ASB's half-year profit climbed 2% as its net interest margin, the difference between what the bank borrows money at through the likes of deposits and what it lends it out at, rose nine basis points.

ASB's net profit after tax (NPAT) for the six months to December 2024 rose $14 million, or 2% to $763 million from $749 million in the same period of 2023.

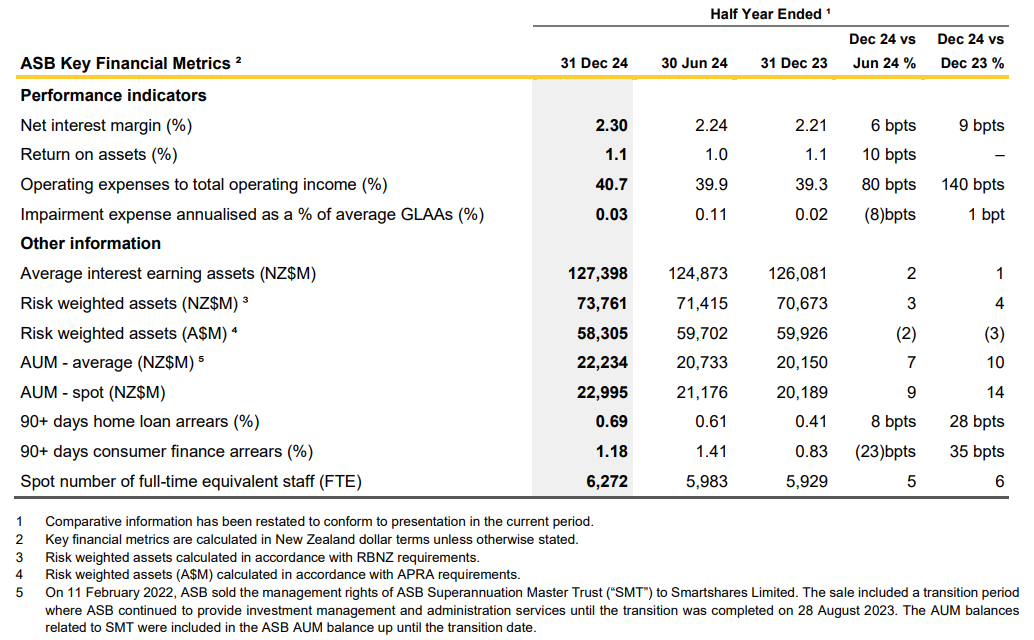

The bank's net interest margin climbed nine basis points to 2.30%, with the bank saying favourable interest rate hedging helped this. Net interest income was up $73 million to $1.546 billion. Other income rose $5 million to $230 million. Total operating income rose $78 million to $1.776 billion.

Operating expenses climbed $50 million, or 8%, to $697 million, with higher staff costs a key factor. The bank's cost to income ratio surged 140 basis points to 40.7%, and its return on equity dropped 60 basis points to 13.5%.

Impairment losses on loans rose $7 million to $17 million, which was attributed to higher consumer finance write-offs, increased home loan collective provisions reflecting interest rate and cost of living pressures, plus house price volatility.

Loans at least 90 days past due, but not impaired, rose $45 million between June and December last year to $487 million.

ASB says its profit increase reflects the 4% operating income rise driven by increased lending volumes and favourable interest rate hedging, albeit this was partially offset by the operating expense increase.

"New Zealand has been through the most difficult economic cycle in a generation, and we need to be patient with what looks like a gradual recovery. With lower interest rates and inflation providing some relief, and export incomes looking up for a number of sectors, our focus remains on supporting customers and providing capital for the next phase of economic growth," ASB CEO Vittoria Shortt says.

ASB's gross lending rose $2.565 billion, or 2%, between June 30 and December 30 last year to $112.194 billion. Home loan lending lifted $2.29 billion, or 3%, to $78.390 billion. That's 70% of the bank's total lending. Corporate lending, including rural lending, rose $319 million, or 1%, to $30.941 billion.

As of December 31, ASB's total regulatory capital stood at $11.987 billion, which was $5.348 billion more than its required minimum of $6.639 billion, the bank says.

Staff numbers jump

Between December 2023 and December 2024, ASB increased full-time staff numbers by 343, or 6%, to 6,272. This was attributed to managing financial and cyber-crime risk, mitigating the impact of fraud and scams, and supporting technology investment.

Salaries and other staff expenses increased $45 million, or 12%, to $429 million, with information technology costs up $13 million, or 10%, to $142 million.

"We are continuing to invest heavily in people, technology and awareness initiatives to protect Kiwis against fraud, scams, and cyber and financial crime and expect to spend another $140 million this financial year," says Shortt.

