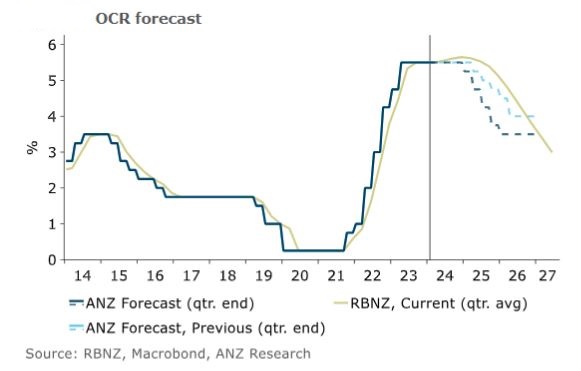

Economists at ANZ New Zealand, the country's biggest bank, have brought forward their forecast for the first in a series of Reserve Bank Official Cash Rate (OCR) cuts to February 2025 from May 2025.

"The Reserve Bank's concern about the run of higher-than-expected domestic inflation is understandable, but we expect that meaningful progress is around the corner. The real economy is very weak and given the vibe of 'soft data' - surveys, leading indicators and the like, we are now more confident in the weak economic outlook enshrined in our most recent Quarterly Economic Outlook. We've been talking for some time about the risks being tilted toward cuts starting earlier than May; we are now rebalancing the risks by moving our forecast to February," ANZ NZ's chief economist Sharon Zollner says.

The OCR's currently at 5.50%, where it has been since May 2023.

It's not the first time the ANZ economists have changed their OCR forecast this year. On January 18 they forecast "a steady sequence" of OCR cuts from August, taking the OCR to 3.5% over 12 months. Then on February 9 they changed their tune, saying they were now forecasting 25 basis points OCR increases on both February 28, and again at the Reserve Bank's April 10 review.

Following the Reserve Bank's February 28 monetary policy review, ANZ NZ's economists acknowledged; "We got this one totally wrong." However, they also said they still thought there was "a very strong chance" the next OCR move would be up rather than down. Nonetheless, they "reluctantly parked" their call for a higher OCR "back in the risk basket, and instead pushed out cuts to mid-2025." This subsequently became a more specific forecast for the first cut in May next year.

'That should do it'

Zollner says before cutting the OCR, the Reserve Bank needs to not only be confident that consumers price index (CPI) inflation is on its way to 2%, but that it can be reasonably expected to then stay within its 1% to 3% target band.

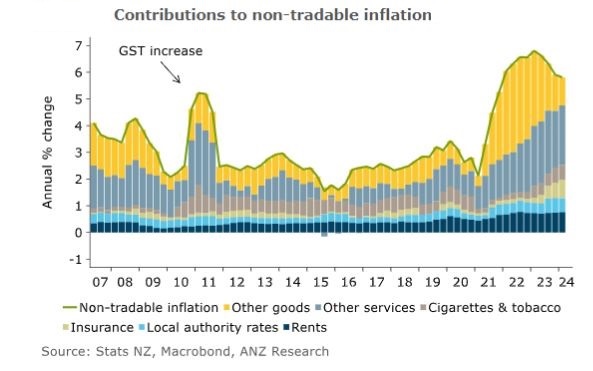

"Various combinations of activity and inflation outcomes could meet those criteria. But by February next year, we are anticipating that the Reserve Bank will have seen fourth quarter CPI inflation at 2.6% year-on-year, [with] non-tradable [inflation] still 4.7% year-on-year, but we are forecasting it to drop sub-4% the following quarter, and unemployment [to rise] through 5%. That should do it, in our view," Zollner says.

The March year CPI was 4%, Statistics NZ said, with the unemployment rate at 4.3%, or 134,000 people. Annual non-tradeable inflation, being inflation from domestic goods and services including rent, council rates, construction, cigarettes & tobacco and insurance, was running at 5.8%, with tradeable inflation, including imported goods such as petrol, at just 1.6%.

The ANZ NZ economists note the housing market "is currently moribund." ANZ NZ is the country's biggest housing lender with exposure of $107.5 billion at March 31.

"Beyond February, we have simply pencilled a 25 basis points cut at each [Reserve Bank monetary policy] meeting. The speed of cutting is not something we have a strong view on at present. Our forecast cuts stop with the OCR at 3.5%, i.e. neutral or thereabouts. Obviously if things really unravel the Reserve Bank is likely to be cutting much more quickly, and on the other side, if inflation doesn’t get all the way to 2%, or bounces meaningfully, cuts may come more slowly or cease," says Zollner.

