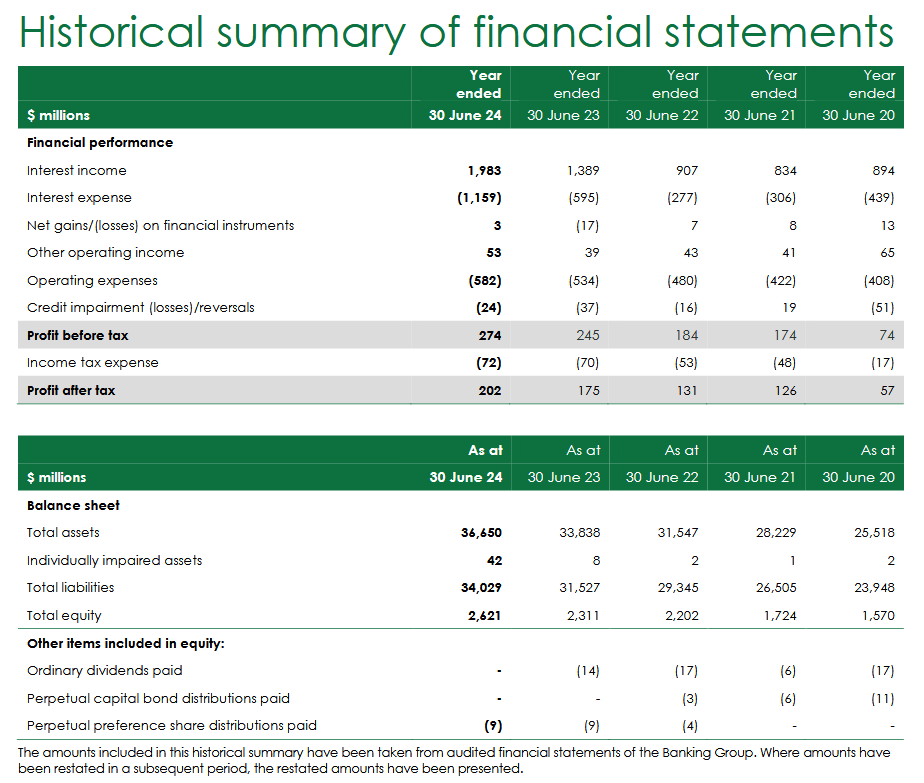

The would be 'maverick' of the New Zealand banking scene, Kiwibank, has posted a record $202 million after-tax profit for the year to June and says it is up for the challenge of taking on the big four banks.

The announcement of the 100% crown-owned bank's record earnings comes amid the backdrop of release of the Commerce Commission's final report into competition for personal banking services.

The Government response has included Finance Minister Nicola Willis asking Treasury to work with Kiwibank’s parent company, Kiwi Group Capital, to provide advice before the end of 2024 on options for raising new capital, including from KiwiSaver funds, New Zealand investment funds and investment from regular New Zealanders.

Willis said she shares the Commerce Commission’s vision for a stronger, more disruptive Kiwibank. "I want it to have the growth capital it needs to become a ‘maverick’ that exerts real competitive pressure on the big four."

Well, Kiwibank's saying it's ready for it.

