UP...but by how much? That's the key question ahead of the release of the unemployment figures on Wednesday, August 7.

Statistics NZ's suite of labour market data, including the unemployment figures, is the last big piece of the puzzle for the Reserve Bank (RBNZ) ahead of its next Official Cash Rate (OCR) decision on August 14.

I'll have much more on the upcoming OCR review itself with a preview of it in a week or so, but, suffice it to say, the labour market figures will be a significant piece of economic 'evidence' for the central bank to peruse as part of that OCR review.

The RBNZ no longer needs to support 'maximum sustainable employment' as part of its monetary policy, with the National-led coalition having officially removed that requirement. But it doesn't mean the figures aren't important.

While it is loathe to say directly that it has been wanting jobless numbers to rise, the RBNZ has expressed a desire to see 'slack' develop in the labour market because this helps to take heat out of the economy and, by extension, inflation. However, the RBNZ would not want the unemployment rate to rise too fast or far.

Therefore, if there is a very big surprise on the high-side with the unemployment number in the coming week, this could possibly be enough to tip the RBNZ over the edge and result in a cut to the OCR at the August review.

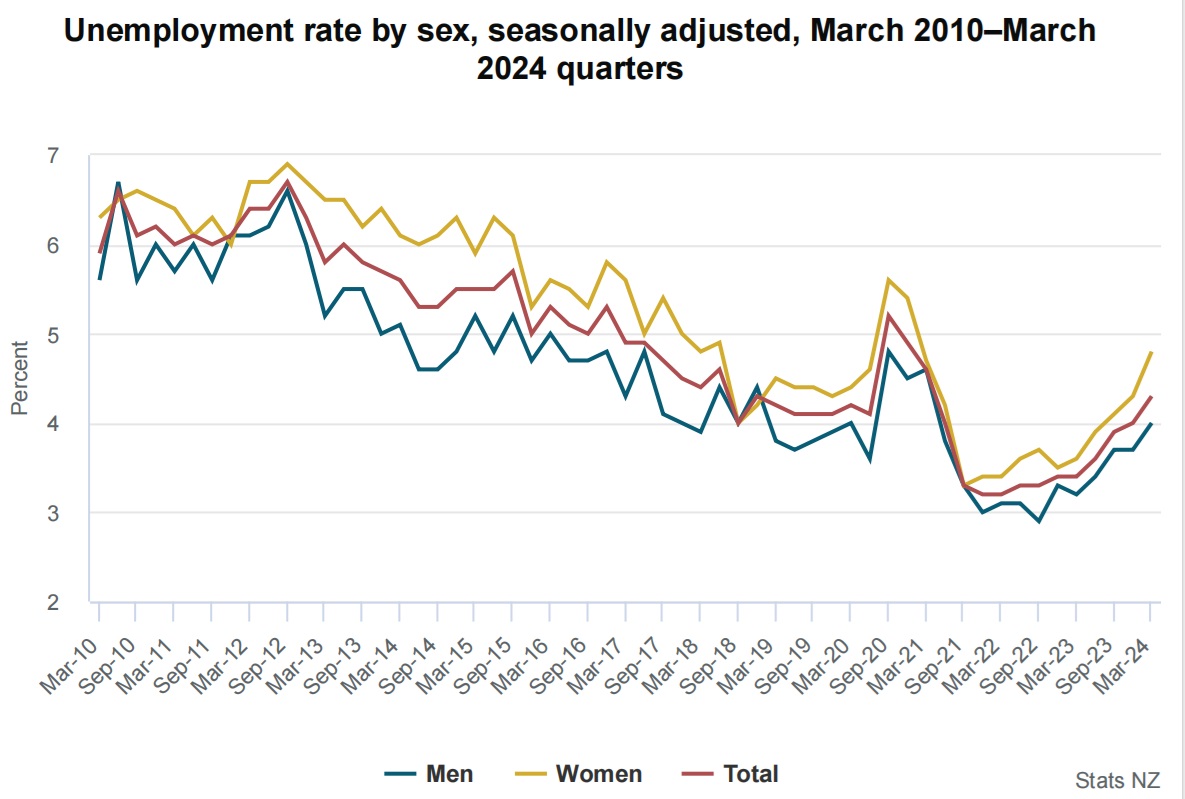

It would have to be quite a big surprise though. In its most recent set of forecasts in the May Monetary Policy Statement (MPS) the RBNZ forecast for the June quarter the unemployment figure would be 4.6%, which would make a fairly sharp rise from the March quarter's 4.3%. It would also give us our highest rate of unemployment in over three years following a period of extremely low unemployment - as low as 3.2%. Therefore the threshold for a 'surprise' for the RBNZ from the forthcoming figures is quite a high one.

I didn't have all economists' previews of the labour market figures in front of me at the time of writing this, but the early indications from certainly the major bank economists is that expectations are settling at around 4.7%.

The RBNZ's picking a peak unemployment rate of 5.1% next year, but the bank economists reckon it's going to go a bit higher than that, with picks of 5.4% to 5.5% being bandied around.

Is there any reason to believe that the figures out in the coming week could surprise?

Well, if the high frequency data we've seen released in and around the June month is any indication, possibly yes. That's because the high frequency data really has been THAT grim.

As I said at the top of this article, it seems beyond doubt that the unemployment figure will be up. The only question is by how much.

The RBNZ has liked to portray itself as 'laser-like' in its focus on inflation and on getting it back into the 1% to 3% target range (annual inflation was 3.3% as of the June quarter down from 4.0% in March). This is why it ramped the OCR all the way up to 5.50% from just 0.25%.

The economy can't be ignored

But 'laser-like' focus or not, the RBNZ can't ultimately ignore the economy at large though - not if there's signs the RBNZ's tight monetary policy might be really starting to tank the economy in a big way. And a very sharp rise in unemployment - more than the RBNZ expects - could start to produce all sorts of unpleasant ripple effects, of which things like a rising wave of mortgagee sales are but one thing that comes to mind.

Let's consider some of that recent 'high frequency' economic data.

In just the past week we've had Stats NZ's Monthly Employment Indicators (MEI) release, which showed that the number of filled jobs in New Zealand fell in June. This was the third consecutive monthly fall - the first time there's been that many consecutive monthly falls since the aftermath of the Global Financial Crisis.

In June also, job ads took their biggest tumble in three years.

Perhaps not surprisingly, at the same time, Kiwis' confidence in getting another job has plummeted.

In terms of broader activity indicators, small businesses reported a big slump in sales in June, both service sector and manufacturing sector indicators are looking dire, and consumers have locked their wallets away.

