This is the second part of our half-year look at 2024. The first part can be read here.

So, what's 2024 to be? A game of two halves? Or just one rather soggy (w)hole?

Well, while it would be nice to think 'the best is yet to come' for this year, it looks like it would be wishful thinking. Very wishful thinking.

As I write this about halfway through the year, we appear as a country to have descended into something of a funk. The previous mental resilience that we saw in the face of high interest rates seems, all of a sudden, to have crumpled rather quickly. The economy is down. People appear to be down. We are in, well, a soggy hole.

Where do we go from here then? How quickly can we pick back up from this. And when?

In very simplistic terms, we need the following chain reaction:

Inflation comes down, the Reserve Bank cuts the Official Cash Rate, retail interest rates (mortgages etc) come down, people feel wealthier and start spending more money again, businesses start to pick up with the increased spending, more jobs are created. Somewhere in the midst of this the housing market will perk up (this could happen at any stage in the chain reaction; remember this is a country that added 40% to its house prices during a pandemic - there's no bad time for a housing market surge in New Zealand).

As ever, I'm not going to try to specifically predict the timing of any of this as such. I will just outline here what I see as the crucial issues over the remaining six months of this year and what the potential ramifications are. Looking for clues, if you like.

Inflation is the key. The Reserve Bank has set out to smash inflation by hiking the Official Cash Rate (OCR) all the way up from 0.25% to 5.5% in order to take heat out of what was a very overheated economy. Hence, we now have: High mortgage rates, reduced spending, reduced economic activity and now rising unemployment.

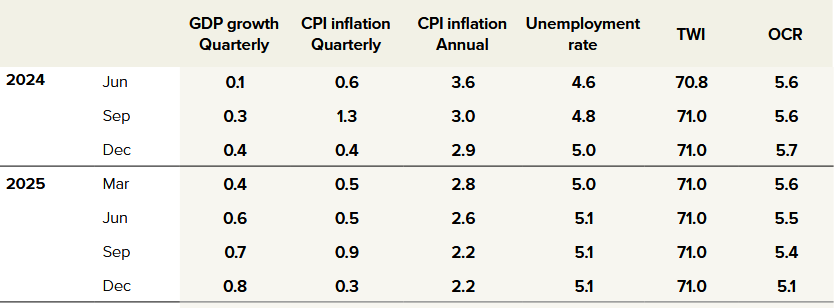

At its peak in this 'cycle' annual inflation hit 7.3%. As of the March quarter it was 4.0%. The RBNZ targets inflation between 1% and 3%, and explicitly, wants 2%. Here's an abridged version of the forecasts from the latest Monetary Policy Statement. (The full table is on page 50).

So, note that the RBNZ is now forecasting inflation will get back under 3% in the December 2024 quarter. Believe me, the RBNZ won't contemplate 'leaving us alone' until then.

But it's not just about the so-called 'headline' inflation figure. The RBNZ frets over domestically sourced, or non-tradable inflation. And this is proving tough to get down. Statistics NZ is releasing the June quarter Consumers Price Index (inflation) figures on July 17. This CPI release will be even more significant than usual just because of how finely the economic situation is balanced. I'll have a detailed preview of it closer to the time.

In the meantime, however, I will say that the RBNZ really needs the June quarter CPI figures to demonstrate signs that, particularly the domestic inflation, is coming to heel.

Prior to the March quarter, the RBNZ had forecast that the non-tradable/domestic figure would fall to 5.3% for that quarter, from 5.9% as of December. In the event it fell only to 5.8%.

The RBNZ is trying again. It's forecasting that as of the June quarter annual non-tradable inflation will, this time, hit that 5.3% figure, down from 5.8%. The RBNZ's current forecast is for non-tradable annual inflation to fall to 4.7% by December. And that of course is the point at which the RBNZ believes 'headline' inflation will fall under 3.0% - to 2.9% to be precise.

We've just got to hope for the best that these forecasts are achieved because the RBNZ's going to keep throttling us till it decides inflation is under control.

Okay, we are getting there - but when?

The RBNZ itself IS starting to show more confidence that inflation will be made to behave. RBNZ chief economist Paul Conway, in recently releasing some new RBNZ inflation analysis, said the bank expects spare capacity to start emerging in the economy over 2024, and this will "feed through strongly into lower domestically generated inflation". He didn't say it, but the message I inferred was: 'Trust us, we are getting there'. Okay, but getting there when?

Frustratingly, nobody can absolutely promise when those inflation figures will definitely be in the kind of retreat that will enable the RBNZ to call off the dogs and start reducing that Official Cash Rate.

As can be seen from the above table of forecasts, the RBNZ is not currently forecasting reducing the OCR till the second half of 2025. Personally, I'm not sure what sort of shape our economy would be in if the RBNZ sticks to that sort of timeframe.

I think the economy has in the past three months, and even more so perhaps in the last six weeks, shown signs of really buckling under. Spending has dried up, the signs are the job market is tightening quickly, the economy is as flat as a pancake. Some economists are already forecasting that GDP will have gone backwards again in the June quarter 2024. And, yes, house prices have gone backwards again and economists are quickly slashing forecasts of future price growth.

Phew. Let's be positive. It is possible that the real swoon that now seems to have come over the economy could see the decline in inflation accelerate - and faster than the RBNZ anticipates. Oh, yes, please.

The wholesale interest rate markets, which like to jump ahead on these things, are currently fully pricing in the first cut to the OCR in November of THIS year. And for good measure a follow-up cut is also fully priced in for February 2025.

Is this possible? Well, yes, I think it is - IF inflation really starts to retreat.

