Kiwi mortgage holders have shortened up the terms of their fixed-rate borrowing much more than they have before previous Reserve Bank (RBNZ) interest rate easing cycles, according to BNZ's chief economist Mike Jones.

In his latest Eco-Pulse publication, Jones has had a detailed crunch of where mortgage holders stand with their fixed rate terms ahead of expected reductions in the Official Cash Rate (OCR) by the RBNZ.

He notes that with the position taken by many mortgage borrowers "interest rate relief will flow through to mortgage borrowers relatively faster than otherwise", as rates come down.

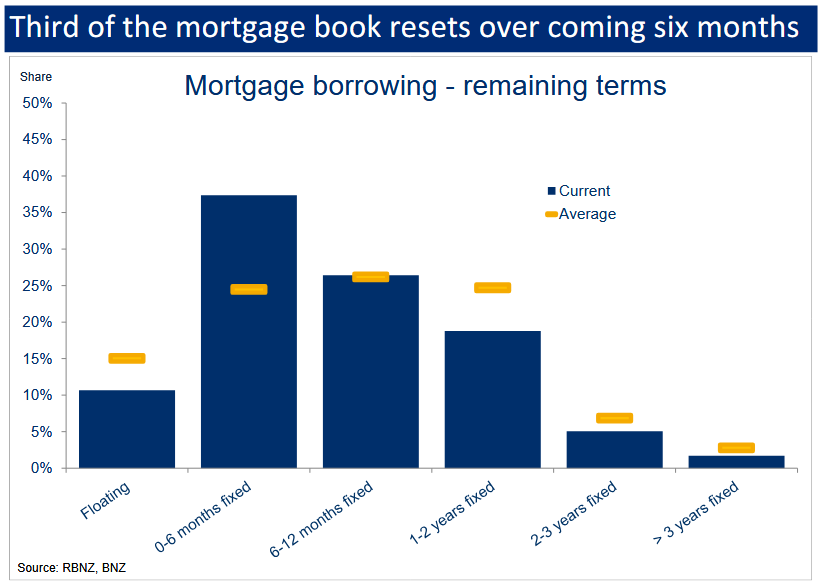

Since February, about three quarters of all new mortgage lending has been at terms of less than a year, Jones says.

"This preference for shorter terms means the overall mortgage book is now quite short. The fixed terms on about 64% of mortgage lending will reset over the coming 12 months (74% including floating borrowing). That’s well above the 51% average run-off rate going back to 2017."

And it is over the coming six months where the mortgage book is most short relative to average.

"About 36% of outstanding fixed rate borrowing will roll off over the coming six months. The post-2017 average is 24%," Jones says.

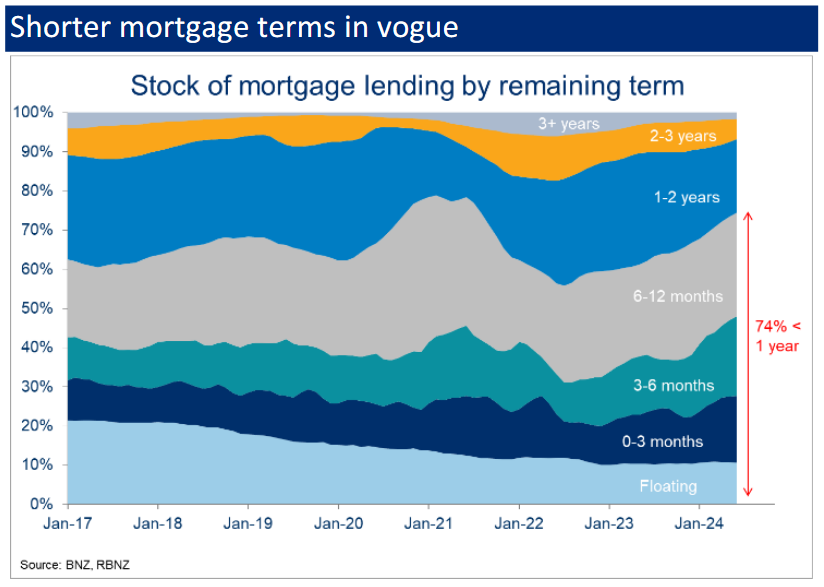

Comparing now with the start of previous Reserve Bank-led interest rate easing cycles shows that the mortgage holders are going shorter, earlier.