And there's just time for an honourable mention of the latest ANZ Business Outlook, which is described as having "a bit of a 'well, can’t get any worse' vibe to it", while the earlier NZIER Quarterly Survey of Business Opinion was truly dismal.

The month of June in particular looks to have been an absolute shocker - the moment the economy started really tipping over.

Now the RBNZ's not unaware of all this. In fact the aforementioned NZIER survey might just have been the biggest factor shoving the RBNZ into its big 'dovish pivot' earlier this month, which completely reversed May's surprisingly hawkish statement.

Clearly if the unemployment figure for the June quarter does turn out to be 4.6% or close to it then the RBNZ will regard itself as being on track. But a figure higher than that might suggest that the RBNZ's inflation 'treatment' is starting to make the patient (us and the economy) very unwell.

The swoon in June

As I read the wave of unfavourable high frequency data that's come out in the past month or so, it points to an economy that went into serious swoon mode in and about June. This suggests that job losses will show up - not so much in the June quarter, but in the September quarter we are now in.

Indeed, in their preview of the labour market data, ANZ senior economist Miles Workman and economist Henry Russell (who are picking 4.7% unemployment) say that the June labour market data is expected to provide further evidence that spare economic capacity is building, and that disinflationary progress is set to continue. And they then go on to say:

"The big question on the day will be whether the second quarter data suggests this is happening at a faster pace than the RBNZ expects.

"Forward indicators suggest that could well be the case, but it is perhaps something we won’t see in the 'hard data' until the next read or even the fourth quarter data."

One of the other major points of interest the RBNZ will be focusing on in the forthcoming labour data is the wage figures. Stats NZ has a whole range of ways of measuring wage rises, but I generally keep my eye on the private sector hourly wages. As of the March quarter these hourly wages were showing an annual increase of 4.8%, but down from 6.6% as of the December quarter.

The RBNZ expects the private sector hourly wage increase to have eased further to 3.8% as of the June quarter.

Of course, if the unemployment rate is starting to push up more strongly than expected, this fact could be expected to have a pretty significant impact on wage rises as well, or lack thereof.

It all depends on the figure

So, there's much to watch out for then. If the unemployment rate is around the 4.6% the RBNZ is forecasting, then the central bank will probably be able to shrug off any perceived pressure to go early with OCR cuts, probably sticking with a start time (and this is of course is only an estimate and not based on anything the RBNZ has directly said) of November.

However, if that jobless figure is surprisingly bad then expect a growing chorus calling for a cut as early as August 14.

I leave the last words to Westpac senior economist Michael Gordon, who is picking a 4.7% unemployment figure:

"We think that for the RBNZ to begin cutting rates in August, we’d need to see a significant upside surprise on the unemployment rate next week, perhaps close to 5% (from 4.3% currently). That would be a very large one- quarter increase – outside of the temporary Covid shock, we haven’t had one of that size since the 2008 Global Financial Crisis, and before that the severe recession in 1991."

"Similarly, the RBNZ would need to see evidence that wage inflation is dissipating more quickly than they expected. While wages don’t play a big role in the RBNZ’s modelling, they are nevertheless a major source of the remaining ‘stickiness’ in non-tradables inflation."

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

150 Comments

The change is coming but the consultation process between company’s/government departments and employees takes a long time - often months. I understand many government employees know their jobs are going but are still in the midst of the process. So I suspect the unemployment print won’t reflect what is going on at the coal face but as per usual the RBNZ are working with lagged data. Some more time spent away from the desk talking to unions and Business leaders would seem prudent.

As someone at one of those agencies, I can say we haven't even hit our peak redundancies, and there is already another round planned for this time next year. Some people are calibrating the reduction in government staff, but I can tell you our contract and consultation budget was cut substantially more than our staff. Once the current contacts run out, there will be even more pain in the private sector.

Knowing for months on end that you will probably lose your job is the current dinner party chat in Wellington. Bad vibes man.

RBNZ will hate the next lot of high wage rise/demands, still to be requested/demanded by the Kiwi worker - who has been routinely inflation robbed and fleeced everytime she/he goes shopping.

Staffing cutbacks will lessen the wage hike squeal, yet won't extinguish it.

So mortgage rates......yay, 6.2% by Christmas........?

Whipdeedoo.

The Deep Ponzi Debt Junkies, can then set about to encourage the FHB --cannon fodder, to drain a fresh syringe of the banks monetary poison, to attempt the reanimation of the back paddling, NZ housing market??

It won't reanimate the road carcass - now carrion/flyblown, of the NZ housing market Ponzi.

Sorry spruikers, the Debt syringe is much too expensive even at: 4.5, 5, 6.2%

The massive Debt burdens already extended into our highly priced market, are overtaxing the leaf springs on ole Jed Clampits hillbilly Debt wagon.

"She cannnnoot take any Moore Capitan!! "

This market is so fockeddead, it needs the 3.5% mortgage rates to reliven the cable...till then, it goodnight nurse for housing price gains

Interesting article with quote from the governor of Bank of England

https://www.theguardian.com/business/article/2024/aug/02/dont-be-fooled…

If we follow others.. don't expect a return to the hey days

Interesting indeed.

But it made me ask the following question - is the NZ economy more dependent on cheap debt than the UK economy? Intuitively I would think ‘not really’ / surely the UK economy is very dependent on it too.

If we talk about NZ, I can’t see how we will avoid total economic carnage unless the OCR drops significantly more quickly than this.

Is the UK governor simply jawboning?

The problem for us is if the OCR drops quickly inflation will likely return. The exchange rate will be affected and likely other economic issues will result. The rbnz won't dare risk having to yoyo.

We also have a likelihood of an oil spike from the mid east.

The rbnz has no choice but to strike a balance and likely will have to choose some minor drops with a high floor and hope the government can do something to slow the carnage.

we really outdid ourselves and extended our boom.. and now are experiencing the downturn that should have happened as the pandemic started..

We propped it up with immigration. Cheap credit and free money. We can't repeat any of those solutions anymore. We have to get rel and build a proper economy that exports something useful.

Our big red warning sign is the smart kiwi kids leaving in droves and no foreign smart kids coming... coz house prices are too high, public service are relatively rubbish and the economy has no engine. As they increasingly leave and more and more kiwis want to retire it will become more and more obvious how exposed we are with no option but a hard reset.

Thanks, good comments.

So you think a floor on the OCR of say 3.5%?

A floor yes. But how long it will take to get there is the question.

