By Geof Mortlock*

The apparent fall-off in the applications for credit by individuals and small businesses in the last few months has raised concerns about the possible impact of changes made to lending law, with the coming into force on 1 December 2021 of tighter lending requirements under the Credit Contracts and Consumer Finance Act.

Concerns have also been raised as to the impact on residential lending – especially lending to first home buyers – arising from the Reserve Bank’s tightened loan-to-value ratio (LVR) restrictions, which came into effect on 1 November 2021.

The concerns in relation to the effects of the Credit Contracts and Consumer Finance Act have prompted the Minister of Commerce and Consumer Affairs, David Clark, to ask the Council of Financial Regulators to review the possible impact of this law change. The Council is made up of representatives from the Treasury, Reserve Bank, Financial Markets Authority, Commerce Commission and Ministry of Business, Innovation and Employment. For reasons that are not obvious, he has not tasked the Council with reviewing the impact of the Reserve Bank’s LVR policy.

There are many factors that will be influencing the demand for and supply of mortgage and other credit. Not least in these factors will be the increase in interest rates (and the expectation of more to come), increased building costs and an expectation of a weakening in residential property prices. These factors, together with a heightened caution by households as to the financial stress that likely lies ahead for many in this country, will undoubtedly dampen the demand for credit and the willingness of banks and non-bank lenders to provide it. These impacts on credit demand and availability are inevitable and part of any economic cycle. A heightened level of caution by households and small businesses in undertaking further borrowing is prudent and sensible in current conditions, especially given the high level of household debt that now prevails (one of the worst in the OECD). Equally, any prudent lender would be taking a more cautious approach to assessing applications for credit in the current economic and financial environment.

However, aside from these economic and financial considerations, the coming into force of new lending restrictions under the Credit Contracts and Consumer Finance Act and the tighter LVR rules for banks are significant impediments to lending – much more so than can be justified by the purported objectives of these regulatory initiatives.

The new lending requirements under the Credit Contracts and Consumer Finance Act have significantly increased the burden on banks and other lenders to assess the ability of borrowers to service the debt being applied for. Although it is reasonable that lenders should be required to undertake due diligence in this regard – as most were already doing as part of their own credit risk management processes – the new requirements are onerous by reference to the consumer credit requirements in many OECD countries and are making it much more difficult for individuals and small businesses to access credit.

The compliance costs for lenders are substantial and will be reflected in the price that borrowers pay for credit (either by fees or interest rates, or both).

The evidentiary burden placed on lenders to demonstrate that they have met the requirements of the Act is likely to be a significant factor in causing lenders to be much more probing and ultimately more cautious in determining credit decisions than would have been the case with a less intrusive set of requirements.

However well-intentioned the new requirements might have been, they are likely to have an injurious impact on many borrowers by denying them access to credit that, in a more enlightened and less cumbersome regulatory framework, they would have had. This is yet another case of a ‘nanny state’ approach to regulatory issues, such that government policy ostensibly seeks to protect borrowers from the predations of unscrupulous lenders, despite the reality that most lenders are not in that category. The resultant regulation is untargeted and disproportionate to the problem the requirements were intended to address. Moreover, the new requirements reflect this government’s apparent mindset that it is necessarily the fault of lenders if individuals end up with an unsustainable debt burden, rather than holding individuals to account for their own borrowing decisions.

These issues should have been foreseen by the government and its agencies. Submissions on the legislation, when it was being consulted on, raised concerns about the compliance burden of the proposals and the effect the proposals may have in impeding access by borrowers to credit. The untargeted nature of the regulatory requirements was a point raised by many observers at the time.

As is all too often the case, it appears that the legislative and regulatory process applied by the government was not sufficiently thorough. Problem definition was not adequately specified. Costs, risks and benefits were not sufficiently assessed. The regulatory impact assessment was undertaken too late in the process and prepared by the government agency that, by then, had presumably already made up its mind on what it wanted in new legislation. The regulatory impact assessment was therefore likely to have been ‘retro-fitted’ to justify the proposals. Treasury scrutiny of the regulatory impact assessment is likely to have been too little, too late, as is typically the case given the under-resourcing of Treasury’s regulatory impact assessment function. In sharp contrast, take a look across the Tasman at the regulatory assessment framework that has long operated there. Unlike Treasury here, the Office of Best Practice Regulation (OBPR) in Australia is relatively well resourced for the task of assessing regulatory impacts and has considerable power to reject proposals that do not stack up against analysis scrutinised by the OBPR.

Sadly, the poor quality of public policy decision-making is a familiar story in New Zealand. For many years, regulatory initiatives in many areas have been progressed by government agencies without adequate problem definition, specification of regulatory objectives, assessment of alternative options, and rigorous independent cost/benefit assessment. And it just keeps getting worse under this government – a government that has made an art form of rushing through half-baked policies based on poor problem definition and grossly inadequate assessment of costs, risks, and unintended impacts.

A review of the new requirements under the Credit Contracts and Consumer Finance Act is clearly needed. However, I fear that asking the Council of Financial Regulators to undertake a review of the Act is rather like asking a surgeon to review his own bungled operation. The regulatory agencies comprising the Council of Financial Regulators lack the independence to do a proper job of any review. Rather, they have incentives to justify the changes that were made and to downplay the concerns raised by lenders, borrowers and others. What is really needed is a truly independent review by relevant experts (who should not be confined to those with expertise in consumer credit regulation; the expertise needed is broader than that). And any such review needs to be based on thorough consultation with stakeholders, and especially with those at the coalface of lending. The review should be transparent and the results published in a way that enables all interested parties to assess the adequacy of the review and its findings.

The review should not be confined to the Credit Contracts and Consumer Finance Act. It should also look at the Reserve Bank’s dubious LVR requirement, which limits banks to having not more than 10% of their loan portfolio to owner-occupiers in the form of loans with a LVR of over 80%. This requirement was rushed through by the Reserve Bank in October last year with barely any consultation. The Reserve Bank’s consultation document lacked sufficient analysis of the argumentation relating to the LVR proposal. The cost/benefit analysis, such that it was, was retro-fitted to justify the policy, rather than being rigorous and objective. As is so often the case, any independent review by Treasury of the regulatory impact assessment prepared by the Reserve Bank was way too little and too late to make any difference to the outcome.