"While the volume of online banking fraud and scam cases increased 16%, customer losses were down a third in the year to December 2024. ASB stopped $29 million in suspicious card transactions in 2024 and responded to 18,000 after-hours calls to its 0800 ASB FRAUD hotline in the first year of 24/7 operations. Across the half year ASB identified and took down around 100 fake ASB websites, to prevent further harm from bank impersonation, a significant source of scams and fraud."

Commonwealth Bank of Australia, ASB's parent, posted a 2% rise in half-year cash NPAT to A$5.132 billion. A 5% dividend increase to A$2.25 sees 73% of cash NPAT paid out.

CBA's net interest margin rose two basis points to 2.08%, with its return on equity down 10 basis points to 13.7%.

ASB's paying $1.1 billion in half-year dividends, up from $800 million last year.

ASB's press release is here.

CBA's press release is here, its announcement is here, and CBA's presentation is here.

14 Comments

So there is more room for interest rate cuts then. HFL no more.

Yes, the banks can't wait to give the public all of this profit out of the kindness of their hearts.

end sarcasm.

Carved out of the CEO's $12m salary.... Not

ASB, one step ahead ...of you

Not out of kindness, but out of necessity due to competition.

clearly happening right now.

....our focus remains on supporting customers and providing capital for the next phase of economic growth,"

Shortt means to say the "next phase of credit creation for non-productive purposes". The idea of "providing capital" invokes all kinds of imagery of the mighty warriors of ASB negotiating deals with foreign investors. Of course most people see the likes of ASB as shrewd intermediaries cleverly lending out deposits and making a return from loans. The problem is that the ruling elite gives Shortt full license to speak with a forked tongue instead of being honest with the people - that the credit is created out of thin air and that ASB is really in the business of purchasing debt securities.

I see the process as.

ASB get asked to fund a $1mil mortgage in NZD, they put in their required amount (what 2.5%)? so $25k and they ask CBA treasury for the remaining 975k which is funded offshore at the current rate plus swap etc etc, So yes 975k is basically magicked into the NZ Economy, but it is real money. Someone expects to get there 975k back plus coupon.

Meanwhile ASB collects there average 2.30% on the entire 1mill, which is a pretty good return really unless things go wrong and credit risks appear.

its the ability of the big 4 to access these funding markets that allow them to be competitive, the smaller challenger banks cannot do this... unless we had our own Hone and Aroha version of Freddy and Fannie Mac.... then that smaller player could sell the debt security and rinse and repeat...

Its animal spirits that make this all work, and right now the animals seem to have no spirit to lend, perhaps because they do not see enough chance of risk free capital gains? its seems that RookieInvestor, TheMAN etc are simply not living up to their talk... not lifting enough weight on behalf of NZ.

if this was lending to small business or Agri the required amount ASB would be required to put in would be many times the 2.5% thus given a choice they would rather lend their capital to residential as the profit is simply better, I think federated farmers has a real gripe with banks , they see themselves as a better risk then a rental..... but banks charge them a lot more as they need to allocate more capital to the loan... RBNZ sets these minimum % amounts.

If the RBNZ wanted more productive lending for growth growth growth, they could adjust these amounts , until they do this banks will probably wring their hands and suggest to SMEs that perhaps they could just extend their home mortgage and put that money into the business that way as its "easier" for them...

Its always confused me who "them" is in this type case...

Maybe Luxy needs to ask RBNZ to view productive growth growth growth lending as lower risk then residential housing lending?

ASB get asked to fund a $1mil mortgage in NZD, they put in their required amount (what 2.5%)? so $25k and they ask CBA treasury for the remaining 975k which is funded offshore at the current rate plus swap etc etc, So yes 975k is basically magicked into the NZ Economy, but it is real money. Someone expects to get there 975k back plus coupon.

Wholesale funding on average accounts for 20% of Aussie bank lending. I don't think you're correct. This $975K ye speaketh is essentially created by keystroke as opposed to an offshore entity stumping up. Naturally it all balances - loans creates deposits - and capital ratios are maintained.

https://www.cfr.gov.au/publications/consultations/2024/review-into-smal…

Trebles all round!!

Pretty solid results, and quite reassuring given the current lacklustre status of the NZ economy.

WTF? Aussie (and Aotearoa) are awash with mortgage debt and this is the answer. This is why Shortt lives a charmed existence.

It will soon become easier for Australians with student loan debt to get a mortgage after Treasurer Jim Chalmers instructed the prudential regulator to relax how HECS was treated when banks conducted mortgage serviceability tests.

https://www.afr.com/policy/economy/aussies-with-hecs-debt-to-get-easier…

Seems they like a side of risk with their main of....risk. Smells of desperation in the air on that one.

Used to be good bank. Maybe they will again?

But look past the rates they offer, into the actual services they deliver ... and whether they actually deliver them ... without error ... on time ... and without much time wasting of my time - doing their job ... And they're pretty awful.

Won't go back to ASB until respected players have said the rot has stopped, the fix is in, and working!!!

Payment processing problems overnight , empty CAPE files.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.