However, I guess if we want to be the ultimate in glass-half-empty pessimists we could also ask, yes, okay - but what if inflation DOES in any case stay somewhat stubbornly high?

Well, that would be when we could really start to worry, I think. And that's why the second half of this year is so important, kicking off with those inflation figures on July 17.

We really need inflation to behave itself - sooner rather than later

If, particularly the domestic inflation figures, stay still quite resiliently high then we are in trouble. Have no doubt. Because the RBNZ would feel compelled to hold the OCR high and the economy would - based on what we are seeing now - start to be squeezed beyond pain.

Conversely, if the CPI figures do show signs of dropping off quickly, then that's very good news.

So, in terms of what happens over the rest of this year, the 'happy' scenario would be inflation retreating to the point the RBNZ starts to at least seriously consider cutting the OCR.

The 'unhappy' scenario would be if inflation continued to be 'sticky' and we would then get to the end of the year with no clear sign of when those interest rates might start to come down.

The best case scenario then would likely be a first cut to the OCR in November. I can't really envisage any situation in which the RBNZ could be convinced to go earlier than then. If the OCR was to be cut in November, that would send the country into the Christmas break in a rather better mood, but would of course not be able to 'save' this year as one of economic stagnation.

So, we would be looking beyond this year and into 2025 for recovery and all that entails, with some spending returning in the economy, the labour market beginning to stabilise and, yes, that housing market starting to perk up again. It would probably be only a gradual recovery, gaining strength in 2026. But a recovery is a recovery. We'll take it.

There's no guarantees

How quickly our economy can start to pick up again is therefore going to be totally dependent on the timing of that first OCR cut. The longer we may have to wait for that, the longer it will take the economy to stabilise and then start to go forward again.

The other point to think about is if inflation does somehow manage to stay stuck above 3%, for how long does the RBNZ continue squeezing? Does there come a point at which the economy simply starts to break? If so, would the RBNZ eventually have to back down on the high interest rates anyway?

All we can do in the meantime is push on through a second half of the year that looks as challenging, if not even more challenging, than the first half was.

Beating inflation has become the be-all-and-end-all. We are just going to have to hope it proves to be worth it.

155 Comments

All this forecasting seems to ignore the basic facts we do know. Here are the last 4 quarters of inflation (latest first): 0.6%, 0.5%, 1.8%, 1.1%. If we swap that 1.8 and 1.1 with something around 0.5, we will be well under 3% this year. We may already be under 3% if the last quarter comes in around 0.1%. And from memory that 1.8% quarter was the reversal of the fuel tax pause, something the RBNZ should look through to an extent.

Sure there are some big rates rises coming up this quarter, but otherwise inflation has been smashed into submission.

If fuel and food end up negative last quarter (seems possible to me), could we see a negative quarter and be well back in band? Would this put some egg on the face of the RBNZ after hammering the economy? Will they be shamed into some big OCR cuts? I’m not saying I’m predicting this, but I’m surprised no one else is contemplating it.

Yes this could happen, and once it does they can cut.

I think they start with 25 although if things are an emergency 50

not sure where the Canada shocking Q uptick came from...

I doubt we’ll see a 0.5 this year. But we may get a few next year if inflation and the economy are dead. With people on very short term fixed rates this will flow through quickly.

Also 2 tax cuts coming up, Auckland fuel and PAYE. Hard to know if they will increase inflation or just decrease the suffering.

? It was 0.6 in the March quarter this year and 0.5 in the 2023 December quarter. We're highly likely to see figures around that level for the rest of this year.

Sorry I meant a 0.5% OCR cut by RBNZ.

No, the Sept quarter is likely to by quite a bit higher than 0.5 due to rates increases kicking in then

Reckon they will remain hawkish with statements and actions until we have 2 quarters within inflation target. They will wait to see the impact of tax changes also.

Then how they try to stimulate the economy will be very interesting. Rather than drop the ocr too far finding a way to get money in the hands of the right people would be a good start.

Doubt it. The last two quarters had modest inflation because of favourable fluctuations in oil prices and exchange rates, and because of seasonal falls in food prices. And because not many big annual price updates (rates, utilities, wages etc) fall in those quarters. Statistics NZ produce a seasonally adjusted version of CPI which suggests the last two quarters were in line with 3.1% annual growth and that's about where I expect us to end up once another two quarters are in.

Agreed. 3% is the new normal.

All this forecasting seems to ignore the basic facts we do know. Here are the last 4 quarters of inflation (latest first): 0.6%, 0.5%, 1.8%, 1.1%. If we swap that 1.8 and 1.1 with something around 0.5, we will be well under 3% this year.

No. That's CPI data. You don't really know what inflation is, but what you should know is that the CPI is likely to understate what the actual inflation really is.

Why is kicking off the property Ponzi again considered "good news"?

TINA?

There are alternatives. But this government likes the status quo and are too fearful to make the changes that must be made,

I guess people spend more when they’ve got a few mil of paper wealth behind them. Obviously not good long term, but in terms of GDP / employment / etc it’s a big boost.

Good for the winners of which there are less of, bad for the losers of which there are more of. All good though, just import more cannon fodder and they can high five our young and talented as leave the country for a better life.

Good for the winners of which there are less of, bad for the losers of which there are more of.

This totally depends on the perspective you're looking at things. From an asset base, more losers, but as a human, just the advent of something simple like pain free dental care makes everyone a winner.

And by that logic, there is nothing worth discussing anymore. Just be happy with whatever comes, so long as it is better than anything you can read in recorded history.

Because the fortunes of the property market is intrinsically linked to the fortunes of the overall economy.

much like the share market was in 1987

Much more so, because we live in houses, shares aren't a need.