As I and other parties submitted at the time, the LVR proposal was not justifiable in terms of financial stability. Banks are not at risk of financial distress or failure as a result of home loans exceeding an LVR of 80%. Stress tests undertaken by the Reserve Bank have shown that banks can survive severe shocks to residential property prices. The Reserve Bank knows this. They know that high LVR loans do not pose an unmanageable risk to individual banks or to the financial system. They have used these arguments to justify the LVR restrictions in order moderate residential property price inflation, reduce pressure on the Reserve Bank to use interest rates to moderate inflationary pressures, and protect first home buyers from the prospect of a fall in property prices. But this is not what macroprudential policy is intended to do. Macroprudential policy should only be based on financial stability objectives; it should not be applied as a substitute for monetary policy or as a ‘welfare’ policy to ostensibly protect a category of borrowers from possible loss.

If the Reserve Bank had a legitimate basis for using macroprudential policy to moderate residential property price inflation, a much smarter and less clumsy way of doing it would be to have a more targeted use of LVRs in the credit risk weighting applied to calculate bank capital ratios. This would have enabled banks to decide for themselves how much they want to lend above an 80% LVR, but to hold a higher level of capital against any resultant exposures. The higher capital ratio would be reflected in a somewhat higher interest rate on high LVR loans. Under such an arrangement, many first home buyers, who are now being excluded from the mortgage market as a result of the Reserve Bank’s LVR policy, would have greater access to mortgage finance, but would likely pay a little more for it. And that would be a far better outcome than the one we now have. Instead, we have a central bank that uses macroprudential policy in a clumsy way, without adequate analysis of costs/benefits, without any meaningful consultation. The result is a policy framework that is poorly thought through and is having a completely avoidable credit rationing impact on households who are already being hit hard by economic forces.

What is needed now is a truly independent review of both the Credit Contracts and Consumer Finance Act and the Reserve Bank’s LVR rules. The review should be led by independent experts appointed by the Minister of Finance and Minister of Commerce and Consumer Affairs, and overseen by Treasury – not by the regulators. The review should be transparent and informed by meaningful consultation with all stakeholders.

Beyond these specific issues, there is a more fundamental need for a back-to-basics review of the regulatory formulation process in New Zealand, including a better framework for problem identification and specification of regulatory objectives. This should include an assessment of how the regulatory impact assessment process can be strengthened so that cost/benefit analyses occur at an early stage in the development of policy options and that such analysis is subject to rigorous scrutiny by a suitably resourced independent agency accountable to a minister other than the minister who is responsible for promoting the policy initiative.

We also need to assess whether a ‘merits review’ judicial framework should be adopted in New Zealand, similar to the one that has long been in place in Australia. Such a framework would strengthen the incentives for better quality regulation and provide stakeholders with a more effective means of challenging poor regulatory decision-making. But that is a topic for another article.

*Geof Mortlock is an independent financial consultant specializing in issues relating to financial stability, risk management, governance and regulation. He is Wellington based but undertakes consulting work mainly overseas, including for the IMF, World Bank, KPMG Australia and other international agencies. Geof has undertaken consultancy assignments in around 25 countries, including for many finance ministries, central banks and other regulatory authorities, as well as for banks and insurers. He has not been engaged by any financial institutions or industry bodies to provide consultancy services on the matters covered in this article.

116 Comments

However well-intentioned the new requirements might have been, they are likely to have an injurious impact on many borrowers by denying them access to credit that, in a more enlightened and less cumbersome regulatory framework, they would have had. This is yet another case of a ‘nanny state’ approach to regulatory issues, such that government policy ostensibly seeks to protect borrowers from the predations of unscrupulous lenders, despite the reality that most lenders are not in that category.

I'll start off by saying that I'm all for individual responsibility, and a hands-off approach to free-market economics.

That said, it's not enough for people to be able to make their own decisions about borrowing. They need to be able to make well-informed, rational decisions about their borrowing, and - financial literacy aside - for a long time now it has been impossible for them to do so, due to mispricing of risk.

There is no way to properly ascertain financial risk in a world where interest rates are so heavily manipulated downwards. Government and central bank policy has been used to deceive people into thinking that there is no risk in the world, at a time when risk has probably never been higher.

When the economic traffic signals are broken, people simply can't make decisions for themselves about borrowing. That's why these regulations are - unfortunately - necessary. They shouldn't be, not in a properly functioning economy, but the fact of the matter is that we don't have one of those anymore.

Given the correct information, people should be able to make their own decisions on affordability though don’t you think? I mean we have to make those decisions on a daily basis.

the change I would like to see is the US one where you just send the keys back to the bank and have no other liability. In this scenario people can make their own decisions and not really lose.

You refer to non-recourse lending which is not applicable in all states in the US.

Given the correct information

Right, but we're not being given the correct information. Interest rates are a risk premium, they're supposed to tell everyone how much risk is involved in a transaction. At the moment the market is telling us that lending and borrowing money is a risk-free proposition, which is complete nonsense at the best of times, but even more so at present. This is the economic equivalent of a lie, and if people believe it then the decisions they make as a result are very likely to be wrong.

The US is a bit of a special case. The "jingle mail" scenario you're talking about isn't a get out of jail free card, you still have to declare bankruptcy and destroy your credit rating in the process. However, it does mean that the bank is potentially on the hook for a lot more than what they are here.

At the moment the market is telling us that lending and borrowing money is a risk-free proposition, which is complete nonsense at the best of times, but even more so at present.

Not really.

Banks demand and get residential mortgage borrowers to pledge the house/land until the conditions of the loan (bank asset) are extinguished - repayment of P&I.

Banks are more interested in the return of their money than the return on it.

I am sure we had a conversation here Audaxes that banks don't lend money? Now they do?

