Kiwibank says its half-year profit fell 12% as its net interest margin dropped and its costs and loan impairment charge both rose.

The bank's net profit after tax for the six months to December 31, 2024 dropped $13 million, or 12%, to $92 million from its record high $105 million in the equivalent period of its previous financial year.

Kiwibank said operating income rose 3% to $461 million, and operating expenses climbed 9% to $311 million.

The bank's net interest margin, the difference between what it borrows money at through the likes of deposits and what it lends it out at, dropped 18 basis points to 2.29%, and its cost to income ratio rose 362 basis points to 67.5%. Loan impairment charges rose 29% to $21 million.

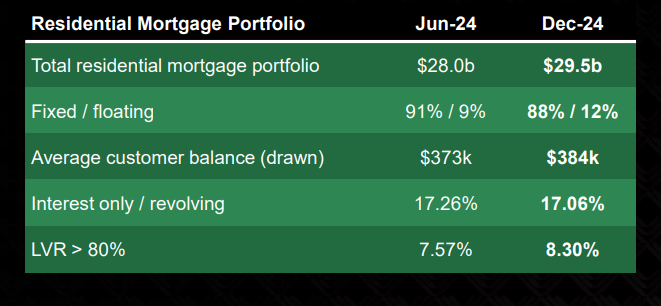

Over the six months from June to December 2024 Kiwibank says net lending grew $2 billion, lifting its lending book 6% to $34.4 billion. It says home lending grew 2.1 times faster than the overall market and business lending increased more than six times faster than the market. Non-housing term lending rose $598 million, or 13%, to $5.14 billion in the six months to December.

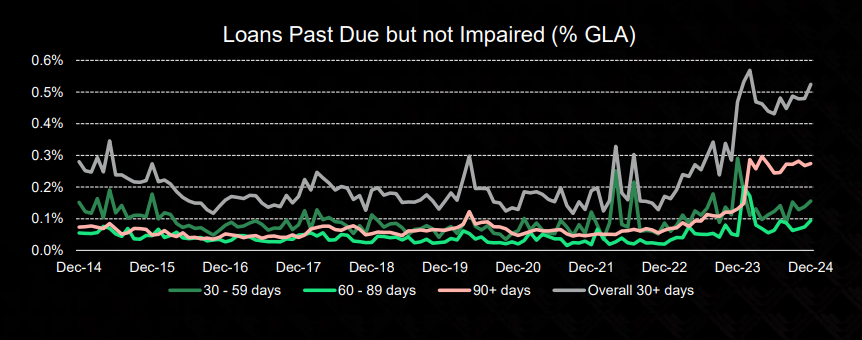

As of December 31, 2024, Kiwibank's impaired assets were at $39 million, up from $5 million a year earlier. Loans past due but not impaired were at $338 million, up from $290 million. The bank's impairment provision rose to $132 million from $114 million a year earlier.

In the six months from June to December 2024, deposits grew $1.8 billion lifting Kiwibank's deposit book 6% to almost $30 billion, with growth 1.6 times faster than overall market, or system, growth.

"Both home and business lending grew faster than the market and deposits increased over the period. This growth underscores our commitment to driving competition that benefits everyday Kiwi and contributing to a productive economy by helping businesses to thrive," CEO Steve Jurkovich said.

"To support our faster than market growth we made significant investments in products, services, and technology to enhance the experience for our customers. This included our transformation programme, which is delivering more scalable and modern systems and ways of working, ultimately driving competition and growth."

"Another area of substantial investment was the proactive measures Kiwibank took to protect customers as part of our ongoing commitment to enhance fraud prevention capabilities. Key initiatives included expanding and developing our specialist fraud team, who are dedicated to improving the detection and prevention of fraud attempts," said Jurkovich.

"Additionally, Kiwibank became one of the first banks in New Zealand to roll out the Confirmation of Payee service."

"Looking ahead, we expect retail and business confidence to begin to return as factors such as lower interest rates provide relief and stimulus," Jurkovich said.

As of December 31, 2024, Kiwibank's total regulatory capital stood at $3.363 billion, up from $2.885 billion a year earlier.

Investment sought

Late last year Finance Minister Nicola Willis said Kiwibank had been asked to raise up to $500 million from local institutional investors in a private capital raise. This is intended as the first step to boosting the bank's capital for ongoing growth ahead of a possible share market listing in 2028.

