ANZ economists estimate it would take 37 years of low house price growth for the house price to income multiple to fall to 2019 levels.

They say it would take annual house price growth of 3% and income growth of 4% over 37 years for the median house price to be 8.3 times larger than the median disposable household income.

Currently, house prices are 10.5 times larger than disposable household incomes. 8.3 was the already elevated multiple in June 2019.

ANZ’s senior strategist David Croy, chief economist Sharon Zollner, and senior economist Miles Workman said: “It’s still early days of course, but the experience to date suggests policy changes [IE reintroduction of loan-to-value ratio restrictions, removal of interest deductibility, extension of the bright-line test] so far are not on their own going to bring about different, and more equitable, housing outcomes.

“House price inflation is still running at an elevated monthly pace...

“Properties available for sale remain very low, and the only real solution to this madness in the longer run is to build more houses…

“However, we just don’t think it’s feasible for growth in house prices to significantly outpace income growth for much longer, as at the end of the day someone has to pay the rent or service the mortgage sitting behind such exorbitant house prices.

“Further, while the picture might change, on current forecasts, the multi-decade tailwind of low interest rates is probably finding a bottom.”

More debt = more sensitivity to rate hikes

Croy, Zollner and Workman expanded on the view Zollner shared with interest.co.nz in early-July; that all the mortgage debt racked up will see Official Cash Rate (OCR) hikes have a particularly large cooling effect on the economy.

They estimated all New Zealand’s debt, including central government, local government, housing and personal, business and agricultural, and corporate debt was $692 billion as at April. This was more than twice the value of New Zealand’s entire economy/GDP.

They estimated $99 billion of that debt had been accumulated since the end of 2019.

It’s worth noting the Reserve Bank (RBNZ) owns most of the new government debt issued, and business and agricultural debt is the only category that didn’t increase.

“In per capita terms, total debt by this measure rose from $118,000 per person at the end of 2019 to $135,500 in April,” Croy, Zollner and Workman said.

However, average annual household incomes only rose by $3,000 over this time.

“No matter how you cut it, the more debt there is in the economy, the more sensitive the economy is to rising interest rates, with more pressure on indebted households, businesses and the government to either cut back on spending or increase prices or taxes, and that will have knock-on impacts on the wider economy,” Croy, Zollner and Workman said.

Debt growth not matched by productivity growth

ANZ economists accordingly “only” see the OCR peaking at 1.75%. It’s currently at 0.25% and is expected to be hiked for the first time in seven years on August 18.

“It’s worth thinking about the bigger picture - which is one of an economy that has taken on another $100 billion of additional debt since the end of 2019 (an increase of around 17%), yet the number of filled jobs only rose 1%,” Croy, Zollner and Workman said.

“Had they also been up by a similar amount, and there were perhaps 17% more cows on farms being milked, or 17% more orchards producing fruit, or perhaps 17% more manufacturing output, that extra debt might not be a problem.

“But the productive capacity of the economy hasn’t grown by anything like that amount. That doesn’t mean interest rates can’t rise - it just limits how far they can rise without becoming a serious drag on economic activity in New Zealand.”

124 Comments

New Zealand needs to change house and rent price expectations. There should be an expectation that prices will be constrained by the marginal cost to build more floor space. That every effort will be undertaken to contain land prices and reduce construction costs (RMA reform, local government funding reform, infrastructure financing reform, market study of building material sector, assistance for the transition from steel/concrete to engineered wood...). Then NZ should be pumping out houses at this affordable marginal cost at a rate of 8 to 10 new builds per 1000 people. This is the rate of building NZ achieved for decades post WW2 to counter the under build from the Great Depression and WW2. New Zealand is just about reaching that build rate - Auckland, Canterbury and the Waikato are doing well. Other parts of the country need to catch up - especially Wellington.

Finally, the divisive 'have and have-nots' economy of the last 40 years has ruined the home owning chances of a generation. There are now huge numbers of life-time renters. New Zealand needs to massively increase the social housing build rate for this group. IMO community housing providers or state housing should be able to provide decent long term rentals to a much wider range of low income households. In the past I have suggested NZ adopt the Austrian social housing framework to achieve this, but perhaps a big increase in state house stock would be fine if there was political consensus not to sell them (which I doubt).

In the decade to 1947 NZ was building social housing at a rate of 1.55 per thousand, and the decade to 1957 at a rate 1.73. In todays terms that would be an annual build rate of 7,750 to 8650 state or community housing provider new builds. Kainga Ora is building at about a third of this rate and the community housing sector is being ignored as a building option.

Tax changes (other than land value taxes which should be the basis all urban councils rating systems) and monetary reform in the long term are just periphery factors. They will not fundamentally change expectations.