However many leveraged their houses to buy more shares and lost it all. All relative.

Agree, the higher housing costs go the more young are forced to leave.

In areas where house prices drop substantially and stay that way, EVERYONE is forced to leave.

Refer Detroit, etc.

Your framing gets causation/correlation completely mixed up.

Detroit didn't collapse because house prices fell. House prices fell because the car industry in Detroit got outcompeted by Japanese/European cars.

NZ and its relationship to housing is not the same as Detroit and its relationship to housing. In NZ house prices going down and becoming more affordable for the median earner (in real terms) would be a great thing for the majority of society, the overall economy, and the future prospects of NZ by not contributing to another few decades of malinvestment.

Whereas in Detroit the decline of the car industry due to competition led a decline in real wages for the median worker, which drove down the housing market overtime as people left.

It's exactly the same thing. Houses in NZ are only worth the high values they are because despite what the per Capita returns are, it's still roughly tracking forwards in aggregate, not backwards.

The sort of environment that'd have houses downtrending and staying low, would be a commercially depressed situation.

> Houses in NZ are only worth the high values they are because despite what the per Capita returns are, it's still roughly tracking forwards in aggregate, not backwards.

Isn't this just saying "House prices are high because they've consistently gone up overtime"? Which is true but the question is why have house prices risen/fallen and what are the preferred/likely conditions going forward. I could say this about any housing bubble that ever happened and it would be true up until the point it popped.

> The sort of environment that'd have houses downtrending and staying low, would be a commercially depressed situation.

It depends why prices got to where they are and what conditions are setup going forward. For instance, the foreign homebuyer ban is a clearly a rule that will lead to lower house price growth on average without necessarily depressing commercial activity. There is also the question of what type of commercial activity we want to encourage. We could legalise meth tomorrow and probably see a big increase in commercial activity but it likely wouldn't be a good thing for the country.

"GDP goes up therefore times are good" is generally a pretty bad metric for assessing overall societal economic health.

Housing downtrending and staying lower, currently, would be a good thing. NZ has some of the least affordable housing to median incomes in the world so clearly it isn't fundamentals like productivity growth that drove prices to their current heights. The key thing NZ needs to do is have house prices decline to the point where they are reasonably achieveable for median income owners to get, then setup economic conditions to prevent what has happened the last few decades of housing being seen as a tool to "build wealth" rather than primarily a consumption good. Some good headway has been made with stuff like DTI ratios, foreign homebuyer bans etc, hopefully reforms of the RMA. But way too simplistic to say "When Detroit house prices declined it meant Detroit was doing badly therefore if NZ houses decline it will mean NZ is doing badly". Need to look at the overall picture. Slow house growth in line with the growth in median wages is a good thing but what we have had with house prices far outstripping the growth in median wages has not been a good thing at all.

Isn't this just saying "House prices are high because they've consistently gone up overtime"?

Not exactly. It's saying that as an economy grows in wealth, it attracts more people, imbalancing supply and demand. And the continued prosperity influences people's decision making when it comes to the amount they're willing to put forward to secure a property - you're not going to pay top dollar if the economic prospects of an area are trending downhill.

"GDP goes up therefore times are good" is generally a pretty bad metric for assessing overall societal economic health.

It's "generally" a great method, but I'd agree the devil is in the details, how the figure was derived.

The key thing NZ needs to do is have house prices decline to the point where they are reasonably achieveable for median income owners to get, then setup economic conditions to prevent what has happened the last few decades of housing being seen as a tool to "build wealth" rather than primarily a consumption good. Some good headway has been made with stuff like DTI ratios, foreign homebuyer bans etc, hopefully reforms of the RMA.

Fundamentally we need to resolve the physical act of supplying enough houses cheaply. All the other reform methods are pissing into the wind until you do that - and if you do, the reforms are far less necessary.

We need to waggle hammers, not pens.

I thought they left due to no jobs etc, I don't see low house prices as a driver - more the result of other things. Therefore, I don't see pumping up house prices as aiding the economy overall other than potential short-term benefits. Long term pain can be the only outcome of focusing on the unproductive folly of tying up capital in land values.

It depends. If housing costs go up because median wages are rising more rapidly than inflation for the average person (so productivity is increasing) then it doesn't force young people to leave.

Unfortunately that is not what NZ has. We have had housing cost increases far exceed the gains in wages in real terms meaning, on average, the standard of living of the average Kiwi has declined. NZ has a housing problem that is contributing to a productivity & economic problems. Making housing more affordable to allow for more money to go to better investments etc is a good thing in our context.

Absolutely TAT, I was just questioning the narrative that higher house prices are a good thing for the economy overall.

With property owning segment of the overall economy increasing their fortune while the other's can get stuffed.

Cherry picking housing ponzi shows how tunnel visioned you are. The fact you neglect jobs, disposable income to spend on goods and services including local businesses, confirms you are a doomer through and through.

Stabilising an economy and employment situation in crash-and-burn mode is supposedly the good news.

This article is about the economy, not property.

Could've fooled me.

Exactly! How moronic that increasing property value is seen as positive! The cost of housing is the most significant determinant of social cohesion and development of human capital. Current housing market has caused despair and hopelessness for many many young people.

I am not envious, I already own big house , mortgage free but when I look around, I see a lot pain and disillusionment.

Rates, insurance, and public sector spending will team up with our 3rd world statistics reporting to drag this out for several months longer than needed.

Has insurance gone up recently, or are some commentators just starting to see last years increases?