Jones says just prior to the easing cycle starting June 2008, the proportion of mortgage borrowings with remaining fixed terms of one year or less was around 48%. Just prior to the 2015 easing cycle kick-off it was 54%. In May of 2019 it was 67%.

"As noted earlier, it’s currently 74%. So it appears mortgage borrowers have shortened up the term of their borrowing in anticipation of the coming easing cycle much more so than prior to past cycles," Jones says.

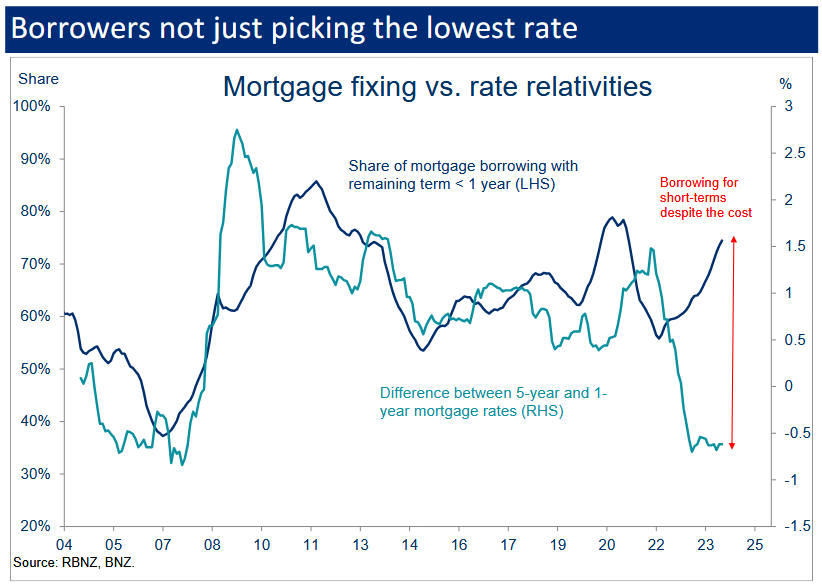

The current approach of mortgage holders now has been all the more noteworthy "given the extra upfront cost involved in going short".

"Short-term mortgage rates have been above longer-term rates (an “inverted” mortgage curve) since mid-2023. Over this period, one-year fixed rates, for example, have been an average of 50-60bps [basis points] higher than three and five-year rates."

Jones says there is "two-sided risk" to the going-short strategy.

"And the proof of whether it proves to be the right one will be in the pudding, and we’re not there yet, but the apparent break from the ‘pick the lowest rate’ past looks more like strategic risk management."

The BNZ economists' current assumption is that the RBNZ will start cutting the OCR in November of this year and move in steady 25bps increments, taking the OCR from 5.50% currently to 3.50% by the end of 2025.

"We describe this as an 'assumption' rather than a forecast as it will almost certainly be wrong. For example, it is quite conceivable that the Reserve Bank will stop to pause and assess several times through the cycle, and there’s also the distinct possibility that a larger-than-25bps cut will be delivered at some point," Jones says.

He cautions that while mortgage borrowers may well be positioned for lower interest rates more so than past cycles, it’s still going to take a while for lower rates to flow through.

"The tanker takes a while to turn, just like we saw on the way up.

"The ‘effective mortgage rate’ – the average mortgage rate being paid on outstanding debt – is currently still rising. That’s despite mortgage rates having peaked around the start of the year. What’s more, and based on our interest rate forecasts and rough estimates, it’s got a little further to rise before flattening off around 6.5% towards the end of this year.

"It's another reason not to expect any immediate change in the fortunes of the presently weak NZ economy, even as interest rates start nudging lower. Most of the flow through effects will occur next year."

49 Comments

Has a trap been set?

Just maybe.

What trap?

If history serves as a guide you're again going to put your foot in yours....

The imaginary trap to lock borrowers in short, only for interest rates to be 10% by Christmas, guaranteed of course 😉.

Always a risk, make your own choices. Would say if that occurs, based on the borrowing stupidity of the last ten years that would decimate all of the interest only leverage monkeys, and drop house prices... hard. Could be a good thing for NZ savers and grafters. Leverage ponzi would start to burn white hot.