There is a big write up here on these matters here.

https://medium.com/land-buildings-identity-and-values/new-zealands-rack…

Another description of the NZ economy is over the last 40-years it became a Kia Ora Club economy. That a minority of privileged and self-entitled people made huge gains not from hard work or enterprise but from regulation that prevented competition in supermarkets, service stations, electricity, house building... while the wider population worked harder and harder but made no gains...

Good description. Sad isn't it.

Unfortunately all the massive damage has been done.

Actually, we increased our population, increasingly.

Doesn't matter who is rich/poor if you do that. And the only antidote is to restrict population - which Nature will do for us if we don't.

So their: "and the only real solution to this madness in the longer run is to build more houses…" is a total madness. Then what? And then what? And then what? We already did that, it's why we're in the pickle, now.

This is where wide-scoped journalism would take in the whole picture - but we never get that (see the Chaston comments, other thread!). We will never ' get back' to median multiples of the past, because we are chewing into the two things needed to underwrite future wealth; energy and resources. They are dwindling (both in quality remaining, and quantity ditto), Productivity is the difference between inputs and outputs, a physics issue (not a labour one any more, labour being less than 1% of ' work done'). They are running into 'diminishing returns' via Thermodynamic limits, totally predictable if one interviewed a physicist, totally bewildering if one sticks to mantra-trained (via Samuelson) economists.

Thus the debt will never be repaid - absent rampant resource/energy price inflation, which I suspect would lead to stagflation, deflation, or just plain collapse. After all, money requires faith and belief - as do 'prices'. Best we instigate a one-child policy and a sinking lid on immigration - would do more to the margin.

Wouldn't it be great if you could go door knocking in the wealthier suburbs and find out interesting stories about how people made their money, the interesting inventions, innovations and enterprises that people came up with. While there would be some, I'd expect a large number would be "Oh I just kept leveraging the into more properties overtime". Pretty boring really.

For over 100 years between 65 and 75 percent of homes are owner occupied... so dont talk shite and moaning

what 100 years was that? who's talking shite?

https://www.stats.govt.nz/news/homeownership-rate-lowest-in-almost-70-y…

We need to accept the fact that there is no housing shortage in New Zealand.

https://www.nzherald.co.nz/nz/ghost-houses-increasing-why-are-40000-hom…

We need to invest ourselves in more productive business (Technology and invention) instead of selling houses to each other.

Yes there is a shortage of houses for people to buy for the purpose of price speculation.

Absolutely @bloodymigrant. But this is too hard for the majority. I’ve been listening to Cathie Wood of CEO of Ark invest recently. Can’t help but think we are going to be left seriously behind over the next 10 years. I’m also looking at the technology channels on YouTube showing how builders around the world are using innovation to build houses more cheaply and using passive building techniques. Incredible what is being done. As usual NZ is still banging nails in wood, stuffing a bit of insulation in the walls and putting in cheap aluminium windows that suck out the heat. But we throw in one or two heat pumps, aren’t we great! Problem is with these building methods WILL NOT meet future building standards. New Zealand is so far behind it’s a joke. But many believe we are doing just great.

need a tax on empty houses, charged through the electricity company to the rates payer, if no minimum static electricity usage recorded.

$1000 per month should do it

Why not charge politicians and their developer bosses, who created this mess in the first place? Might focus our esteemed leadership on making responsible decisions, rather than just taking instructions from self interested lobbyists?

So will just leaving a few lights on lights on and both the towel rails and a small electric oil heater on low. Nobody is going to pay a $1000 a month on an empty home mate, get real.

Or have your house running on solar

Start taxing empty houses heavily as if they were rented out, based on a higher than average rent due to them taking up houses stock that is not being used, which costs the country because then more need to be provided.

Start taxing empty houses heavily as if they were rented out, based on a higher than average rent due to them taking up houses stock that is not being used, which costs the country because then more need to be provided.

Property deliberately left empty is often due to unfair flawed legislation that empowers the renters against the owners and owners understand this so prefer to remove the risk of renting and await capital value increase. Once capital value increases cease or become negative the market will determine prices and move them closer to actual value.

DP

“Properties available for sale remain very low, and the only real solution to this madness in the longer run is to build more houses…"

That's where the impasse occurs.

It's absolutely possible for house prices to outperform income growth over extended periods of time especially if the rising prices are also part of that income.

Per capital public debt means little to the individual or households as it doesn't actually work the same way as household or individual debt. If it does, USA would had been a nation of bankrupts by now.

I'm not surprise that all the debt growth doesn't matched productivity growth if you understand the country's business culture. Big businesses in NZ have the wrong connotation that investing through debt will boost productivity when it should be the other way round. On the other side, businesses that should be expanding aren't taking on or being facilitated debt to expand. A higher salary will not boost the productivity of an unproductive worker- instead it rewards non-productivity. A business that can't get a loan is unlikely to expand its business much less to say hiring more people.

