Home loan borrowers were convinced in 2024 that future fixed rates would be lower.

And the turn lower of the OCR encouraged that view.

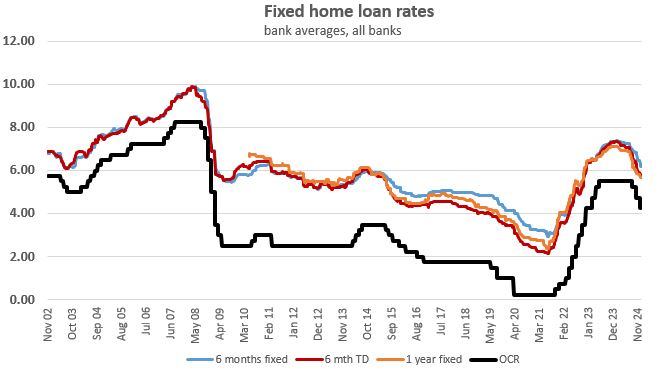

But history clearly shows that even though the OCR may fall, mortgage rates don't fall as fast.

So, if the OCR continues to fall in 2025 - and wholesale markets are suggesting that, absent new unexpected conditions that need to be prices in - then will fixed rates follow - but at a slower pace?

Despite the barbeque philosophy that "banks will conspire to keep them up", that in fact probably won't be the reason, just as it wasn't in earlier similar cycles.

Banks are constrained by regulation. They have core funding and mismatch regulations to meet. In turn that means they must raise an outsized share of their funds in the "non-market" sector (that is, from depositors). They will need to pay enough to stay competitive on the term deposit and savings account front no matter what the OCR is. And in 2025 they will have to start paying the deposit guarantee levy. (You can see our analysis of the term deposit sector here.)

And behind all that is the "market sector" where they raise wholesale funds. And at present, it seems clear that international rates will remain relatively higher for longer as some major economies are still struggling to tame inflation, especially the US.

Paying 'more' for local savings, and paying 'more' for wholesale funding, will inevitably mean fixed rate mortgages won't fall as fast at the OCR is expected to.

History also shows this. Prior to 2008, the difference between the one year fixed rate and the OCR averaged +1.25% over the six years we tracked. Then the OCR fell sharply as the GFC bit, and from 2009 to early 2023 that same margin averaged +2.70%. But then this latest trimming cycle for the OCR has gathered pace, and that difference has fallen to just over +1.50%. And that cycle is still far from finished.

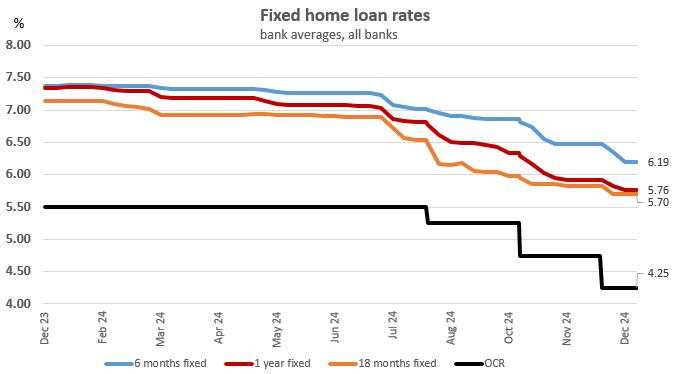

And if we just hone in on 2024, this is what it shows.

You should go into 2025 with your eyes open to the fact that fixed rates are unlikely to fall in lockstep to the OCR.

Of course, the average shift varied between mortgage lenders..

The following table tracks the net change from where we started the year, to where we finished.

| January 2024 | December 2024 | |||||

| carded rate offers | 6 mth | 1 year | 18 mth | 6 mth | 1 year | 18 mth |

| % | % | % | % | % | % | |

| Main banks | ||||||

| ANZ | 7.35 | 7.39 | 7.15 | 6.24 | 5.79 | 5.59 |

| ASB | 7.39 | 7.39 | 7.15 | 6.19 | 5.79 | 5.59 |

| BNZ | 7.39 | 7.35 | 7.15 | 5.99 | 5.79 | 5.59 |

| Kiwibank | 7.39 | 7.35 | 6.15 | 5.79 | ||

| Westpac | 7.39 | 7.39 | 7.19 | 6.19 | 5.79 | 5.69 |

| Challenger banks | ||||||

| Bank of China | 7.09 | 6.99 | 6.24 | 5.79 | 5.59 | |

| China Construction Bank | 7.19 | 7.09 | 6.89 | 6.24 | 5.79 | 5.59 |

| Cooperative Bank | 7.30 | 7.30 | 7.15 | 6.09 | 5.79 | 5.69 |

| Heartland Bank | 6.99 | 6.89 | 5.49 | 5.39 | ||

| ICBC | 7.19 | 7.05 | 6.95 | 5.99 | 5.79 | 5.59 |

| SBS Bank | 7.55 | 7.55 | 7.25 | 6.24 | 5.89 | 5.59 |

| TSB | 7.39 | 7.39 | 7.19 | 6.19 | 5.69 | 5.79 |

So then the question becomes, what will happen in 2025?

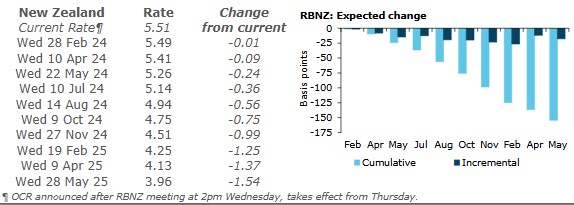

Regular readers will know that we don't predict or forecast future rate levels. But the financial markets do, by setting forward pricing. This isn't infallible, and as each circumstance changes, that pricing is adjusted (as it should be). In 2024 there were many adjustments, so what these markets priced for 2025 at the start of 2024 turned out to be quite different to what they priced at the end. No-one should be surprised. That is just how financial market pricing works, and always has done. (We have extracted the January 2024 version of the table below to show just how much these "priced in" levels have changed since the beginning of 2024.)

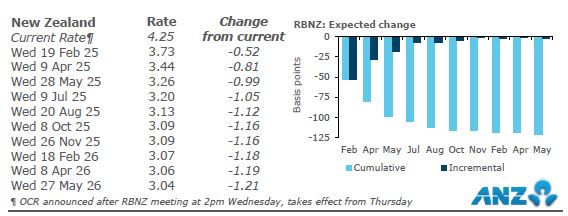

This is what is priced in as at December 20, 2024, for the year ahead when looking at the OCR.