Insurance is going up another 20% ish this year per my broker mates. The reinsurers are still working out how to price in all of the global floods

Yes we lost a vehicle that was in a yard in Wairau Rd getting fixed. Vehicle losses where massive.

I think most rural properties suffered some damage, though most did not have fence cover.

There could be a lot of deflationary forces over the next few years (again not a prediction just a possible scenario). Maybe these floods are not climate change and are just bad luck, a few years without claims should see lower reinsurance and premiums. If interest rates drop, borrowing costs for the likes of councils will decrease and we may see much smaller rates increases. More EVs could see fuel demand peak and fuel prices drop.

I suggest you rock along to an insurance convention. You won't find any skeptics among the people scrambling to pay the ever-increasing bills and doing forwards-looking sophisticated modeling for our world.

Premiums will never go down.

Absolutely right - even the low-end estimates are horrific.

I’m not a skeptic at all. But there is also no guarantee we are going to get a repeat of last year any time soon. Extreme weather events will no doubt be more frequent, but that may already be covered for a decade or two by the recent significant increases in premiums.

Maybe not deflation, but hopefully some disinflation.

Disinflation is still inflation.

When insurance was priced on a one in 100 event and now needs pricing at a 3 in a 100 (or whatever), you don't need rocket science to see what follows ..

We've chosen over recent decades to build high density housing on flood plains and liquefaction zones. Trying to blame climate change for the results of this is disingenuous. Also, "climate change" is a nice little excuse to bump up insurance margins.

councils have big infrastructure gaps, in WGTN they have an everything gap.

FED rate is the benchmark... Uncle Sam makes the rules....lol

"Baby, im tired of toein' the line , Dont know why you wanna jump on me!

(Rocky Burnette... "Tired of toein' the line")

I have some bad news. The idea that the economy picks up because people 'feel wealthy' and start spending down their bank balances is nonsense. The idea is included in old and broke economic models that ignore credit money creation.

How it actually works, particularly in NZ, is that people or businesses feel positive about investing in property (mostly), so they ask the bank to print them some money to buy or improve property. Some of this money gets spent into the economy and this stimulates economic activity.

The money stops doing any stimulatory work when it is either saved, taxed back by govt, or used to repay a loan.

Because our economy is so efficient at channeling money to wealthy savers onshore and offshore, it takes a significant net inflow of credit money to keep the economy ticking along.

When credit stops flowing (2023/24), Govt deficit spending has to take over or the economy would literally implode. You can see the combined govt and bank money creation trend clearly in this graph, which uses inflation-adjusted figures.

The new Govt financial year starts on Monday. Govt are planning to reduce deficit spending from 5.3% of GDP in 2023/24 to about 1.9% of GDP in 2024/25. Pulling out of the recessionary nosedive we are in now will therefore require banks to lend out (net) about 8% of GDP - approx $35bn. The figure for the last 12 months was $16bn.

So, what will actually happen is that RBNZ will reduce rates with the Fed towards the end of 2024 and use some 'we are now confident that the war is won' line regardless of what the data says.

By this time the economy will be in a tailspin and govt will be blowing their budget to pay the welfare bill (benefit numbere are already well above Budget 24 forecasts). Unemployment will be in the late 5s and real wages will be sliding backwards.

In early 2025, a painfully slow recovery will start fuelled by poorly negotiated 10% interest rate private finance deals, which will be used to build BNPL roads and infra.

Nah, forget all the economic calculations, it’s all about spending, ask any business why they are struggling at the moment. People spend when they have money and when they feel good about the economy. A few decent OCR cuts will start that off.

Where do you think people get the money to spend?

In NZ - cheap borrowing.

Anecdotally I have stopped spending as my mortgage is now costing a fortune, this decreases the amount I can spend and also encourages me to make additional repayments with the money I still could spend. A few juicy OCR cuts will dust off my wallet after a max of 6 months that I’m fixing for. I have decided that I’m already putting enough into the mortgage, any OCR cuts will be spent and not used to pay it off quicker. It wouldn’t take much to double or even triple my discretionary spending.

Yes, that was my point - borrowing drives spending. When we stop borrowing, spending slows quickly.

Ok I must have misread. So if RBNZ cuts OCR, economy will recover fairly quickly, right?

I reckon it will depend on whether inflation is sticky or unstuck.

In most balanced economies quickly cutting rates should stimulate the economy if lending follows, but in NZ 70% of lending is for residential property. So if that market is still depressed (still unaffordable and high unemployment), then there will not be much new lending, rather people will be able to afford the power bill, rates etc.

I do not see a sudden recovery to property in NZ as its still incredibly expensive compared with income, wage inflation is minimal and job security is scarce. DTIs are about to kick in.

I agree, I don’t see property taking off either (although stranger things have happened). I think current property prices have already priced in rate cuts. But I think spending will return to some extent

There is a lot of property on the market right now, I wonder how much is up/down sizing, vs leaving for aussie...

Some will be investors getting out.

Some is clearly debt related.

As you say above, a lower OCR will (slowly) release more money for discretionary spending (due to lower mortgage costs) and should lead to more people borrowing money to buy houses, some of which will get spent into the economy. My rough guess is that OCR will have to start with a two before we see any real stimulatory impact (restart of the bloody housing ponzi). Look at the mortgage cost index for example - either house prices have to fall significantly or borrowing costs have to drop a lot.

Looking at overseas recovery from housing crashes, house prices dont start ticking up until near the end of the interest rate drop cycle, not at the beginning. This will be 2-3 years away minimum.

re ... "restart of the bloody housing ponzi"

May not happen if the RB aggressively uses LVRs & DTIs. (I live in hope.)