Raising the OCR prematurely and harshly will trigger an immediate loss of confidence in businesses, create an atmosphere of uncertainty and that is the last thing the economy needs coming out of a pandemic.

We should focus on building more affordable houses, increase productivity and business competitiveness though R&D and re-skilling workers for the future.

The socially conscious banks had already raise their mortgage rates, there's no need to pressure RBNZ into putting businesses at further risks and hitting at the heart of business confidence.

The next step for banks is to facilitate loans to small businesses in meaningful quantities (instead of curtailment) to become more complete in being socially responsible.

Build more houses .......how about some population planning?

They need to breed those Labour voters

The next thing Labour will be doing is opening the doors to the pacific, just to to be nice, because we don't have enough low skilled people in NZ to feed and house already.

Yep Philthy ......also I did find it interesting that a farmer was complaining he was working 16 hours a day and couldn't get staff...and then we find out he's an operations manager trying to run four farms.

I guess in the past each farm had a farmer...now each farm has a syndicate owner and no farmer....what could go wrong?

But there is population planning. The plan is to cram as many people into NZ as quickly as possible. It may be yeasty planning, with zero basis in physical reality, but it is a plan.

News flash the USA is bankrupt, they just keep on moving their debt ceiling up and up so the whole country doesn't fall over.

No news anymore, they just call it some different name, and we all accept it. Funny that the big companies want to go into space, is there a taxman too??

Everyone focuses on their $30T national debt, but Medicare and Medicade debt is $170 TRILLION!!!!

The Entire Fiat system is absolutely screwed.

Listen to any interview with Greg Foss, a Canadian Bond trader, he breaks down just how bad it is really well.

Actuarial Obligations Owning to future Generations is not the same as current Debt. There is no interest currently accruing on that $170 Trillion.

They estimated all New Zealand’s debt, including central government, local government, housing and personal, business and agricultural, and corporate debt was $692 billion as at April. This was MORE THAN TWICE (200%) than twice the value of New Zealand’s entire economy/GDP.

Debt as a percentage of GDP is particularly useful in comparing debt levels over time and among countries of different sizes. The United States' debt-to-GDP ratio at the close of March 2020 was Less than (100%) at only 82%. That figure is up from 79 percent at the end of 2019, and is the highest since 1948.

I think NZ has bigger Debt Problems. US Productivity significantly higher.

https://www.google.com/search?client=firefox-b-d&q=What+is+the+US+debt+…

In August 2020, Zollner and Croy , who at the time saw an OCR of negative 0.25 percent by April 2021, tracking to negative 0.75 percent wrote " we’d note that it is a good

idea to combine a negative OCR with policies that will protect the banking

sector from the worst of the impacts on their profitability, thereby protecting

the free flow of credit." ANZ share price currently trades above levels pre covid .

“Despite the very real challenges being experienced by many of our customers, we have the financial strength to continue to support our customers, while also returning surplus capital to shareholders." - Paul O’Sullivan, ANZ chair.

ANZ buyback presents optimistic bank dividend outlookz

Great support for their customers through mortgage rate hikes and pressuring the central bank to raise OCR.

Ain't no policy making boomer care about 37 years, that's the future generations problem.

I really wish I could give you more thumbs up!

The sad reality is that fixing the problem is somebody else's problem, the older you get!

And no policy maker of publicly elected official ever will. You dont get votes by making the hard decisions, you get them through hugs and wishy washy bribery <3 Kia Kaha, Team of 5 Million "Smiling Zombies"

ANZ economists estimate it would take 37 years and low house price growth for the house price to income multiple to return to 2019 levels; They expect small rate hikes to go a long way towards cooling the economy

JENEE your headline sums it up - How bad the housing situation is and from worse it is reaching point of no return - WHY .... Only because Mr Orr inaction and going with policy of Wait n Watch and Robertson for allowing as it suits them.

Now both Orr and Robertsons will have no choice but to support and promote the ponzi at all cost despite dire social consequences / unrest.

Roy - Central Bankers & politicians think they can move levers (like a signalman) and the train (people) will change direction but they don't and won't unless it suits them. The recent small interest rate rise could be a test of reaction which is sensible, but the effects will take time to eventuate and economic activity and job security are key issues so should another rise occur close to an economic shock peoples reaction may be more violent with unforeseen consequences, I was surprised that NZ was a global leader in increasing interest rates.

Roy - Central Bankers & politicians think they can move levers (like a signalman) and the train (people) will change direction but they don't and won't unless it suits them. The recent small interest rate rise could be a test of reaction which is sensible, but the effects will take time to eventuate and economic activity and job security are key issues so should another rise occur close to an economic shock peoples reaction may be more violent with unforeseen consequences, I was surprised that NZ was a global leader in increasing interest rates.

