Sometimes in life it's interesting to imagine yourself in someone else's shoes and mull how they might be thinking about a certain issue.

Doing that from a big four bank CEO's perspective, what do I make of the Commerce Commission's final report from its market study into competition for personal banking services?

Am I quaking in my boots? Nope.

But that's not to say there aren't useful recommendations among the 14 from the Commission. There are. And the Government pledging to act on all 14 is encouraging for bank customers and New Zealanders more broadly because bank competition is now very much on the political agenda.

However, with the two key recommendations being; boosting Kiwibank's capital to try and turn it into a "maverick disruptor," and ensuring open banking is fully operational by 2026, it's unlikely to move the dial in the short to medium-term.

Speaking after the release of the report, Finance Minister Nicola Willis said with Kiwibank focused on its digital transformation, she didn't think any capital raising would happen until at least 2026. Kiwibank CEO Steve Jurkovich told interest.co.nz on Thursday, that is indeed the timeline the bank's working to.

The Commission's report says there's currently no disruptive maverick in NZ banking to shake-up the big four banks' oligopoly, which has them holding around 85% to 90% of NZ bank assets. It notes Kiwibank lacks the scale and capital backing to do the disrupting, and its business model doesn't vary significantly from the big four.

Open banking laggard

In terms of open banking, Kiwibank was given two years leniency over the big four, by when it needs to be technically and operationally ready to allow its customers to share financial data with third parties. Whilst ANZ, ASB, BNZ and Westpac have been, and are, working to deadlines this year, Kiwibank's are in 2026.

And Kiwibank has sounded far from enamoured with open banking. In a submission to the Commission it; "questioned the appropriateness of open banking for the New Zealand economy, and considered a cost-benefit analysis of the investment is required."

Cost-benefit analysis should consider which open banking use cases would deliver the greatest impact, the appropriate level of investment by industry, measures of success, the distribution of risk between participants, and the best legislative/regulatory vehicle for delivering it, Kiwibank said.

Citing "a real risk" NZ’s open banking framework could end up being "inappropriate for the relatively small size of the market, over capitalised, and underutilised," Kiwibank didn't sound much like a disruptive maverick.

On top of accessing hundreds of millions of dollars of new capital, and modernising its IT, some attitudinal change may also be needed at Kiwibank. Because like it or not, open banking is already underway, and coming to government-owned Kiwibank.

That's because the Commission recommendations the Government has pledged to implement include; "industry and the Government should commit to ensuring open banking is fully operational by June 2026," and "the Government should support open banking by being an early adopter." Politicians and their advisors are developing a consumer data right, giving people greater access to their own data and allowing it to be shared between businesses.

Lessons to learn

Speaking in our Of Interest podcast, Chairman John Small said on open banking the Commerce Commission looked closely at Australia and the United Kingdom, which are ahead of New Zealand, and thought about what lessons could be learned from their experiences.

It'd be fair to say open banking hasn't been a silver bullet for competition in either country yet.

Asked about UK uptake, the UK Competition and Markets Authority points to a July announcement saying there are 10 million consumers and small businesses "who have been empowered to take advantage of the benefits of open banking and manage their financial lives in new and innovative ways."

Despite this seemingly reasonable interest level, the new UK Labour government has announced plans for a Digital Information and Smart Data Bill saying, among other things; "open banking is the only active example of a regime that is comparable to a 'smart data scheme' – but needs a legislative framework to put it on a permanent footing, from which it can grow and expand."

Meanwhile asked for figures on the uptake of open banking in Australia, the Australian Competition and Consumer Commission says it's; "unable to provide the information at this time. Information on Consumer Data Right uptake is not currently publicly available."

Small acknowledges open banking hasn't yet hit a home run in Australia or the UK, saying; "it hasn't been a roaring success in either of those places. I think we can learn from both of them and do it a lot better."

In NZ open banking has been overseen to date by Payments NZ, whose shareholders/owners are ANZ, Westpac, BNZ, ASB, Kiwibank, TSB, HSBC and Citibank. And as the Commission's report notes, successive commerce and consumer affairs ministers have called for open banking progress back as far as Jacqui Dean in 2017, albeit leaving it up to a bank-owned company to oversee.