If it drops too fast they won't be able to control any side effects. I reckon 4.25 by the end of 2025.

We have to reduce house prices/rents and control inflation whilst trying to keep the economy alive and unemployment manageable level.

I dont think anyone is expecting or trying to manufacture a boom.. just a balance to sort out the mess. The question is how long that takes to sink in for the leveraged entities and our zombie businesses that can't survive with expensive credit or reduced consumer spend.

One thing in our favor is that aussie has to start to limit its immigration and will see growth also flatline.. as with us the infrastructure and public services can't keep up. Which should start to stop the exodus for us in 2025+

You could well be right. Sadly, if you are, unemployment will almost certainly get to at least 6-7%

And that is exactly why the OCR will drop by far more than most expect in 2025. Yep my prediction for 2025 is a significant drop of the OCR by over 2% lower.

Sounds like I better start looking at a 2 year TD and to kick that can as far down the road as possible.

A managed investment grade bond portfolio will give you much longer duration and liquidity, if you think rates are falling faster than currently priced in.

I think 3-3.5 may be NZs Neutral, but this is going to get messy and may need to go lower back into stimulate to fix things up, but then a huge amount of damage will have been done. If I had lost a business here, I would move to Aussie to restart.

Puts no value on being networked in a community/market.

I can and have had businesses attrition themselves away, moving into something else has always been way easier by having a decent understanding of how local markets work, and who the people are to deal with.

It'd be a struggle to justify leaving my life behind, spending 10s of thousands relocating, and then taking a few years to re-acquaint myself with a new business environment.

Depends on your area of expertise, a digital native will fare a lot better with a much faster market capture locally and nationally across borders than an industrial dinosaur….

If the argument is restricted to a digital native, then moving from NZ to Australia is a pretty lame option. You'd be better off moving to somewhere with a temperate year round climate with a fraction of the living costs of either NZ or Australia. Take your income arbitrage and use it to fund an asset, or work 1/2 as much and enjoy your free time.

Being a digital native doesn’t restrict you to online only, these skills can be used to generate significant bricks and mortar traffic.

Sure, you could build a Saas and move to Thailand, but if you want a similar life with a larger population, it can be done in Aus at reasonably fast pace if you’re savvy….

UK private debt (domestic credit to private sector) is about 120% of GDP compared to 140% in NZ. So as a rough measure of impact - 5% UK interest rate x 120% UK debt to GDP = monetary restriction of 6% of GDP. NZ is 5.5% x 140% = 7.7%. Term structure of mortgages is pretty similar I think.

Worth noting that Govt debt in UK is 100% of GDP (give or take). So, Govt is paying out a lot more interest to the private sector than NZ. This is crap quality stimulus, but it is stimulus nevertheless.

For those interested, here's how the private debt to GDP ratio has changed since interest rates peaked in the late 1980's.

https://tradingeconomics.com/new-zealand/private-credit-by-deposit-mone…

https://data.worldbank.org/indicator/FS.AST.PRVT.GD.ZS?locations=NZ

Private debt or private credit?

It’s whoopdeedoo, not whipdeedoo.

Going by the numbers direct from the Ministry website here; https://www.msd.govt.nz/documents/about-msd-and-our-work/publications-resources/statistics/weekly-reporting/2024/jul/income-support-weekly-update-26-july-2024.pdf ...the unemployment numbers are tracking up - yes, but they're not soaring right now. Will the RBNZ really have cause to panic and cut the OCR earlier than anticipated at the next review? It's debatable.

An export led recovery aided by a lower dollar is the way forward to a sustainable recovery however, with a lower dollar comes imported inflation. This said, its hard to build a case for mortgage rates dropping a great deal. This traditional recovery is assuming our now weakening trading partners still have the appetite to buy our products for premiums that are profitable...

An export led recovery aided by a lower dollar is the way forward to a sustainable recovery however, with a lower dollar comes imported inflation

Just as a matter of interest, the higher mortgage rates have led to a trade surplus already - our exports are static, but our imports of the likes of vehicles and fuel are way down.

Stop it! You can't use the June month figures alone to call a trade surplus. Look at the data, Also remember that it's the current account deficit that really matters.

How would you like me to describe the practice of exporting more of value than we import in a given time period?

If I have a business, and lost money for months or years, and then due to my costs being lower than my sales, is that instance not posting a profit?

We are seeing first hand that when money is cheap enough, we will spend it on trivial matters of consumption, and when it is more expensive we will walk away from that and keep doing what it takes to keep the lights on.

And somehow we are supposed to believe that if we make money cheap again, this time, fingers crossed we will use it for productive enterprise, rather than empty consumption.

If you have a kiwifruit business and you sell more than you buy in the month of the year that you harvest and export (June), would you celebrate your profitability? Or might you look across the whole year?

Not sure what your point is on the 'making money cheap again', that's not a point I made.

If I sold the same amount in June this year as last year, and reduced my input costs well below my cost of sales, I would consider that achieving a surplus, where I didn't before.

We can keep watching our import figures in the following months, and if the reduction in consumption continues, then we are trending towards having a trade surplus.

You think our imports will jump back up again in the coming months? We'll go back to buying new cars and burning fuel transporting 2023 amounts of goods to ourselves?

They’ve already shit the bed, what you’ve said, & what others have said as ways to achieve a slower long term recovery is probably best…but best would be industrious/hard…& with a cheeky wee lazy/easy option sitting just there…you can almost hear the printers warming up…they’ll kick the can 🖨️🦵🥫🤷🏻♂️

Let’s just hope they stick to their guns with DTIs/LVRs…because the lag effect of the printers probably won’t fix the numbers fast enough they’ll turn to cutting restrictions to enable it to 🤦🏻♂️😂

The way to earn our way out of our hole would be a 5-10+ year slog, involving more work than we're currently doing, while also enduring a lower quality of living.

Logical, but politically untenable.

And for the bigger picture, for our kids/grandkids it’s what we should be discussing…but do they have the stones to do that? I just can’t see it…guess we’ll find out over the next 12 months but I can see an OCR well below neutral and DTI/LVR restrictions being eased.

EDIT: So I guess the discussion is what can we do for our kids/grandkids to prepare them for the pending boom/bust cycles/unaffordable housing?

Job seeker cancel and obtained work is on par with last year.

Not looking distressed.