Are the housing being sold for the many millions, borrowed money? There still seems to be those who can afford a million dollar mortgage - their banks think so calculated on almost 7% interest rates - assumes they will maintain their income for the life of the mortgage. How long until we see sections in the suburbs in Auckland going for one million and build costs being four or five thousand per square? Who can afford a two million dollar mortgage?

It's already four or five thousand per square meter to build.

Lousy tiny sections are 650k+ on the outskirts of Auckland.

Why are the banks not lending on business and agriculture?

Risk. With housing, there is no risk as the government subsidises the cost of debt servicing through welfare payments. It’s a one way gravy train

At least that is the narrative in NZ - you have that conversation with people who live in Spain, Japan, UK, US who have seen housing bubbles pop - they know and will tell you that housing isn't risk free.

Yeah nah.

We're different.

“House price inflation is still running at an elevated monthly pace...

“Properties available for sale remain very low, and the only real solution to this madness in the longer run is to build more houses…

Why not restrain 60% of NZ bank lending which is dedicated to residential property purchases for one third of already wealthy households because the RBNZ offers them a RWA capital reduction incentive to do so?

{kind=link}

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $313.255 million (61.13% of total lending) as of June 2021.

It’s worth noting the Reserve Bank (RBNZ) owns most of the new government debt issued, and business and agricultural debt is the only category that didn’t increase.

A comment from Michael Reddell - ex RBNZ economist.

One of the incidential curiosities of the bond purchase programme is that at times like this you hear a great deal of talk about how it is a wonderful time to borrow and the government can lock in very cheap long-term funding. And yet what do really large scale central bank bond purchase programmes do? They transform the liabilities of the Crown from quite long-dated to increasingly quite short-dated, exposing the Crown (us as taxpayers) to really substantial interest rate risk. Perhaps at the end of all this the Reserve Bank will have $50 billion of government bonds, with a representative range of maturities. On the other side of its balance sheet, it will have a lot of very short-dated (repricing) liabilities – all that settlement cash (see above). Whether the Bank eventually sells the bonds back into the market – which hasn’t happened a lot in other countries – or holds them to maturity, the interest rate risk doesn’t go away. It isn’t obvious what public interest is being served by skewing the Crown’s (net) debt so short term. Perhaps interest rates will never rise again……but that won’t be the view many people will be taking. Link

“RBNZ owns most of the new government debt issued.” Book figures. Peter & Paul scenario. That too is what they found when Enron for example, unravelled.

Treasury and bank economists display no better understanding of how our monetary system operates than the average man in the street when they talk of taxation and borrowing financing the governments spending.

Michael knows his stuff but is he wrong about this? The settlement cash is sat in the commercial banks’ RBNZ settlement accounts. It is completely up to RBNZ how much interest (if any) they pay on deposits in those accounts. The ‘exposure to interest rate rise risk’ is surely therefore a complete red herring when discussing Govt ‘borrowing’. Furthermore, when settlement accounts are so awash with cash, banks will compete to swap that non-interest bearing cash for interest bearing bonds (hence the low yields).

Allocated credit tiers for ESAS account holders will be removed, and all ESAS credit balances will be remunerated at the OCR.

Which confirms my point.

Furthermore, when settlement accounts are so awash with cash, banks will compete to swap that non-interest bearing cash for interest bearing bonds (hence the low yields).

You have confirmed my point.

Central banks had no choice. Policy rates would be zero without this action.

Before the crisis, Congress passed the Financial Services Regulatory Relief Act of 2006 authorizing the Federal Reserve to begin paying interest on reserves held against certain types of deposit liabilities. The legislation was supposed to go into effect beginning October 1, 2011. However, during the financial crisis, the effective date was moved up by three years through the Emergency Economic Stabilization Act of 2008.4 This was important for monetary policy because the Federal Reserve’s various liquidity facilities5 initiated during the financial crisis caused upward pressure on excess reserves and placed downward pressure on the Federal funds rate. To counteract these pressures, on October 6, 2008, the Federal Reserve Board announced that it would begin paying interest on depository institutions’ reserve balances.6 Link

