Here we go. Watch, Worry and Wait Part II.

This coming Wednesday (August 16) will see the Reserve Bank's second consecutive 'do nothing' Official Cash Rate review since it raised the OCR to 5.50% in May and at the same time signalled, via its forecasts, that it would not be going any higher - not in the foreseeable future. At the last review in July the RBNZ made good on this intention by duly leaving the OCR unchanged.

This time around the review is accompanied by a new Monetary Policy Statement (MPS) - the first since the May review.

This document will give us the opportunity to see if the watching, worrying and waiting ('watch, worry and wait' is a term the RBNZ itself uses) has led to any changes in how the central bank views the way forward from here.

So, most interest will centre on the forecasts part of the MPS towards the back of the document and whether any of the key forecasts have changed since the May MPS was issued.

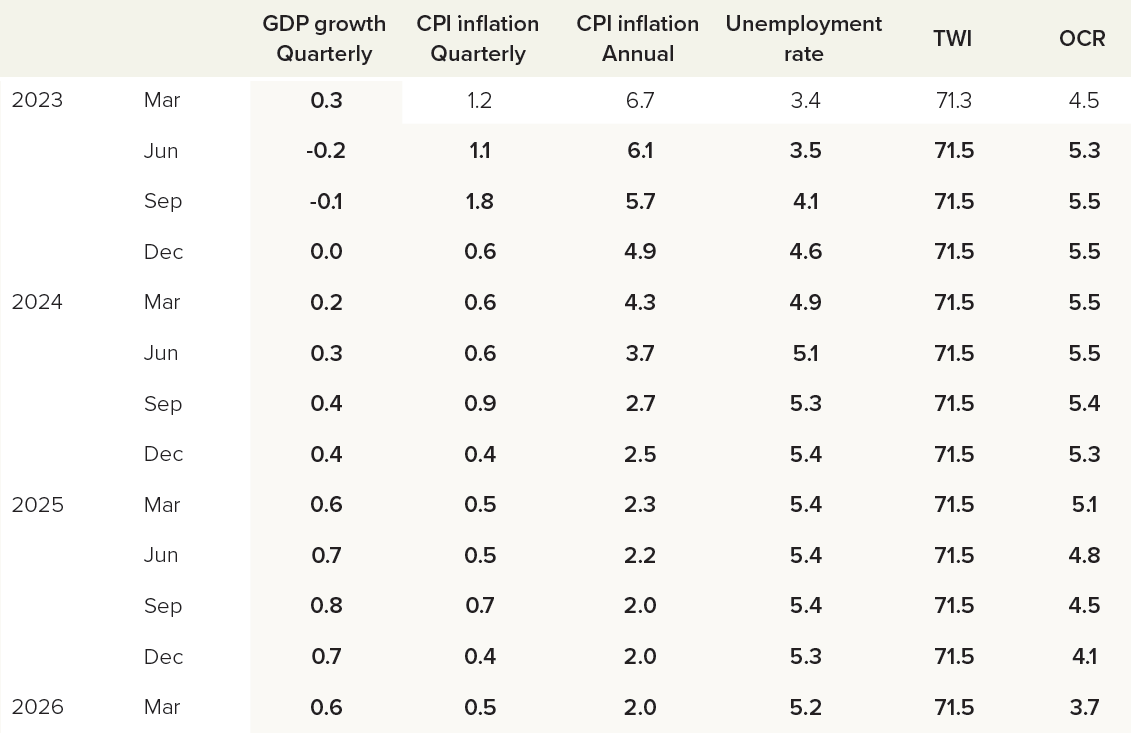

To refresh memories, here's an abridged table of the main forecasts made then. (The full table appears on page 57 of the MPS.)

How might the new forecasts differ from those in May?

Well, we need to consider the most recent economic events.

The 'big' economic data released since the last OCR review have been the June Consumers Price Index inflation figures and the labour market figures, including the unemployment numbers and wage data.

To take the CPI data first, you can see from the table above that the RBNZ was picking 6.1% annual inflation as of the June quarter, while the actual figure was 6.0%. Great! All on track then! Well, kind of...