The government really needs to make it easier on employers to fire non performing staff or engage in genuine redundancy dismissals. It’s an absolute minefield these days employing people. It makes small employers gun shy replacing staff if they’ve ever encountered these no win/no fee lawyer firms that will find the smallest of legal errors and take the employer to the cleaner. This is just going to add more people on job seeker benefits and less of a tax take. This will also be inflationary, I see a big rise in one man bands having a higher margin due to not wanting to bother with staff anymore.

These young guys are targeted on social media advertising by these no win/no fee lawyer firms. The employees know how hard it is to get fired these days which drops productivity and standards. There’s still great young workers out there but I’m finding this attitude is on the rise. Rant over.

Maybe I should just cash in and be a landlord.

I see this in my place of work. Non-performing workers feeling they've got a God given right to an annual performance based wage increase to gloss over their own financial short comings. When the inevitable happens, through anger and frustration, applications are then made for jobs offering higher pay, when really, all they've got on offer is their bank account number. The irony is, these same individuals are getting short listed and they'll likely be a given a good reference in the hope they become someone else's problem! Employers beware of the professional interviewee as these questionable work ethics will only come in tow.

What about non performing managers? Management in New Zealand company's is appalling. I worked for a major NZ teleco and management were only interested in pleasing the higher management. The end result was high staff turnover ( each Monday I suspect management wondered who was going to quit this week). - people who had little understanding of the systems ( poor or no training ) and the implications of the failure of those systems to their customers.

Unfortunately the emperor has no clothes and management know / knew it. Credibility is a major issue and until that is sorted NZ Inc will continue to make the same mistakes with the same results.

(and before you reply have you considered it may true....)

"That would be a very large one- quarter increase – outside of the temporary Covid shock, we haven’t had one of that size since the 2008 Global Financial Crisis, and before that the severe recession in 1991."

Well all other data recently has surpassed these two periods, so why not unemployment.

"While wages don’t play a big role in the RBNZ’s modelling, they are nevertheless a major source of the remaining ‘stickiness’ in non-tradables inflation."

The idea that wage growth is overheating the economy went out the window about 12 months ago.

"so why not unemployment."

Because workers can leave the workforce in ever-increasing numbers. We have an optional exit date from the workforce of 65 years of age, and that is an option that more will go for as each day passes. Will the Participation Rate fall? Undoubtedly. And it will continue to. Not only in NZ, but across the Developed World (with varying exit ages, of course)

"indications from certainly the major bank economists is that expectations are settling at around 4.7%."

So quite a way to go until we even get to neutral.

"An unemployment rate of 5% is often considered full employment. This level of unemployment is enough to minimize inflation and allow workers to move between jobs, but those wanting full-time work should be able to find a full-time job (even if it is not their preferred occupation)."

You realise this is complete nonsense right? Irony?

It's as nonsensical as the Phillips Curve.

Looking at "4.7%" or (pick a number) doesn't really give us the underlying reason why we are where we are. But 'economists' will head to their uniform training to tell us why that isn't so.

"A Recession is when your neighbour loses their job. A Depression is when you lose yours" and all of that.

The data for the last year has been building to this, but the collapse really amped up in March as Govt pulled back budgets (and projects) from Ministries, a decent chunk of people rolled onto new mortgages, and overseas visitor spending pulled back This clearly (and predictably) created a tipping point.

RBNZ are showing us both the potency and impotence of monetary policy. Our massive pile of short fix private debt makes monetary policy very effective at crushing consumer demand and driving up unemployment a year or so after a large hike. However, the impact on prices is pretty marginal given our low competition, cost+margin, 'reselling imports to each other' economy. In fact higher rates are just as likely to have prolonged inflation as subdued it. Our CPI has just tracked down a little behind other advanced economies - many of whom have not sacrificed jobs on the altar of the false god of monetarism.

The unemployment figures will be in the high 4s but they are already out of date. Look at benefit numbers for example - jobseeker numbers have taken off, already well ahead of the forecasts that Treasury made for the budget in May. Macroeconomics is all about the rate of change and momentum. Our recession has become an oil tanker stuck on full throttle and RBNZ is an underpowered tug boat that would need the whole of the Pacific to turn it round.

So, the focus now shifts to Govt. John Key and Bill English deficit spent around 5% of GDP per year for four years from 2009 to 2012 to pull us painfully slowly out of the GFC recession. That's about $100bn in today's money. They also got billions in offshore insurance investment. Luxon / Willis plan to deficit spend around 2% of GDP for the next three years ($30bn). They will try and stick to those plans and use PPP deals or whatever to stimulate the economy. If they do that, we will have stagnation / recession through to their election loss.

Yes going to be interesting to see how National tackle this. I agree with you that they are eventually going to have to change their tune and increasing spending/debt to get the economy out of the doldrums. And may make them look a little two faced after the recent cuts they’ve made and the associated redundancies etc.

They’ve already started with their first budget deficit. Followed by the promise that next year they’ll be back on surplus target, which we all should know is utter nonsense.

They may have come to terms with the necessity of fiscal stimulus during a recession that we all saw coming.

I think the first budget was tight to help with inflation and also to blame Labour and clear the decks, that first 100 days was a ruthless rejection of everything Labour did. Now the hard work starts, how to fix things.

I personally think they need to

- Allow foreign investment big time.

- Slash the corporate tax rate to 15% to attract foreign investment, sure steal company HQ from aussie.

- Stamp duty on houses to bring new revenue in

- Capital gains tax on all land transactions , even family homes. Possibly the only way to take heat out of the market.

- Lets take GST off food and veges.

- No tax first 10k income.

- Compulsary Kiwisaver, with a variable % of contribution set by RBNZ, no opt out. Moved up when markets hot and need to fight

- Setup Fannie Mac style secondary mortgage market which will finally introduce competition into the mortgage market

I agree with most of those. However to borrow from Yvil, there’s a gulf between what ‘should’ happen and what ‘will’ happen!

The Nats are far too conservative to initiate most of those things

which is why they will be voted out

That's not why they'll get voted out. The other crowd will dangle baubles to address whatever malaise their target demographic are clambering for.

Then in another 3-6 years, it'll swing back the other way again.

what like tax cuts?

Yeah that'd fit under the bauble umbrella. Tax cuts, supplements, moral nice-to-haves, adding or removing of certain rights and laws.

Basically anything moving money from one hand to another, without actually generating an extra cent of value.

Although maybe this perpetual political change industry in itself adds to GDP growth. Except we're having to finance it.

How does Manapouri dam fit in to your idea that the government doesn't ever create value?

Also have you ever lived in a place without roads? It would be pretty hard for others to create value without those in place.

Does a private hostpital create value? Why would a public one not create value, but a private one would?