We can add that to our 2024 charting. That might help you think about what could be in store for fixed mortgage rates in 2025. Stay short? or go long from here? Nobody knows the future, especially spruikers pitching their products. Your judgment will be as good as anyone's, and probably better than anyone conflicted by salesmanship. If it seems to good to be true, it almost certainly is.

Just remember, international events have a big influence on the New Zealand cost of money. The RBNZ's OCR isn't the banks' cost of money. It is the actual deposit and wholesale funding (and capital) that makes a bank's funding base, and not the OCR. The OCR has an influence on these things, especially at the very short end (less than one year funding). And even then, it is only one influence.

By going or staying short, you are gambling that your current judgment will still apply when you next need to make a mortgage rate decision. By then the wholesale money markets will have re-priced their positions. You could be facing the quite different outlook, even if the OCR has fallen more.

And as we saw above, at very low rates, the OCR has even less influence on the cost of money for banks. Fixed home loan rates will track the OCR less and less as the OCR falls.

For reference, here is what was priced in at the start of 2024.

90 Comments

Just remember, international events have a big influence on the New Zealand cost of money. The RBNZ's OCR isn't the banks' cost of money. It is the actual deposit and wholesale funding (and capital) that makes a bank's funding base, and not the OCR

Some duds need to read this a number of times..

USA have $7 trillion of debt that needs to be refinanced in 2025 alone and rates are now considerably higher.

https://x.com/StealthQE4/status/1871971880225452176

If you have NZ Mortgage debt rolling over the 1 year looks attractive, 50% at 1year and 50% at 2year if you are conservative and CANNOT afford higher rates. If you have to sell as rates rise it will be difficult as buyers purchasing ability will be collapsing.

In the USA buyers purchasing power has collapsed 10% in the last Q due to rising mortgage rates.

Looking around the world, and given the position of the USD in trade, where do you think those with the wherewithal to invest will head?

Russia? China? perhaps Europe or the Middle East? or even NZ?...I suspect the US will be fighting them off with a stick for the foreseeable.

USA have $7 trillion of debt that needs to be refinanced in 2025 alone and rates are now considerably higher.

We'll never get to see the correspondence between Powell / Fed and Yellen / Treasury. All deleted. All shredded.

Great rant from this guy. Likely on the money and I love how he refers to the necessity of QE again. It's inevitable. The moronic responses from the Aotearoa ruling elite about 'back to normal' amplified by our generally braindead media is essentially about QE being ramped up again in the US.

Trump: "We're going to slash government spending."

Public: "Yay !!!"

Also Trump: "We want an unlimited debt cap."

Public: "Yay !!!"

What could possibly go wrong?

If you plot mortgage rates vs OCR you will see a very clear correlation over a long period of time. International influence is extremely minor in comparison.

Have another look at that correlation using this thought: The OCR is good for setting a floor. While absolutely hopeless at setting a ceiling.

Bond market fears USA debt out of control and inflation not under control according to wolf Richter. Rates will have to remain higher for longer. Only logical to hope for half a % drop anywhere

Poor article.

A chimpanzee can work out approximated Interest rates for 6mth, 12mth, and 18mth from expected OCR movements.

Where is your analysis on 3 and 5 year rates.

Our loan is coming up next month. We have these rates in the ASB app. I think we could have done better 4 months ago!

6 month: 5.99

12 month: 5.65

18 month: 5.59

24 month: 5.49

Bond yields hit their recent low on 18th September, but since then, 10-year government bonds have climbed to 4.6%. Rates from four months ago aren’t coming back unless yields drop to 3.6%, like they were in September. I think the bond market will continue to sell off, and we could see 7.5% fixed mortgages again in 2025.

No, you couldn't. 4 months ago the 1 year discounted rate was 6% or higher.

1 year fixed was being offered for 5.59% for a period of time

The markets are in for a huge shock in 2025 because they continue to ignore the difference between money and credit and the fact that the BIS, in effect, threw ALL fiat currencies under the bus when they reclassified physical gold as a Tier-1 balance sheet asset on January 1, 2023.

Of course, the BIS member banks, the ones with half a brain that is, began gold stacking well before this date and along with the BRICS-bloc central banks continue to do so to this day.

The huge irony is that Western-centric governments and CBs are in essence, gold's best friend because they are destroying their economies in debt death traps along with their fiat currencies as well. As I have repeatedly mentioned on this site, all of them have already lost between 98 - 99.98% of their purchasing power.

The governments don't want to encourage gold ownership or even have this conversation, because the 5000-year-old stable purchasing power of gold, in terms of purchasing goods and services, remains essentially constant. It also reveals how badly they manage their economies and their currencies.

The glaring exception of course is China which openly encourages its citizens to invest in gold.

Countries like China and Russia have so much gold that they could hard-back their currencies tomorrow and declare a physical buy price, which would immediately revalue physical gold worldwide. This could bring down the Western fiat casino virtually overnight.

All credit to the BRICS countries for not having already used this financial nuclear equivalent weapon. They don't need to anyway because of the U$ hegemonic obsession with weaponising its reserve currency status.

Meanwhile, total debt rises exponentially along with ridiculous market-cap 'values' of corporations. As a measure of how distorted this situation has become, think in terms of the 10 largest U$ companies at a combined $17 - $18 trillion - compare that to all of the global gold production which adds up to approximately $17 trillion based on the current spot market.

So too, look at the 'value' of the 3 largest companies by market cap...

Apple @ $3.9 trillion

NVIDIA @ $3.4 trillion

Microsoft @ $3.2 trillion

These numbers are totally out of sync when all of the world's central banks combined own only $3 trillion in physical gold. This to me suggests a looming exponential revaluation of gold, given the extremely limited supply and a massive increase in demand once institutions and individuals catch up with why the well-informed central banks are all gold stacking.

In the 1920s in countries like Sweden and the U$, you could buy a house for around $5,000, or the equivalent of ~250 ounces of gold. Today they would pay that same 250-ounce price which equates to ~$650,000.

What has changed - it's not the price of gold, and not even the cost of the house, the change is in the purchasing power of the currency.