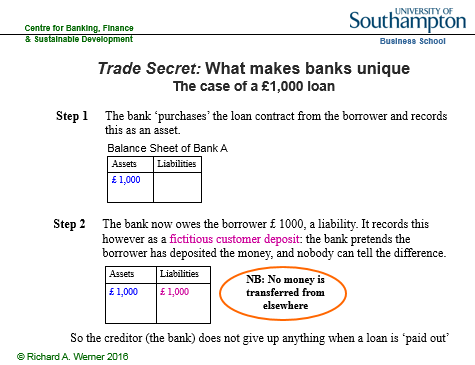

I have posted the written version many times: Here's an image: https://professorwerner.org/wp-content/uploads/2017/01/fig1.png

{kind=link}

The out of thin air recorded bank liability still needs to be repaid by the borrower to retire the bank asset (promissory note).

I owe you + you owe me + magic banking laws = Money out of thin air

Agreed, I once heard that "interest rate can only go down, there is no way for interest rate to go up. Don't worry about borrowing, the tenants will help you pay off the mortgage." Just look at where are we now... People should make their own decisions. Right. But there are always dumb decisions made by people and most likely those decisions will drag others into the consequences as well, especially we just discovered this new thing called FOMO, which most "wanna be home owners" people are under influence by. Sorry, no, please regulate...

Humans at core are greedy. In greed no one makes good decesions. Humans are also followers, they look at others and copy. They do what others are doing and follow even if it's a stupid thing.

Hence you cannot expect most individuals to make good decesions on their own. Most adults are like little kids, they need to taken care and told off so they do not create havoc and a mess.

A few intelligent humans have created this system of debt and interest for their own good but now it's become huge and covers every aspect of our life and they now they have to make good choices and policies to keep the system stable. The stupid will do their worst and if the system is unstable it creates worse for everyone. So intelligent need to control the stupid to do the worse. Credit control policy is one such measure to keep the system balanced.

Most adults are like little kids, they need to taken care and told off so they do not create havoc and a mess

I don't agree, and frankly this type of thinking is dangerous. Too much harm has been caused by people claiming to do things "for your own good". C. S. Lewis perhaps said it best:

Of all tyrannies, a tyranny sincerely exercised for the good of its victims may be the most oppressive. It would be better to live under robber barons than under omnipotent moral busybodies. The robber baron's cruelty may sometimes sleep, his cupidity may at some point be satiated; but those who torment us for our own good will torment us without end for they do so with the approval of their own conscience.

The most we can do is ensure that all relevant information is available for people to be able to make their own decisions, and learn to tolerate and accept any "wrong" ones. Pretending that the world should be, could be, or is perfect, is the exact same mentality which causes economists' predictions to be consistently inaccurate. When your modeling is based on assumptions like perfectly rational actors, and 100% efficiency, you're not going to produce answers which reflect reality in any way. Economics is just as much about human behaviour, and all the imperfections that go along with it, as it is about dollars and cents.

We don't live in a tyranny. It's called an election. When queen Jacinda cancels the elections I'll be the first to Mount barricades. But right now we are just talking stock standard speculation bubbles

The ccfa and all the other recent measures were needed due to the stimulus levels being pulled that have created the massive asset inflation.

Articles like this are just vested interest complaints.

No one saying get rid of the cccfa now was complaining about near zero interest lending artificially propping up Prices etc.

Its a credit cycle. Just need to adjust your personal and business activities accordingly

The CCCFA isn't achieving anything that a properly functioning economy shouldn't be able to do on it's own. I agree that at the moment it is necessary, but it's necessary because we don't have a properly functioning economy, not because we need to save people from themselves.

I like your posts.

With the RBNZ (and global central banks) in a tightening monetary policy regime, the CCCFA really has dramatically cut off the velocity of money/ circulation in the real economy. Even if CCCFA is revoked or amended with less strict implications, credit will be inhibited by households and corporates due to the human behaviour of tightening the purse strings due to (1) uncertainty of the future and future cash flows and (2) increasing cost of money from higher interest rates PARTICULARLY at a time of over-indebtness amongst households and businesses.

The challenge for central banks regulators is they're "between a rock and a hard place" by (1) needing to maintain financial stability and/or price stability and (2) acting responsibility by implementing the necessary interest rate hikes to mitigate against high and rising inflation. For central banks, if they fail to raise rates, assets prices may continue to rise posing an even larger bust when it occurs vs. if they hike rates, it poses a risk to financial stability due to widespread defaults if they hike rates too quickly.

The banking industry has a gripe with regulations, time to trot out Geof Mortlock to do some lobbying and frame it as an “independent” voice. Basically every article written he has written for interest is criticising a regulator on behalf of the banking industry. Shameless

*edit* removed the word, "pay", as that may have been a step too far.

Agreed. An "independent" voice who adds on to the almost daily slugging away at the CCCFA by MSM. Granny Herald is a leader in treating the CCCFA as a punching bag. If parties concerned had actually been practising prudent lending in the first instance ( as they vocferously claim to be), why did the govt feel compelled to introduce this law??

Just to be very clear, I have never been engaged by any person, bank or industry association to write any article for any news media outlet. I have not been engaged by anyone to consult in relation to the matters covered in this article. I write an article from time to time when I believe I have something useful to say on a topic. This is such an example. So please refrain from making accusations that are completely incorrect. Your comments should focus on the issues addressed by the article and be substantive and well reasoned in nature.

Geoff, I'm embarrassed by Miguel's ignorant, accusatory comment above. Sadly it represents the majority of comments here, as exemplified by the number of up votes

That reflects the anger out there with the status quo and the vested interests that feed off it and have milked it for all it's worth.

Indeed posts written out of anger, devoid of reason or logic. Attacking the writer who doesn't deserve it.

I agree a personal attack is underserved. All I am trying to say is that people need to try and understand the anger. There are very good reasons for it.

That reflects the anger out there with the status quo and the vested interests that feed off it and have milked it for all it's worth

Most people don't pay much attention to how the status quo / vested interests have been the real winners in all this. Now that the open bar is looking like a mess (drunks everywhere, top shelf whiskey all gone, the bar staff are either leaving or threatening to quit), nobody has any new ideas how to keep the party going.

Never in my 74 years on this earth have I seen so many interest groups with axes to grind. In a pandemic or war there will always be winners and losers. I think that the Government has made a pretty good fist of managing the pandemic in the face of competing self-interest groups each chanting how hard done by they are.