The not creating value comment was in regards to shifting subsidy from one area to another, i.e. a tax reduction here, or an entitlement provided there.

You're referring to government capital expenditure. Which can add value, but much of the government's projects do not. Which is fine, if we're talking about some sort of social good, like a hospital, or schools (although our education should be contributing towards fostering individuals who are able to have a net positive impact on our economy), but that needs to be tempered with an equal or greater amount of investment in projects that create a net positive return. What's our track record been over the past few decades?

The government provides the environment for a countries people to live well and be productive. That has value.

You seem to be measuring value simply in terms of dollars made. The government is not a business, so they don't focus on making money. They have some investments but mainly tax and spend. In fact, every time they have a profit making business, the right wing get into power and privatise those businesses.

As for the governments track record, NZ is still a pretty great place to live compared to the rest of the world, so they can't be doing that badly. Whatever is lacking won't be fixed by cutting budgets. Not sure what projects you would like them to do more of. The new ferries and the pumped hydro storage sounded positive to me. But the current government decided to knock those on the head.

IMO - the short sightedness and feigning to the trucking industry over the replacement Ferry debacle will come back to haunt National

I agree with most of those. However to borrow from Yvil, there’s a gulf between what ‘should’ happen and what ‘will’ happen!

That is the funny thing about interest. If the aim is understanding things economic to use in your personal financial endeavours, you really have to try and determine how things are, and where they're going.

Playing "what I'd do if I were calling the shots", is kinda fun. Sorta like envisaging what you'd do to survive a zombie apocalypse. But invariably daydreaming.

Haha yeah

I agree with quite a bit of that. But, the first bullet - ramp up offshore investment - is a big no for me. What that means is encouraging offshore ownership of domestic assets. This invariably creates a flow of rent offshore over the medium- to long-term, which will add to our current account deficit and diminish our monetary independence. We don't need offshore finance - we built a whole country after 1930 using public investment from Govt / RBNZ - the kind of investment that keeps cash and demand onshore. This is one of the many reasons I hate PPPs - it's a double loss - expensive finance that creates a mechanism on purpose to literally drain our domestic economy of cash. Crazy.

Ironically, the first one is the ONLY one the coalition are likely to implement. Luxon is the worse National leader in living memory.

"They will try and stick to those plans and use PPP deals or whatever to stimulate the economy."

Sadly I fear you are correct...what an unnecessarily expensive way to hobble our economy out into the future.

Damien Grant reality check

"We are not in a recession because a recession implies a hiatus between periods of economic growth. We are experiencing sustained economic decline and are unwilling to either discuss this fact, nor do anything about it."

https://www.stuff.co.nz/money/350364940/damien-grant-we-may-be-avoiding…

Great article.

What a shitshow our economy is.

And the quote from Dr Wilkinson is notable. We can beat our nationalistic chests all we like about our country’s beauty and ‘quality of life’, and how good we are at minority sports that no one outside this country cares about, but wages and the cost of housing really, really matter.

Basic stuff.

In the grand scheme of things

They don't really matter at all.

Sometimes I wonder if our economic malaise isn't partially attributed to Kiwis' bent towards lifestyle over being too commercially orientated - goes for both business owners and workers.

Well, it’s very easy to say that if you are in a position of financial comfort.

come on, mannnnn

I've had times in my life where while not totally destitute, my family's financial situation was fairly dire. One thing that made that tolerable was the fact we live in such an amazing place, where you can find enjoyment for free.

Even now, commercially I am fairly underutilizing myself, because commerce is a fairly arid endeavour. If I didn't think I could live to the ages of my ancestors, I'd be doing even less.

CPI would take 50k to 71k not 83k so wages grew faster than costs. Forgotten GST increase.

Lower taxes less infrastructure.

Interesting that he reckons a change back to Labour next election. Who knows if he’s just being provocative.

It’s certainly a chance if our economy is as dire as I think it will be over the next couple of years.

Real unemployment is 11.6%, MSD quarterly reports.

Real Inflation is 8.9%. HHS+CPI.

Labour did it! A. (Eeee)Orrs $100b Bazooka killed the NZ economy and has turned into a Boomerang.

Oh. And GDP 'growth 0.2%.

Oh! Oh! And the NZD has found a new bottom by fluctuating btw 58 cents to 59 cents to the no longer Petro US Dollar, Reserve Currency.

Some people's "reality" is just unreal.

US unemployment ticks up. The number of unemployed people across the US rose by 352,000 to 7.2 million, a notable increase from the 5.9 million registered a year earlier, when the jobless rate was 3.5%.

US Fed Chairman J Powell sits on the fence again. Maybe, maybe not, rates cut in September or November or when Trump gets elected? - He said just this week passed.

Recent migrants will be ‘employment lambs to the slaughter’. The unemployment of lots of people here on work visas will be the only thing preventing ‘official’ unemployment rising above 6-7%

The RBNZ pumped excessive liquidity into the markets during covid19 and let interest rates drop far too low.

Now people and families are being thrown on the unemployment scrap heap to crank up interest rates again.

The whole RBNZ needs to be sacked.

Also if we had direct median house prices in the CPI (as was historically done in the US & I think NZ) then interest rates would have never gone as low as they did and they wouldnt be going as high as they need to now. Houses are the biggest consumer purchase & most people buy secondhand. There is no justification for including new build costs and rents only in the CPI. The majority of the population of consumers are excluded.

The govt is also complicit. It sets the capitalist framework, the need for the OCR, and the minimum wage requirement. In such circumstances unemployment is required. It is not the fault of the unemployed. The govt should be providing govt guaranteed jobs and/or UBI and/or govt paid retraining, the last is done in some Scandinavian countries.

Good ole Liam having a reckon on the direction of interest rates:

https://www.nzherald.co.nz/business/liam-dann-whats-going-to-happen-to-…

ain't reckonomics brilliant?

The RBNZ needs to think of the 12 months after they change rates and assume the economy will drop another 20% in that time before a slow turn.

Nobody is going to retain staff today because of a .25% OCR drop.

Correct

I am increasingly thinking it’s going to be the mother of all recessions. Quite likely the worst since the early 1990s. Many people only seem to be realising this now that redundancies are a reality at their workplaces.

As soon as the rate went up so much so quickly it was apparent jobs and companies were going to get wiped out.

I guess people can always redeploy their skills in to things like porn:

https://www.nzherald.co.nz/nz/onlyfans-layla-kelly-from-banking-consult…

Granny Herald is such a world class publication isn’t it!