Cheers to all

Colin Maxwell

Top central bank buyers of gold in 2024 were Turkey, India, Poland. Of course, China went on a hiatus for 6 months but recently started buying gold again. Aotearoa and Aussie would never buy gold. It seems as if any two countries are happy with the monetary status quo (and how it operates) and see no hazards on the horizon, it's us.

I bet most senior Banking execs and RBNZ staff have a bit of gold and btc, just in case.

Many FX traders do re BTC or own gold miners etc

Yes J.C. - and we can add the US to that list as well - they were the one country that continued to bet against gold after the BIS reclassification.

That for me was huge news as it signalled a splintering of the U$ away from the other global CBs in their coordinated synthetic paper manipulation of the physical gold price.

It was a major break from the 50-year pattern of gold manipulation that came about after 1971 when the Bretton Woods system self-destructed, only to be replaced with the petro-dollar in 1974.

This deal committed Saudi Arabia to trading oil exclusively in US dollars in return for American military and economic support, establishing the dollar as the global oil currency for decades, until its recent expiration.

That plan then subsequently went up in smoke in June of 2024 when the Saudis didn't renew the 50-year-old agreement.

The situation remains in a state of flux with Saudi Arabia still sitting on the fence - although the BRICS approved it as a potential member back in the 2023 Summit, and it was set to formally join in February of 2024, it announced at the last minute that it was not yet ready.

Back to the gold - yes, as the saying goes if you have a ring on one finger, then you own more gold than the RBNZ.

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/publications/…

Australia, in November of 2024, at least had $6.8 billion of physical gold in reserve.

According to the CEIC data, these are the countries like NZ that are sitting on a big fat ZERO...

Armenia, Azerbaijan, Canada, Croatia, Israel, Ivory Coast, Kosovo, Israel, Ivory Coast, Kosovo, Montenegro, NZ, Norway, and Panama.

https://www.ceicdata.com/en/indicator/new-zealand/gold-reserves

NZ's last substantial reserves were sold off in1962 when Holyoake (National) was Prime Minister

The last of the gold was finally squandered for pennies on the pound in 1990 with Jim Bolger (yes, National too) at the helm.

And no prizes for guessing which RBNZ Governor was on watch when that decision was made - only the longest serving Governor of all time - 14 years in all, from 1988-2002

This was a period of overt neoliberal economics which would no doubt have thrilled the World Bank economists that he had worked with in 'Warshington' from 1966-1971.

Season's greetings

Colin

Why do the vast majority choose (it is a choice) to trade in USD?

I can see a variety of reasons, Frank apart from common garden variety habit, but including hegemonic threats, and coercion as well.

Also, the fact that alternatives have been very limited, especially if you wanted one that was not Western-centric.

So too the Triffin Paradox* effect which means that productive real economies that rely on significant exports don't want to become the next incumbent global reserve - history proves that this status has always ended badly.

That's why I prefer the idea of a trade-only reserve currency instrument that doesn't also double as a national currency.

*The key takeaways from Investopedia...

- Robert Triffin believed the dollar could not survive as the world's reserve currency without requiring the United States to run ever-growing deficits.

- A popular reserve currency lifts its exchange rate, which hurts the currency-issuing country's exports, leading to a trade deficit.

- A country that issues a reserve currency must balance its interests with the responsibility to make monetary decisions that benefit other countries.

- Another reserve currency replacing the dollar would increase borrowing costs, which could impact the United States' ability to repay debt. (This is the reason why the U$ will fight tooth and nail to keep its reserve currency status.)

- A new international monetary system could potentially help countries maintain a reserve currency status.

Cheers

Colin

We can all posit desired alternatives but we have to deal with what we have.

There are alternatives out there already, Frank, including the massive logistic and financial architecture to support a new cooperative global merchantile reality.

Here is just one example of a global financial renaissance.

https://globalsouth.co/2024/12/27/brics-to-build-uae-based-logistics-hu…

The question I have Colin is when (if ever) will the worlds businesses decide that BRIC is a better option than the USD. Do any of the BRICs advocates produce commercial aircraft? What is the comparative quality of their military equipment? Do they have a viable(and desired) communications network?...and ultimately do they have the cohesive capacity to implement a common agenda?...and (edit) energy...while many countries have the raw materials they rely on US technology to access it.

If and when a significant proportion of the world accept that they do then they may rival the USD....if something else considered better dosnt appear in the meantime.

Perhaps this clip by the very sharp and straight-shooting U$-born Kevin Walmsley (now living in China) can answer at least some of your many questions, Frank.

https://www.youtube.com/watch?v=wu5vo0E0jMo

BTW, what search engine do you use? - all of this info is readily accessible on DuckDuckGo.

The algorithms on Google are constructed in such a way these days that all you ever find is neoliberalst/neocon misinformation and bare-faced lies - all designed to protect the status quo Western financial casino.

I use all manner of search engines including DDGo....but no search engine is require to play scenarios and apply logic. The youtube clip is unnecessary to answer the simple questions I asked...BRICs has been an entity for 15 years and the use of USD remains unchanged...why is that?

At the beginning of 2024, Frank we saw the culmination of a long negative trend that has seen the US currency’s share in foreign reserves held by central banks fall from over 70% in the early 2000s to under 60% today.

This has undoubtedly continued as the U$ has increasingly weaponised the dollar and with the geopolitical turmoil they constantly stir up, this trend can only accelerate.

So too a replication of the Smoot/Hawley tariff idiocy that Trump is promoting, alongside his regime's overt exceptionalist neocolonial foreign policy.

https://theconversation.com/why-the-world-is-turning-away-from-the-us-d…

...quoted...

"Over the last 20 years, China’s share of the global economy has more than doubled from 8.9% to 18.5% while the US’s share declined from 20.1% to 15.5% in purchasing power parity terms (which compare prices of specific goods to determine currency purchasing power).

Last year, the BRICS economies (fast-growth developing countries Brazil, Russia, India, China and South Africa) overtook those of the G7 (developed economies US, Canada, UK, Germany, France, Italy, Japan and Germany) based on their share of world GDP in purchasing power parity terms."

..................................................

With all due respect, I wonder if you are confusing the much lower percentage of U$ currency figures share in foreign reserves with its huge 88% share in the foreign exchange casino markets? - obviously, these are two very different scenarios.

