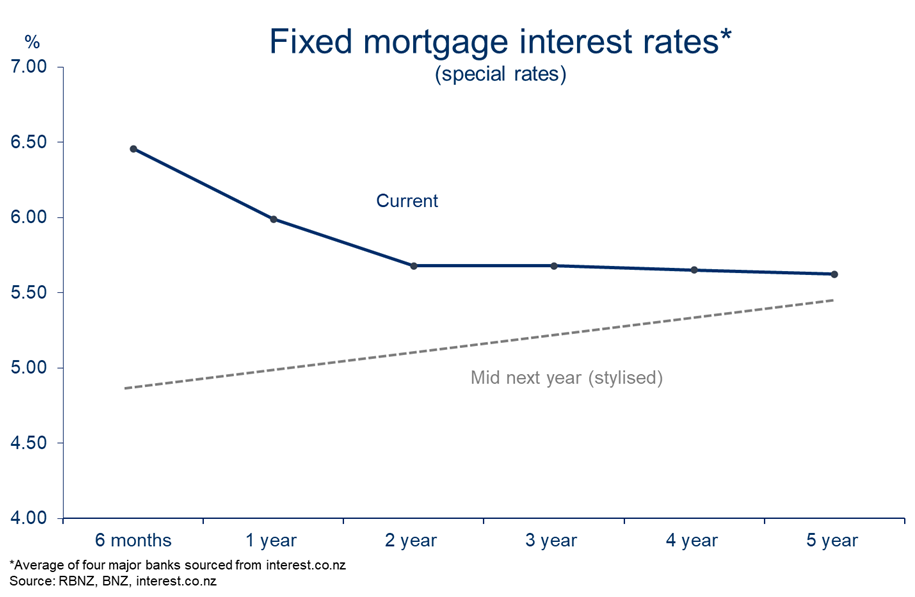

Longer fixed term mortgage rates are already reflecting expected Official Cash Rate (OCR) reductions - but shorter term mortgage rates have more 'downside' potential, BNZ economists believe.

In his latest Eco Pulse publication, BNZ chief economist Mike Jones says one thing that was notable in last week’s round of mortgage rate cuts was the larger (20-25 basis points) declines at the short end of the interest rate 'curve' compared with the modest 5bps or so of cuts at terms of two years or more.

"We think that might be a taste of things to come with those lower, longer-rates already factoring in a schedule of OCR cuts similar to our own forecasts," he said.

Shorter-term rates, by contrast, "have more downside" as they follow the OCR down.

"We don’t forecast the full range of mortgage terms. But the chart [below] provides an indicative sense of how the mortgage curve could look by mid next-year, based on our OCR and wholesale interest rate forecasts," Jones said.

Jones notes that since the start of 2023, mortgage fixers have been "busily shortening fixing terms" in anticipation of lower interest rates.

"In August (the latest month we have data for), a record 86% of new mortgage lending by value was written for terms of 12 months or less.

"This preference for shorter terms will probably stick around in the short-term but we wouldn’t be surprised to see more of an inclination to look at longer terms as we head towards the end of the year," Jone said.

Following a 50 bps cut by the RBNZ earlier this month, the OCR sits on 4.75%.

BNZ economists are forecasting another 50 bps cut in the review on November 27, the final review of 2024, with 25bps cuts at each review next year taking the cash rate to a low point of 2.75% by the fourth quarter of 2025.

Jones says the chances of a "sudden surge" in the housing market throwing the RBNZ off its rate cutting stride appear low.

"The market is still shuffling sideways. Recent and expected mortgage rate cuts have buoyed sentiment and interest, but not so much the hard numbers just yet."