Emerson, the NZ Herald's resident cartoonist, summed up the situation brilliantly when he depicted Ardern surrounded by cats each wandering off or around in different directions; the caption was: "Herding cats.....".

Ardern is not just the Prime Minister, she is also the chief "cat herder".

Re the PMs placing NZers into effective lockdowns and closing the border for returning kiwis - we’ll see how the Auckland mayoralty race pans out and whether the Labor-sympathetic incumbent gets thrown out or not. By the likes of Leo Molloy or similar which will give the govt some good feedback.

People start arguing and fighting with the bouncer next...

oh wait

Just to be very clear, I have never been engaged by any person, bank or industry association to write any article for any news media outlet

No disrespect Geoff, but given your professional background (APRA, KPMG, central banks), it's going to be clear that your outlook will be shaped in some degree by the institutional position. It's always useful to know this in understanding how you may weigh the interests of different stakeholders.

I suppose you would rather listen to your local baker or a mate at the pub or another "like minded" commenter about the CCCFA because they don't have "vested interests".

The stupidity on this comments section knows no bounds

David Chaston, to satisfy most of your commenters, could you from now on publish articles by people that are not specialists in the field on hand. Please get the local mechanic to write about interest rates, a WINZ beneficiary about the economy and maybe a dentist about housing.

Actually let's take this all the way, you are a journalist therefore by their logic you should no more write on Interest, it might be best to get a supermarket employee to lead Interest's editorial.

That’s how I personally perceive Stuff

I suppose you would rather listen to your local baker or a mate at the pub or another "like minded" commenter about the CCCFA because they don't have "vested interests".

That's not what I said. I said that outlooks for those who come from institutional backgrounds will be shaped by their experience and peers. The problem here is that "oversight of independent regulation" is often done by those with backgrounds in entities who are conflicted to some degree. As I said before, no disrespect to Geoff, he has professional experience with certain entities such as APRA who are funded by the industries it regulates.

No, J.C. made a very valid and reasonable point.

He didn't attack the author, rather he pointed out the author's links to the status quo that have continued to advocate for, and profit from, the way things have been for a very long time.

I agree. I think it is very difficult to be truly independent when even if you haven't been engaged on the specific topic, you are speaking in relation to a policy that has severely hampered your main clients who pay your bills on a regular basis.

I'm not saying you can't pull that off Geof, I don't know you as a person, but it's a long shot for most people, and I think you may be so embedded in the industry's view points you may struggle to see it from the average end of line customers view point.

Regardless of what's been happening in other OECD countries and how readily available debt is there, the damage it is causing / has caused in NZ is clear from all sorts of angles.

This is one approach that is actually starting to redress that, it may be a slightly imperfect vehicle, (they all are usually) but I say not a moment too late.

Plus when you use comments like "nanny state" to describe the current government of the day, you are using subjective and unhelpful language in any independent and professional debate. So you open yourself further to these criticisms.

Can you say none of your consultancy work is done for any of the Banks in New Zealand or their parents in Australia? Unless the answer is a hard 'No" then we can't take you as an independent voice, as expressing views contrary to their interests could jeopardize future work.

Lets take a look at your article history. RBNZ starts investigating capital requirements for Banks late 2018. You then did a slew of articles criticizing a range of aspects about RBNZ governance, including several directly attacking the proposed capital rules.

Perhaps I missed them, but I can't remember reading a single article that was critical of any of the New Zealand Banks, or critical of actions by the RBNZ that would be favorable to the NZ banking industry. Every article i've read seems to advocate for the interests of the Banking industry, so call be cynical, but if quacks like a duck, walks like a duck etc etc.

David Chaston, to satisfy most of your commenters, could you from now on publish articles by people that are not specialists in the field on hand. Please get the local mechanic to write about interest rates, a WINZ beneficiary about the economy and maybe a dentist about housing.

Actually let's take this all the way, you are a journalist therefore by their logic you should no more write on Interest, it might be best to get a supermarket employee to lead Interest's editorial.

Stop using a strawman argument, nobody was saying that you should publish unqualified opinions, just that working for banks makes at the very least seem bias.

Can you say none of your consultancy work is done for any of the Banks in New Zealand or their parents in Australia? Unless the answer is a hard 'No" then we can't take you as an independent voice, as expressing views contrary to their interests could jeopardize future work.

Agree 100%. That's how it works.

I would almost expect to see an article like this on One Roof... A lot of noise but simply filled with with assumptions:

they are likely to have an injurious impact on many borrowers by denying them access to credit

Surely to call for a review you'd need some real world cases - with detail - that show the impact of the legislation. Or how about some stats - decline rates etc...?

Perhaps some need to give the legislation time to bed in? Rather than crying foul just after 1-2 months of it being implemented.

Can we please also address the elephant in the room and why we may need this legislation: NZ - largest property bubble in the world.

Hold on Nifty, just a few days ago, when I stated that the CCCFA was preventing some people from obtaining finance you argued tooth and nail that this was not true.

If so, surely you shouldn't have a problem with a review of the CCCFA.

Try to be consistent in your posts, it helps with credibility.

Calm down Yvil, not sure what you're getting at? It seems very consistent to me with what I've been saying. It's another article with no stats or real case studies showing what impact CCCFA is having. There's approx 6 'likely' statements in this article about CCCFA. 'Likely' doesn't warrant a review. If it did, we'd be reviewing everything...what a waste of money that would be huh.

So you still think the CCCFA doesn't prevent some people from getting a mortgage? Yes or No?

Let's revisit your initial comment:

the CCCFA pretty much ends the FHB's dream of borrowing money

Yeah, I still totally disagree with that...FHB's can still borrow.

Here's the problem... people need to borrow excessively in NZ to purchase a home. CCCFA is making banks check what they should of always been checking - income, expenses and outgoings. Now this is required to be done & evidenced, it's 'likely' reducing the amount people can borrow.

Example - someone had a preapproval for 1 million, proposed purchase 1.2 million... it expired - they had to reapply. Under CCCFA the bank rechecked their expenses more thoroughly and noted they actually had a few credit cards showing in their credit check & and a payment for loan showing in their bank statement. They didn't spend $100 per week on food/takeaways/coffees, it was actually $250 per week. After taking this expenditure into account they could now only borrow $700k, proposed purchase $900k. The person wasn't happy- they went to the media about it furious because they couldnt buy what they wanted due to 'spending to much on coffees'... One Roof headline 'CCCFA locks first home buyer out of market for having too much coffee' They don't disclose any detail about their credit cards or loans in the article...