Alice’s Adventures in Equilibrium

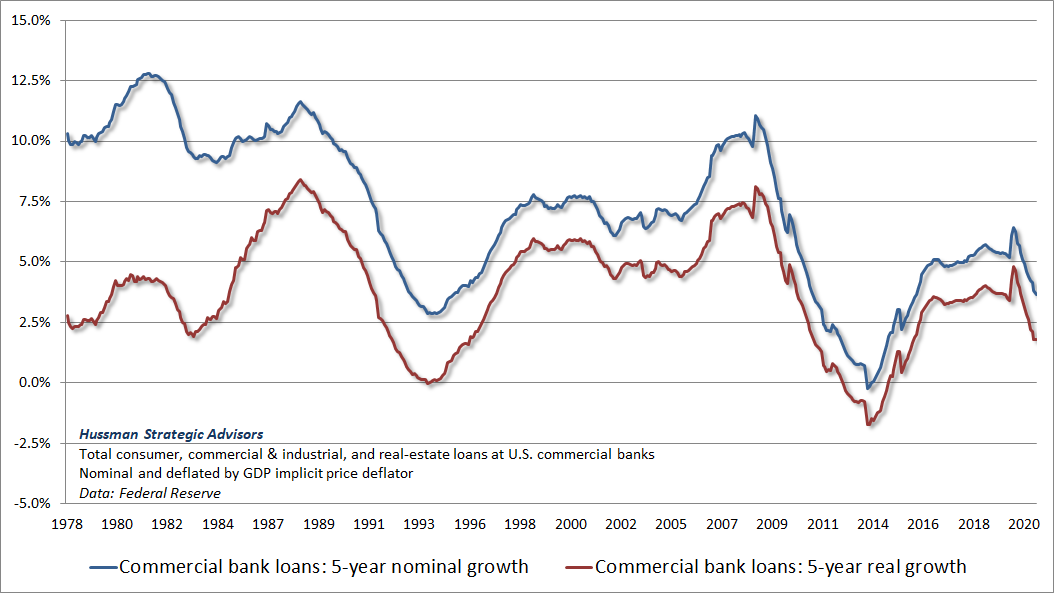

Here’s the thing. Despite over a decade of deranged Federal Reserve policy – I use that word intentionally to mean both “wildly outside of the historical range” and “bat$%!# crazy” – bank loan growth has been utterly unremarkable. So the growth we’ve seen in bank deposits primarily reflects the fact that the Fed has replaced trillions of dollars of Treasury bills with base money. That’s really the crowning accomplishment of QE – creating a massive pool of zero-interest hot potatoes that someone has to hold at every moment in time, and that does virtually nothing but destabilize the financial system with yield-seeking speculation. The chart below shows 5-year commercial bank loan growth.

{kind=link}

"...the only real solution to this madness in the longer run is to build more houses…"

Never going to happen, local councils have property owners backs by keeping land scarce. It's artificial scarcity that supports the current valuations.

Repeat after me: There is no such thing as Land Supply

There is land which is already doing something else - because city-dwellers need supported by sunlit acreage (and mines and dumps) elsewhere. The disconnect is cranial, we forget where food/resources/energy come from (thinking they come from the supermarket and the pump, and that all we need is more money to buy more). The planet is majority-urban now, and no city is 'sustainable' in the real sense of the word.

This nonsense about 'opening up land' and ' land supply' and Councils and the RMA - not only is it factually adrift, it's p-poor journalism and it's NZ-wide. Kim Hill is the only one, so far, to ask "what is the land doing now?" We need a few more doing that......

The way I see it is supplies of almost anything, land included, have economic use or value across multiple groups of people. Farm land is of little monetary value to society as we have plenty of food while housing zoned sections are in short supply so of great economic value to society. Perhaps one day, when birth rates get low enough, we'll bulldoze houses to return the land supply to whatever economic activity is needed at the time.

Here is why I like sections. My grandmother grew up in the first world war in England, when food was scarce, and wouldn't have dreamed of being without a vegetable patch or fowl to feed the family. The settlers in New Zealand where also wise enough to realise that houses needed sections of sufficient size such that people could have gardens and a lemon tree in each for health. Now we are building houses on gardens (under the auspices of "urban densification") because we believe the elimination of the humble vegetable patch represents some measure of progress. I think it a better measure of hubris and our parochialism.

Houses will never be bulldozed for agriculture it doesn’t make “economic” sense. Your comment regarding food is laughable and shows how insulated and disconnected we are to our food chain. Until we realise the planet has a healthy carry capacity/population, we’ll continue to fight over the remaining resources and put our species survival at risk.

New Zealand produces enough food to feed about 40 million people and we could easily increase that if required. We don't have sufficient housing for 5 million people however.

To out this in context, according to StatsNZ, people spend 25% of income on housing but only 17% on food. That figure is actually far more acute for the lower income New Zealanders:

https://www.stats.govt.nz/information-releases/household-living-costs-p…

Yeah, but it's the income off that food exported that pays for the imported materials, to build those houses and infrastructure for the five million. It's like saying, you'll give up your job, so you can build your house.

Which might be perfectly reasonable if you can do it at a lower cost than a builder?