Scaling up Kiwibank was one of the key recommendations in the Commerce Commission’s banking market study, published in August 2024, which found the banking sector lacked competition.

Sourced from Kiwibank’s Disclosure Statements and management information.

GLA: Gross Loans and Advances

1 System figures are based on Reserve Bank statistical series S50: registered banks total loans as at 31 December 2024. Figures exclude credit impairment provision on undrawn commitments.

Kiwibank's full press release is here, and Kiwibank's presentation is here.

18 Comments

I have had excellent service from KiwiBank.

I was looking at switching so asked them, and they could not even be bothered (arsed) replying, I asked multiple times.

They do not have the capacity to service IMHO, let alone capital, they need an offshore funding vehicle (which would struggle due to credit rating)

Or we set up a Freddy Mac or Fannie Mae type vehicle in NZ , but the NAct will never do this.... Labour might

Its just pretend competition.

Kiwibank is not the first to report bad debts rising, Heartland just did it too. Kiwibank will not be the last neither.

I've mentioned this before so I'll be a broken record. Two loan attempts from Kiwibank 15-24 years ago unsuccessful. A big bad Aussie bank gave me the mortgages, no extraordinary interest rate. From the banks point of view paid off too soon so no long term interest earned for them. Now Kiwibank have increased their loan impairment. Perhaps they need to change their loan criteria or fancy algorithm that decides whether you are good for a loan. Maybe go back to the criteria when I was refused.

I do still bank with them for TDs and the odd 90d notice. Have another bank for my main dealings.

I found the same. Tried for a loan on my first home, a high quality studio in an established building. 50% deposit. Kiwibank just said that they wouldn't loan at all against that type of apartment. To be fair there wasn't much money to be made on it as I paid it off in 3 years. But now I'm kind of loyal to the Aussie owned bank that did give me the loan, and have just bought my first proper house while keeping the apartment.

Similar experience. We'd saved what was a 20% deposit back then with Kiwibank. Couldn't get any engagement from them on getting a loan to buy our first home. Both in steady full time employment. Ended up with an Aussie bank.

You should hear the odd stories about their toxic working culture.

Try the crook yarns of the friday night drinks at ANZ in Wellington with all the free craft beer one could drink.

Kiwibank launched in 2002 and I must admit my first dealings with them when they were relatively 'new', from a customer service point of view, weren't, to put it mildly, as favourable as I would have liked them to have been. But somewhere along the line we gave them our mortgage (closer to it's end life by that stage) and had no trouble with them.

We refinanced to them 2.5years ago. They were rubbish, 3 days before our first mortgage payment was due we did not have logins or account details to get the mortgage money into. Our broker had to chase them down and get things resolved. As a result we won't transfer any of our other accounts to them, and still don't have any kiwibank cards at all. Very likely to jump to another bank once we are out of the cash contribute clawback period, unless KB offers us much better rates than ASB or ANZ.

went with my ex wife to open accounts as we have sold our property and wanted to move business to Kiwibank from ASB -- Had tried in teh past but usually .5% difference in mortgage rates!

Three staff in the branch -- no customers - we had all the correct ID and documentation -- but they refused - said we had to book an appointment!!! Even when we pointed out that this was $1.5 million in cash between us we wanted to deposit and invest - and both have Kiwisavers - Still insisted we book an appointment to open an account!

At that point -- I basically thought -- if this is the service I am likely to get -- may as well stay where I am!

We've had a similar experience just recently albeit involving a small amount of money only .... still, it is very frustrating, none the less.

Less staff and hardly any branches opened, appointment is the only way they can manage the flow I guess.

Their AML process may require a pre approval etc for onboarding....

Had exactly the same experience, I wanted to invest 100,000 , went into branch and was told to make an appointment which would be the following week

Found service appallingly

KiwiBank needs to provide an uneconomic return due to offering below market rates. It's pretty simple.

I still cant fathom why the Government think external shareholders are a good idea for this.

There isn't a lot of banking competition in New Zealand. But there is enough that if a bank tries to run itself like a government department it won't do so well. I don't want my Kiwi Saver funds going anywhere near it for now.

Their fund is managed by fisher funds now, I've had good performance of my fisher funds kiwisaver (not through Kiwibank). Kiwibank has let me down with only offering advertised rates on the app. I am tempted out of principle to fix 6months for this half of the mortgage so both come up at same time and break fee is lower.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.