So what's the real issue here... is it CCCFA? Or is it the fact that people can't really afford borrow to buy at these unsustainable & over inflated prices? Did banks not do what they were meant to be doing in the first place? Does the market just need to adjust? Do people just need to start reducing their debt/expenses? This is where we need to hear real cases (with full detail) and stats to see what's actually happening out there.

Stop deflecting the question:

Do you still think the CCCFA doesn't prevent some people from getting a mortgage?

Yes or No?

You're not providing any answers Yvil, just seems like you've got your knickers in a twist...

People have always been declined mortgages, for a variety of reasons. I have no doubt that some have been declined due to CCCFA but I would suspect for good reason. Mostly as I've explained it would be a matter of not being able to borrow as much... But hey, as I've also said we're not geting the full story or detail in these articles...so it's hard to tell.

Do you have any real cases or stats that you can speak of or are you going to refer me back to 'independent economist' Tony Alexander that makes the bulk of his money from the Real Estate Industry?

So you don't understand "Yes" or "No".

It would help if you stopped changing the question, Yvil. First you claimed that the CCFA was making it:

extremely difficult for a couple on average income to get finance to buy a house with these new strict rules.

To which the right response is that it was already extremely difficult for a couple on an average income to get finance to buy a house, given current house prices.

Then it was that:

the CCCFA pretty much ends the FHB's dream of borrowing money, so it doesn't matter about vendors [with regards to meeting the market].

As was pointed out to you, there's a difference between not being able to borrow as much as you want and not being able to borrow anything at all. And so far, you haven't produced a solid example of someone who was not able to borrow anything at all due to the CCFA, let along large numbers of FHBs in general not being able to borrow any money at all, which is what would need to be the case for your statement to be true.

Now you want to know:

Do you still think the CCCFA doesn't prevent some people from getting a mortgage?

To which the answer is yes, it's possible that there is at least one person who could have borrowed sufficient money to buy a house under the previous rules and now borrow any money at all. But again, not one single example of a case like that has been provided. But it's not clear what you are trying to do with any of this, other than consistently weakening your claim hoping other people won't notice, in order to claim 'victory' when you get some other commenter to 'admit' something both obvious and that obviously wasn't your original claim.

But in any case, a lot of this is beside the point. What's more important is this: not whether the CCFA makes it more difficult than it did previously, but whether the CCFA is actually appropriate or not on its own merits. And for that we need more than some Herald story light on details apart from someone saying a trip to Kmart cost them a mortgage.

Wow, that's a lot of words for nothing. The question to Nifty has always been the same:

"So you still think the CCCFA doesn't prevent some people from getting a mortgage? Yes or No?"

There's no need to write a novel,

Yes or No

The question to Nifty has always been the same

No it hasn't, as I just pointed out to you using quotes from your own posts. Just saying something is 'nothing' and complaining that it was too long for you doesn't actually refute the point.

By the way, he's already answered that question.

Do you not understand how

I have no doubt that some have been declined due to CCCFA but I would suspect for good reason.

is an answer to the question:

So you still think the CCCFA doesn't prevent some people from getting a mortgage?

Hopefully this post is short enough for you.

Yes or No

Yvil - we all know your 'yes or no' answer to this right now: https://ibb.co/xShrzZB

And Yes - I agree with a123 comments above

Nifty1

You have answered the YES/NO question posed. And answered it very well. No use bloodying yourself banging your head against a wall if that question is persisted.

The whole point is to make it harder to lend money to people who can't afford it. So the answer is yes it makes it harder for first home buyers to borrow, AS INTENDED. Hopefully in the long run it will mean people will borrow less and house prices will come down making buying houses more affordable.

no surprise that financial consultants are lobbying against any kind of blue sky law or regulation that will hinder the flow of money available for speculation.

Most small business borrowing is secured by property in this country and most kiwis work in a SME.

So what happens now that nobody can borrow? Zero investment in new fit-outs, materials, vehicles and IT systems?

This is going to head backwards very fast. A lot faster than the government tries to blame the banks.

All those gleefully pointing at house prices should be nervously speaking with their bosses instead.

CCCFA doesn't apply to businesses...

Any decent loan needs to be secured. In nz this is nearly always against a personally owned property. Making it hard to access credit for housing will always have a big impact on sme,s

I think you'll find if borrowing under a business and the loan is secured against a family home, CCCFA doesn't apply...

I think a lot of that borrowing is along the lines of creating a home loan overdraft and drawing down to fund a business. In the past that's been far easier, quicker and cheaper than obtaining a business loan.

Yes it does

Credit contracts not covered by the CCCFA

A contract is not a consumer credit contract when:

- the credit is for commercial or investment purposes — lenders may get a declaration from customers that the credit is for business or investment

- the total amount to be paid is due within two months and the debt equals the sale price of the products or services

- a borrower goes into overdraft without the lender’s prior agreement

- the borrower is acting as a trustee of a family trust

- it is a student loan under the Student Loan Scheme.

https://www.consumerprotection.govt.nz/general-help/consumer-laws/credi…

Totally agree that there should be independent reviews of the CCCFA and LVR changes.

The extra costs imposed on banks, applicants & mortgage brokers is a total waste of money.

It reduces the efficiency & effectiveness of NZ’s financial system.

It also creates more inequality as renters now face a much bigger hurdle to get a mortgage.

If you are a Labour supporter think carefully about what this government has done to its biggest support group (ie renters).

Renters now face reducing rental supply caused by excessive regulations against private landlords. Rents will continue to accelerate due to the idiotic changes made by this government.

Was there any private review of govt action to prop up the market over the last decade ?

Exactly. And any so called independent review would merely deliver the bias of the ‘independent’ review member.

I look forward to these rules reversing the property madness that has been going on for too long.

I am seeing for rent signs popping up everywhere, very unusual. Is this the reduction in rentals you speak of captain ?

Probably that time of the year.

