The overall home loan market is growing moderately. It was up +4.0% in February 2025 compared to the same month a year ago. That is better than the overall economy, even when inflation-adjusted, but it is less than half the growth rate during the pandemic animal spirits, and far lower than the +15% growth rates we saw in the 2003 to 2007 pre-Global Financial Crisis frenzy.

But there is one part of this market that's bubbling along with much higher levels of activity - the refinance part. This will be no surprise because borrowers have gone very short and a great wall of home loans are up for new rate setting in the next six to 12 months. Most of them in fact.

Change and churn creates activity even if it doesn't expand the market.

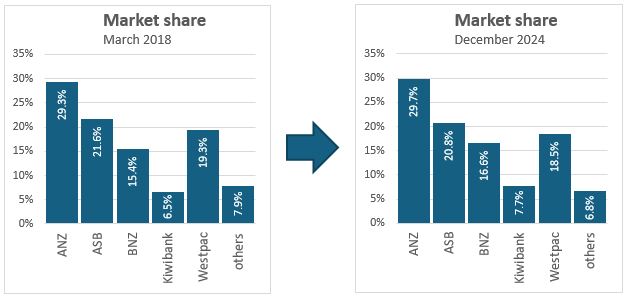

The curious thing about all this activity is that market share between banks is not really changing much at all. There are shifts, but at a glacial pace. You can't really see them except in a very long perspective.

Lots of activity with not much net change is the very definition of 'churn'.

Let take a look under the hood.

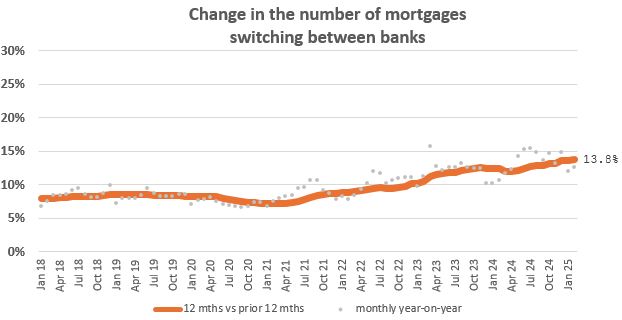

About one in seven existing mortgages change banks. And that is the highest level ever.

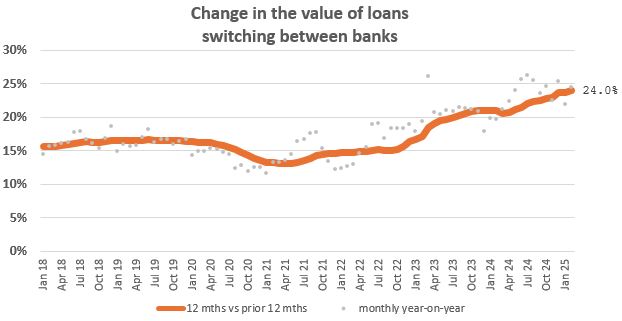

On a value basis, almost a quarter of these are changing banks - also the highest ever.

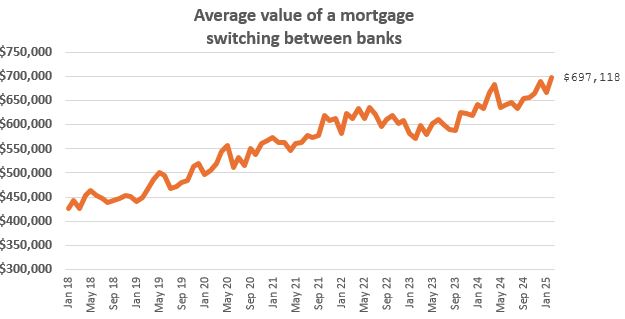

The fight is on for high-value home loans.

And it is not only for loans with prime loan-to-value ratios (LVRs). Those with LVRs over 80% are changing banks at a faster rate than those under 80%.

Mortgages that change institutions - shopping around - is a high-activity sector.

But if market shares are changing little, what is going on? High activity in a little-changing overall market just seems pointless. Interest rates are stable. But borrowers need to refix. They seem to be checking the market for the best deal, but the result is hardly changing banks' market shares.

Changing banks seems like churn for the sake of it. Only one group benefits. It isn't the borrowers who are just getting the same deal any bank would give. It isn't the banks, who are holding their share. The enablers who benefit are the brokers. Churn gives them the opportunity to earn a fee "for the service provided".

A good mortgage broker can bring valuable benefits to a borrower, including lower rates, better incentives, and a better structure of the lending that suits the borrowers situation. For borrowers who are not confident in the financial world, it can be comforting to have 'professional help' especially when it seems like it comes at no added cost.

But borrowers need to watch out for broker motivations. Brokers are paid by the banks, so have a clear conflict of interest. Brokers also take the opportunity to sell other related financial products, especially insurance (and paid by the insurers). These commissions are built-in to the offer rates.

The best way to ensure your mortgage broker is doing the best for you (and not for themselves or the "lending panel" they work with), can include the following points.

1. Before you talk to a broker of bank representative (and independent of them), go on a comparison website that shows all the current carded rates. (Make sure this resource is not associated with any of them, of course, and that it is comprehensive.) Find a low rate option* for a term you are comfortable with.

2. Insist they offer you at least three alternatives, nothing less. Ask them to explain if what you found in 1. above was not among what they offered you. Never just accept one (or two) 'options' presented (because 'we know the market and this is best for you'). That should be a real red flag if they do that. Three options should be the minimum they present.

3. Get them to declare the brokerage they will earn from each of the alternatives. They need to be paid for their services, but that needs to be reasonable. Brokers can help guide you through the bank requirements for information disclosure. This is valuable guidance. And when multiple banks are involved, they can insulate you from repetition.

4. Be very wary if they work with a limited 'lending panel'. In fact some brokers are owned by a bank. For example, NZ Home Loans is owned by Kiwibank. That is not a disqualifying attribute on its own, but you should go in with your eyes open.

Update: NZ Home Loans has asked us to clarify this point. They say "NZHL is a Government-owned subsidiary of Kiwi Group Capital Ltd (KGC) alongside its sister company, Kiwibank – with which NZHL has an arms-length arrangement. NZHL & Kiwibank operate with Independent Boards. NZHL has a bespoke Managed Home Loan through two main lenders, ASB and Kiwibank. However, clients who do not fit with NZHL’s proposition or want another lender can access a full panel of lenders through NZHL advisory.

[* At present, the banks with the most competitive rates are New Zealand registered Chinese state banks. It should be your choice whether you consider a competitive offer from them if it is the best in the market. Mortgage offers from such banks are in fact little different from any other New Zealand registered banks. Their documentation and requirements will be very similar.]

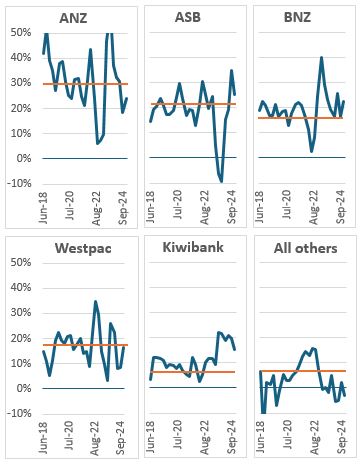

For the record, here is the long term market share change based on Reserve Bank Dashboard data.

And here is the same data over time for each bank to December 2024. The orange line is their long-term average. Those above the line are making mortgage market-share progress, those below are losing share. The variances are really very minor overall in the long run.

All the current activity is busyness, basically within a steady state.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.