The reality is that the drop in the inflation rate from 6.7% to 6.0% was largely a story of falling petrol prices helping to drive a sharp drop in the so-called 'tradable' or imported, inflation. But it's 'non-tradable', domestically generated inflation that the RBNZ can do something about and therefore directly worries about. And as of June the non-tradable annual inflation rate had fallen only slightly from 6.8% to 6.6%, while the RBNZ had forecast it to fall to 6.3%.

If that's not great news well the further cloud on the horizon is that petrol prices, as I'm sure you've noticed, have gone up again since the start of the September quarter. And of course at the end of June the Government reversed its previous cut of petrol excise duties.

The upshot is that the 'headline' inflation figure for the September quarter might well actually rise again to above the previous 6.0%, while the RBNZ's May forecast was for it to keep falling to 5.7%. This should be a short term blip. But it won't inspire confidence in the wider community that all is on track.

Not wonderful news either for the RBNZ was delivered via its own Survey of Expectations in the past week, in which the most watched measure, the expectation of inflation in two years' time actually increased very slightly to 2.83%. This contrasts sharply with the RBNZ's own forecast as of May that inflation will be sitting comfy on its explicitly targeted level of exactly 2.0% in two years' time.

The survey result shouldn't be taken too literally, as in don't expect inflation to be 2.83% in two years' time. But do take that result as conveying apprehension out there that the RBNZ's not got this inflation battle in the bag yet.

So, watch out for a tweak to that September quarter inflation forecast in the new MPS, but more significantly perhaps, we need to keep an eye on the December quarter forecast (which was for 4.9% as at May) and see whether the view has changed.

As at May the RBNZ was picking inflation to get back into its targeted 1% to 3% range in the second half of next year.

Watch out then for any slippage in the timing of inflation getting back under 3% in the RBNZ's new forecasts in the coming week. This would cause flutters in financial markets.

Right, so, that's inflation. Then there's the labour market and the June quarter data. The employment figure came in much higher than the RBNZ forecast, but the wage inflation was pretty much in line with what the RBNZ picked, while unemployment, at 3.6%, came in actually a touch higher than the RBNZ forecast.

That latter fact might be sufficient to encourage the RBNZ to stay with its May pick that unemployment will shoot up to 4.1% in the September quarter and 4.6% in the December quarter. These were very bold picks that effectively suggest the labour market will capitulate in the second half of the year. There's a fair degree of scepticism among economists that the labour market will go that cold that quickly - though everybody agrees the unemployment rate will rise, just not necessarily that fast.

There's no doubt a slowdown is under way though. And further evidence was provided of that in the past week with the latest electronic cards spending data showing a decline for the second month in three.

For the RBNZ, creating some 'slack' in the labour market (IE more jobless) is crucial to the inflation fight, since this will dampen down spending and reduce pricing pressure. So, we should keenly watch whether the RBNZ sticks with view on the unemployment rate, or backs away and picks a slower cooling of the labour market. If it's the latter, this will cause concern.

All right, so, there go the big economic stats we need to be worried about. But then there's the not-at-all insignificant matter of what the RBNZ will do with its forecasts of the OCR level in the future. The May forecast was for the OCR to be at 5.50% till the second half of 2024 and then slowly dropping.

Even if the RBNZ were of a mind that it may yet raise the OCR again in future, I doubt whether it would be inclined to indicate as much yet. If it were for example, to just quietly slip in a new peak of 6.0% into the new set of forecasts in the coming week this would likely produce an out-sized reaction in the wholesale interest rate markets.

And at the moment the markets are behaving probably pretty much as the RBNZ would like.

For a long time the market was getting ahead of itself and pricing in future reductions in interest rates - as soon as later this year. But current pricing has just a under 50-50 chance of a further OCR hike before the end of this year and then for reductions to not begin till the second quarter of next year.

As far as the RBNZ's concerned, this is probably about right, other than that maybe it would like the market's view around timing of OCR reductions to be pushed out a bit further.