RE: RBNZ culpability:

Thus instead of the central banking narrative that lower rates lead to higher growth, the empirical and verifiable reality is that higher growth leads to higher rates and lower growth leads to lower rates. If rates are the result of growth, they cannot be the cause.

This raises some new questions. Firstly, if it is not interest rates that drive growth, what then? And secondly, why do central banks keep insisting that they are using interest rates as their main monetary policy tool, when this is simply impossible? Recently, central banks have been lowering rates, while proclaiming that this is a measure to stimulate the economy. But the empirically verifiable fact is that they lowered rates, because economic growth has decelerated. Falling growth means interest rates must follow down. And what has been the role of central banks in the growth slowdown preceding the lower rates? We may presume that they had not used their vast powers to engineer economic growth – powers they worked hard to obtain in previous decades, in the form of independence with little meaningful accountability.

Instead of unravelling this mystery, central bankers have been making counter-factual assertions about the causation of interest rates and growth. Yet we know them to be in possession of thousands of highly trained staff and the best quantitative data sources on the economy of anyone. Since the hypothesis of complete incompetence or irrationality is a last resort, it stands to reason to adopt the working hypothesis that central banks have employed these counter-factual assertions on purpose. Two reasons come to mind: Firstly, they are using the interest rate narrative in order to suggest that they are adopting beneficial policies, when this may not really be the case. Secondly, they may in this way be able to distract public attention from the true causal relationships in the economy. In this case, a far less benevolent interpretation of central bank policy becomes suggestive.

As Forder (2002) has argued, obfuscation has served central banks particularly well since they have become so all-powerful: the danger for them in this era of unprecedented powers is that the general public may simply (and rightly) link bad economic outcomes to bad economic policies adopted by central banks, not to the – now far less powerful – governments. In other words, since almost all economic keys have been handed over to the central banks, one can reasonably expect them to be blamed for the economic mess that is such a recurring feature of economic policy during those decades of ever greater central bank power. As a defense mechanism, central banks could be expected to argue that they are doing all in their power to help the economy, while pinning the blame on other actors. But for this to work, observers need to be misinformed about what the true levers of monetary policy are.

A desire by central banks to misinform would explain why they have spent vast resources on “economic research” – pseudo-scientific writings that are often far removed from reality, but are designed to place any blame for the terrible economic performance that they have been responsible for on other actors – preferably the government, fiscal policy or ‘irrational’ and ‘uneducated’ ordinary people who are looking for ‘easy answers’ or seeking ‘populist explanations’, while anyone contemplating the possibility that big banks and central banks might not always look after the public interest and instead might collude in order to put their own objectives first is identified as a ‘conspiracy theorist’. In other words, the “economic research” produced by central banks is usually of a kind that at best looks like political PR to objective observers, if not outright propaganda. Link

'If rates are the result of growth, they cannot be the cause'.

Actually they can be both. Feedback loops blah blah.

The rate of interest – the price of money – is said to be a key policy tool. Economics has in general emphasised prices. This theoretical bias results from the axiomatic-deductive methodology centring on equilibrium. Without equilibrium, quantity constraints are more important than prices in determining market outcomes. In disequilibrium, interest rates should be far less useful as policy variable, and economics should be more concerned with quantities (including resource constraints). To investigate, we test the received belief that lower interest rates result in higher growth and higher rates result in lower growth. Examining the relationship between 3-month and 10-year benchmark rates and nominal GDP growth over half a century in four of the five largest economies we find that interest rates follow GDP growth and are consistently positively correlated with growth. If policy-makers really aimed at setting rates consistent with a recovery, they would need to raise them. We conclude that conventional monetary policy as operated by central banks for the past half-century is fundamentally flawed. Policy-makers had better focus on the quantity variables that cause growth.

Audaxes

Keith Woodford in an article about a week or so ago implied that the mathematics used by economists is overly simplistic and outdated.

Do you think that economists should by now be incorporating the Standard Model equation into their analyses and projections to regain their credibility. (The Standard Model equation is that used by quantum theory physicists and mathematicians to explain everything about the world that is known at the present time.)

The noted British mathematician and theoretical physicist, David Tong, has recommend this improvement.

I would be interested to know your thoughts on this.

What is the Standard Model equation in respect of interest rates impacting GDP growth or not ?

Do you mean replacing: The Use of (DSGE) Models in Central Bank Forecasting: The FRBNY Experience?

There you go again, confining your thinking about economics in terms of outdated existing models instead of incorporating universal models (e.g. the Standard Model) which apply to all fields of knowledge that use mathematics in their analyses and projections.

This was Keith Woodford's gripe in his recent article which surely must have read....he explicitly criticized economists for using outdated equations as David Tong obliquely did when he made a joke at economists' expense alluding to their use of outdated models and equations in a lecture delivered at the Royal Institution in 2017:

https://www.youtube.com/watch?v=zNVQfWC_evg (around the 29.22 minute mark)

Banks are now looking at what someone takes home each pay packet and then what their regular expenses are. And we are crying because banks aren’t giving loans where the repayments are larger than the individuals left over income after doing the income - expenses calculation??

The only reason for removing LVRs is to add more fuel to the fire and transfer wealth from first home buyers to boomers exiting the market.

Banks are assuming that nobody who takes out a mortgage can alter their spending to pay for their largest new expense. Why decline someone because they had a couple of coffees a week? People have changed their lifestyles to pay off their home for a few generations, but now we are assumed to be incapable of running our own lives.

I don’t buy this logic - to maximise my deposit and prepare for a fortnightly mortgage being debuted from my account, I remember significantly cutting my expenses before I bought my first house

Well said JJS

Banks have NEVER operated like this, and cashflow and servicing has been important post-GFC to all banks.

The problem now is that banks are scrutinising unreasonably and are unable to apply discretion (some may say common sense). One example I saw last week was someone being questioned that she had no takeaway food spend in the past 12 months. Her response is that she doesn’t eat out for health and cost reasons, and so prefers to eat in. Her banks response was that she was basically hiding expenditure from them because everyone eats takeouts…

Mortgage broker ?

No! Wouldn’t touch a banking career with a 19 foot pole! I have in laws in banking.

Review of LVR....seriously.