Liquidity Colin...what can you buy in a currency that few want? You have yet to answer why the the USD remains the currency of choice for trade, even after they seized Russias (offshore) assets and shut them out of Swift....if anything was going to motivate the BRICs economies to move their trade into something else that would be it, and yet even the founding members cannot agree to its use.

China may be approaching a point where it can match US technology but the US isnt going to simply fold their tent...and the world of business knows it...they are still betting on the USD.

I suspect that by the time an alternative will be accepted there will be very little left to fight over.

I fail to understand why you continually underestimate China's superior technology in so many spheres Frank - I will leave that one alone and hope this reality dawns on you in your own good time.

ABOUT LIQUIDITY AND HOW IT RELATES TO A NEW PARADIGM IN GLOBAL TRADE

I repeat from earlier posts - China does not seek to make its currency the world world reserve currency. The U$ dollar already serves that dubious role, and China remains quite at ease with that situation for the time being.

Remember that a U$ dollar in circulation is a debt. U$ dollars are U$ debts to foreigners. Why would China want to create trillions of dollars in yuan-denominated debt just to dump into the global market - why not let the U$ continue to play that game.

This situation remains a major blindspot for Western-centric eCONomists and analysts.

China's central bank is moving into using the digital yuan and introducing programs for Chinese citizens and businesses to use digital yuan. Adoption has been slow because the Chinese already have many payment options.

These plans have nothing to do with digital currencies using the U$ dollar. Remember that the U$ has zero plans to implement a central bank digital currency - the House of Representatives has passed a bill which permanently bars the Fed from issuing digital currencies backed by U$ dollars.

This is just as it should be - doing so would have given the private cartel which owns 100% of the shares in the Fed, total power over every aspect of the U$ financial 'system', and also over the entire population.

This leaves the field wide open for other countries to build a digital dollar.

Remember that China is by far the largest bilateral creditor and the leading trading partner to most of the countries on the planet and they could use the digital yuan to challenge the dominance of the dollar - yes, absolutely they could, but why would they?

They can instead just digitalise the U$ dollars that they hold in their own banks. They can then use those dollars to encourage new economic activity around the entire planet - especially via the enormous BRICS initiatives.

The U$ seriously risks losing economic leverage and financial power if China continues to dictate the norms and use of digital currencies

Meanwhile, the U$ still takes a lot of pride in the fact that their dollar remains the #1 reserve currency. However, if the BRICS countries can build a system that uses U$ dollars to finance their trading activity, all of those perceived advantages of being the incumbent reserve currency fly out the door.

This means that if China wants to build a CBDC system, without using yuan we shouldn't look for China's digital yuan as a model for what they intend to do.

Neither can we look to Bitcoin either as it is such a lousy instrument for use in international trade settlements, and not the least because of its wild price fluctuations.

Instead, it is probably wiser to look at Tether, which is a Stablecoin that tracks the U$ dollar. Tether claims to have U$ dollars or T-bonds in reserve to back all of their Stablecoins that are in circulation (more than $116 billion worth).

Russia is also using Tether to bypass the international sanctions - importers use Russian Rubles, then go through an intermediary to convert them to Tether, and Tether then converts again into foreign currencies. It is fast, simple, very inexpensive to do so, and completely outside of the Western banking system.

The U$ authorities cannot track Tether and the trading numbers are astonishing - like $120 billion in trade per day - and for 2023 came to over $10 trillion.

Bear in mind that Tether's reserves are $116 billion and it turns over more than that amount in trade every day. China's trading reserves are ~25 times that, and sitting at probably more than $4 trillion now.

What Tether is doing is providing a blueprint for China to follow and they have already announced plans to make Hong Kong a centre for digital currencies, a global hub for financial technology, and the world capital for Stablecoin.

Much of the world wants U$ dollars to make this happen and no one has more of them sitting around than the Chinese banks.

Five years ago Tether didn't even exist and yet already it's bigger than Visa. Perhaps China sees that it can take over the financial system of the world using U$ dollars as a vehicle and leave them to let their printing presses rip.

Methinks, that 2025 will be the year of the wild ride, interspersed with rounds of beers and popcorn for those who have prepared themselves mentally for the possibility of the great unwind.

Cheers

Colin

It dosnt matter if I underestimate Chinas technological 'superiority'....what is evident is that those that decide what is useful to them do not (yet) rate China as superior to the US....until they do, if it ever happens we have what we have.

I have suggested reasons why this is, you can agree or disagree, ultimately we dont make the decisions that impact it.

I’m not sure which concerns me more, the fact you think China’s crumbling economy is superior to that of the US or that somehow the human population would put a boot on their own neck and gravitate toward communist backed currency.

China’s economy is a garbage paper tiger and sinking rapidly thanks to its disturbing anti human, anti freedom government.

For all its faults, the USD or US backed currency will endure in the interest of the human spirit.

''Thats All' - you state - “...China’s crumbling economy…”

This is the economy that just happens to be by far the largest creditor nation in the history of the world.

Given that it’s economy is an overwhelmingly a productive real economy, in comparison to the U$ which is largely a financial FIRE (Financial Insurance Real estate) model, if we bothered to work out the respective productive GDP numbers I would estimate that China’s would be at least 400% larger.

“...communist backed currency.”

This no doubt will come as a profound shock to you, but China’s economy is no longer technically communist.

The Chinese model is an open-market-capitalist/socialist/Confucianist model – and an utterly unique and fascinating one at that. It is quite unlike any other model in the world, other than Vietnam, which I don’t classify as communist either.

The only really close remnant China has to pure communism that I can see, is their population’s inability to own farmland – this is a legacy of the communist era. The problems of returning that vast country into private ownership would be insurmountable given the 1.4 billion population – this is a legacy of the era of a pure communist model and I don’t see how the clock could be turned back.

The CPC (Chinese Communist Party) has less than 100 million members making it only around 1/14th of the total population – not by choice though, but limited by the enormously strict conditions for membership.

Just as the blue party in the U$ wears its “Democratic” label, but is a sad joke because it doesn’t fit with any sane interpretation of that word, I would argue that the ‘Communist’ label in the CPC acronym doesn’t define them either.

China has a public utility central bank - this is the big game changer and the number one reason why it is the most successful economy on the planet. This was the latter part of their long transitional phase which took hundreds of millions of poverty-stricken people into middle-class-hood.