Lets not underestimate the impact of overpaying for a house, perhaps paying 1mil for it at peak and now its worth 700k

That's 300k to repay at 5% (6's right now) over the life of the mortgage

- It is less money to spend in the NZ economy.

- its money you could have been saving for retirement.

- Its dead money that eats at your soul.

Is it any wonder so many are scared of overpaying right now when we are only half way down the slippery slope.....

Just stop with this “halfway down the slippery slope nonsense” Sound utterly foolish.

I try not to be rude of those who make different predictions to mine (and I'll happily admit I am somewhat optimistic). But to believe we are only half way through the decline seems to be more a hope then a reasoned deduction from the data.

We are currently 2.9% up YOY. Even if this is a dead cat bounce you surely have to admit that momentum is dropping?

It’s a zero sum game. That money was taken off the table by someone else and spent or invested.

The wealth transfer has been great for many.

"We describe this as an 'assumption' rather than a forecast as it will almost certainly be wrong."

Maybe it's time we just realise it's pointless listening to them any more.

Stay tuned tomorrow when yet another economist gives a reckon on what interest rates are doing.

Smart money filling their boots now. Quelle horreur! That excludes most of the dour sour bunch on here😘

Not long to wait now for the cuts to start coming. Fully expecting an instant turn around in the housing market sentiment by Christmas with the only possible problem being more bad weather in February.

Ok...got ya. We are at the mercy of a sunny Feb.

Adrian...hire a weather forecaster.

I agree, I expect a fairly swift turnaround too, depending on how big the cuts are. But then again I have been surprised by the housing market many times before.

I really don't think so.

Actual industry in NZ is in a bad shape.

Exactly. I predict an economic slump in Nz for housing and related activity for a few years.

Oldies want to sell, most skilled youngsters are comparing nz with Au and choosing to move.

The country simply isn't an attractive place to live for people in their 20s and 30s. Which is killing us economically and socially.. the public services are already noticeably crap vs alternate countries coz we don't have the tax revenues or people to run and upgrade them effectively

Who would want to pay $1m + to live here on a low salary.. vz aus house for 800k and a higher salary. With all the public services and great infrastructre to raise a family. And money left over each month to save.

Anyone expecting a boom here is dreaming.

Logically I agree, however that has applied for decades, why have the last booms happened?

One word - China.

China itself is in massive decline. Seems like everyone has forgotten this elephant in the room.

All the issues you highlighted are everywhere though. There is nowhere to run (although many will try).

These interest rate cuts are going to be HUGE for the property market. Yes, lots of supply to get through, but with build rates slowing down and rates 2% cheaper it would seem the next 6mths will be the time to buy

That's a big call. Personally, I can't see prices turning north again for another 12-18 months.

His last post was 2 years ago. Looks like he's decided it's time to jump back into the forums & save the market!

#fear

I agree, if you missed the August till September 2023 then August to Christmas this year will be the next best option. The DGM's were holding out for 10% rates, that was never going to happen, as predicted the rates maxed out at the limit the housing market would take.

🤣😆 Zwifter, you crack me up. So August to October is now no longer the "last opportunity to enter the housing market" ?

Like a few other's here rendered embarrassed, your predictions have morphed along with real and unavoidable realities.

Your posts are amusing!

The good houses will be desirable.

If you bought a townhouse in an outer suburb or high density cookie cutter place, then good luck.

The good houses will be desirable.

Now that buyers have the luxury of choice - that pretty much sums it up. We are no-where near peak unemployment so it will be interesting to see the progressive effect this will have on house sales/prices and rents achieved and therefore yields. From now till third quarter 2025 still a lot of headwind. This is assuming there is no global economic shock of course.

"The good houses will be desirable" - every house is desirable at a certain price, and its all relative. If you can pick up a townhouse in an outer suburb for $500k, then less people will want to pay $1mil for a detached house in an outer suburb. Then if you can pick up a detached house in a nice outer suburb for $800k, less people will want to pay $1.5 mil for a townhouse in a central suburb. Then if you can pick up a townhouse in a nice central suburb for $1 mil, then less people will want to pay $4 mil for a detached house. Etc etc.