LVR and DTI as a tool to protect FHB who over expose themselves under FOMO should not be touched. More than LVR, it is DTI that should be implemented asap but no word on it even after six months from rbnz. With his policy of kicking the tin down the road, Mr Orr earlier confirmed that will take time but will have DTI by early 2022, now that we are in 2022 - WHERE IS IT MR ORR.

All those FHB who thought that interest rates will be very low for next several year and house price keep going up are being saved from being sucked into pyramid ponzi.

This all noise is not for FHB (Who are already SC$#@) but to protect vested biased lobby who are enjoying continuation of ponzi.

If someone is really interested in helping FHB, let the market take its own course and fall. A fall of 10% when prices have gone up from $900000 to 1.3million will be good for fundamental and also to calm FOMO and bring some sort of normalcy in the housing sector.

The ticket clippers seem to be very unhappy about something.

I can't quite pinpoint what it is.

Orr ask for DTI in December 2020

https://www.interest.co.nz/news/108367/reserve-bank-happy-have-more-reg…

After six months gets the tool or will get

https://www.interest.co.nz/news/110868/finance-minister-gives-rbnz-debt…

Now after six months, evrryone is silent but will soon find excuse to kick the can down the time.

Should ask Mr Orr, is the so called consultation even started.

In 50 years of working life I have never seen such foolish behaviour in the property market as in the last 2 years , and here we have somebody wanting the brakes taken off . How about looking back at how quick the reserve bank was in taking the brakes off a couple of years ago it took them only days to release any constraints on finance for housing and to dump interest rates to record lows. I hope the taxpayers are never expected to bailout any of the results of this stupidity , a fall in house prices should be expected and a substantial fall at that .

When we look back over the last few years we should be asking what actions a competent reserve bank governor and a competent finance minister would have been taking.

Then contrast it with the abysmal performance we got from Orr and Robertson.

Then question why on earth are they still in their roles in 2022.

Well TBH Guv'na Orr hasnt been in the office all that much lately

I'm glad you mentioned Robertson. Many commentators on this website have been nailing Orr to the mast while omitting any mention of Robertson. This is very convenient for Robertson as a political animal. He has more legal tools (the Reserve Bank Act) in his chest that he either doesn't know about or did not care to use otherwise the results of those decisions would have fallen on him. Those tools would have allowed him to act more decisively in reeling in the RBNZ but then he would have to share any fall out from them.

I've read the remit between him and Orr some time in either 2020/21 and its a poorly written document. If any of the govt lawyers wrote this the they need to go back to legal school.

How you apportion blame between them is up to each reader. Mine would be 50/50

50/50, I probably agree, although it may be 60/40 in favour of Robertson.

The amendments that GR led to the Reserve Bank Act were missteps of the highest order.

If the system becomes unstable, it's not the taxpayer bail out which we should be worried about. The whole cash and money system which we are used to these days is in the cloud somewhere. You don't know it's in the country or offshore or even if it's real. RBNZ doesn't secure or insure even 5% of the money in the system.

Any instability of it happens, we all are in for a very rude shock.

The present day government policies have let us get to this point. Be very scared.

Yes I think the last several years has shown that there are a lot of people out there who may well have made some money in property, but don't necessarily have a high level of financial literacy. Anyone can make money in a stacked environment when you have access to cheap debt, property, shares or whatever.

The challenge comes when things change as they are currently, a lot of people never thought this day would come. I personally know several people who have recently talked of buying investment properties and when I asked why the answer was always "Well everyone else is and its easy money". When I question them further pretty much none of them had any knowledge of such things as the current rate of inflation, role of RBNZ, current RBNZ Governor, current minister of finance, the current OCR, yet they are prepared to jump in to a $700,000 investment no questions asked.

Similar with shares, the amount of people currently squealing that they are "losing thousands" in the value of their shares in recent weeks! So the expectation is that shares (like property) can only go up??? Where is that written! Scary stuff but reality is you take the risk thats fine, but if the worst comes to pass you wear the consequences as well.

my customers can't over borrow and i can't make money from them !!! cry me a river

There will be more and more squealing as the year progresses.

I've also been fascinated to read pieces early in the new year by people with vested interest talking up the housing and share markets and general economy. Usually they preface their opinions with 'challenging times', 'volatile' etc. before going on to pretty much say everything is going to be fine, if not booming.

The scary thing is most people who read the articles will probably believe it.

Quite fascinating to observe.

Yes, please have a review and get rid of the CCCFA so the banks can let me, and a million like me, go long on mortgage debt and when we get in trouble the govt will panic and crush real rates down even further into negative territory to rescue us at the cost of savers. I expect help from savers to let me buy property.

There, I used the 'expect' word, which has magical powers in Nyow Zillun. Let the review commence.

I would put money on the government folding on this.

We know who they listen to the most.

However, by the time they have reviewed it and made changes, the economy will be toast.

Your missing the point.

Any toast as you put it was inevitable.

Before covid after, it doesn't matter. As a country we have been exponentially running up a credit card tab to our house price bubble.

Credit cycles are inevitable.

Many people borrowing money need protection from themselves. Crunch time is coming and everyone should get the Memo before its to late. People need to batten down the hatches because we are sailing into uncharted territory. Start paying down that debt and quit taking on more.

Today, one can borrow to any extreme as they need not worry for you have rbnz and Jacinda more worried than the person borrowing as it is their reputation which is at stake as they are feeding debt.

Aspects of the CCCFA will have to be rolled back to some extent otherwise the overall economy will halt - and faster with rising interest rates & ongoing lockdowns/border closures.

When a household buys a house with a mortgage a whole raft of economic activity results - way beyond the house purchase: business finance, household goods purchasing, credit creation, etc.

Reasonnable (a bit lenghy) article by Geoff. I especially agree with the "nanny state" criticism which takes away personal freedom to supposedly "protect everyone"

Haha that was the one part that I thought discredited the professionalism and independence of the whole article!

Love the different view points on this website...

Interesting, innit, that most commenters have taken a biased, binary approach to the article: either its that CCCFA&LVR are perfect and need to be left alone to continue their Good Work, or that fiddling with either equals Open Slather.

Whereas what the author is suggesting, surely, is that the present one size fits all approach needs to be refined into one where differing financial.situations require more or less or different regulatory treatment.