The Commission has also recommended Minister of Commerce and Consumer Affairs Andrew Bayly designate the interbank payment network under the Retail Payments System Act to support the delivery of open banking. This, it says, will enable the Commission to set rules and standards for the interbank payment network and act as a regulatory backstop for industry work developing APIs (application programming interfaces). The interbank payment network, it says, is; "all bank payment instruments between registered banks or within a registered bank for the payment of goods or services initiated by either a consumer or a merchant as payee and where payment instructions are sent directly to the payer's bank."

Sunlight on bank switching

Among other Commission recommendations is; "industry should invest in making improvements to its [bank] switching service," starting with greater promotion of the Payments NZ service and monitoring and reporting on service standards.

This switching service has been in place since 2010, but has been little promoted. That's bad enough. But on top of that, there's no public information available on how many people are switching banks, even though banks get monthly data on this.

Such information, the Productivity Commission said in 2014; "would help demonstrate the effectiveness of the current switching process and give consumers greater confidence about the ease of switching banks - hence sharpening the overall level of competition between banks."

Also notable is the Reserve Bank being told it should; "broaden the way it undertakes competition assessments" under the new Deposit Takers Act (DTA) and; "place more focus on reducing barriers to entry and expansion in the banking sector."

The Reserve Bank notes its proportionality framework; "taking a proportionate approach to balance the costs and benefits of regulation for different types of deposit takers," is part of the DTA. Furthermore it's; "consulting on graduated minimum capital requirements across groups of deposit takers, and potentially reducing the minimum dollar amount of capital required for new entrants [currently $30 million]." And is; "considering widening the use of the term ‘bank'."

How all this plays out is going to be fascinating given the Reserve Bank tends to get pretty feisty when told what to do, and rightly takes its responsibility for financial stability seriously. It pushed back hard, and successfully, when the Commission's interim report recommended it even up the regulatory capital playing field between the big four banks and the rest.

And this is what Governor Adrian Orr had to say in March;

The main work we do is not going to shift the competition dial very much at all. We can not just let lots and lots of small companies that will be unsafe or likely to fail [obtain bank or non-bank deposit taker registration] in the hope that it creates competition.

A political line in the sand

Ultimately though, what really caught my attention was the response of Willis in her press briefing after the Commission report was released. Below is a flavour;

"Our government is committed to delivering a more competitive banking sector so that New Zealanders can get a better deal. We do not intend to put this report on a shelf somewhere."

Willis says the Commerce Commission has proven what has been long-suspected, that NZ’s banking sector is uncompetitive, and Kiwis are not being well served by a highly profitable, two-tier oligopoly.

"Today’s report calls-out the market behaviour of New Zealand’s big four banks: they are highly profitable compared with international peers, they lack innovation and do not aggressively compete for customers."

"Instead, ‘competition’ between them resembles a cosy pillow fight, with profit margins coming first and everyday Kiwis coming second," she adds.

Whilst these are words not actions at this point, they are strong words and ones Willis and her government can be held to account for. She has drawn a line in the sand and the public should now rightly expect to see improved banking competition.

How politically charged could things get?

With the parliamentary select committee banking probe to come, and the competing political interests of the three coalition partners, let alone the opposition parties, there's plenty more water to flow under this particular bridge.

With farming lobby group Federated Farmers so vocal in calling for a rural banking probe, and coalition partners National and Act competing for rural votes, expect Reserve Bank regulatory capital settings to be a focus in the parliamentary inquiry. Indeed, among the terms of reference is;

Determine how and to what extent the RBNZ’s capital requirements and credit risk models influence lending rates (see emphasis in Rural Banking section).

When the Reserve Bank pushed through its new bank capital requirements in 2019, it was against the backdrop of Federated Farmers appearing to be hand in glove with bank lobby group, the New Zealand Banking Association (NZBA). In a press release on its biannual survey of farmers' satisfaction with their banks in June 2019, Federated Farmers oddly included the following;

[NZBA CEO Roger] Beaumont says the Bankers’ Association analysis shows the Reserve Bank’s proposal to almost double capital requirements will have a net cost to the New Zealand economy of $1.8 billion a year.

“Depending on individual banks’ commercial decisions, it’s fair to say there’s likely to be an impact on customers.”