Even more remarkable was the fact that this was all done with zero destructive inflation – so too were the monumental infrastructural programs and all done deploying the public banking solution (PBS) all of which created wealth for generations to come. None of this was unique – in fact, the PBS models were borrowed from Western models over the last few centuries – now is the time for us to swallow our pride, to look back over there, and simply borrow the models back again.

I do not reject socialism either, as I see an element of it as essential for any modern-day society to function – the important thing is that it is not the U$ Western brand (reverse socialism) disguised as socialism but in reality the polar opposite - one where the booty is pocketed by the entrenched financial plutoccrats, and the losses are socialised to become just another societal burden.

My calculations of 0.5% (down from more than 30% in the 1980s) of the world population that is governed by technically communist regimes, means that as a threatening global political force it is farcically minuscule - communism is no longer the “boogeyman" (Putin’s words) that the West and NATOstan have always dressed it up to be.

The tiny 0.5% remnant, which amount to Laos, North Korea and Cuba only just survive, but to me it is simply incalculable how much their economies and socioeconomic circumstances could have flourished into hybrid free-market models, if the West hadn’t made it their mission to try to literally starve them off the planet.

I would hazard a guess, that just as China and Vietnam have done, these countries would have transitioned into vibrant hybrid economies too, and become positive contributors to global cooperative mercantilism and security.

Cooperation from other countries and a friendly synergetic demeanour would have almost guaranteed that these stalwarts could have developed more along the lines of Vietnam – that remains the ultimate irony – the U$ lost the war fighting communism, and yet this 99 million strong country transitioned organically into a mixed market economy – no one needed to die!

I would suggest that you shed your neoliberal blinkers, 'Thats All' and reflect on just how strictly non-interventionist China’s policy’s really are - actually, it could be argued that this adherence is pursued to a fault, especially given the West’s wanton ongoing genocide within Palestine.

https://globalsouth.co/2024/12/29/china-a-debate-how-chinas-rise-herald…

I suggest that the USA is quite happy to have trillions of dollars debt for it ensures US$ remains the dominant world currency. Interest on the trillions of dollars debt is payed in US$ and as such the lenders are forced to spend those dollars internationally. For example China receives US$ for the moneys lend by way of bonds to the USA. The US$ gets spend to buy Saudi oil. The US$ remains as the default trading currency. The loop closes as Saudi spend the US$ hopefully in the USA. All the interest money returns to the USA in the form of goods and services purchased there.

The size of the debt is largely meaningless for it is the interest money that returns to the USA (eventually) to maintains the USA economy. Countries like China and Japan that have large holdings of US debt will be in the power of the US$ until they can palm off the debt to other nations. USA will never repay the principle (no need for the principle is already spent internally) just the interest only, keeping control of the US$ as the default world currency.

BRICS will not, in the foreseeable future, override the US$ as world currency whilst the USA only pays interest on the Chinese and Japanese (and to a smaller amount, India) loans.

Gold has the problem that it is not as easily transferable as a trading mechanism as currency. Hard to pay for a barrel of oil using gold for one would surely have to take physical possession to complete a transaction.

If gold was to become a trading payment commodity, at least New Zealand could easily dig (Green's permitting) to financial freedom. Making every New Zealander as "wealthy" as their Danish or Norwegian counterpart with their oil/gas reserves.

It is not just the inefficiency of gold as currency (especially in a vast, busy, global economy) there are also limitations of scale....and a point that those promoting gold may wish to consider.....if currency once again becomes gold backed who is going to own/possess that gold? The issuer of the currency, not the users.

Australia, in November of 2024, at least had $6.8 billion of physical gold in reserve.

TBH, I thought the RBA had sold all their gold, but you're right, they own 80 tonnes of gold as part of official reserve assets. A far cry from 1997 when they owned 247 tonnes.

In the 2023-24 financial year, The Perth Mint held more than AUD 7.3 billion worth of precious metals for its global clients. The Perth Mint is a subsidiary of Gold Corporation, which is a statutory body wholly owned by the Government of Western Australia. The Perth Mint's operations and liabilities are backed by a guarantee from the WA Govt, enshrined in the Gold Corporation Act 1987.

A whole 6.8 billion...Australian GDP is 1.7 trillion USD...their gold holding amount to a hill of beans.

Too true, Frank - as you say, that's not a lot when you look at it as a percentage of GDP.

At least it is audited though, unlike the U$ reserves (last audited in 1953), which are leased out and rehypothecated to such an extent, that they probably don't even exist as a reserve asset.

The real tragedy though is that if only Aus had kept their Commonwealth Bank of Australia going (a defacto reserve bank public utility model), they could have become by far and away the wealthiest country on the planet.

Yeah. 2 relatively large economies (Australia and Canada) among plenty of small, globally insignificant economies such as NZ.

Some here will be jumping in soon to assert that NZ is too strategically important to fail simply because "we feed the world".

NZ and Australia have gold in the ground. New Zealand extracts approx 10 tonnes a year, it’s there if needed.

Let's see what happens when, very shortly, the US establishes its strategic Bitcoin reserve.

Not a done deal. BTW, Japanese govt officially rejected rat poison as a strategic reserve asset yday.

Hmmm... Eschaton - legislating for the U$ Government to buy up 5% of a global Ponzi/pyramid scheme - what could go wrong?

Imagine if the Dutch government had done the same thing during the height of the tulip mania era - a bad idea would have been made exponentially worse.

Hmmm... Eschaton - legislating for the U$ Government to buy up 5% of a global Ponzi/pyramid scheme - what could go wrong?

Idea is for the the purchase of 200,000 Bitcoins annually for five years. Add that to the existing US govt supply of 214,000 = 414,000.

New supply of BTC over next 5 years is 683,235. So the US govt will be gobbling up approx 34% of new supply.

Long-term holders sold approximately 128,000 BTC during the recent price surge to $99,000 in November. At this point, analysis indicates that long-term investors have sold almost 550,000 BTC, which represents about 4% of their total holdings.

If it's 200,000 BTC annually over 5 years, is that not 1M total?

Why don't they mine it instead of buying?

If it's 200,000 BTC annually over 5 years, is that not 1M total?

Yes. You are correct. Not sure why I didn't sense check this.

US govt demand for ratty will exceed all new supply. When you factor this in, USD1 million BTC by 2030 shouldn't sound so outrageous.