And if new houses escape restrictive LVRs and DTI ... Well. We know what will happen. New stuff will be created faster. (Like I said, I live in hope. Maybe even a fantasy world where good things happen.)

Imagine how much easier it would be to stimulate our way back from a recession if business lending took up more of the banks portfolio, and people which more easily access the credit needed to invent, produce, develop and manufacture new goods and services, create jobs etc.

"Yes, that was my point - borrowing drives spending. When we stop borrowing, spending slows quickly. "

I think that Jimbo's point is that instead of money being shipped off to lenders; who either save it, or take it away overseas; more will be circulated by to other places. In that being the case, i.e. the velocity increases together with far more people being recipients of it, things can improve without more borrowing. (Sadly though, too much will be spent on imports and we're back to needing to increasing borrowing again.)

(edited: Sorry Jfoe. I see you clarified just above.)

Indeed:

The rate of interest – the price of money – is said to be a key policy tool. Economics has in general emphasised prices. This theoretical bias results from the axiomatic-deductive methodology centring on equilibrium. Without equilibrium, quantity constraints are more important than prices in determining market outcomes. In disequilibrium, interest rates should be far less useful as policy variable, and economics should be more concerned with quantities (including resource constraints). To investigate, we test the received belief that lower interest rates result in higher growth and higher rates result in lower growth. Examining the relationship between 3-month and 10-year benchmark rates and nominal GDP growth over half a century in four of the five largest economies we find that interest rates follow GDP growth and are consistently positively correlated with growth. If policy-makers really aimed at setting rates consistent with a recovery, they would need to raise them. We conclude that conventional monetary policy as operated by central banks for the past half-century is fundamentally flawed. Policy-makers had better focus on the quantity variables that cause growth.

Hear. Hear. Thanks Audaxes.

Seems an OCR of 5.5% is now viewed as "high", I guess it would be if you jumped to it from fairytale rates... Nobody's lined up outside banks with placards complaining about credit card rates . The 'FIRE' economy needs low rates so it can do what? .... We cant keep up with infrastructure already . Do we want another run on RE where the ratepayers enjoy a hefty lag before reality shows itself.Then everyone that enjoys a sizeable 'CG' whinges about their rates bill . The Taxpayer ends up carrying the burden while the smart money players eject to the sideline and watch all hell break loose waiting for the next low OCR to roll in . I think if you want stability...you need to build it into your economy and having an OCR that extracts a penalty for credit is essential particularly if your nation is already sitting on a mountain of DEBT. The alternative is a CG TAX that bites hard... The powers that be will do what they do ...but are they doing what really needs to be done....?

We cant keep up with infrastructure already

That's due to the absurd economic structures, extraordinary overheads and poor planning/technical incompetence related to building infrastructure in NZ.

No. The ants have eaten all the easy sugar.

A new road requires new energy and materials. An old road does to maintain it.

The easy cheap stuff has gone.

Penny needs to drop for many.

JJ - the only trickle down spending that happens in nz, is buying more property, get more debt…we’ve just seen this unfold and what a mess it leaves behind. You want to repeat? Nuts.

I’m not saying I want it, I’m just saying it could happen. Although it doesn’t really make much difference, without a decent increase in supply house prices will be whatever people can afford to borrow, with higher interest rates the house price might be lower but the repayments are the same (in fact currently much higher than the peak).

The question is if the credit isnt expanded by increased lending on property AND the Gov is self imposing a credit limit where is the credit expansion to come from?....what apart from the property ponzi entices investment in NZ?

More local production? required infrastructure?....4 decades have demonstrated that there is no appetite to invest in those options (at the level required) and successive governments have abdicated that responsibility to the private sector.

If RE inflation cannot be maintained by local incomes then the inflation (in aggregate) will be maintained by volume (migration)....tis the only game in town....nevermind that it is unsustainable and unproductive.

"The money stops doing any stimulatory work when it is either saved, taxed back by govt, or used to repay a loan."

Would I be correct in that the billion of dollars of equity LLs have locked up in residential property you included in 'savings'?

As 'savings' ... it is even less stimulatory than term deposits which most people think of as 'savings'. And that fact is a major problem for much of the western world. i.e. the money supply grows, but less and less is of that growth actually in circulation.

I tend to separate out assets (like equity in properties) from fixed NZD denominated assets / liabilities like term deposits. Probably because I conceptualise the economy with stocks and flows of money as my starting point.

When a landlord buys a house with a loan, the bank issues newly created cash to the buyer, and the seller receives the actual cash. It is the journey / velocity of this cash thereafter that determines the stimulatory impact on economic activity.

But, yes, I guess landlords' equity could be considered savings. Remembering that for all the bleating, landlords own 75% of the total value of the houses they rent out. We tend to hear a lot about the 25% that is mortgaged.

Thanks for the clarification. Your approach is not unsound, conventional even. ;-)

But it is worth considering that quite of bit of the 75% of equity (stagnant capital) can be very quickly turned into cash via credit creation (becoming active capital) while it's reduction is initially the length of a loan / mortgage. The RBNZ will almost certainly underestimate the speed this can occur at. And once again they'll be caught acting far too late to stop the damage.

Yes, liquidity can be fluid! My guess is that RBNZ are prepping to use DTI / LTV to counter any surge. But how will our economy work without regular bursts of excitable borrowing or govt spending?

Most of the money created in our economy is debt based. If debt levels go down and debt is net repaid that is equivalent to money being destroyed out of the economy. Recession automatically ensues.

What money is created that is *not* 'debt-based'? Money is debt.

I agree with your basic premise though - but debt can deflate without recession if, for exampke...

