, will be exceedingly difficult.

Politically impractical?

Another great article, David. Thanks.

I really hope people take the time to understand it. This is critically important stuff to a small trading nation like NZ Inc.

Sometimes what seems like a minor change in some distant market can lead to changes that can last years and years for our market. A case in point - Japan's about face!

I'm trying to wrap my head around it, and comments like I_O's and kraken's have been helping with this (and have been for years). This site really has been helping me make financial decisions, so cheers David et al. Mission accomplish(ing)

It is precisely for articles like this and the knowledgeable comments that follow, that I am happy to pay the very modest amount requested by interest.co.nz

More please.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.