The Tulip mania lasted 1 year...and yet idiot comments like Colin's still pops up comparing it to Bitcoin? Please go back under your rock for 2025...the world has moved on.

A Ponzi-pyramid scheme is just that, Baywatch - it has zero to do with the time frame of people being sucked into it. Indeed, the longer it lasts, the more potentially dangerous it can become.

That said, you are wrong about the time frame - Tulip Mania ran from 1634 until its dramatic collapse in 1637. Also, the comparison is perfectly valid as the term is commonly used to describe a situation where an 'asset' price deviates wildly from its intrinsic value.

Given that Bitcoin has zero intrinsic value - it is about as extreme an example of credit as you could find anywhere on earth - this is a perfectly valid analogy.

The real tragedy in all of this is when people cannot distinguish between money and credit - they will find out the hard way when the mathematically imminent certainty of the Western fiat financial casino meltdown unfolds.

Ad hominem attacks from the likes of you and Chris* are like water off a duck's back to me - besides it is most helpful in revealing the true character of the commenter - to me it is infantile behaviour if it is done whilst hiding behind a nom deplume.

I don't hide behind anything and have no book to talk. My only agenda is that I live in the hope that we might one day wake up and learn to value, and to reward accordingly, the global labour resource, instead of allowing all of this wealth transfer to the parasitic financial sector.

EG - this copy and paste of an absolute shocker!!!

by ChrisOfNoFame | 27th Dec 24, 6:51am

"fundamental distinction between money and credit?

Is there any such distinction? Or is there just a made up one?

.....................

For crying out loud Chris - your question can be answered in one paragraph -

Credit is always matched by debt - IOWs, your financial asset is someone else's obligation - real money has no such counterp[arty risk.

Until we understand the distinction between money and credit, and also the mechanics of the creation of credit, then Western society will continue to slide into socio-economic mayhem.

If we don't understand these basics, we are easy prey and highly likely to become recruits of the very enemy we fancy ourselves fighting.

Colin Maxwell

021 341 501 (texts only please)

Agree.

Unfortunately, just as "time is money" has become a programmed belief, so has "debt is money". We can't distinguish between debt and credit.

The distinction has been lost. Everyone here has been taught about credit creation over many years, but we still like to be impressed by the big numbers.

Haha yet we've never really moved on. All we've done is replace tulips with Bitcoin, and everything in between. We've repeated it continuously throughout history and still we choose to learn nothing. The gaps between financial crises get less and less, and we expend more to keep the casino going.

Governments are broke everywhere, especially the US, and "investing" in a national strategic BTC reserve is going to solve this? It's just pumping the "asset class", because all the rest are already pumped sky high.

Spot on Meh! - BRAVO

You just explained the entire puzzle in two concise paragraphs.

Cheers

Colin

All we've done is replace tulips with Bitcoin

Was a similar narrative bouncing around the BBQs in the 1970s when gold appreciated 1,357%?

Just about the tulip bubble, it lasted for approx 7 years from 1630-1637. When prices crashed, it ended. Estimates suggest that some bulbs had been sold for as much as 10x their intrinsic value before the crash.

That would suggest that the "gold bubble" of the 70s is due for a reckoning - priced in USD, gold is up another 343% since 1980.

As for the ol' rat poison, it has "crashed" numerous times.

Perhaps you need to stop thinking about these assets in terms of "bubbles" and think of relative pricing and declining purchasing power of fiat currencies.

Perhaps you need to stop thinking about these assets in terms of "bubbles" and think of relative pricing and declining purchasing power of fiat currencies

Hence the reason for pumping assets and all the propaganda and manipulation to keep them pumped. I don't think of them as bubbles, merely a cleverly crafted narrative and system of control and power.

Those in the know, know that since the gold standard was busted and deregulation of banks to print "money" results in declining purchasing power, and attempt to store the "value" in assets. Meanwhile the plebs and peasants do what?

The idiocy being that paying more for assets also proves the loss in purchasing power, further feeds the machine and requires more to keep it going. But we ignore this because we magically believe it's wealth.

The illusion must be maintained.

Those in the know, know that since the gold standard was busted and deregulation of banks to print "money" results in declining purchasing power, and attempt to store the "value" in assets.

Gold could appreciate 50% in fiat terms in 2025, and the media, experts, water cooler crew would still deride it and call it worthless.

What use gold?

The idiocy being that paying more for assets also proves the loss in purchasing power, further feeds the machine and requires more to keep it going. But we ignore this because we magically believe it's wealth.

Bingo

How about this wild thought. The FED keeps buying up Bitcoin, the price goes to the moon and they sell it to wipe out their debt ? I mean its all just numbers right ???

How about this wild thought. The FED keeps buying up Bitcoin, the price goes to the moon and they sell it to wipe out their debt ? I mean its all just numbers right ???

Yes Z. The concept of minting a $1 trillion platinum coin was a topic of discussion, particularly during debt ceiling crises in the United States. This idea stems from a legal provision that allows the U.S. Treasury to mint platinum coins of any denomination. Advocates propose that minting such a coin could provide a workaround to raise the debt ceiling without congressional approval, effectively allowing the government to meet its financial obligations without incurring new debt.

However, the US cannot really mint ratty. And debt is now increasing by $1 trillion every 100 days.

Bad Girl Yellen has firmly rejected the idea of the trillion-dollar coin. In early 2023, she described the proposal as a "gimmick" and expressed doubt that the Federal Reserve would accept such a coin if minted. Yellen emphasized that there is no obligation for the Fed to recognize a coin minted in this manner, stating, "It's up to them what to do" regarding acceptance of the coin.

Spot on Colin

Silliest comment of the year Colin, well done you just sneaked in.

Gosh, and you provide such a compelling and factual rebuttal, Baywatch :-)

The real tragedy in all of this is when people cannot distinguish between money and credit

Sigh ...and you actually believe you do?

Let's have this debate every Xmas Colin, you seem to have arrived late to the party and most of us have left.

You mention Texas and Florida and sound money..is this an example?

Texas House introduces bill to establish a strategic bitcoin reserve

A house bill does not define a state's position, Baywatch.

Texas's depository has been operational for many years, and BTW I know precisely what sound money is - the first requirement is that it has no counterparty risk.