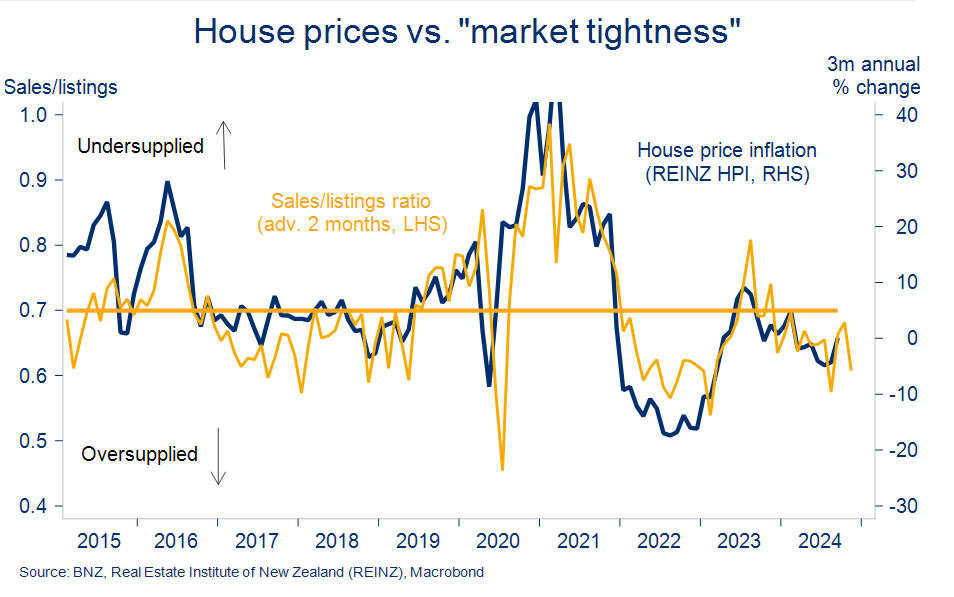

Jones says that for house prices to start rising in a sustained fashion the first thing that needs to happen is the excess supply currently "overhanging" the market needs to be worked off.

"There hasn’t been a whole lot of progress in this regard, as the sales/listing ratio in the chart [below] shows.

"This being so we remain comfortable with our view for a broadly flat house price performance over the remainder of 2024.

"We continue to expect more of a lift as we move into next year. Our forecasts remain consistent with a 7% increase in house prices through calendar 2025.

"It sounds bullish but it’s almost bang on the long-run average. Note too that if it’s even ballpark correct, house prices would still end 2025 around 10% below the 2021 peak. Compare that to Australia where prices surpassed the previous (2022) peak late last year," Jones said.

51 Comments

Some areas ie Auckland Central will come close to 10% 2024 increase when all is said and done.

Leafy suburbs already up circa 4% in the last 2 months!

🌳🌴🥂

Todays baseless predictions and anecdotes brought to you by Cote d'Azur

I expect refixing in May 2025 will be sub 5%. His take on house price increases does seem premature. We have a much larger overhang of supply than Australia. The last crash in 2008 didn't see a recovery until 2010-12. Much like topography, market floors can be flat and wide alluvial plains while the heights are pointy peaks.

Yep, I agree. I have seen a few sold stickers go up on the RE signs I drive past on the way to work in the last couple weeks, so volumes might be ticking up a bit. Also a few more new for sale signs up. Be interesting to see where the prices are going.

Prices are going up.

given the carded 6 month rate is 2% above OCR I would hope so .

Best observation today.

So many just accept high bank margins. They should be around 1% (and falling!) ... Not 2% to 2.5% !!! ... Good god, what they do really isn't that complicated!

If it's made complicated does that count? *Tongue in cheek*

Poor Mike has had a terrible 2 years with his predictions. Only out-douchebagged by the hopeless Tony A. I think this article might be the closest he has been to being right...not like it matters in his game...just wipe the egg off your face and keep smiling.

Not anecdotal, one needs only to review REINZ HPI directly. Might be too much effort for some however, easier to scan a sky-is-falling article on this site!

🥂😅

From the August report:

"The national median price decreased by 0.6% year-on-year, from $770,000 to $765,000, and increased by 1.3% month-on-month."

Looks good. But...that 1.3% increase month-on-month? That's included in the 0.6% fall year-on-year. Buy, hey. If we compare prices to 10 years ago, then we're talking! The history of anything only tells us what has happened. That's what stats do. But if history tells us one important thing, it's that very, very few people 'see' what's coming before it arrives, otherwise mitigating steps would have been taken.

Get ready for a doubling of property prices over the next 10 years by all means. But be prepared for them to halve. It's about surviving the unexpected that's important.

"Our forecasts remain consistent with a 7% increase...almost bang on the long-run average."

Ah yes, Mike. The clichéd price double every 10 years.

It's not that "cliché" bw, it's just fact. Look at any chart (including Interest's), and you will see that the average house value growth over the last 30-40 years has been close to 7% pa.

See mine above.

LOL, lots of charts start off with exponential increases. How do they end?

Off the chart ?

Yes, but in the opposite direction

Yes because we experienced an interest rate supercycle for 40 years. Interest rates diving from 15-20% to 0% allowed asset prices to boom - far above the general rate of inflation. (if you look at the past few thousand years of interest rates, what we have just experienced is an extremely anomaly).