Between Helensville & Orewa and down to Albany that land is there. It's current productive use is mainly "Lifestyle Blocks"-read that as "land banking". It would support perhaps 400,000 residential sections tied into the CBD via Light Rail like they do in New York City and Chicago or London.

30 minutes train ride down the Northern Expressway corridor would do nicely to open up tons of affordable land. Same thing as they did in the 60's to the South of Auckland. And that was more fertile usable crop growing land. Really only an issue of Rezoning, and then a few 10's of Billions of Infrastructure by Central Gov't to allow the lost generations to get on the Property Ladder in Auckland.

“It’s worth thinking about the bigger picture - which is one of an economy that has taken on another $100 billion of additional debt since the end of 2019 (an increase of around 17%), yet the number of filled jobs only rose 1%,” Croy, Zollner and Workman said.

A persistent global problem not helped by limp real GDP growth. Graphic evidence here and here.

{kind=link}

{kind=link}

{kind=link}

China got the jobs, we (anglosphere) got the debt. But not for valued added productive enterprise.

Headline article in The Herald. “Ghost houses increasing. Why are 40,000 lying vacant in Auckland?” Answer: Greed.

Isn't it cute these bank economists predicting things getting better by the time we are retired or dead.

If they looked out the window they would quickly realise things only go from bad to worse in this failing country.

I think that is what they are saying- oh crap, things will take forever to get back to unaffordable from severely unaffordable. Anyway, the finance system is already crumbling. I'm growing veggies.

In their ivory, or more likely glazed and cozy, towers

“However, we just don’t think it’s feasible for growth in house prices to significantly outpace income growth for much longer, as at the end of the day someone has to pay the rent or service the mortgage sitting behind such exorbitant house prices."

Gee , ya think?....and they paid you how much for years to come late to this conclusion?

I'm prepared to cut them some slack on this. It's an idiotic situation choking to a constraint. Doesn't hurt for them to spend a sentence on stating it. The banks are just profit making engines. The policy failure lies elsewhere.

My "hope" is it gets so bad that most of us turn our backs on state-conjured currency.

They’re right, but their own practices belie this. How many mortgages would their bank be issuing if they relied on income solely as the basis for credit, rather than equity in other property?

Hypocrites, right

expectations will count for nought when the nurses follow the lead of the oil companies and let the inflation tiger out of the cage.

I think that a large percentage of nurses are in the process of giving up on nursing. The government will continue the pattern of treating them like dirt so don't expect any meaningful salary rises. Nurses have mostly finally seen the writing on the wall. The hospitals will have largely collapsed before nurses salaries have any effect on inflation.

If you have any of your family that are considering taking up the profession, do every thing within your power to talk them out of it. There are far better professions that are respected and fairly rewarded. Nurses are treated like dirt by the government, the DHBs and many of the patients. As the system collapses the working conditions will only get a hell of a lot worse. A collapsing downward spiral. The shift work plays hell with your health and family life. The sacrifices are simply not worth it as many mature nurses who have devoted their lives to the profession are sadly accepting and leaving to do almost anything else.

We are on the far side of growth, globally. Expect everyone - not just nurses - to traverse this sinking feeling. That's what voted for Trump and Brexit.

if the nurses insist on a percentage increase anywhere near what they are asking,over 10% , and refuse the cash bribe then they will set the benchmark for other govt employees,that in turn will boost the increase in super and other benefits,we are talking billions.

If it was govt employees working shifts, weekends, public holidays then OK.

I don't think that the nurses give a toss about that. In fact the impression that I am getting is that in their hearts and minds many have moved beyond nursing and are more concerned about how to leave the profession in New Zealand. When a large number of them are gone and we cannot run our hospitals what are you going to do? Take away their passports?

I concur with everything you wrote. When people ask me if they should study nursing I do everything in my power to advise against it. Moving to Australia is the only reason I'm still working in this field.

Anyone reading this should be pretty worried about this.

Our social infrastructure is crumbling.

It was always going to.

Read Tainter, Catton, Orlov, Heinberg, Soddy, Diamond, Morgan (Tim); the list goes on.

Just remember that Victoria Uni had a symposium on 'optimum population for NZ' - they held it over 2 weekends in 1972.........

Unreported, unremembered, unreferenced. This is why I sigh; we are useless at keeping sight of the truth, very good at peddling the myth.

On the back of this thread.