Did you and Chris go to the same school?

https://www.schiffgold.com/key-gold-news/texas-committee-passes-bill-to…

What if it passes Colin, is sound money the same as hard money...please enlighten us? You must be a convert to Peter Schiff house of gold shilling.

Also what are your thoughts on this

In less than a year, these BTC ETFs have become the most successful in history, surpassing $100 billion in total assets — compared to $285 billion for gold ETFs over their entire history

So gold is not sound money because of performance of the ol' rat poison? And why do you use ETFs as a proxy for sound money?

Write off gold at your own peril in terms of its properties. Because you made a motza on BTC is not an argument against gold.

What's rat poison? How potable is gold and how easy to verify....this one for Colin.

I really can't be bothered answering questions from people with your attitude Baywatch - besides, why on earth would you seek my opinion anyway?...

A C&P of your brand of arrogance...

by Baywatch | 28th Dec 24, 7:39am

Silliest comment of the year Colin, well done you just sneaked in.

Just like Chris, you don't have the foggiest notion as to the gigantic distinction between money and credit.

Over and out - I have much better things to do than to engage and argue the toss over these basic concepts.

- Good for you Colin..enjoy our summer and we can chat next Xmas. Your thoughts of BTC at that time being close to $200k will interesting.

Silly season predictions make for summer BBQ crap-chat. When All Is Said and Done we in New Zealand, are hugely influenced by what happens overseas, we are price takers not pricemakers. The pending international geopolitical/financial crisis is looking an odds on bet, hence, expect rates to ease slightly over the next 6mths, then as the Black Swans appear watch the bank rates head north.

Hypothetical question:

If the RBNZ allowed anyone to deposit money with them - while agreeing only the nominal amount would be lent out - at the OCR rate, would you deposit your money with them? I.e. the RBNZ would not, as retail & commercial banks do, create new, additional money from the reserves they have?

Or would you only ever look for the highest interest rate, for the duration you want, without regard for how the recipient of your deposit used it?

If the nominal amount deposited is all that is lent then where does the interest come from ?

There's a reason interest/usury was illegal and/or there were debt jubilees. I think it had more to do with ethics then.

Now, mathematically, whether it makes sense or not, we need to create new credit to pay the interest on the old, and lower interest rates to enable it.

But it would appear the financial market is in a conundrum. The OCR/inflation war might have worked 40 years ago when debt was relatively more proportionally spread over households. Inflation also "inflated the debt away". It doesn't seem to work so well now. More debt but highly centred and a massive cost base, having more influence on inflation than it used to. There's now more excess money, massive asset funds that demand higher returns over inflation.

We're between a rock and a hard place when it comes to interest/returns, and debt.

" There's now more excess money, massive asset funds that demand higher returns over inflation. "

It is not that they demand 'higher returns', it is the effect of compounding growth...ultimately there must be defaults, and to attempt to overcome this the powers that be have accelerated that (monetary) growth to avoid defaults.... they cannot succeed.

There are two ways to pay the interest...monetary expansion and/or increased productivity (as measured in money)...which is effectively deflation.

Unfortunately we no longer have the option of a deflationary reset because we are on the downslope of productive capacity....energy.

PDK is correct

I think the banks can answer that. Future lending, of course!

The lender pays interest at the OCR rate + a small amount to cover admin, with the OCR portion going directly to the depositor.

The lender 'forgoes consumption' of other stuff to pay the interest.

The 'model' does not require the retail banks no longer exist. Only that there is a non-profit lender that pays lower deposit rates and does not become part of the fractional banking system.

Would depositors actually deposit money with them? There seem to be many that believe fractional banking is an obscenity. Ergo, I'm asking them if they'd forgo higher deposit rates so their 'principles' were preserved.

In answer to Frank at 11:53 - The interest comes from creating ever more credit.

The legal reality is that banks don't take deposits either, and neither do they lend out existing money.

https://www.educatedinlaw.org/2017/03/banks-dont-take-deposits-banks-do…

... paraphrased from the link...

A deposit is not a bailment and it is not held in custody - at law, the word 'deposit' is meaningless.

This money that we term a deposit is simply a loan to the bank.

So banks borrow from the public, but what about lending - surely they are lending money - no they are not - banks don't lend money. It is very clear at law that banks are in the business of purchasing securities -that's it.

And so the public says, don't confuse me with all of that legalese, I want the loan, they are given the offer letter and they sign - once again at law it is very clear - you have issued a security, namely a promissory note which the bank purchases.

What the bank is doing is very different from what it presents to the public.

When the customer says "I don't care about the details I want the money" - if the bank says "you will find it in your account, then that would be technically correct - if they say "we will transfer it to your account", that's wrong, because no money is transferred at all, from anywhere inside the bank or from outside the bank.

Now the bank owes you money and its record of the money it owes you is what you think you are getting as money and that's all it is. That is how the banks create 97% of the money supply - it is created out of nothing when they make loans.

"That is how the banks create 97% of the money supply - it is created out of nothing when they make loans."

Indeed...and it is destroyed when those loans are repaid...or crucially, defaulted upon.

Does any CB or Gov want a decreasing GDP? And why not?....difficult to pay interest (return) when the supply of money is flat or (esp) decreasing. The same occurs when that 'money' is effectively parked in assets, especially non productive assets. So they have two options, increase the money supply at the rate of productive increase or increase money supply above the rate of supply and create inflation (the only question is where, in many cases it is RE)....add in that production is currently flat and will fall and you see where it is heading....unavoidable.

And just to complicate things further, an economy may increase its money supply in line with its productive capacity and be impacted by the activity of a connected economy....and nearly all economies are connected.

So we end up where we are, an effective currency war and a bidding war for assets that hands a distinct advantage to the issuer of the reserve currency who are increasingly deciding that the only course of action is to use that advantage and bad luck everyone else....and if that dosnt work, then they have the military capacity to seize it anyway....not going to end well....especially as those assets are in decline.

Monetary policy cannot solve it.....and they have known it since GFC (or shortly thereafter)

Precisely, Frank - we both travel our different roads but appear to arrive at a very similar destination.

After all of my decades of geopolitical/geoeconomic studies, the only solutions I can envisage are...

#1 A total meltdown of the Western-centric casino model in which the public demands total financial and political reform - the least desirable option - with JIT supply chains it only takes a few days for a Mad Max scenario to occur in an urban setting, and what could come out of this is highly likely to be far more chaotic than what got us into this debt-trap vortex the first place.