If you understand the discounted cash flow model as a means of determining asset prices you understand how this allowed asset prices to rise at 7% while rents and incomes only went up half of that. But if interest rates become flat or start rising then it becomes mathematical impossible in the longer term for that model to sustain itself - there is a massive hole that exists between the asset price and the cash flows that justify its valuation.

I think we have decades of flat or rising interest rates ahead of us (from a base low experienced in 2020-2021 ie OCR basically at 0%) and that becomes problematic for asset price rises significantly above the general rate of inflation - especially for housing that is entirely dependent upon the cash flows from incomes and rents which is intrinsically linked to the general rate of inflation ie if rents/incomes rises quickly (to justify even higher house prices) then interest rates are going much higher again which will drive asset prices down even further. If rents/incomes rise at 2-3% to keep the RBNZ happy and interest rates are flat, there will be very title house price growth above the general rate of inflation. I mean we could artificially drive interest rates to zero again like in 2020 but we risk a repeat of the last 2-3 years again - inflation way above the mandates level and an OCR 5-10% once again.

Glad to see that you all agree that house prices have gone up roughly 7% pa for the last 30 - 40 years. Which is the only point I was making.

Thank you for clarifying that this was your only point (which I didn’t disagree with you upon!)

The more important point is whether it is sustainable going forward to which I provided an analysis of. Feel free to reply to that analysis if you have points to add to that.

No thanks, not interested in writing a novel of "reckon's"

I appreciate you for doing us both a favour then 🙂

Yip and yet the cash flows that determine the present value of the asset (using a discounted cash flow model)(being incomes and rents) will be forecast to rise at half of that ie inline with general inflation. It is a completely unsustainable model of finance - asset forecast to rise at 7% but the underlying cash flows only 2-3%. The only way this model works is if the discount rate (mortgages) are forever falling. Which worked from 1980’s - 2022ish.

If the discount rate is flat, the model no longer works as the asset can’t rise at 7% while the cash flows rise at 3% and the discount rate is flat. Ie Price = cash flow / discount rate. Dropping the discount rate for 40 years allowed asset prices to rise much faster than the cash flows did. But that may have changed now - see the US 10 year bond yield. We have now broken out of that 4 decade long downward trend. If that is true, for house prices to rise at 7% then the cash flows are going to have to grow a lot = high inflation. But if we have high inflation then mortgage rates will be going even higher in the future than they are now! Meaning those same cash flows will be discounted at and even higher rate = zero or negative asset price growth.

I can see even more asset price falls in real terms in the future.

The banks are still talking like " for house prices to start rising in a sustained fashion" as if it would be a good thing. My hope is that some sort of regulatory hand brake is applied to stop this from happening. Meaningful LVR / DTI / land taxes etc. History would not appear to be on my side.

@middleaged...agree, I just don't get the obsession with wanting house prices to rise, steady as she goes, rises around the rate of inflation has got to be better for the country in the long run. Everybody wants inflation down between 2-3%,but some how want house prices to increase at many multiples of this and think this could be sustainable...so all other prices / costs to remain relatively stable, whilst the price of their main asset to exponentially rocket up...what could go wrong?

Because a lot of peoples financial viability is based upon capital gains and not a cash flow basis. Ie they have purchased negative yielding property - without capital gains their investments are no good. Hence the desperation for continued price rises.

Exactly. Also called speculative gambling.

I_O

I've wondered about this for a while.

At what level of equity do you expect positive cashflow?

0%? 20%? 50%?

you talk about negative yielding properties and people on interest.co.nz talk a lot about investors ruining it for FHB.

the way i see it is if you can be positive cash flow at 0% yield then the investor will buy up everything, if you need 50% then house prices are too expensive.

So what do you think an acceptable level of equity is before a property is cashflow positive?

RI - I don't see the relevant comparison being between one residential property situation and another residential property situation. They're the same asset class. Although there's variations between individual properties, the macro factors move the medians and HPI.

For me the relevant comparison is between residential property and every other potential investment

My personal practice is to calculate gross and net yield based on purchase price - otherwise you're not considering return on invested capital and are only considering return on borrowed capital, therefore ignoring opportunity cost for your invested capital

5-10 years of nominally flat house prices, while wages / inflation runs at (say) 2% / annum would greatly improve affordability for the generations to come. A bit tough if you bought at the 2021 peak, but you cannot please everyone.

Regulations that stopped banks promoting their bias would be welcomed. There is just so much self-interest that we shouldn’t be subject to it.

Meanwhile, Caltex / BP / Mobil economists claim that the government could reduce taxes on petrol to encourage NZ drivers into enormous SUVs.