So, if there is to be a tweak of the OCR forecast in the coming week, probably the most likely thing is for the RBNZ to push out the forecast time for when the OCR starts to come down from 5.50%.

No OCR hike in the coming week then. But much to look out for. This watching, worrying and waiting thing is stressful. And we might have a fair bit of it to do yet.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

54 Comments

The next "Influencer" will be the change in government in October. People may think the RBNZ is independent but its not.

Did you read this in the chemtrails?

They are "independent" but must answer to the government. Who else can summon the RBNZ to justify their decisions? The government is in the best position to pin the blame for economic woes on the poor performance of the RBNZ.

The chemtrails are about to turn into entrails for Labour. I'm awaiting some really desperate election promise from them like UBI.

Many believe they were just doing a poor job...but it's just not possible.

Roll on green stimulus... and, the restructure of all else.

No chance of any change until after the election for sure. Political nicety.

RBNZ have done the damage. Businesses are now paying $25M per day to the banks in interest (on business loans), Govt is chipping in another $6M - $7M (net on settlement balances), and mortgagors (incl landlords) are handing over a ridiculous $50M per day. That's $29 billion per year by the way - well over 10% of household consumption expenditure!!! Savers are getting about half of this as interest on their term deposits etc, and bank shareholders are getting the other half.

We are now in the extremely rare position where the total balance of current (transaction) accounts are reducing as businesses and households start to struggle. And, lest we forget, we still have people rolling onto higher mortgage rates and businesses taking on debt and overdrafts as they try to survive being bled out.

Meanwhile prices (CPI) are coming down more slowly than in other countries because, although import prices are falling, businesses are trying to keep prices at a level where they can afford to meet higher costs - including credit costs, and other unavoidables / non-substitutables like fuel, rocketing insurance premiums etc.

RBNZ know all of this of course but they have trapped themselves in a position of having to 'maintain credibility' - hoping that at some point prices will come down and they can say what a good job they've done. The Fed are trying this in the US - arguing that raising rates led to a dramatic downshift in prices a few months later despite there being next to no evidence to support this position, nor any possible causal chain through monetary policy that could explain such a rapid impact.

Jfoe I get the queries about the effectiveness of interest as a tool but it’s hard to argue two things:

(i) and indirect consequence with asset prices coming down making people feel less rich, and

(ii) those paying higher interest costs spend less on everything else

Both these lead to lower demand and then lower prices.

I the OCR is a shitty tool but I does kind of work with direct causation and indirect influences. We just need something better.

The reverse wealth effect is slowing house renovation projects etc - but the comfortably off kiwis who do most of the spending are feeling pretty good regardless. Remember, households are actually net beneficiaries of higher interest rates - households with savings / term deposits are getting more $ than households with mortgages are paying out. How? Because the big losers at the sector level are businesses.

All of that said, higher rates are sucking money out of the economy, and you can see this is reducing spending (e.g. latest card spending data). The question is: Will reduced spending actually lead to slower price growth? Why would it? A company that only has half the orders it used do is more likely to downsize than to start a price war, and, if companies do drop prices and start losing money, and we see reduced competition as they fail, will that reduce or increase prices?

My concern is that with this episode of supply-side inflation, a high OCR could actually be inflationary. How can you add $10bn of costs to business per year whilst throwing money at rich people and then expect price increases to moderate?

Will reduced spending actually lead to slower price growth? Why would it?

Yes it will, Jfoe, why? Because with less demand, businesses will stop raising prices. Remember the prices don't need to drop to lower inflation, they just need to stop rising!

I agree that lower demand due to reduced affordability may prevent prices going up, but what other forces are at play?

If businesses go bust and competition reduces, will businesses use their additional market power to increase nominal mark-ups / profits? If costs are going up for competing businesses (eg credit, insurance, diesel, carbon) will those businesses pass on increased costs to their customers knowing that they are all in the same boat? If all businesses in a sector have faced weather-related losses, will they not all seek to rebuild their balance sheets? What about those that have monopoly power and can use inflation to stack up the cash? There is a reason AirNZ is top of the share price growth chart at the moment (closely followed by energy companies)!

