ANZ New Zealand's interim profit rose 18% helped by a significant reversal in credit impairment charges and a red hot housing market.

The bank's net profit after tax for the six months to March 31 rose $141 million, or 18%, to $930 million from $789 million in the same period of the bank's previous financial year.

After a $232 million credit impairment charge in the March half last year, ANZ NZ reported a $70 million release this time. Meanwhile, ANZ NZ's expenses were down $64 million, or 8%, to $764 million. Operating income rose $33 million, or 2%, to $2.025 billion, with net interest income up $13 million to $1.661 billion.

With rival the Westpac Banking Corporation reviewing its ownership of Westpac NZ, ANZ Banking Group CEO Shayne Elliott was upbeat on his bank's NZ subsidiary.

"New Zealand continued its recent strong performance with record lending growth combined with disciplined cost management. This is a well run business that is an important part of our overall portfolio and is well placed to manage increased regulatory capital demands," Elliott said.

ANZ NZ CEO Antonia Watson told interest.co.nz she took Elliott's comments "as a vote of support," and was unaware of any suggestion the ANZ Group might want to follow Westpac and review the ownership of its Kiwi unit. Watson noted that ANZ NZ contributes between 25% and 30% of ANZ Group profit. That makes it a significantly bigger contributor to group profit than Westpac NZ, ASB to its parent Commonwealth Bank of Australia, or BNZ to the National Australia Bank.

Watson said ANZ NZ's cost reductions were due to lower personal costs, a series of "simplification initiatives," and the September 2020 sale of finance company UDC. The simplification initiatives included automation, straight through processing and developments with digital tools, Watson said.

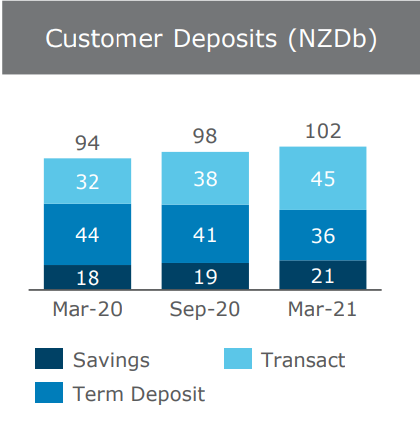

ANZ NZ, the country's biggest bank and biggest home lender, grew customer deposits 2% and increased gross lending 4% between September last year and March this year.

Home lending up almost $6 billion to 69% of all ANZ NZ lending

On housing, Watson said the market had "defied expectations" due to historically low interest and deposit rates, reduced loan-to-value ratio restrictions, and supply constraints. ANZ NZ's home lending increased $5.8 billion during the six months to March 31.

"It's in everyone's interests for residential property prices to be sustainable long term, and for home ownership to be accessible to as many people as possible," Watson said.

Figures released by the ANZ Group show ANZ's NZ home loan market share at March 31 was down 10 basis points year-on-year at 30.6%, with total home lending at $95 billion. Housing grew as a share of ANZ's total NZ geography lending to 69% at March 31 from 64% a year earlier.

Meanwhile, Watson said the full impact of COVID-19 on the NZ economy is yet to play out, although sectors like housing, construction and agriculture have proven resilient.

"Across the economy, businesses have generally fared better than we expected so we've been able to release around 25% of the additional credit provisions we had put in place since the start of the pandemic," Watson said.

"While there's room for optimism, we also know the impact on the economy is uneven."

"Sectors that relied on overseas visitors, such as education, hospitality and tourism, have been disproportionately affected and we've seen first-hand the challenges facing our customers in those industries," Watson said.

"As we look ahead, a full recovery is still some way off. Economic confidence will take time to be restored as residual impacts of the pandemic are felt."

At March 31 ANZ NZ's total capital ratio, as a percentage of risk weighted assets, was 15.9%. That's up from 14.4% at September 30 last year. The Reserve Bank's new regulatory capital requirements, being phased in over seven years from July next year, mean ANZ NZ will require a total capital ratio of 18%. ANZ NZ isn't paying an interim dividend to its Aussie parent.

Figures released by the ANZ Group show the net interest margin for its NZ division at 2.32% in the March half, up one basis point year-on-year. The NZ division cost-to-income ratio was down 340 basis points to 38.3%.

The chart below from the ANZ Group shows movements in ANZ NZ deposits.

ANZ NZ's press release is here, and the ANZ Group release is here.

2 Comments

ANZ NZ CEO Antonia Watson said the cost reduction was due to lower personal costs, a series of "simplification initiatives,"...

Did Henry Ford famously pay his employees enough to purchase the product they were manufacturing?

Banks reaping big profits....they will be going "yeeeeehaaaaa!!"

And if it all goes belly-up, we'll have to bail them out. 'Too Big To Fail'.

How good is moral hazard!!??!!

'Privatize the profits, socialize the losses'.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.