A rough analogy is speed limits. Sure, a 10km/hr blanket speed limit would get the road toll down in a hurry. But it would also crash the economy.......trade-offs everywhere....

It is interesting that banks are willing to lend, and people are willing to borrow on an asset (housing) where between 1/3 and 1/2 of the value is made up of non-value-added costs, ie the banks are lending, and the purchaser taking a mortgage on hot air: it does exist except for the fact that its value is artificially created by restrictive monopoly polices.

Nice article, there should be a law, everyone cannot think straight, and then greed takes over rationality.

There is a common perception in kiwis, if you want to make money take as much debt as you can, they consider NZ govt will never fail them which is happening in the last few years which leads to crazy inflation with no accountability.

And these banks will make unimaginable profits backed up by govt. which is unfair, also in the worst-case scenarios like quakes or tsunamis if people default the savers will lose all their money, we have to consider all the points rather than giving a free hand to crazy debt takers.

AJ123, This perception is fed and fuelled by likes of Orr and Jacinda.

Promoting Greed and FOMO to create debt ridden society to remain in power.

While I would normally agree with your Nanny State argument, if you have a large portion of the population behaving irrationally and doing the same thing over and over until their demise and the whole countries demise, then it warrants some extreme rules put in place to stop that behavior.

Great article.

CCCFA most likely going to be temporary contributing the market slowing down. The entire humanity is driven by debt with the odd artificial cycles. Contact tracing and mask wearing will slow things down but eventually things/people move on.

After CCCFA was introduced I recently got approved for same amount as before CCCFA, even though I had some expenditures during Christmas. So I am not sure what everyone is crying about.

When market was growing and becoming unaffordable people were saying nothing is being done to moderate is growth. Now when market is stalled and about to turn everyone is crying about not getting enough credit to buy. "What do you want?! Ever increasing capital gains?!"

My understanding is that people with vested interested had led vendors and buyers to believe that house prices would always keep on increasing and when they are sensing that market is about to turn then to save face they need a scapegoat and that scapegoat is CCCFA. Wait for few weeks and you would see all the property experts and especially the property bulls (some very big names) mention that they were caught off guard by CCCFA. "We would have been right and the market would have been more bullish if not for CCCFA". However with everything that's happening its becoming more and more clearer that cheap credit seems to be the major cause responsible for aggressive house price growth.

My basic understanding is when buyers wont be able to meet vendor expectation then vendors would have to realign their expectations accordingly and that would bring market correction, I am not sure what its magnitude would be - small or big. So if you are a buyers and not getting more credit then market will meet you there don't panic and stay calm. Don't give into the FOMO.

I may be wrong but the real reason for credit tightening could be that money or foreign investments are about to move out or become more expensive due to upcoming FED rate hike. May be banks are anticipating this and trying to save people from stretching beyond capacity. And on top of everything the big squeeze is here. People haven't felt its full effects yet, after few more weeks everyone will realize it true impact.

Vested interests exist all over the place . Cognitive bias etc has existed since man started walking this earth.

.

She/He who dies with the most debt wins.

1) Mechanic and Interest Rates

Yes sure, they'll probably tell you spare parts have increased in price due to supply issues.

2) WINZ beneficiary & Economy

Yep, cost of living is too high.

3) Dentist and Housing

Have no money 'cause prices are so high, so have to put the practise on the house

That was fun

I've not really seen this point discussed, but it seems to me that you are not made worse off by being allowed to borrow less for a scarce resource so long as everyone else is subject to the same rules, which seems to be the case here. In fact you are made better off, because in theory at least if everyone's lending ability is reduced, then the amount of money chasing houses is reduced, and the prices should go down, meaning that the fact that you (and everyone else) were not allowed to borrow as much has resulted in you (and everyone else) not having to borrow as much. So rather than the new requirements being 'injurious' to borrowers by denying them credit, they in fact benefit borrowers because credit for everyone - including them - is harder to access.

Nail on the head. Most people challenging the changes could care less about the FHB. They want to know that future FHBs will have enough access to debt to be the next greater fools.

Yes although there are no guarantees, complex markets etc, but logically this change has enough behind it that it could and should move things further in the direction that removing interest deductibility for property investors started.

Not a moment too late. And I have all my fingers and toes crossed.

More background on how the law & code is unworkable

https://www.oneroof.co.nz/news/40804?utm_source=nzherald&utm_medium=nzh…

Interesting. I see in the article TA has weighed in: "The question now is how to fix the mess. Independent economist Tony Alexander has suggested separating consumer credit lending by predatory lenders on one hand and on the other mortgage lending."

Given this started out as an attempt to save punters from a housing hyper-bubble, TA's suggestion would be a brilliant way to completely defang the changes and get those finance floodgates open again.

Who calls himself as Independent economist. Him highlighting in itselves suggests that he is not and everyknow the truth.

Wild idea, maybe allow the housing market to correct so that lending for an average (or lower quartile for that matter) house isn't considered high risk? We've been chasing the equity bubble with frivolous debt for too long. Taking out a half mill or more shouldn't be easy for most households, full stop. Six or seven times gross household income is too much, particularly in the face of increasing inflation and imminent interest rate hikes. It's frankly irrational how far the bar has moved on what people consider a normal level of debt.

A good article.. What also needs to be counted is the large number of non bank lenders who will no longer lend on consumer contracts – the CCCFA, the disputes resolution process – the risk of lending to consumers is now too high, so many in this group now lend only on commercial contracts. The objectives of this legislation is laudable however the undoubted loser is the consumer

I’d like to see all regulators (Reserve Bank, FMA, Comcom, Trustee/supervisors) have a compulsory rotation of work in the sectors they regulate. They can’t possibly know how businesses they regulate operate unless they have first-hand experience - in the business. How about running the operation of this CCCFA legislation through a cost:benefit test? Whilst at it, lets add in the anti money laundering laws – I suspect the application of this legislation too would fail dismally a cost:benefit test

"... a government that has made an art form of rushing through half-baked policies."

Beautifully written and I haven't seen the phrase for a while.

We will look in hindsight the cause of NZ's very own economic collapse and ponder.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.