My challenge here is this....What is the net result of all of hte cpmpeting factors above and how much difference is the OCR actually making? Higher credit costs are dramatically increasing costs for businesses and may lead to some going bust - that creates an upwards pressure on prices. Higher prices are already reducing affordability (and therefore demand?) - how much difference is hammering a heroic group of a few hundred thousand mortgagors actually making to demand?

You ask many valid questions, I guess we'll have the answers within two years.

Japan has low interest rates and low inflation. The BOJ hasn't bought into the world wide mania and it is supporting its economy and people by running large budget deficits.

1. Japan has a huge current account surplus and therefore can afford to buy its own bonds to keep interest rates low.

2. The Japanese are net savers and the New Zealanders not!

That current account surplus does give Japan a stronger monetary sovereignty. NZ now has $70bn of bonds held overseas (a record high in nominal and % terms). My personal view is that a country needs to achieve a broadly balanced trade position (self-sufficiency in food and energy particularly) to break away from just tracking the Fed rates.

I would look at other countries like Denmark, Spain, France etc where moderate rate rises accompanied by strong govt action have led to rapidly reducing inflation.

The telling number is the disparity between business loans and mortgages. Just a ridiculous amount of capital in non-productive assets. I'm no jack tame fan, but he had luxon on the ropes on this, old mate wasn't comfortable, nor did he have any solution.

100% Agree. A good summary.

Why the RBNZ sticks with the OCR, a tool developed back in the 60s and implemented first in the 70s and became 'mainstream' in the 80s and 90s, is beyond me. A perfect example of moribund thinking if ever there was one.

The target is 2%, or has it changed to 1 - 3% in other words gone up. The whole thing I’d crap, the RB tries to show control but they have very little. Inflation is here to stay. They simply cannot put rates up much future because it’s going to go boom.

Seems quite obvious to me that the economy is cooling and demand inflation will dry up. Supply inflation has already decreased in terms of global prices. Food inflation should disappear if we have a decent growing season next year. If anything the RBNZ should be thinking when the first OCR cut is needed, it might not be as far away as everyone thinks.

Largely agree with this. I’ve been surprised with how hawkish a couple of the bank economists have been lately (ANZ, Westpac) - emphasizing the upside risks of inflation and downplaying the softness in economic activity. Q2 GDP will be critical for the overall narrative. Do we see a bounce back after a couple of negative quarters, or another weak result?

RBNZ always moves in 25bps jumps, but predicts 10bps changes?

I wonder how the higher energy prices will play out relative to last year’s spike. If budgets are more constrained (higher rates, etc.) will there be more substitution vs. ‘consumption level maintenance’ from higher overall spending? Will be bad for headline inflation regardless, but could be a more significant drag on growth than what we saw last year.

What I've factored in is the following:

1) Personal: higher energy prices combined with reduced household disposable incomes will see them using less energy. The older and wealthier with term deposits receiving high interest payments will continue to operate as they have. Net effect: less energy being used.

2) Businesses: They'll use slightly less as demand contracts overall but they'll try and pass on the costs. Net effect: less energy being used - some inflationary pressures but more businesses going to the wall.

3) Public: Like businesses but possibly a more significant reduction in consumption. Net effect: less energy being used.

Overall the inflationary effect will be much less than back in early 2022 when Pootin shocked many (i.e. those who weren't following the news of what russian forces were up to. It came as no surprise to those of us watch Pootin. It was well telegraphed months - if not years (2014) - in advance.)

It's a puzzle why much notice is taken of consumer predictions of future inflation. If you'd asked the same bunch just under three years ago whether a Labour majority government would be a good idea it would have been a (net) resounding yes!

Will the bank also take into account the lower milk payout. This could take several billion out of New Zealands economy. Few dairy farms will show a profit this year and therefore won't be paying much tax next year. The last thing the highly leveraged rural sector needs is further interest rate rises. Townies might have a negative view of farming, but they should remember which sector kept the economy going through covid, when tourists were locked out. The effects of interest rate changes take a while to feed through, the bank should consider a 0.25% cut to signal a glimmer of hope.