- Govt takes private debt onto it's balance sheet

- Private savings are reduced

- The country runs a large and sustained current account surplus

- Taxation is used to redistribute money aggressively to stop it pooling in savings accounts

The problem with the system that complicates it for understanding is (imo) the impact of currency and the free movement of capital....it is a simple system if you remove the impact of multiple currencies and the ability to enter and exit markets....however as a certain NZ Telecom executive let slip...make it complicated and the plebs wont notice....think she may have learnt that from central bankers.

ALL of the money in a fiat economy is debt based....and that debt is theoretically backed by assets.

And it is crucial to understand that in order to pay interest (at any level) that credit (debt) must grow

As houses increase in price and as the NZ population increases it only stands to reason that the total debt pile increases over time.

Correction, the debt is backed by resources.

Hilarious how the only way we stay afloat, let alone progress is to create the same amount, or more debt. We promise further and further into future resources just to maintain our standard of living and feel wealthy. System is broken and needs a revamp.

Does there come a point at which the economy simply starts to break? If so, would the RBNZ eventually have to back down on the high interest rates anyway?

Yep, because their mandate is about maintaining a sound financial system, and their inflation targeting is only one part of that.

Push it till it breaks, then swoop in to save the day.

We are still a mile away from statistics showing our financial system is in trouble. Unemployment low, GDP flat. Growth per capita is bad but they have never cared about that.

That's because we don't have up to date statistics....when the rich start selling of their trinkets you know it's getting bad..

Wealthy’ Kiwis selling off their treasures to stay afloat, says agent

Cost of living crisis is squeezing the top end of town.

The great news is, like inflation targeting, the decisions made are ultimately arbitrary.

The rate at which things will go sideways will only increase without intervention, so when things start looking more dire, chances are the RBNZ will be stepping in, in spite of what inflation is doing on the day.

"this is a country that added 40% to its house prices during a pandemic"

Indeed. And that, of course, is fabulous; economy rescuing and all of that.(sarc/off). Because property price increase aren't Bad ol' Inflation are they, oh no, they are Good, Capital Gains - two totally different things. Until we realise, or perhaps accept is the correct word, that Inflation is the creation of excess Debt (money) over the productive capacity of the country that in turn generates price rises (more Debt chasing the same amount of goods etc), then we are going nowhere but backwards. And one day, that is going to catch up to us; all of us, in a big, big way.

What could possibly go wrong.... that day you mention is hear now.

Nailed it BW 👌

Impossible! (No green tick showing = no value add)

Exactly. Less money on debt repayments means more spent in the productive economy directly, or indirectly via investment from higher savings.

House Ponzi is terrible for the economy but good for a few vested interests. Let it burn .

Speaking of going backwards, we have lost 100K+ skilled locals to greener pastures and gained 200K+ mostly lower skilled migrants.

Add aging boomers to the mix and we now have a lot less productive capacity per capita than we did during previous cycles, so will need boatloads of more debt than ever before to kick the can down the road.

But its so much cheaper to clean power pylon nuts now....

Oh and don't expect the old boomers with the equity to risk it on productive lending at the end of their lives....

we are so stuffed, Nact blew 2.9bil on reversing interest deductability, yet we need ferries and planes , before we even talk about more generation, power network, decent roads. oh and health where we have empty new buildings without staff.

I seriously think the interest deductability should have been left as it was.

Same with the PAYE tax cuts. Yay we get at most $20 a week, but every year that’s $3 billion the government could have spent on infrastructure. There isn’t much room for day to day spending cuts - National may have cut some public service, but they have also increased spending on pharmac, prisons, etc. So the tax cuts will be paid for by less infrastructure spending.

Speaking of going backwards, we have lost 100K+ skilled locals to greener pastures and gained 200K+ mostly lower skilled migrants.

Do you actually know the makeup of skills of the incoming and outgoing? Plenty of people leaving are those that can't make a go of it here, thinking geography will resolve their lower market value as a labour resource.

The tippy top performers/most skilled have had enough success to be happy enough to stay.

Medical Specialists, Drs and Civil engineers are leaving...... our infrastructure projects are too stop / start, there is no defined roadmap.

NAct has finished the easy 100 day rollback and now looks a little bereft of ideas.

So you reckon successful Drs with a 5 million dollar house, a beach house and a launch are leaving in droves?

Yeah I tend to agree, there is a level of salary where more money is less important than location. However if that more money is also somewhere with better weather, infrastructure, etc that’s different.

Does the wealthy Dr care about good public transport?

No, but they do care about stone chips, cement splash and pot holes damaging their Ferrari. My niece was considering travelling to Australia with the family for orthodontic care as the Auckland waiting list isn’t dealing in months, but years. Luckily a Hamilton surgeon has availability. Doctors and nurses are leaving in droves and I can’t blame them.

We need more medical specialists and surgeons around the country, period.

So you reckon successful Drs with a 5 million dollar house, a beach house and a launch are leaving in droves?

The guys already at the very top of the pile certainly have little incentive to leave (unless they are looking to pursue career advancement and professional development at more prestigious institutions). It's the next level or two down which is exiting, the new consultants but not the heads of department. And why not if you can earn say 50% more in Australia, be in a properly staffed organisation where your shifts aren't always moved around to fill in gaps, and you get the latest equipment to work with.

What actually happens is a bit like this ...

- a few young doctors leave

- that creates a shortage

- all doctors end up working longer hours

- more young doctors leave

- the older (and wealthier) get exhausted trying to keep up

- the older (and wealthier) get pissed off and retire

- Now the problem is huge ... and there's no way out.

A lot of younger doctors (and nurses) also figured out that they could earn more in NZ by going with temp agencies and filling in the gaps that their exit from the permanent contract system helped cause. Capitalism at work.