#2 In the US the massive move to sound money initiatives, state repositories, state monetary and fiscal autonomy, plus even secession from the broken federal model. This method could demonstrate successful models that become blueprints for other states, and even sovereign countries. When you have states as diverse in size as Texas and Tennessee going down this track they could be inspirational for sovereign countries with similar GDP profiles.

From only one state travelling this road for almost a century (North Dakota), there are now some 35 in various stages of legislation aimed at pushing forward with sound money and public banking solutions - including the two very different behemoths, Texas and Florida.

#3 BRICS creditor nations with strong balance sheets and sustainable societal wealth models which could in turn inspire other nations to adopt similar policies.

I hope for a combination of #2 and #3, but all the while fear that we are all dangerously close to seeing #1 unfold, as the Western hegemon flails more and more desperately in trying to save the status quo.

With their influential evangelical-rapturist element entrenched within the AAZ alliance, my greatest fear is that they will invoke the Sampson Option.

All the best

Colin

So banks borrow from the public, but what about lending - surely they are lending money - no they are not - banks don't lend money. It is very clear at law that banks are in the business of purchasing securities -

Precisely. Would be good if more people understood this.

So you're saying: the more stuff we create, the more stuff there is that can be securitized, so the money supply increases?

So we should stop creating stuff to halt the ever increasing amount of money? .... ;-)

There's a conspiracy theory that suggests your birth certificate is the legal document to securitize you.

We're in the machinations of monetizing every aspect of human living.

Which came first? Creating or money supply? Maybe it's not as connected as we think it is. Negative GDP growth, therefore less creating but money creation still happening.

Fiat money originated in China during the Tang Dynasty (618–907 AD) as a response to shortages of precious metals. The Song Dynasty later issued the first widely recognized fiat currency, the "jiaozi," in the 12th century. It became prominent in the West during the 18th century and globally dominant after the U.S. abandoned the gold standard in 1971 under President Nixon.

There's a 'money museum' in Beijing. Well worth a visit if you like economic history.

Our 'current money' is actually little more than a toddler, maybe a tween, and the museum shows the births, and deaths, of many types and flavors, of money. I have every expectation our 'current money' will be little different and will eventually go the same way. It'll be replaced by something new, that's basically the same, and the cycle will continue.

As always, hard assets will hold their value irrespective of how their value is measured using whatever money or currency is used at that time. But take note - one's ownership of hard assets can be stripped away with ease when revolutions occur.

But take note - one's ownership of hard assets can be stripped away with ease when revolutions occur.

Which revolution are you referring to? The cultural revolution? Yes, the Chinese government banned private ownership of gold and silver and the state, through the People's Bank of China (PBoC), took control of all precious metals activities.

Ironically, such periods of history have seem gold demand rise because of its intrinsic value and properties.

Not only the likes of 'revolutionary China'....

"The passage of the Gold Reserve Act of 1934 signified that the American people could no longer hold gold, with the exception of jewelry and collectors' coins. After the passage of the Gold Reserve Act several people were indicted for violating the clauses that restricted gold ownership and trade. "

https://en.wikipedia.org/wiki/Gold_Reserve_Act#:~:text=The%20passage%20….

1930s America was not what I would call a 'revolution'. Under the Act, personal gold holdings were confiscated in exchange for fiat. Some exemptions:

- Allowed individuals to keep up to $100 in gold coins

- Exempted "customary use in industry, profession or art," which included artists, jewelers, and dentists.

- Rare and unusual coins of recognized special value to collectors were also exempt

During the Civil War, the Confederacy faced significant challenges related to gold. At the start of the war, the seven Confederate states possessed only about $27 million in gold and silver. The Confederate Treasury raised approximately $15 million in gold by selling bonds to smaller financial institutions willing to take on risk. As the war progressed, the Confederate currency became almost worthless, severely limiting their ability to purchase supplies and weaponry.

Think you miss the point....'revolution' is not required.

Think you miss the point....'revolution' is not required

Gotcha. No reason why gold confiscation can't happen in Aotearoa or elsewhere. Wonder how the Perth Mint would cope given that most of their gold is owned by foreigners. The Federal Govt would have to first fight with the WA Govt so there would be a time horizon for owners to get their gold to a safe jurisdiction.

How long would it take to shut the border(s) to prohibit the movement of physical gold...a late night Act of Parliament (or by decree in a 'less democratic' state)?

The Perth Mint became an international member of the Shanghai Gold Exchange (SGE) in 2014, which allowed it to sell gold directly to Chinese distributors. This membership has enabled the mint to expand its market presence in China significantly. Since its accreditation, the Perth Mint has delivered over 800 tonnes of gold valued at approximately USD $33 billion into China. This positions the Perth Mint as a major player in supplying Australian gold to the Chinese market, which is the largest consumer of gold globally.

I don't think the Aussie federal govt could get away with it.

J.C. "Which revolution are you referring to? "

Pretty much all of them.

That's how they get their names. (It's not a revolution without the massive transfer of wealth.)

Take, for example, the 'industrial revolution'. The losers were the big land holders that couldn't get remotely close to the yields that manufacturers could derive from the same number of investment $$$.

I guess that wasn't what you were thinking of, right?

You were thinking of revolutions involving the overthrow of governments?

There are very few of these, almost none, where they didn't result in massive wealth transfers. Off the top of my head - I can't think of any. (And please don't pick the individual scoundrels that seem to get richer in a revolution as examples. They are the exception, and sometimes the cause, rather than the rule.)

I'm not aware of gold being confiscated during the industrial revolution. Please enlighten me.

You're likely not aware but central banks have been net buyers of gold since 2010, following decades of being net sellers during the 1980s, 1990s, and early 2000s. This shift was influenced by financial crises, such as the 1997 Asian financial crisis and the 2007–08 global financial crisis, which highlighted gold's value as a safe-haven asset. Since then, central banks have consistently increased their gold reserves annually.

https://www.weforum.org/stories/2023/03/heres-how-central-banks-have-us…

"You're likely not aware but central banks have been net buyers of gold..."

I am well aware. Their reasons are many and various, including it being 'undervalued', a precious metal used in numerous manufacturing processes, etc. etc.. But, let's be clear, their purchases are fairly trivial in the grand scheme of things.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.