It's certainly reasonable to expect the big four banks will be gagging to tell MPs their regulatory capital requirements are higher than they need to be. And Willis has said she's open to the debate. Watch this space.

On the other hand MPs may get drawn into a clash between Federated Farmers and the big banks over greenhouse gas emissions, climate change and environmental sustainability. The farmers' group accuses banks of "acting as pseudo-regulators" of farmers, and ASB CEO Vittoria Shortt says farmers need to take account of what their customers want.

Put a red circle around 2026

Ultimately, however, what the dual Commerce Commission and select committee probes mean for the big four banks remains to be seen. The demise of banks was touted as long ago as 1994 by none other than Microsoft founder Bill Gates, who described banks as "dinosaurs" that could be bypassed.

They have, however, survived thus far, and are good at partnering with threats to their business and finding new tickets to clip, something we're likely to see plenty of with fintechs and open banking.

Meanwhile, 2026 looms as potentially a make or break year for enhanced banking competition in NZ given the timeframe for Kiwibank's capital raising and deadline for fully operational open banking. With an election due that year, perhaps we might even have a contest of ideas on banking competition from our political parties?

There are no silver bullets in the Commission's report. But, if nothing else, the market study has put improved competition for banking services firmly on the political agenda, and provided impetus for, and evidence that, change is needed.

As for the politicians, I'll now be watching what they do, more than what they say.

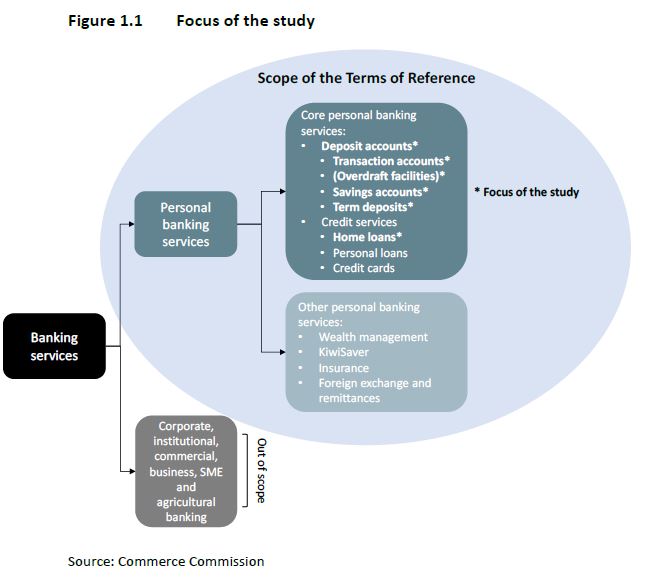

*The Commission's market study had a narrow focus on home loans and deposit accounts as demonstrated by figure 1.1 below. The recently launched select committee banking inquiry has a much broader focus.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

6 Comments

Open banking was never pushed hard by Labour, Kris Far Far Far away Foi, had his chance but the cool startups went offshore, its over now for NZ competition.

The only way to introduce competition is a secondary mortgage market like Fannie Mae or Freddy Mac, which we may need yet if we see a global recession really kick off.

Nice piece of racism to start your day IT - you must feel like a bigger man already.

A play on someone's surname is now racism? Get a grip.

I was at Telecom in the Mid naughts, and have been saying to the many Telco dispora that now live in banking that there are strong parallels to that situation. Once something becomes political, it becomes very unpredicatable and public. I think we can all agree that the banks are very cozy, and while a solid banking sector is a requirement, not as solid as the 'record profit' mob would be nice.

I would also caution that much of the pushback from the banks on how hard things are is complete BS. Why can't we have bank number portablity like we do in Telecommmunications? Too hard you see. Banks are in fact more like telco's than they want to believe, they just move 1s and 0's, with a risk framework on top.

And then Open banking - what a red herring. Technically open, commerically locked down tighter than a ducks bum. It won't affect any change.

"Why can't we have bank number portability...." Spot on. And that should at least be the very first step. How many of us shelve the idea of going somewhere else because we can't be bothered telling everyone what the new account number for customer payments; direct debit etc is.

Expect a big increase in marketing and lobbying efforts from the big four.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.