The neutral OCR is the level at which it's deemed to neither stimulate nor constrain the economy. The Reserve Bank currently puts this at 2.75%.

"In terms of the risks around where rates ultimately settle, noting of course than in practice equilibrium is a purely theoretical construct, to the upside we’re mindful that sticky global inflation could mean it takes higher average interest rates to keep CPI inflation as low as it has been in the past. Conversely, we’re mindful that a negative economic shock could come along, necessitating an OCR well below neutral for a time," Zollner says.

The Reserve Bank itself isn't forecasting an OCR cut until August next year. Financial markets have a cut priced in for November this year. The Reserve Bank is scheduled to next review the OCR on July 10.

Meanwhile, on Thursday Infometrics' chief forecaster Gareth Kiernan changed his forecast for a first OCR cut to February next year from November this year.

"Although we don’t think a further delay in beginning to cut the OCR is necessarily the right move, the [Reserve] Bank’s backward-looking approach to setting monetary policy means that households and businesses will need to wait longer for any interest rate relief," Kiernan.

85 Comments

"Our forecast cuts stop with the OCR at 3.5%, i.e. neutral or thereabouts"

So a 2% drop in interest rates, probably over a long period of occasional 0.25% drops not starting until Feb. Will it be enough to turn the economy around again?

They need to get the economy back to a sustainable starting point. So much damage has been done it feels like it's a long road back to something that works.

Okay. Then could you explain why you are so enthusiastic about the OCR going even higher?

Because cheap debt is not really sustainable.

Did you mean "unlimited, or uncontrolled, cheap debt is not really sustainable"?

I think you did !!!!

The RBNZ can control both the quantity and the price of debt. (Albeit they're pretty hopeless at the former).

The RBNZs ability to control especially the quantity of debt is seriously constrained.....they may attempt to control it within the limits deemed acceptable by those who issue it.

As I have said before, our debt and housing-based economy will not properly start ‘improving’ meaningfully until the OCR is down to at least 4%. That’s not likely until at least late 2025.

We don't want the debt and housing based economy to improve. We need to kill it so we can grow a real economy in its place. It's no coincidence that all the usual suspects who thrive in an unproductive, rentier economy are agitating for OCR cuts.

Yes, interest rates should be used to curb inflation, not to kickstart the economy. RBNZ has no need to lower rates unless they feel inflation will go under 2%

@HGWR

Can you share your plan of how to grow a real economy?

An easy start, change the tax structure to remove the 'tax free capital gains' from residential property, so it is no longer such a tax favourable asset class, pushing investment from mum, dad, and everyone else, back towards business and other more productive endeavours.

Hahaha jesus fn ch*st... the first thing out of this guy's mouth to "grow a real economy" is to tax more... no wonder NZ is fked

He literally said "change the tax structure" not "tax more"

He meant tax more.

Very easy indeed, all you have to do is write some legislation.

The much, much harder part is in actually increasing productive active economic activity.

It's like saying the easy start to being a long distance endurance runner, is to stop eating donuts. Like, yeah that'll help, but the rest of it's exponentially harder.

I take your point, which is valid

Another way to look at it is: the way to get back to a normal weight is to have that surgery to eliminate the tumour to begin with

Both analogies (yours and mine) are using living organisms, which in the end describes the economy well enough: it has ways to survive and grow independent of the conditions. It's just a matter of what is stimulated to grow?

The issue is whether we can get back/revert to the mean.

When we embarked on Rogernomics/Neoliberal economics in the 80s, the theory was if we ditched manufacturing and have that be done by someone who could do it cheaper, we'd gravitate to higher paying tertiary industry.

That didn't really happen, almost everywhere in the West, and potentially can't happen to a level that supplants what was lost.

So it very well may be that real estate is what you invest in when deprived of any possible alternative.

I agree. Cranking up the housing market again would be a mistake. You know one definition of stupidity is doing the same thing again and expecting a different result.

You, like everyone else making the same observation, are missing the fact that recent changes (.e.g. DTIs) can be used to ensure that doesn't happen. I.e. "this time" won't be like "last time" (with the proviso that the RBNZ under current leadership is somewhat capricious).

The DTIs can be used thus but it presupposes that they will remain in place and at a restrictive rate....the banks (and various administrations ) have resisted their introduction for years and there is no reason to assume the decision to introduce them can not be undone.

