The Commerce Commission plans to monitor and consult on scheme fees charged by Mastercard and Visa, saying it's concerned about "the complete lack of transparency" of these fees and "limited competitive constraints" on them.

The Commission makes these comments in its Interchange fee regulation for Mastercard and Visa networks - Draft Decision and Reasons Paper released on Wednesday.

Scheme fees are unregulated charges financial service providing merchant acquirers and card issuers pay the operators of card payment schemes like Mastercard and Visa for their services. They can include assessment fees, processing fees, licensing and access fees, and other fees. The Commission is concerned about the opaqueness of these fees, and their sizeable contribution to merchant service fees.

"Scheme fees are the second largest component of the merchant service fee [after interchange which is regulated] which also drive undue complexity and opaqueness of the merchant service fee. We are concerned about the complete lack of transparency related to these fees and the limited competitive constraints on these," the Commission says.

"Initial monitoring suggests that these fees differ considerably between Mastercard and Visa. We will continue to monitor these fees and provide further transparency of other components of the merchant service fee in future work."

Taking a lead from the UK

The Commission says it plans to consult on possible disclosure requirements for Mastercard and Visa on acquirer scheme fees next year. It notes scheme fees are currently being explored by the Payment System Regulator (PSR) in the United Kingdom.

"We will also need to actively monitor acquirer scheme fees to ensure these are not increasing to fund more favourable issuer compensation positions. This could involve, for example, requirements on Mastercard and Visa to disclose information on acquirer scheme fees. We intend to consult on any potential information disclosure requirements in the second half of 2025," the Commission says.

The PSR is undertaking a market review of scheme and processing fees associated with Mastercard and Visa, like New Zealand the UK's two largest card payment system operators.

The PSR says it launched the review following concerns a substantial proportion of prior fee increases to acquirers couldn't be explained by changes in the volume, value or mix of transactions.

"Based on the evidence it has gathered as part of this market review, the PSR estimates UK businesses pay more than £250 million extra annually due to these fee increases. UK businesses have little choice but to pay these increased costs as Mastercard and Visa cards account for 95% of transactions using UK-issued cards. We have provisionally found that Mastercard and Visa do not face effective competitive constraints," the PSR says.

Here, the Commission says net issuer scheme fees may be higher in NZ than in comparable jurisdictions.

"Currently the interchange fee regulation partially limits the ability for schemes to provide further rebates and discounts. This [interchange fee] draft decision proposes to change this, by instead requiring that an issuer's benefits from the scheme cannot exceed an issuer's payments to the scheme."

"The schemes can reduce an issuer's scheme fees, subject to an upper limit dictated by the value of the issuer's payments. However, we do not expect this to be funded in increases in acquirer scheme fees," the Commission says.

As interest.co.nz reported earlier this year, revenue Mastercard and Visa book includes a smorgasbord of fees such as; domestic assessment fees, cross-border volume fees/international transaction fees, transaction processing fees, service fees, data processing fees, and royalty fees.

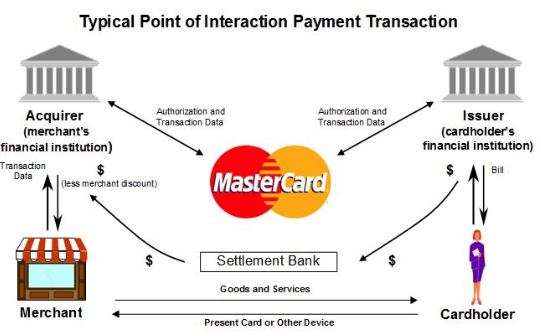

*The Mastercard diagram below highlights its network supporting what's referred to as a “four-party” payments network.

Evidence suggesting interchange fees directly relate to fraud prevention investment lacking

Meanwhile, the Commission's paper suggests lower interchange fees are both unlikely to have a material impact on fraud protection, and unlikely to materially increase losses to fraud across the retail payment system. (Also see this related article on the Commission paper focusing on proposals to lower interchange fees and surcharges).