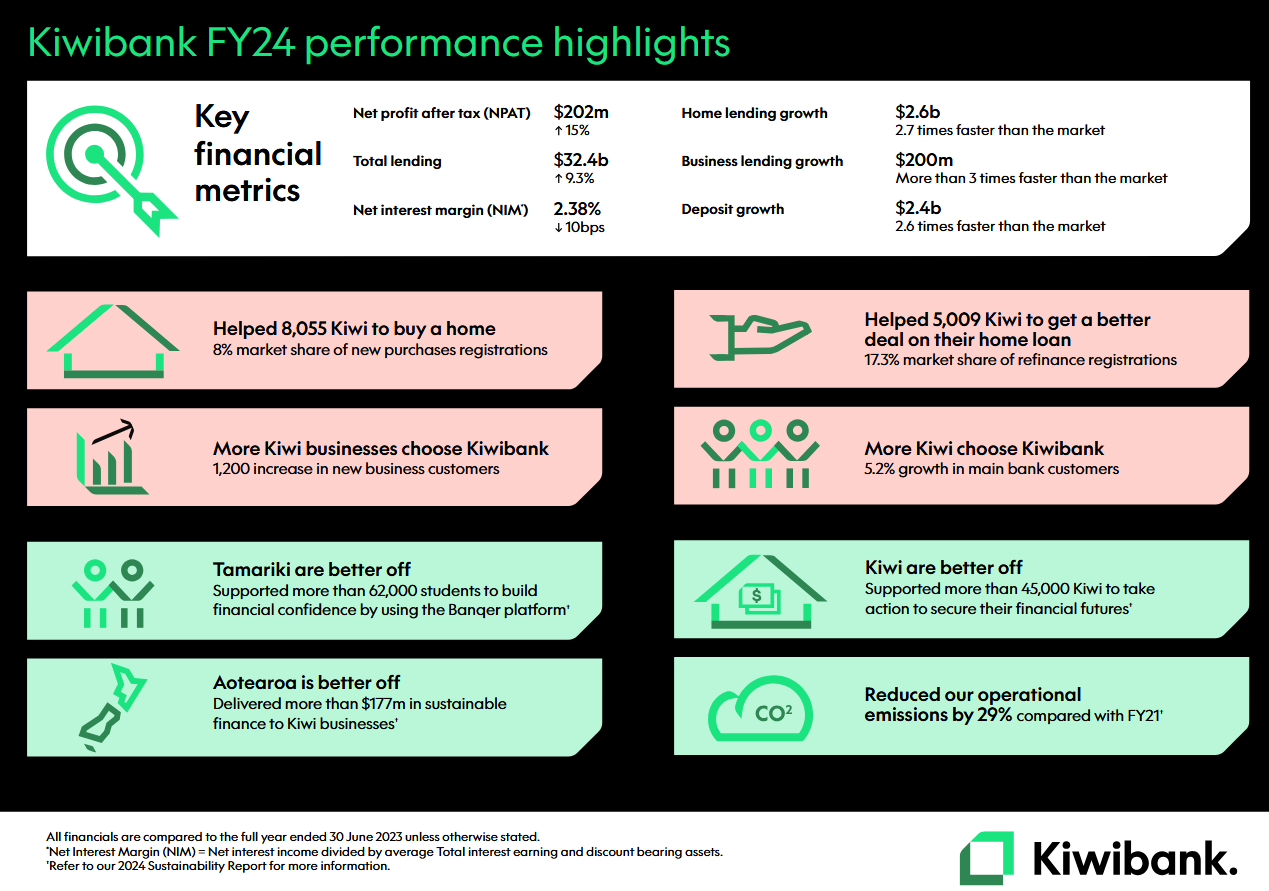

In announcing a 15% climb in after-tax profits and 9.3% growth in the lending book to $$32.4 billion, Kiwibank's chief executive Steve Jurkovich said Kiwibank was "up for the challenge of fulfilling the role of 'maverick' and taking on the large four banks".

"Kiwibank has been successfully growing market share for some time now, supported in part by $225 million of additional capital injected in July 2023 by our 100% shareholder, Kiwi Group Capital.

"We would welcome more access to capital over time to deliver on our Purpose. Kiwibank is currently focussed on a multi-year transformation that will deliver more scalable systems to enable it to further accelerate its current growth. Any future capital investment would need to take timing of the transformation into account in order to maximise value."

In terms of the financial year just finished, Jurkovich said Kiwibank had "once again outperformed the New Zealand banking market" while continuing to invest more than ever in its transformation to enable future growth and "deliver on its Purpose of Kiwi making Kiwi better off".

"For the fifth consecutive year, Kiwibank has improved its profitability and grown faster than our competition, as we continue to build a stronger asset for New Zealand with all our earnings staying right here.

"We know there’s plenty of choice out there, but today’s result shows once again that we are fulfilling our role as a disruptor, more Kiwi are choosing us, and momentum is on our side.”

Mr Jurkovich said Kiwibank recorded positive gains across nearly all key financial metrics in FY24, in a challenging economic environment.

The bank achieved net lending growth of $2.8 billion, growing its lending book by 9.3% to $32.4 billion. Home lending grew 2.7 times faster than the market and business lending more than 3 times faster than market. Deposits increased by $2.4 billion, growing the deposit book by 9.4% to $28.2 billion and 2.6 times faster than market growth.

"We’ve worked incredibly hard to build and maintain the trust of our customers during FY24 and to be there in those moments that matter."

Jurkovich said the Reserve Bank's decision to cut the Official Cash Rate last week [from 5.5% to 5.25%] was the "right thing to do" and that Kiwibank was forecasting twelve, 25 basis-point cuts, or 300bps in total.

"The magnitude of these rate cuts will be positive for Kiwi households and businesses looking to borrow and create momentum for the New Zealand economy.

"As inflation and interest rates come down, we expect to see a rise in confidence and a much more positive outlook heading into 2025 and beyond."

29 Comments

Very good news .... for Kiwi's regardless of whether they have an account.

For those that have an account it's not so good news, it's them that they made the money off.

Just look at uncompetitive their rates were last week. They have just dropped rates again today, and so did ASB, but kiwibank drops are twice the size, and at best match the ASB rates (1y) or are higher (everything else).

Good to see the post shop making some money.

Willis will be checking with JK on how she spins the selling of Kiwibank..for the good of the sheeple..(and to pay for those landlord taxbreaks and a Corolla)

... that depends upon how you define " selling Kiwibank " ... Willis has indicated that they could almost double Kiwibank's balance sheet by diluting the governments share from 100 % , down to 51 % ... allowing a massive expansion of the bank via an NZX listing ...

Which is a good thing , right ?