What would an administration do should the internationally connected banks hand them an ultimatum do you think?

That's the theory. Here's property prices 9 years after a DTI was introduced.

https://www.google.com/search?q=ireland+house+prices+2024&client=ms-and…

We can maybe argue prices would be higher still if not for a DTI, but we can't really say DTIs substantively reduce house price inflation.

Can also argue that DTIs impact supply, which also drives up prices.

Right Chris, l am not as confident as you that regulations put in place will prevent another property bubble in time. Humans have short memories, especially across generations. And what’s to stop future governments removing dti restrictions? Sort of like reinstating interest tax deductibility for landlords. How about we try and direct some capital into productive enterprises, instead of importing debt so we can exchange houses with each other while driving prices up.

How about we try and direct some capital into productive enterprises

Like building an abundance of affordable housing?

Or even make something we could sell for foreign currency to make our trade deficit smaller.

The problem is the "something". What can we make here more efficiently or to a higher standard that someone else isn't already competitive in?

In a world where most countries run roughly the same algorithm, you need some serious entrepreneurship to advance yourself. Or an amazing crystal ball.

It's like trying to improve productivity via subsidy. The productivity should really be self funding, otherwise it's not genuinely productive.

Yes that’s why I put ‘improving’ in inverted commas

Dont forget that NZ is a country of SMEs.

SMEs need to use personal/family assets to raise funds.

Cant you see that small businesses are collapsing? They can't get funds.

Big business or mature businesses will do well.

Oh, but NZ LOVES to kill the productive sector.

Labour has distributed wealth from productivity to non-productivity got to stop soon surely and there is nothing left to take from the younger people.

Boomers and big business must be loving it... and for the record, I am very low on debt and not so young.

Interest rates are the symptom not the cause.

Let's not become too speculative and lose sight of the plot......

The aim must be to get inflation back within the band that RBNZ is required to maintain. If we don't do that, inflation will continue having a corrosive effect on the economy - including its devastating impact on building/construction costs, house prices and rents.

"Higher for longer" interest rates might seem bitter medicine to swallow to some people. But, from a longer term perspective encompassing economic stability and household welfare, it's not too difficult to justify.

TTP

So… be quick?

Has your account been hacked?

I was wondering the same thing. Maybe a bad trip?

8 months to the predicted cut. [In such a volatile world ] I wonder how many times their predictions will change in that time.

In my experience prediction revisions come in multiples... I'm sick of hearing squeaks from the ANZ already though hehe

The RBNZ will most likely cut in November. The economy is shrinking at such a fast rate that their hand will be forced. Having said that, Adrian Orr will probably come up with reasons not to cut, such as "inflation is sticky " blah blah blah

How will their hand be forced? They are not meant to be saviours of the economy.

Would trying to stimulate a f**ked economy maybe be a part of the whole “financial stability” thing they mention occasionally 🤔

Maybe recessions are a requirement of long term stability.

If the only way they can achieve financial stability is through very low interest rates and free money, then I would argue they haven't actually achieved long term financial stability.

100% agree…but trying to find stability (using months old data) surely requires them to both throttle, and boost our economy as needed. If NZ is absolutely cooked in 12 months wouldn’t they need to stimulate and the only tool they have is this up/down lever?

I don’t envy them…rates should never have got so low, households and businesses should be able to cope with current lending rates considering they’re not really outrageously high…but everything I read seems to be trending towards us being f**ked…I’d imagine they’ll panic and just kick the can further at some point over the next year unfortunately eh

I agree it will be November.

International cuts will come through.

NZD will increase a bit too much reducing NZs income from production.

Plus oil down and job losses will finally be showing up.

Let us hope the woke economy is yesterday's economy.

Just paid $6.50 for an item at the Warehouse today that they were selling for $9 a few months ago... profit led business gouged all they could until they killed the hands that fed them!

Recall the infinite monkey theorem? The one about monkeys typing away for long enough eventually coming up with Shakespeare?

Rephrase it with 'ANZ economists' and 'calling the OCR correctly'....

Either they (a) had the dartboard out at Thursday night drinks once again... or (b) the lending team asked them to soften their stance as it was frightening off potential buyers in a slowing housing market. I suspect it was (b). That said, I think their new "forecast" first cut date is more likely than their last "forecast".

In the current global, political and economic environment these ‘predictions’ are meaningless.

The current global, political and economic environment isn't much different to every day for the last 50+ years. (covid excepted - that was quite different.)