The Commission argues that because both the costs of fraud and the benefits of fraud prevention are faced by multiple parties, it's reasonable for anti-fraud investment to be paid for by the same parties.

"As one of those parties, [card] issuers have an incentive to invest in fraud prevention, not only to reduce their own fraud losses, but also to maintain the reputation and integrity of their payment product, independent of interchange revenue," the Commission says.

"In addition to this, we have not found sufficient evidence to suggest the interchange fee is directly related to investment in fraud prevention and anti-fraud innovation by issuers."

"Regarding a reduction in interchange revenue, issuers also may recover their fraud prevention costs through other fees and revenue sources, i.e., investment in fraud prevention does not need to, and does not appear to, entirely come from interchange revenue," says the Commission.

"Therefore, we believe that lower interchange fees that we have proposed are unlikely to have a material impact on investment in fraud prevention and are unlikely to materially increase losses to fraud across the retail payment system. We welcome substantive quantitative evidence suggesting otherwise."

Change in consumer behaviour expected from surcharge reductions

The Commission also says it expects a change in consumer behaviour to result from surcharges "reducing to appropriate levels."

"We will likely see this in debit transactions being made by contactless payment instead of inserting or swiping the card when surcharges reduce to appropriate levels. Currently, excessive surcharges discourage some consumers from using contactless payment methods which they may find more convenient," the Commission says.

It acknowledges concerns raised "by multiple submitters" about non-designated (non-regulated) payments networks, such as American Express and buy now, pay later networks, having a competitive advantage by not being subject to regulation and interchange fee caps.

"We expect some consumers may migrate to higher cost payment methods. However, we consider the impact on efficiency will be limited because they currently have less merchant acceptance than Mastercard and Visa credit card networks due to higher costs, a gap that will increase. This limits the level of consumer adoption which would allow other networks to fully take advantage of reduced interchange fees on the Mastercard and Visa credit card networks," the Commission says.

"We also expect higher cost payment networks to respond similarly to when the initial interchange fee regulation came into force by reducing their costs to merchants. We will be closely monitoring these networks."

The Commission estimates consumers pay up to $150 million in surcharges annually, with between $45 million and $65 million of this stemming from "excessive" surcharges.

"Given the extent of excessive surcharging currently, it seems likely that some form of surcharging regulation will be needed. We expect to consult on surcharging regulation in the new year."

It says potential options to address excessive surcharging may include:

♦ A maximum surcharge based on average merchant service fees;

♦ A maximum surcharge based on average merchant service fees unless merchants display a certificate from their acquirer setting out their own average merchant service fee (in which case they could surcharge up to that rate), such certification would need to be renewed periodically;

♦ Any surcharge to require the display of a certificate from the business' acquirer documenting the business' average merchant service fee (in which case the surcharge could be up to that rate); and

♦ A requirement for terminal providers to sight evidence of a merchant’s average merchant service fee prior to uploading a surcharging rate higher than the average and to not allow a surcharge greater than that to be charged.

The Commission says it welcomes feedback on these "or other practical and enforceable options" to address "excessive" surcharging. Consultation is open until 5pm on February 18 next year.

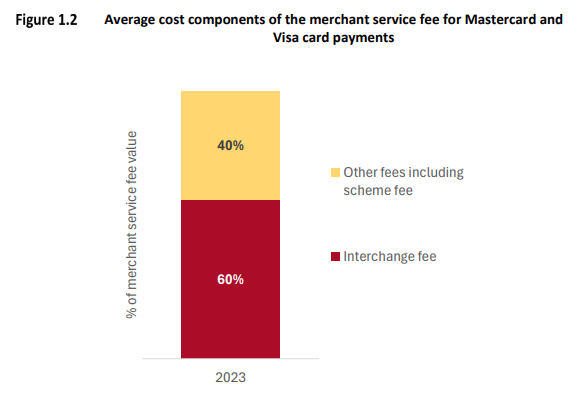

*Figure 1.2 below comes from the Commerce Commission's draft decisions and reasons paper.

*This article was first published in our email for paying subscribers first thing Thursday morning. See here for more details and how to subscribe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.