How is your OnlyFans going HouseMouse, mine is not getting as many hits as I had hoped.

I think there might be a niche market in ‘intellectual f%#%s’, you know, women who like brains AND brawn.

working on it

Here’s my prediction - it is already much too late to avoid the adverse consequences of RBNZ leaving the OCR much too high for much too long. By the time they realise how abysmal the economy is and finally take their foot off the break, the economy will continue to deteriorate beyond their control for another 6 months (at least) as their is a lag between OCR reductions and economic improvement. At this point, RBNZ’s incompetence will be plain for all to see. Then, RBNZ will be forced to reduce rates by much more and much quicker than almost anyone expects.

That’s plausible!!!

Yep, that's very a similar to what I posted yesterday.

It will take a lot longer than 6 months to find a bottom in our economy. It could be 24 or even 36 months before that happens.

Yep…12-18 at least…oh boy, then the printers will be roaring 🖨️🦵🥫

You make it sound like the OCR is the only reason for the failing economy Don't forget the cancel government NZ elected.

Most of our problems come from the last mob.

Complete bs

Our problems go back way further than that, certainly to 2008 if not beyond. We only avoided what's coming back then by printing inxs.

And agree above rbnz is only part of the problem.

Infact we have been voting this problem in every three years.

Oh I agree they go way back and have said that many, many times on this website.

But the last mob were especially bad. Awfully wasteful with spending, lock downs that were way too long ( and costed the country a lot), and an abysmal choice of RBNZ governor who is a big part of the current woes.

They also wasted a huge opportunity through 2021-2023 to plan for counter-cyclical investment, but didn’t. As I have said before, I talked to officials and even an ex- Minister in 2021-2022 about an imminent housing construction crash, and the need for the government to urgently plan for that, and was effectively laughed out of the room.

the last mob also set Wellington up for failure big time with the excessive bureaucratic bloat. That was never remotely sustainable and has set Wellington up for a cluster-f##* of an economy

.

You know what? Recessions happen. Always have, and always will.

And as for this one, here? The RBNZ explicitly TOLD anyone who cared to listen that one was going to be engineered. Now we can discuss whether that was right or wrong, but nobody can say "Why wasn't I told?!" Because we all were. Those who listened, got ready. Those who brushed off the warning, for whatever reason, will be the ones that pay the price of that decision.

"The Reserve Bank is deliberately engineering a recession to rein back inflation after being slow to raise interest rates,"

https://www.stuff.co.nz/business/130568638/adrian-orr-admits-reserve-ba…

Yes, financial illiteracy reigns supreme.

Nailed it, exactly correct and on point. Several idealists here jumping on the “be kind” bandwagon wanting to shred the OCR in order to save the economy. Why? How bout leave the OCR where it is and let the economy burn a little more. Or do we just want to carry on booming and busting? Let it crash and then we can start again and have a proper go at doing it right, which I can help with. (There’ll be very little of being kind)

It’s not about ‘being kind’. It’s about warding off complete economic carnage.

I would agree with you if I thought the government had a credible Plan B to the Housing Ponzi.

But they don’t.

In which case, Plan A is going to kill us anyway.

See those riots across the UK today? That's what happens when the same Plan A is all there is. The tragedy at the kindy is just a catalyst for the anger and resentment Britain's feel when they have nothing to lose. We have a choice: Find Plan B, or suffer the same fate.

100%.

The UK Tories stayed in power for 14 years by blaming Labour and saying Labour would be worse, catering to special interests and deflecting attention to "others" (immigrants, wokesters, liberals, political correctness, wasteful bureaucrats, European regulation, Human Rights rainbow community, Muslims, etc...). People sucked it up big time. And the whole time they were running down the public service and borrowing money to pay to their rich private sector mates.

If you can't see this is the exact same playbook the coalition is currently using you are a fool.

Sure. But Blair wasn’t so brilliant and who can forget his Iraq lies???

“Riots” in NZ is just an occupation that will involve weed & live music…I guess it gets the job done but you’re drawing a long bow with that connection to what happens in Europe

Replacing one Ponzi with another is reckless, we will have to convert to new growth based on exports or services with no free money based or speculation. Its going to hurt as most are not intellectually strong enough to compete.

Restarting the current Ponzi will not work as our interest rates are linked to global rates BUT our property is much much more unaffordable then most.... the ones less affordable are collapsing, china etc. Makes one question value here vs say Aussie. You can restart the Ponzi if it falls far enough, but those in it don't seem that keen.

Just got my new AKL rate bill but the CVs not out yet? so 24/25 rates are being set on 2001 cvs?

I am actually starting to come around to cutting to zero on first15k earnings current 10.5% tax, and replacing it with a tax on all property RV's to central gov.... prefer that to a sudden cut in wealth tax that David Parker was proposing.... The tax would be on every piece of land across NZ, I think just resi in nz is 1.5trillion so add in farms and commercial and you could be bringing in a few billion a year to help off set the cuts at the lower end.

10.5% off 15k would put $30 a week for almost everyone in NZ who works. Could be collected by councils and they charge a fee for collection

"You know what? Recessions happen. Always have, and always will.

And as for this one, here? The RBNZ explicitly TOLD anyone who cared to listen that one was going to be engineered. Now we can discuss whether that was right or wrong, but nobody can say "Why wasn't I told?!" Because we all were. Those who listened, got ready. Those who brushed off the warning, for whatever reason, will be the ones that pay the price of that decision."

BW, absolutely bang on.

People act on civil defense warnings of natural disasters for their own personal and physical safety yet many people ignored the warnings given by the RBNZ governor for their own financial safety.

Why did people choose not to prepare?

Perhaps the warning was only implicit and people failed to connect the dots and think of the potential consequences of a recession so this may one reason that many failed to act accordingly. They didn’t know the potential consequences of a recession. If the RBN governor had explicitly stated specific measures to prepare would that have changed some consumer behaviour? Perhaps it might then have been self-fulfilling and impacted the economy and businesses more? (given that consumption is a large part of GDP - about 80%.)

One other reason of failing to prepare was a belief that a recession wouldn't really impact them.

In February 2021 Adrian Orr also warned about overpaying for houses but Kiwis didn't listen:

The warnings from Reserve Bank Governor Adrian Orr to house buyers were stark, and simple: “taihoa”, “hold strong”,and whatever you do, don’t succumb to the FOMO.

Speaking on The AM Show about the overheating property market, Orr said investors in particular were getting “pretty carried away”.