Add in overworked doctors since 2020 causing burnout for some, added health anxiety from this period onwards as well as many worry more than they should about smaller things, and I'd be interested to see if we are seeing a trending uptick in more serious conditions due to lack of treatment (3-4 weeks to get into some GP's for a 15min consult so some simply forego this). There's never been a better time than now to eat well, get or keep fit and healthy to your best ability.

Pa1nter: "So you reckon successful Drs with a 5 million dollar house, a beach house and a launch are leaving in droves?"

Do you know any young doctors who have that level of assets?

Jnr Drs in most places are paid pretty poorly. So seems unlikely.

Is a Jnr Dr skilled (which is the subject of contention), or qualified?

Yes agree, a lot will be lower skilled NZers leaving. And a lot of migrants are skilled. On balance it is probably close to equal.

The top performers will have left too, because they always do, even in good times. Nobody is going to stick around in NZ when they can earn $500K+ overseas in Singapore, UK or US. This is part of NZ's problem, everything is run by people left here because they're too useless to be able to get a good job overseas.

A friend of mine in Australia just got a $75k pay rise moving jobs, and is now on $250k a year. They're a fleet manager. Try getting that in NZ.

And if you have the right experience they don't even require that you have a university degree.

Swings and roundabouts though. A friend of mine from the UK who lives in NZ, said they prefer it here as they are a bigger fish in a smaller pond, in the sense that there are still niche markets here to be accessed in comparison to the UK, and less competition for jobs, lending to being more capable of changing to a better role without needing to have 99% of the skills needed for it.

Do you actually know the makeup of skills of the incoming and outgoing?

No, but if no one else does either (in terms of those arriving) then that alone is reason to stop until such time as we do have a way of measuring instead of running with the 'there is no evidence so it must be fine' approach. One immigrant uber or bus driver is evidence we have the policy wrong in my view. We have hundreds of thousands not working that could be trained for these roles. And yes, those roles should earn enough to live where they are performed without cramming 20+ to a 3br house.

Plenty of people leaving are those that can't make a go of it here

No, like the immigrants here they see a better or just different life somewhere else. None of my family were having trouble making a go of it here, they just could to better over there when all things like house costs were considered.

The tippy top performers/most skilled have had enough success to be happy enough to stay.

Agree, but they also have the choice of where to live and often chose not stay in NZ despite family ties for a reason. Fair enough, they are also likely intelligent enough to see where NZ is heading with cut the OCR (this 'article') and grow the population as Plan A, B and C.

Those hundreds of thousands didn’t want the roles. They had plenty of time to apply before the government finally caved in and changed immigration settings.

The country they are moving to has the same plan A, B and C.

Those hundreds of thousands didn’t want the roles.

...at the total renumeration on offer JJ.

Make the wages high enough and they will. I have P and class 4 and will happily drive a bus if the pay was better. We do it for immigrant for bus drivers...two years' service here and permanent residence (valued at hundreds of thousands of dollars) is given as a bonus. The local gets no bonus for their two years' service. Therefore, the overall renumeration is not comparable in the slightest. I also note a news story recently saying they had enough drivers now...no prizes for guessing there was a link between a shortage and residence being offered for bus drivers. So, while your statement is factually correct (most didn't want them or have the relevant licences), the why is critical.

they could just reduce gst,

job done

its not targeted, though I support removing from food and rates., GST on rates is a rort.

Simpler to refund it to the councils than remove it. Same with food, we all have to eat it, probably simpler to give a small monthly UBI or similar.

You can’t cut gst.

How is Winnie going to be able to afford that giant bronze statue of himself like Kim Jong Un’s

money well spent

Worth remembering that it was actually Jacinda who got the big title

Well if we are talking about who likes titles the most, John had to change the law to get his - https://www.stuff.co.nz/national/politics/93326903/former-pm-john-key-t…

So inflation is going to go down below 3% with 10%+ Council rates increases, 30% insurance premium increases, an extra $35 a month for power (plus the continued price increases from the low user plans being removed) all incoming. Good luck with that.

I guess we will find out on the 11th. I’m prepared to admit if I’m wrong

Let’s say it does go below 3% even with everything you’ve listed…does that mean the rest of the economy is getting absolutely smashed to balance it out?

All things that the OCR doesn’t affect.

Wrong

Inflation in NZ is largely cost push international influence nothing the reserved bank can do as has been proven the past two years inflation still high despite ridiculous high interest rates

Cancel the RB it’s unelected ideologue bureaucrats let them lead way by sacking them they want unemployment higher start with them

The cost of a burger at a pub has gone up about 50% over the last 5 years (by my anecdotal observation). How much of that is international influence? Maybe the grain in the bun has increased by 10 cents or something.

Basic home grown food inflation is still largely impacted by overseas conditions it’s all interconnected if sellers can get more for their produce offshore then up goes the domestic price

The fact in 2024 NZ is still clinging on to the silly reserved bank setting economic policy is foolhardy

If high demand and excessive money supply don’t cause inflation, what happened to Turkey? They have different overseas conditions?

Except we constantly see food prices overseas that are LOWER than in New Zealand, which blows that out of the water.

Costs have gone up, minimum wage a lot.

Don’t underestimate the increase of sick days from 5 to 10 and an extra PH to boot. Not all staff take their 10 per year but when you get a bad run of staff exploiting the system and taking their 10 days every year, as a business you build that worst case scenario into the hourly rate.

Matariki didn't help either.

Also they rollover. So long timers can end up with 50 days or so. And then can start to take them as of right. Lots of doctors now just write a letter saying: can't attend work for 1 week without much reason why. Also these can be issued after an online appointment, so little effort invested to get them.