My friend who works as a nurse at a large city hospital just messaged me this. M=Me H=Her

M. Hows is the general sentiment at work? do you think most people are leaning towards leaving rather than staying?

H: Yeah definitely people are over it, mostly young ones like me not sticking it out and leaving. The older ones kind of just tough it out, they've worked for years on the Wards so they just keep going

M: they just dont know anything else really ae

H: Where as I think us younger ones recognize we dont have to stick it our and we maybe prioritize our mental health more

M: And we are more willing to pack up and shift if we want to, like going to Auz

H: It's crazy we work 3 nurses down with sick patients and no icu beds and stay late for no pay all the time. And then we get told of my bour management for taking sick days

M: Holy shit, and then you get told by the government that you arnt going to get a pay rise for the next 3 years

H: The hospital had high nursing sick leave a few months ago because of burn out and instead of fixing that they made it compulsory for a doctors note for 1 day sick leave Just so done.

Argh accidently reported.

Do you realize that the government has just given the hospital doctors a 10% pay rise after about a weeks discussion and without batting an eyelid. Imagine how the nurses feel.

House prices were totally un-affordable for a large percentage of the population before covid, so taking a large chunk of your working life to just get back to a situation which was un-affordable makes no sense to them. The only logical option for them is to leave for another country where houses are affordable and salaries far higher.

It is amazing the number technical and skilled people ~35 and under talking about leaving when travel opens up again. Despite all the good press NZ has gotten globally, looking good doesn't feed and house people.

And they absolutely should leave too. The move to Australia is especially easy and the instant rewards are there. It's a no brainer. NZ doesn't deserve to keep them.

I have started to view NZ as a filter system for Australia, people are either born here, or migrate here. Then about 20% are scared off to Australia, any that can't adjust to the Australian way of life, are returned to NZ.

"the only real solution to this madness in the longer run is to build more houses…"

This doesn't solve anything when the cost of building is rising much faster than inflation. The immigration/overseas buyer narrative is demonstrably disproven. This crisis is fuelled by low interest rates and greed. NZ has plenty of residential housing stock, with a non-trivial % sitting empty. How about working on the demand side first? Put interest rates up, implement a capital gains tax and put a cap on using equity to borrow more.

Perhaps the government could also entertain requiring minimum "cash deposits" for investors instead of allowing equity based deposits. This could curb the equity snowball and level the competition with FTHBs.

The house price to income gap is going to increase with current set of policies, now there is no returning back.

The interesting thing here is, Govt have floated an idea/suggestion to not write the property related articles to media, so that the housing market will not be fueled due to FOMO.

But this govt act only if there is media pressure because once they are in power they can do anything, no one can question them other then media.

So clearly the above idea/suggestion to media is the fine way of controlling the perspective.

Whosoever have suggested this idea is brilliant strategist to cover the failure of this govt & also help to double on wait n watch game.

"ANZ economists estimate it would take 37 years and low house price growth"....

I think this headline misses the other half "...and high wage inflation". They are using an assumed 4-5% in wage growth. Right, maybe for the odd period here and there, but it isn't going to average that for 37 years.

Yes. As wages make up a part of the CPI, (but land prices don’t), there’s no way the Reserve Bank would allow this to happen. But it’s unlikely to happen even more so given the fundamentals of a low productivity services sector based economy who’s primary driver over a decade or more has been (mostly imported) population growth.

very interesting if you were to overlay each of these graphs with government of the times .... even allowing for a little lag when a new government came in -- its obvious where the real debt and house price growth lies

What we need is a global pandemic. That would constrain incomes and demand for a while and house prices would fall as a result.

Haha nice one

Well thats what I predicted at the start of the Pandemic, how wrong I was. I can only laugh about it now when I saw prices going in the opposite direction and bought a house a year ago.

As you know, its the perfect excuse/cover story for the central banks to act in an irrational manner without public outcry.

“However, we just don’t think it’s feasible for growth in house prices to significantly outpace income growth for much longer, as at the end of the day someone has to pay the rent or service the mortgage sitting behind such exorbitant house prices"

I've tried this angle of conversation with property investors for years now and all they do is point to the past and say that 'this isn't actually true'. House prices can outgrow wages indefinitely...

Exactly. It was logic that I thought would apply years ago, it just doesn't.

Exactly. It was logic that I thought would apply years ago, it just doesn't.

There is obviously a limit to house prices, however from what is still happening in the market it is clear that we have not yet found the ceiling. Its a fine balance and several factors are involved.

Not quite accurate. There is a limit to the ability to repay debt, without devaluing the proxy to unbelievable levels.

But banks can key-stroke numbers, people can borrow the numbers, lever more numbers, and look at them gloatingly - till the cows come home. The is no ceiling to that process.

Reconciling money, though - it hasn't been price-discovered for at least 11 years, arguably for 30-40.

House prices can outgrow wages indefinitely.....if nobody cares about a return or repayment. Meanwhile back in the real world house prices can outgrow wages until suddenly they can't.....pop!

It is crazy, noticed two houses that were sold last year in November for $770000 asking 1.2 million and another sold for $885000 asking 1.3 million.