There's always stuff going on globally that could - but seldom does - derail things. (It all depends on which news sources you read - and place prominence on.)

Financial markets have a cut priced in for November this year, and this is what I think is going to happen. The economy is slowing down significantly. Keeping rates too high for too long would be a mistake as bad, if not worse, than the one made by Orr when he kept rates too low for too long.

Importantly fuel prices down quite a lot, although they are a bit volatile

Interesting to see the ANZ still use pencils.

Does anyone else in Auckland think the roads are generally much quieter? Maybe it’s partly because university classes are finished

Feels that way

I drove through Auckland at 9am this morning. It was much quieter than I expected. Pretty much got from North to South without any stops.

That’s all over NZ. Look at retail, hospitality and construction.

Will be interesting to look at traffic data

Actually look at transport companies. They're doing the worse at the moment. Less activity = less stuff moving about.

It’s a bit weird ey. A bit eerie. Is it a sign that our economy really has fallen off the cliff, ahead of lagging data?

Probably. Helicopter flights to Waiheke Island are way down. Which suggests that fewer people have a spare couple of grand to pop over to a vineyard for lunch at the moment. Seriously.

Literally thought the same thing yesterday. Wonder if more people trying to WFH to save costs as well?

Friday is always light traffic....

It’s been noticeably lighter throughout the week.

Not complaining- it’s nice!

But maybe not a great sign for the economy

Seasonal sickness? covid? keeping people at home perhaps.

It’s not a great time to be in transport and delivery. Insolvencies in the industry increased by 136% to 26 in the last quarter, compared to 11 in three months prior.

The next biggest quarterly increase was in business services ‒ think accounting, marketing, business consulting and the like ‒ which rose from 48 to 73 insolvencies, a 58% change.

Maybe a little. But still seems way quieter. Painter’s point is valid, and also I think a lot fewer construction vehicles around.

Bus trips are almost up to pre-covid levels. That's what you get when you invest in public transport, walking and cycling. Less congestion.

Is it not just the sign of tighter budgets and people slowly returning back to the office?

So this analysis is based on Qtr 1 2024? Alot has changed since then, almost an entire quarter

""Beyond February, we have simply pencilled a 25 basis points cut at each [Reserve Bank monetary policy] meeting. ..."

Which would be the WRONG thing to do.

The right thing to have done would have dropped by 0.25% beginning Nov '23 with longer gaps in between marked against falls in inflation.

The end point - say August '25 might have been the same but NZ's economy would have benefited from less inflationary pressures from ... wait for it ... high interest rates !!!!

ANZ doesn’t have a great track record of being right when it comes to this topic of late.

These guys have shifted the goalposts so many times they may as well be groundsmen with the credibility of a wet, several-day-old homeless' sock.

Question is, will the economy be completely destroyed by February? If not, maybe cuts should be held off for at least another year.

ANZ’s predictions are becoming embarrassing. They have no credibility- the only one placing value on it is our naive friend Painter.

Thumbnail for these 'meh' articles should be a crystal ball.

The first cut will come in August 24.

A weak GDP result on June 20th and a soft CPI number in July will be enough for Adrian Orr to panic and slash rates to save the day. Interest rates always fall much faster than they rise. The economy is broken and we just need the data to confirm it.

Yep been predicting August since the so called economists have changed their minds like three times already. Its going to be small like 25bps. Its not the size that matters is the signal for more cuts to come.

The DTI is now finally in place. I think that will allow the RBNZ to drop earlier than anticipated so I’m throwing my vote with that November crowd.

As TA would say... 'Survive until 25'

I thought it was "Prices up more in 24"

That's a given every year...

It only rhymes once a decade

Prices thrive in 25'... coming to a TA/Oneroof article soon.

Living on weetbix in 2026

Nothing to celebrate in 2028

Works better when reversed?

In '26, living on Weetbix

In '28; nothing to celebrate in 2028

This article is under the Banking/News caption but is it really? ANZ's forecasts recently could be under the captions Farcicle/#FakeNews couldn't they??

In a nutshell the RBNZ shouldn't take an ounce of notice of the economists at the ANZ. If I took any business advice from them I would be broke

They'd be better to just shut up, wouldn't they?

An open letter to the RBNZ

Are there any good trackers for economists predictions on rates and housing?

It would be good to see who is most accurate re ocr predictions, who is consistently calling bullish/bearish in the housing market. Something like what is done for Good Judgement guesses. Understand it would become very difficult to judge degrees of accuracy but anything done at all atm?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.