I think the GST from the Construction sector is going to be down massively as well.

I think the next move is down but think it’s a 2024 story…. Milk payout has closed rural wallets . Red meat prices not flash and many builders forward books empty . The necessity recession is here I think recovery will need offshore demand and China is looking a bit sad here, This could be a lost decade

Does anyone know how tourism is looking ?

I used to work for a produce wholesaler and would work with the growers in Pukekohe. They all know each other and talking point has always been the price in the supermarket. 20 years ago they would get cents for potatoes onions and carrots, look at the price now. Covid was a turbo boost and the growers will never let the price go down again.

Inflation ain’t going down till we see some decent unemployment.

Even unemployed people need to eat, the labour gst removal on fresh vege and fruit is a gd thing …. There is going to be carnage in the million dollar mortgage market

Removing gst on fruit and veggies is dumb as it’s hard to implement. An easier way would be to introduce a tax free threshold.

Many OECD countries have implemented differing tax rates for different things. It isn't actually that hard.

The "hard to implement" in this situation is meaning hard to close every loophole, and whether that effort is warranted when the supermarket duopoly will just increase prices within a year to the GST inclusive values, meaning the public will be paying the same amount but Woolworths and Foodstuffs will be making more profits.

The growers don’t set the price of the fruit and veg. The market does. It would have been hard for any Pukekohe veg growers this year given the fertiliser prices and the amount of rain since December. I doubt any of them are raking it in at the moment.

When you say the market you mean the supermarkets? The supermarket buyers are nothing without the growers, supply is king. Don’t dance to the growers tune they’ll export it. Again the growers set the prices not the market.

There are many growers and 2 supermarket chains. How would the producers be able to set the price? It is a negotiation but the power is with the buyer. Not many carrots, potatoes, brassicas or lettuces are exported. Apples and Kiwi fruit yes. Have you seen the price of Avocados at the moment? 3 for $5, growers are not making money.

If you think growers aren’t making money at $1.66 per avocado you obviously haven’t seen the cars these guys drive!

What price do sprmkts pay, it should be 75 to 80 pct of that and give the growers a fair deal. But.... ahem

Most of the ones I know drive utes and tractors.

This Great Inflation decade of the 2020s is not going anywhere. The new normal.

I expect to see the OCR go to 6% or higher in late 2023/24 and stall well high into 2026.

Given the common monetary policy lags that take place, this expensive Debt world will be here for 6 years or more, completely tearing into any Debt funded asset values.

When will the mortgagee sellers lawyers take a class action against the frauds who write the Property Ponzi Pumping articles on the ONEROOF ???

They are still at this openly false financial advise giving, at calling "bottoms in". This Utter Rubbish advice that will be seen by all come Dec 2023. Falls will accelerate with higher interest rates and the pending higher MPS track that is now certainly coming down the pipe.

Not just oneroof, the ponzi uses several channels to disseminate false narratives.

Westpac economist makes a bucket list of worsening conditions the NZ economy will be facing going forward and nothing positive to expect other than added demand for housing from over a hundred thousand net migrants pouring into the country.

Yet he concludes that house prices will rise 8% in 2024.

Using one measure, that of increased wages between 2019 and now, the housing market, based on past 'fundamentals' (as screwed up as they have been), must be close to bottoming from the perspective of some first home buyers and some owner occupiers with considerable equity from purchases made 10+ years ago. Those outside these two groups will be far more circumspect.

Might I suggest looking at how the RBNZ might implement Debt-to-Income ratios?

My guess is the first implementation will be quite benign (from the view of the retail banks). However, the DTI regulations will have adjustable leavers that can be (will be?) ratcheted up over time to stop the massive waste of money going into ever increasing house prices. Obviously retail banks profits will fall unless they change their behavior. (Actually they'll fall anyway. DTI ratios are a real weapon when used properly.)