I hear ya. Staff know exactly what to say to get extended time off. The doctors with no skin in the game won’t be held liable for a work place injury because of the “illness” the patient presents so will write a one week sick leave med cert.

I won’t be employing any more staff for this reason alone. Only keep the tried and tested. Smaller tax grab for the government. This be kind BS is backfiring big time.

has been proven the past two years inflation still high despite ridiculous high interest rates

The OCR is not considered high, however the level of debt is far too high which makes it feel like the interest rates are high in terms of money having to be paid in interest on the likes off residential mortgages.

Inflation will roil in NZ for many years still. We are a thin, weakling, buffeted by every international geopolitical and economic breeze and storm alike, with little safeguards or natural shield.

The Western world is moving out of China bigtime currently. The USA in particular, know their enemy should not be making their toasters, phones, war drones or heavy steel plate used within the US War Tanks.

The expensive re-Factory-isation of the West (especially in the USA) will be inflationary for many years.

- It will settle somewhat, once this massive NEW pull and use of resources, labour and capital is spent and bedded in.

This will boost the prices of highly transformed manufactures / finished goods, that NZ is now almost fully dependent upon (that is, if we want a first world life and economy)

We will continue the low value/high freight cost business of food export, that can be done much cheaper in the emerging producer nations within South America or Africa.

This will leave our biggest buyer China, much poorer, more geopolitically polarized (will we be a friend or foe??) and no longer able to be our economic ("pull us out of the ditch bro") Saviour.

NZ - Warning, Warning, Warning!

So high inflation with low to negative growth is the current path for NZ.

Get ready to thrive with High Inflation and High Interest rates NZ. We lived with it before and we will again!

The simple and obvious outcome is plainly in sight and playing out right now.....ANY DDDEBT funded asset price, is and will continue resetting much lower to compensate for much higher and sustained interest rates.

The RBNZ and the government would do well to identify who is pushing inflation up.

(Hint: the who is likely a combination of monopolistic / oligopolistic price setters and a group of lazy price takers that drag the rest of us with them in rolling over in the face of higher prices driven by the need for an ever higher level of profit. )

Once they identify the who - policy action can be taken. (But not by this government. This would be attacking their voter base.)

RBNZ don’t care. They have one tool to rely on.

Adrian Orr is like the woman at the side of a street fight shreiking “Stop, STOP, STHAAAP!” RBNZ can’t think critically, much like the aforementioned woman.

Rate cuts are not the right solution, we need to improve per capita productivity improvements.

This is a tough ask in a country that mainly exports primary product with no value add, because it can be added cheaper offshore due to lower costs. Logs, Milk powder, kiwi fruit etc. Tourism and education... hard to add productivity.

Bit hard to add value to logs when about 70 percent of forests are under some form of overseas ownership.

Can't see Europeans buying NZ fancy cheese. Mostly sold in the cooking section.

Like wine exports now. Overseas owners of wineries are now shipping wine in their tanks to export markets, then bottling it over there, because its cheaper. Next thing they'll just be shipping the grape juice.

Probably too much effort considering they'd need added chemicals and/or refrigeration containers to manage that. But indeed many are shipping containers lined with giant bladders overseas. Apparently they can't suck the last 150L out of the bladders either, every industry has it's perks I suppose ;P

Indevin, that purchased Villa Maria in recent years, is doing this. They ship in bulk mainly to the UK for a handful of large customers to bottle in their own label. They control well over 20% on NZ grapes now, and climbing.

Yes we definitely do. But government after government isn't interested in doing anything material about it. We would have had a Germany-style property market implemented decades ago if they were.

Prices of goods-&-services need to INCREASE substantially in order to support property/house prices.

Have the Canadian's replaced the ink in New Zealand's money printer yet?.. ..time to go brrrrrrr!

PS: It's not my goal to increase property/house prices - don't complain to me!

The key to a better/less bad economy is lower interest rates. It's that simple!

You're not alone in confusing the economy with house prices.

If we had no debt, would low interest rates still be the key to a better economy then?

You Murray, like so many, don't seem to make the difference between the economy and house prices, I certainly do, and I repeatedly pull up people who talk about housing, when the topic is the economy. I hope you find the answer to your own question. (hint, debt is not only for housing).

Yet, with our limited economy, housing kind of *is* our economy, don’t you think?

Especially when, as others have said, many SMEs rely on their house as collateral.

My apologies, both my sentences seem to have flown off - narrowly missing the top of your head!

Lets say that cpi goes down to the target of 2% annual. Doesn't that just mean that the current settings are correct. And only if it gets near or below the 1% lower bound that they should really start tempering ocr? Or am I just misunderstanding the general principles?

It won’t magically stop at 2% with the current settings - it is like a spiral downwards and requires significant cuts to get us out of the tail spin.

inflation is going to be very hard to pull back in an environment of deglobalization, war on fossil fuels and high fiscal spending.

The reality of inflation taming is falls in asset prices. Whilst many homeowners can Ostrich their way to their next available liquidity event at some point in the far distance, listed NZ (and global) REITs not so much. The main REIT players on the NZX have lost between 30 and 50% of their values in recent times. It's an inconvenient truth to have to be marked to market on a daily basis. Realtors can claim the bottom is in to save their faces for Residential clients, but where cold hard investor cash meets transparent market rubber the slide has only accelerated this year. This is a global effect, so you can't just blame NZs govmt or the RBNZ. Still calling for a 50% drop minimum ttb for residential once wiley coyote notices the commercial ledge has already given way..

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.