50% return in lease than a year but as is not happening next to PM house to wintness, she is .........

Arohahaha.

Absolutely correct there are lot of examples like that and amazingly our beloved PM is unaware of that.

Pathetic show by Labour.

Yep pathetic. And the blue bunch are useless too.

.

She talks(!!) about saving the planet... then you get this "Last year the country's main coal users imported more than they had in 14 years, and this year government officials expect even more to come in. Most of this coal is burned to power our homes and businesses." I wonder how bad 2022 and beyond will get before someone sits up and takes notice

We need large scale hydro schemes to power us, not fanciful wind and solar. The Govt allows the Greens to protest against flooding valleys with water, new generation gets stymied behind decades of process.

https://www.rnz.co.nz/news/national/447679/new-zealand-likely-to-have-r…

I have a 21-year-old finishing a degree and an 18-year-old starting a degree, both see no future in NZ as far as financial security goes and this just confirms it. Sad but true.

You need to give them 100k each towards their first home deposits.

100k probably isn't even enough

Don't worry, they'll get there by degrees

;)

College education is a double edged sword and can easily turn out to be the worst investment in a person's lifetime.

Presuming your kids are on student loans, upon graduating, they have to service a substantial debt and at the same time needing to raise a deposit if they wanted to buy a house.

The misery can be avoided by investing in houses instead of wasting time trying to achieve the old rite of passage.

When they become rich, they have the options of paying college fees in cash or they might see no point in it.

Everywhere in the world is the same.

Most human misery are self-inflicted as a result of personal discretion.

Most - although certainly not all - of the time people will be far better off with a tertiary education, on average.

Sure people who get into trades can do well, but many people don't have the skill or aptitude to do trades. Just as many people who do trades don't have the skill or aptitude to do a university education.

Being interest free also makes a big difference to student loan debt.

These endless scare stories about the impact of increased interest rates are getting silly. For a start, interest rates will hardly move if they move at all. All the market interest rate indicators (e.g. 10-year bond yield) suggest that there will be next to zero movement. Secondly, government ‘debt’ is completely irrelevant here - a rise in interest rates will make no difference at all to government or to government spending. Household debt is much more important, but household debt servicing costs have never been lower - with servicing costs of around 5% of disposable income. It would take an increase in interest rates of 200 - 300 points just to get us back to 'normal' levels. There will of course be a cohort of people who will be exposed if rates rise - but the question is 'who are these people, how big will the problem be, and what can we do about it'? https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-household-debt

For example, if rates increase and it leaves FHBs over-extended, then Govt should just buy the land under their house (i.e. pay a chunk of the mortgage off) and then rent it back to the poor souls on a peppercorn rent until they are in a position to re-purchase the land at cost (potentially at point of sale).

Totally agree, it's scaremongering, some of it intentional, some of it not.

But why should taxpayers have to bail out FHBs? Bank stress testing should prevent people borrowing more than they can afford when interest rates rise.

Govt buying land creates an asset on the govt balance sheet that at least equals to cash spent. Makes literally zero difference to taxpayers.

maybe the latest political poll will scare them into doing something,looks like there are plenty of potential voters who feel they are asleep at the wheel.they wouldnt want collins to get replaced either as her suck-a-lemon style was never going to be popular.

Banks have a vested interest. Yet they keep coming up with this or forecasts.

House prices simply increase because of supply and demand. Period.

The problem is that banks keep taking income to debt ratios. The reality is, most of the people who own assets, do not have an income and just have a lot of cash from their previous assets, and keep adding more and more.

Raise rates 3% and build a million houses of good quality to rent. That would obliterate debt bubble and solve housing shortage. Gov will not do this as 15% of its vote is National supporters

Excellent article - just proves that it was a big mistake to introduce maximising sustainable employment in the Reserve Bank’s mandate - all that has happened is excessive debt put into unproductive assets resulting in massive house price inflation. If the Reserve Bank had been allowed to focus on keeping interest rates at 2-4% house price inflation would have been much lower.

Good description of the issue at hand. But who do you think in your country is worried?

I see first home buyers extending their buying capacity far beyond they are comfortable with.

They have no idea how those next 30 years will be.

What else did we expect from a ridiculous policy of printing billions of dollars, and ridiculously low interest rates?

The negligent RBNZ needs to start raising interest rates immediately.

I would have liked to see a version of Figure 3 (House Price to Income projections) using an assumption about house prices falling. Would it really be all doom and gloom? I know the US real estate market dynamics are different than NZ, but I survived two house price drops, one of which was significant (40%). The world didn't end. While I understand that everyone expects the value of their house to go up overtime, I doubt that anyone can justify the 20% rise that occurred in 2020.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.