The OCR is a stupid tool that is way, way past its "best before date". Expect it to be deprecated from being the major tool. So no. The OCR won't go to 6%. The threat of DTI ratios alone will cause retail banks to restrict lending on houses. People who want to borrow big will be facing big interest rates to do so. The days of borrowing $100,000 or $2,000,000 at the same interest rate will go. (NZ mortgage market will be back to where we were 70s in some regards.)

Agreed. DTI is the speculators ebola. What...me, real equity and low leverage. Equals low to nil tax rinse. Oh the humanity.

One step further is Top's policy of requiring a 100% deposit for investment properties.

I kinda like it!

Yes the coming DTI will be the Kryptonite to the AC, TA and fellow travelling property Ponzi- spruikers.

It will be the second shoe to drop for already punch drunk, leveraged Ponzi-aficionado's........once the 6X or lower (+sinking lid) DTI is set, wow.

- Mega property reset towards a DTI of affordable 3 to 4x coming.

Rather than DTI's I would rather see a fixed minimum test rate of 10% (Or the OCR + 5%) for owner occupiers.

And a fixed test rate of 20% for all secondary homes or investment properties. (Or the OCR +15%)

The above test rates would simply be bank rules, there would not be any further oversight needed and wouldn't cost the govt a cent. This is where the K.I.S.S principle would really shine.

I still can't fathom why no parties are focusing on getting people into first homes, by making it significantly more difficult for investors to bid against FHB.

Anyone who has done the slightest bit of homework around the valuation type websites websites should know better, the more disturbing spruikers are ‘independent economists’ pumping paid for narratives into property investor Facebook echo chambers etc. People love reading what they want to hear.

Yep. PROPaganda.

The longer the OCR is left unchanged, the bigger the chance the next move is down (in 2024). This is because the lag of the effects of the 2022 rises is more likely to show in the economy the longer we wait.

100% agree. With the retail banks pushing the line that "rates will be higher for longer" to get people to fix long (to assist in future bank profits) the RBNZ will need to be extremely careful they are not seen to be operating in a way that furthers the retail bank's mega-profits.

That is not what the RBNZ chart suggests. OCR above 4% till 2026.

And the assumptions in the chart suggest this would be a best-case scenario.

On the balance of probabilities - I'm sticking with my prediction that the RBNZ will be making lots of lovin' noises in Feb/March 2024.

Ready for some humor?

First up, read BNZ's hedged guesses for where the OCR is going ... (Sensible stuff but still biases towards banks IMNSHO, i.e. "rates higher for longer" and "they could go really, really, really high").

https://www.bnz.co.nz/assets/markets/research/20230808_RBNZ-August-Mone…

Now read MSM 'interpretation' of the same. It's just amazing! Sure, some vignettes of reality in there but some leaps in logic that are just staggering.

https://www.nzherald.co.nz/business/liam-dann-worst-of-both-worlds-fall…

The bondmarkets are now in charge of determining the wholesale interest rates and not the RBNZ. If you look at the last 3 bond auctions they were all well over subscribed but nobody offered lower yield than the preveious one. All those investors see an increasing risk with the New Zealand Economy. All countries with a current account surplus, Taiwan, South Korea, Netherlands, Sweden, Norway, Australia and a couple more have significant lower interest rates while their inflation has been at a higher level or still is. Some have even higher debt levels than New Zealand but the markets deem their capacity to service those higher debtlevels superior to New Zealand.

Dave, you have neglected the value of the TWI which sits far below the forecasted 71.5 at 68.6. This creates a significant upward pressure on everything we import from anywhere in the world.

With the OCR remaining above 4% until 2026 (assuming this is a BEST CASE scenario) I really can't see much upwards house value movement between now and then. As house price is dictated by how much people can afford to borrow.

- We are currently at record low new listings for homes.

- Record low completed sales.

- Yet prices continue to decline.

It's not hard to guess what will happen with the spring/summer surge of new listings.

The writing is on the wall for property speculators and landlords - no meaningful carrying cost relief for 2 to 3 years. All the while their asset value will continue to drop in both nominal value and inflation adjusted.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.