Exactly my point, the weighted factor of 'desirability' will keep the price of some houses steady, and others (shitbox townhouses) in the toilet. You will be able to model it mathematically with desirability or whatever other adjective you want in place of that as 'factor x' in the equation.

And in all honesty you would have likely seen the same model play out since 2022. The houses that tanked the market is high density crap (especially in outer 'burbs) trying to be offloaded.

There is always demand for a quarter acre house which has has been maintained well in a nice suburb. Supply of them is low.

And it is precisely why regional property hasn't been hit as hard as larger centres where these hd subdivisions have been built.

Perhaps the last 6 months were the time to buy...I've commented last week that a relative just bought a modest standalone house in Auckland after looking all year (with a 50% deposit, secure employment & finance preapproved). Advised that the last few weeks saw a very significant uplift in open home attendance & interest (at least 4 firm offers to beat on the house) & obtained a 3 brm for previously 2 brm prices in preferred area

Agreed, where is NZgecko now lol?

He is probably busy getting denied offers for 1995 house prices.

Yes I expect the speculators to be returning about now. I'd be tempted if I was such a person.

He just bought. So all his eyes let him see is self justification for a poorly timed decision.

Buying a house is not about timing, it's about lifestyle.

If you got the timing wrong (e.g. 30 Nov, 2021), your lifestyle might be pretty bad right now.

Although looking at the house price chart, there is only a short period (Feb 21 -> Nov 21) where the average house is now in negative equity. For all other recent buyers its just the extremely high interest repayments they need to worry about.

Over the many years the owner owns his house, a market downturn is inevitable but it will matter very, very little. What is really costly is to wait, and wait, and wait !

But that's not the whole truth is it..

The FHB that saved a deposit by late 2021 and decided to wait, is in a better position today.

And if bought the same house today instead of 2021, could be in a much better position in ~17 years time.

$1m with $200k deposit vs $800k with $220k deposit (two years of TDs)

If paying the same weekly amount the mortgage at an averaged 5% interest rate, the mortgage taken out today would be gone 13 years sooner, saving nearly $700k over the remaining 13 years.

It 100% matters when you buy.

$1m with $200k deposit vs $800k with $220k deposit (two years of TDs)

Most houses haven't dropped 20%, and you haven't factored paying rent for 3 years into your maths.

It 100% matters when you buy

Except of course no one really knows at what point a market is at what level.

For instance, people thought houses were expensive in 2017. How does that same maths you used above work in that scenario (i.e. buying in 2017 vs holding out to 2024)?

Why would we apply the same thinking today as in 2017 when the OCR was 1.75% ?

Since 2017 we’ve gone through ZIRP followed by a rapid 2100% increase in the OCR. Now we're staring down the barrel of an all-time recession.

No, this is bs. Again with the poor math.

Watch out its maths, there is zero tolerance from the spelling police on here and the US version is not allowed. Yeah sorry probably anal English teachers running about getting the deck chairs perfectly lined up on the Titanic as it goes down.

Only if you buy before age 30-ish

We traded up in December 2021. ~50% deposit. Currently sitting at 22% equity, and locked in at 4.95% until December 2026.

I can imagine there'll be a few that bought with 10% (or less), that fixed short who are feeling the squeeze. Rates shoot up and loss of deposit. Do they hold on or lock in their losses?

For Specuvestors, it's always about timing the market. Specuvestors will often duplicitously post on here that it's not about timing. After the stupidity of recent years FHB's timing their entry became a better strategy by default. This strategy will now be paying off big time. I think the market is still deleveraging - there is a ways to go yet. On the basis that no quick fire recovery expected, post any purchase, it should be viewed as a lifestyle choice as opposed to a get rich quick scheme going forward.

What a particularly useless graph showing the fix ranges. It's not like people fix for 15 months.

Is a 1 year fix counted as 6-12 months or 1-2 years? Why even bother with ranges? How many people possibly fall into the cracks between 1-2 years or 2-3?

I was thinking the same thing. I would believe that the 6 to 12 months would have the 1 year fixed in it.

I believe the intent is to show the time left on fixed rate loans. For example, I fixed everything for 5 years in May 2021 (yay me!) so I would fall into the 1-2 year range right now.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.