“We’re saying look, taihoa (wait) here folks, there is no free lunch, there is no one-way bet in any investment. And when prices are so far stretched beyond the earnings of the household, that is a sign you’ve gone too far.”

It winds me up that Orr gets blamed for decisions that were made by politicians we voted in.

Did the government; drop LVR’s, keep the FLP going a year longer than contemporaneous information indicated in needed to be, implement the LSAP or keep the OCR at record low levels for much longer than necessary?

While inflation is like the sweetest of tax free suger highs for the leveraged speculator, it is a poison for the rest of the economy. Especially for those relying on govt welfare income, and actual tax payers funding that.

This mess was always coming. Those that prepared for it will do well, very well. Those blinded by endless suger rush ignoring the warnings... should burn.

🍿

Honest question but who does well out of a faltering economy? Debt collectors, insolvency services and.. (I’m ready to invest on a winning horse)

Hahaha Wowee…what a crock of 💩!!

Ole Tane Mahuta also told everyone not long before that “low rates are here to stay for the foreseeable future”…imagine it like this…he encouraged everyone to speed as fast as they possibly can…then just as the car was flying off the cliff he yelled “brake” 🤦🏻♂️🤦🏻♂️😂😂

Anything above 4.7 the RBNZ is really going to feel the heat at the August review.

And drop the OCR to do what? Reignite the Property Market? If that's the hope, then we probably have a lot longer to wait than most anticipate.

Rule No 1 : "When you have your foot on the throat of the enemy, keep it there for some time after you think it's dead. Then, stamp down on it just one more time; a bit harder to make sure. Then and only then remove foot"

Why? Because if you let it recover, it's not only going to be very angry, but seek revenge.

This maybe why the RBNZ ends up cutting more slowly then people in property debt think, If housing crashes another 20% then yes they will cut quite hard to form a floor, then raise rates at the first hint of growth

And that....sounds like a Plan.

If they really want to mess with the idealists they should lower it by 2 points this month followed by a raise of 3 in November. Shake it up.

Dropping the OCR swiftly would help the ailing residential construction sector quite a lot.

Other things not so much, at least not for a while

💯 they could slash rates in ten days & it wouldn’t do bugger all to house prices…maybe give it a wee bump…people are scarred, people have used their savings, houses aren’t seen as “double in 10 years” gig for this next group of buyers…use DTI/LVR just in case & drop rates to give some relief to businesses who need it

I come back to ‘what will be done’ compared to ‘what should be done’ (Yvil)

Housing is a huge part of NZ’s political economy. It won’t be allowed to crash much more.

"Life is what happens when you're busy making other Plans" ie: What's 'allowed' and what actually happens can be polar opposites. Given all the uncertainties on the World this very afternoon, we might all look back on Adrian Orr as our saviour, as he at least got us as ready as we were prepared to get.

"Russian submarine sunk in Crimea"

"UK prepares to evacuate civilians from Lebanon"

"Venezuela: Blinken congratulates González on winning election"

Would that sub be nuclear armed? If so, what happens to the nukes on board ? Would the Russians try and recover them?

Ukraine's military says it attacked and destroyed a Russian submarine while it was anchored at a port in the occupied Crimean peninsula.

The Rostov-on-Don, a kilo-class attack submarine launched in 2014, sank after it was struck in a missile attack on the port city of Sevastopol on Friday, Ukraine's general staff said in a statement.

It was reportedly one of four submarines operated by Russia's Black Sea fleet capable of launching Kalibr cruise missiles. The Russian defence ministry has not commented.

Officials in Kyiv said the attack also destroyed four S-400 air defence systems protecting the peninsula, which Russia illegally annexed in 2014.

we might all look back on Adrian Orr as our saviour, as he at least got us as ready as we were prepared to get.

It is really hard to determine how much forecasting of global affairs is involved in the RBNZs decision making. Sometimes it feels like they are making all their decisions in a vacuum that assumes global continuity, but perhaps they have elevated interest rates in anticipation of some seriously bad global events.

Only the low and no skilled people will end up on the unemployment benefit. Which is great for them as they'll earn more on a benefit than working anyway (Jobseeker pays $63k a year for a family with 2 kids). The skilled professionals will simply move to Australia for higher wages and better weather. Thus we will have the worst of both worlds - high unemployment AND a skills shortage that crushes our ability to deliver public services like health and education, and crimps private productivity.

NZ has turned into South Africa. Brace for electricity grid failures.

NZ has turned into South Africa.

The South Africans still moving here would strongly disagree.

I know plenty of expats leaving/left nz… they look around when shit gets real…don’t blame them

It always makes me laugh when people say we're like South Africa, pretty sure they have never been or if they have it's to a nice resort.

Dribble…nothing like SA 🤦🏻♂️

One of the many reasons that I don't think the interest rate is that relevant to the next year or so economically...

The banks have risks to manage and term deposits to see throgh - they will take ages to pass through the change. The last 20 years of data suggests that a 1-year fixed rate mortgage of less than 6% will only happen once the OCR is at or below about 3.5%. If you want a 2-year fixed rate at less than 6%, you are probably going to need an OCR well south of 3%.

Twenty years of history also teaches us (of course) that RBNZ have never achieved a smooth transition from high to low rates or vice versa. The idea that this time we will find some kind of equilibrium at 4% or something it hopelessly naive.

That’s interesting. It makes the banks current 3 year rates of sub 6% worth considering.

Although there’s question marks over the data in those graphs. I seem to recall 1 year rates of 2% in 2021.

The data is from RBNZ B20. There are often better deals than the averages they publish, that's true. But I left a bit of a margin of error for that.

So we are screwed regardless. Especially with a govt not willing to pull the fiscal lever.

Is pulling the fiscal lever inherently good? Often it is just short term stimulus with a bill to pass on. We sorta did that over Covid, and are paying for it today.

Correct, it’s not inherently good. But it’s potentially very good.

Labour squandered a great opportunity to progress a FHB house building programme running over many years that would help negate this boom/bust nonsense we are experiencing *once again*

sigh….

But it’s potentially very good.

It requires our decision makers to be

A) good custodians of government spend, delivering projects of reasonable value and suitability

B) capable of entrepreneurial vision

The former is something we don't have much of a good recent track record of. The latter is hard to do via committee.

Agree.

The calibre of our politicians is generally very poor.

huh...?

"Labour squandered a great opportunity to progress a FHB house building programme"??

I think you will find Fletchers squandered a great opportunity.

could have been the volume to allow long term investment in modern plants

still stuck with yards and building materials outlets.

let the whole system reset and find new land, finance and build costs

Private sector will never build housing that middle and lower middle income households can afford.