/sarc

@ Middleaged - "encourage NZ drivers into enormous SUVs".

Why would that be a problem?

Not suggesting we should control people's vehicle choices as well as financial choices? What's next? Free speech zones?

Slippery slope from there towards dictatorship. Careful what you wish for, for your electric car won't save you.

That escalated quickly

Didn't it just!.

I didn't expect to need to actually spell it out, but my point was that banks commenting on the "need" for lower interest rates so we could all buy more expensive houses would be like oil companies encouraging the government to ditch petrol tax so we could all drive bigger cars.

@gwgb

"Why would that be a problem?"

At least two problems come quickly to mind

1: All of our petrol is imported so using more petrol means a worse balance of payments.

2: More petrol used = worse air quality = more health problems.

And speaking of stats; the 10 year property-always-doubles 'rule', and the unexpected. Here's an event that none of us experienced, but all have a vague knowledge of (and there's some spookily similar things happening this very day):

"Using new data on market-based transactions, we construct real estate price indexes between 1920 and 1939.

During the 1920s prices reached their highest level in the third quarter of 1929 before falling by 67% by the end of 1932 and hovering around that value.....The value of properties strongly co-moved with the stock market between 1929 and 1932. A typical property bought in 1920 would have retained only 56% of its initial value in nominal terms two decades later."

https://www.hbs.edu/ris/Publication%20Files/Anna_tom_59f6af5f-72f2-4a72…

We are not in the Great Depression. I can’t see how this data is relevant. Policies put in place at that time actively tanked the economy (the equivalent of the government implementing austerity in response to the pandemic)

the chances of a "sudden surge" in the housing market throwing the RBNZ off its rate cutting stride appear low

Any reason why a turn in housing sentiments is being mistaken for a stronger economy and/or inflation? The markets are overly confident that the current economic downturn is solely due to a contractionary OCR and not glaring structural issues within our economy.

Where does our government vowing to cut fiscal spending even further sit in all of this?

Proportion of working-age Kiwis on main benefits is close to levels last seen during the GFC. What happened back then? RBNZ cut OCR from 8% to 2.5% within 10 months back in 2008/09 but unemployment didn't begin heading south until 2013.

If you are a low wage couple with kids and both of you are working. If one of you loses your job it is likely the income of the other will disqualify you from many WINZ benefits. I expect some do the math and work out they are better off both not working and maxing out WINZ assistance. More free time to plan a move to Australia

Which is why I reckon we should replace most of the welfare system with a universal UBI.

Where is Yvil - Jimbo literally uses the term ‘reckon’ in this post.

Watch out Jimbo you might have the thought police on you soon for offering an opinion.

@ Independant Observer - Nah we voted out the ones that tried to pitch free speech as an act of terrorism, & deliberately confused difference in opinion as hate speech last election. Power corrupts given enough time. If we had let them reign any longer, the thought police may have actually been a real thing, rather than a sarcastic joke.

Your view might be a bit more extreme than mine on this topic but generally agree with what you’re saying. I think the Dems in the US are the same hence why I’m hoping the Republicans win the election.

When interpreting the graph, I think it says only 6 out of 10 houses sell within a 2 month period? pretty low isn't it

Also I went to an open home and the place was buzzing like bees around a honey pot only to find out virtually no one turned up to the auction as they were all conditional buyers

Also, not everyone at an open home is in the market for a house. Many are probably just bored and want to browse for décor ideas.

Once again, an example of how commercial banks coordinate their commercial activity via their "economists". This is anticompetitive behaviour in plain sight.

@independant observer - what are you spruiking- it seems like you understand the economy in opposite world - are you trying to save people from making a mistake in property -you seem anxious to prove that property is not the way to go - maybe a bit more observing and a bit less opinion?

Glad to see Independent_Observer is living rent free in your head. The only place one can live for free!

@IO perhaps you are living here rent free however your anxiety is sticking out like a dogs bollix

Looking at the more affluent eastern suburbs of Auckland prices are moving north again. I don't understand why real estate agents still stay "below CV" CV's were inflated figures from June 2021.

Whilst its not always analytically correct the Homes and Oneroof sites do give a more real price range. In the last two weeks I have noticed houses selling in the higher or above range. This is now moving out to the suburbs. looking at the clearance rates today they were high too. Last 18 months has been in the lower ranges for selling and price paid.

The cycle begins again...I do not see it ever returning to the ludicrous prices people were getting late 21 to early 22 though. A crystal ball would have been nice here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.