100 % , down to 51 % ..just like JK did with Meridian Energy. So the benefits to you and I this year with power prices has been? (Or has investors made millions)

Comparing apples & mangoes there ... the eclectic gentailers were sold down , $ billions pocketed by the Key gumnut ... and subsequently $ billions pocketed by KS funds & private investors as those eclectic companies grew their profits mightily... ...

... a different story here , the Luxom gumnut pockets nothing , nada , $ zero ... but ... KB pockets $ billions to fund it's growth ...

Maybe a Chairmanship after his 3 years when he is un-employed?

I wouldnt at all be surprised ... our nation is beset & hamstrung everywhichway you look by " jobs for the boys " ... rather than by selecting the most suitable candidate ...

How is Kiwi bank a maverick? They don't budge from their special rate card ( ANZ and BNZ both appear to be offering lower rates than the lowest "specials" on offer, via their app). This means that rather than competing Kiwi bank is just plain old more expensive.

"Home lending grew 2.7 times faster than the market....."

That's all that matters ....as long as the property market doesn't go belly-up. (NB: That... "and business lending more than 3 times faster than market" will more than likely be backed by the same collateral - property. And if Kiwibank wants to be anything but a small, mainstream bank, being a maverick is lending to business' based solely on business' case)

What does that lending growth mean in terms of marketshare?

Not at lot, they are still small, eg total assets above of 36.65B, the registered banks have $490billion in housing, personal loans and business lending, so they are still well less than 10% of that. (I left out agriculture, $63 billion as KB doesn't play in that market afaik)

From my mate Chatgpt. The trend is good, albeit a bit slow.

Also of interest, ANZ lost 10% market share in the last 20 years, going from 40% to 30%.

Here are the approximate mortgage market shares for Kiwibank over the last 10 years:

- **2014**: ~4.1%

- **2015**: ~4.3%

- **2016**: ~4.5%

- **2017**: ~4.7%

- **2018**: ~5.0%

- **2019**: ~5.3%

- **2020**: ~5.7%

- **2021**: ~6.0%

- **2022**: ~6.5%

- **2023**: ~7.0%

- **2024**: ~7.3%

These figures are based on estimates and growth trends from various financial reports and sources.

If that's correct, at the current growth rate they will hit 20% market share in ~15 years, which would put them on a similar scale to ASB, BNZ and Westpac, who are all around 20%, but would lose some market share to Kiwibank.

But as others have noted, to me Kiwibank's only real point of difference these days is that they're NZ owned and their profits stay in NZ. Interest rates appear to be broadly similar to the other banks, and the types of accounts are similar across all the major banks.

Given interest rates are actually reasonable at the moment, one idea would be an everyday chequing account that also carries interest similar to the various savings accounts. At the moment it's a bit of a pain moving money between accounts to get interest, but also ensure you always have enough for bills. I think something like that could be a reasonable draw card, though the other banks would likely match it.

They should use some of this profit to develop a decent app that its super easy to use, like ASB and ANZ have.

ASB business app is deplorable...and don't even mention ANZ- technology from the 80's

a bit of an exaggeration, i find them quite good and easy to use. Kiwibanks looks woeful.

Most of the apps in banking are a thin layer of modern web tech on a stack of steam-age stuff.. and that's fine because the old stuff works and doesn't need to change very often.

Strange comments - but new business are going around banks. Emerge.NZ - Business Credit Card app that connects to Xero - set up 10 cards in a day for a business team. ASB please fill in paperwork..talk to many people in the Bank...secure your life and we may issue you one begrudgingly in about 4 weeks.

I find kiwibanks mobile app is good, not as good as the co-ops but better than Westpac and BNZ.

You mean the highly insecure apps of ASB and ANZ that have such reduced functionality you might as well use the website. (have used and tested both and they are so insecure I would not trust them)

No surprises there.

Any lending institute will do very well in a low wage, high living cost environment like New Zealand.

Especially lending into the highly worshipped and sacred NZ property market.

Ahh! So that's why they want to privatise it now. The banks want less competition and the rich want to reap the profits.

... no , they have repeatedly said that they will not sell it ... emphasis on the word " not " ...

But they can add $NZ Billions to KB's balance sheet by allowing KS fund investment / or an NZX listing ...

... ergo , the governments net share of KB drops from 100 % ownership , to 51 % ... but the $ value of the state stake in KB remains unchanged ...

Long piece of string your playing with there Gummy...going to take a while to roll it back up this arvo?

All the better for stringing the blighters up if they lie to us ..

Prof Robert MacCulloch opines that if the government gifted every Kiwi kid a KS account with $ 100 in it , at age 10 ... we would create a new generation who's banking life & interest starts with KS ... an awesome advantage to take future kiwi bank customers away from joining the big 4 Aussie banks ... a true disruptor to their cosy pillow fight competition ...

That's a great idea, I like it.

KB also need to get to the point they can bank the Crown as well, that's when you know they are nearing the ability to compete with the 4.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.