Of course it’s a huge call to think any of our governments could ever be capable enough to execute a mass house building program for FHBs.

Oh it will, when that’s all the punters can pay

They got in on a mandate to cut tax a bit and stop waste, I do not think they know what to spend a stimulus package on.

Most NAct supporters just want to got back to the good times of the Ponzi... sadly its over, Labour have no clue either look at the covid spending, even the Auditor General was disgusted.

Hey JFoe - if you do not want foreign investment how would you fund stuff, general gov borrowing? what about the posibillity of the gov borrowing building toll roads , then issuing bonds with that revenue as security , so they could recycle the spending? over 30 years the asset could pay itself off and stay in NZ hands?

interested in how you see things being funded?

"the good times of the Ponzi... sadly its over. Let's hope so. And if we can take heart from any clues that we might have been given, perhaps they come in the form of the words from our Minister of Housing/Associate Minster of Finance = "I want to see property prices fall" and our Prime Minister, who is selling investment property at the moment. Words and actions slightly less pointed than "I'm going to engineer a Recession" but probably just as noteworthy.

Yeah but talk is cheap

I remember some of the utterances of Don Key back in the day on housing….

"Yeah but talk is cheap"

Politicians are known to use their political rhetoric / verbal jujitsu / political spin on the voters, so that they can win those popularity contests.

Yes, Govt has unlimited access to funding in NZD. Even now they have $30bn in their Crown Settlement Account, plus a $5bn overdraft that RBNZ can, at any time, extend to $10bn, or $100bn, or whatever. The amount Govt spends is constrained by votes not by the availability of finance.

Govt still goes into debt when it spends money of course - that's what Govt debt is, money that Govt has spent into the economy. That debt sits in commercial bank settlement account (earning OCR) or in the form of interest-earning Govt bonds. When Treasury sell bonds they are swapping the form of debt - it's not a borrowing operation (unless you believe in the fairytale that RBNZ is a completely independent financial entity).

So, yes, absolutely use the cheapest finance available to build stuff. Why pay 300 - 400pts more in interest to borrow privately just to avoid your debt showing up in our stupid definition of Govt debt?!?

In terms of what taxation or other mechanism (tolls, fees, excise etc) to use to take back the money that Govt has spent into the economy, I guess that depends on your politics. I would personally go hard on unearned income - rent extracted by people who own rent-generating assets. I would also tax excessive capital gains out of existence.

My view, as people probably know, is that we shoud be mobilising more of our real resources for the public good. Why have people standing around in Harvey Norman trying to sell us stuff, or packs of estate agents trying to get people to bid up the price of houses, when we need more people looking after older people, building infrastructure, and helping out in classrooms? Higher Govt spending and taxation are the obvious way of changing this balance.

Ultimately all the mess has been caused by the bank deemed "credit worthy" exploiting those that are not over the basic need of shelter. All the while the banks laughing to the proverbial bank as the exploiters greed create and ever greater vortex of tax free flipping to the next exploiter. We then end up with this mess being the center of the economy

Untill it all spirals out of control. Let the greed of the exploiters burn themselves down.

Ultimately all the mess has been caused by the bank deemed "credit worthy" exploiting those that are not over the basic need of shelter.

Government policies change consumer behaviour. RBNZ policies change lending behaviour. Speculation is inherent in a capitalist system. Speculators can outbid end users. There has been speculation in many items (tulips, beanie babies, art, baseball cards, etc)

On residential real estate in NZ, it seems that the borrowing power for non owner occupiers has increased more than for non owner occupiers, meaning that non owner occupiers may be more likely to outbid owner occupiers if other borrowing criteria are similar (similar deposit, similar uncommitted monthly income).

A person wanting to buy their first home could borrow up to $21,500 more under the bank’s income tests after the change. That assumes that both members of a couple get $20 a week extra. It’s a small amount, but it could push some borrowers over the line.

Property investors will be able to borrow slightly more as a result of the tax cuts. That’s because when they buy a rental property, they also get more rental income. A couple wanting to buy an investment property could borrow up to $32,000 more under the banks’ income tests now the tax cuts have come into effect.

https://www.oneroof.co.nz/news/latest-news/what-will-you-spend-your-tax…

This has been one of the better reader comment threads of late. Some good insights and very interesting - thankyou all

RBNZ look on track to meet their 2% mandate if the next read comes in at about the same level the last three have. This is what a soft landing looks like.

RBNZ could cut rates but they'd need to suppress inflation, they have about $30bn of bonds they could move it the market to achieve that suppression but it's higher risk than "wait and see." Reserve Banks like "wait and see."

RBNZ looking at unemployment (a lagging indicator) to decide whether to cut or not is like putting your foot on the accelerator while looking in the rearview mirror, just as you are about to drive over a cliff.

The theme going forward, likely until the end of 2026 if not later, is going to be rising unemployment and bankruptcies.

We might be tempted to compare this to the GFC because of recency bias, but that would be quite optimistic. The GFC will seem like a walk in the park compared to what is coming.

In a debt-based economy, the main risk is deflation, not inflation. Tightening sets off a vicious cycle of bankruptcies -> unemployment -> demand destruction -> more bankruptcies

Agree. This might give the early 90s ugliness a good run for its money.

Absolutely. According to NZIER, 73% of manufacturers said profits are declining, the worst reading ever (since 1969). Plus, 39% are planning to lay off staff, the worst since the GFC. We are seeing GFC-like numbers and some of the worst readings in history before the fireworks even start.

Hey Wingman Buffet is selling here not buying

https://www.zerohedge.com/markets/buffett-calls-top-berkshire-quietly-d…

When yesterday we said, when discussing Buffett's ongoing liquidation of his Bank of America stake, that "Berkshire's rising cash stockpiles merely reflect the firm's inability to find deals in today's overvalued and weak economic environment", little did we know just how accurate that would be, because fast-forwarding just one day later we find that far from only dumping Bank of America, the 93-year-old Omaha billionaire had been busy quietly dumping his most iconic holding in an unprecedented selling spree that sent Berkshire's cash pile soaring by a record $88 billion to an all time high $277 billion at the end of Q2.

and the VIX is up big time, probably nothing...

He is too smart to be a bagholder. Seems like he is making sure he is not the last one standing when the music stops.

He has very good timing

Indeed. Stock markets provides a path to exit an investment quickly, and if the market is large, exit large positions without fuss. Overpriced NZ rotbox anyone....?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.