Bank economists are increasingly calling for the Government to start reining in spending to avoid fuelling higher inflation.

BNZ’s head of research Stephen Toplis has for some months been worrying about building inflationary pressures.

Now other retail bank economists are saying the time is right for the Government to change gear and start preparing for the next crisis.

ANZ economists Sharon Zollner, Miles Workman, David Croy and Finn Robinson recognised there are still people in desperate need of government support. But they worried elevated expenditure in a capacity constrained economy risks raising prices at a time the Reserve Bank (RBNZ) is lifting interest rates to try to put a lid on inflation.

They said striking the right balance is a “tough gig” for Finance Minister Grant Robertson.

Similarly, Kiwibank economists Jarrod Kerr, Jeremy Couchman and Mary Jo Vergara noted the need for investment to address the country’s infrastructure deficit. In fact, they expected Robertson to put more aside for capital expenditure when he released his 2022 Budget Policy Statement last week.

But they said “fiscal decisions should be balanced against inflation risks” in the “current capacity constrained economic environment”.

“Tempting as it might be, pumping up Government spending risks driving inflation even higher. The RBNZ would then have to work harder to cool the economy and raise interest rates more aggressively,” they said.

ASB senior economist Mark Smith believed it “remains to be seen” whether the Government has struck the right balance between meeting shorter-term demands and preparing for future economic and fiscal challenges.

Robertson to keep the purse open for health reforms and infrastructure

The economists made these comments following Robertson last week unveiling the level of new expenditure expected in next year’s Budget.

He pencilled in a whopping $6 billion for new operational expenditure for the 2022/23 year, and $9.8 billion over four years for new capital expenditure.

Robertson foreshadowed new operational expenditure falling to $4 billion and then $3 billion in 2023/24 and 2024/25. By way of context, $3.8 billion was allocated to new operational expenditure in 2021/22.

Robertson noted next year’s $6 billion allocation would be a “one-off” largely to support health sector reforms. Some of this will likely go towards writing off debt held by district health boards.

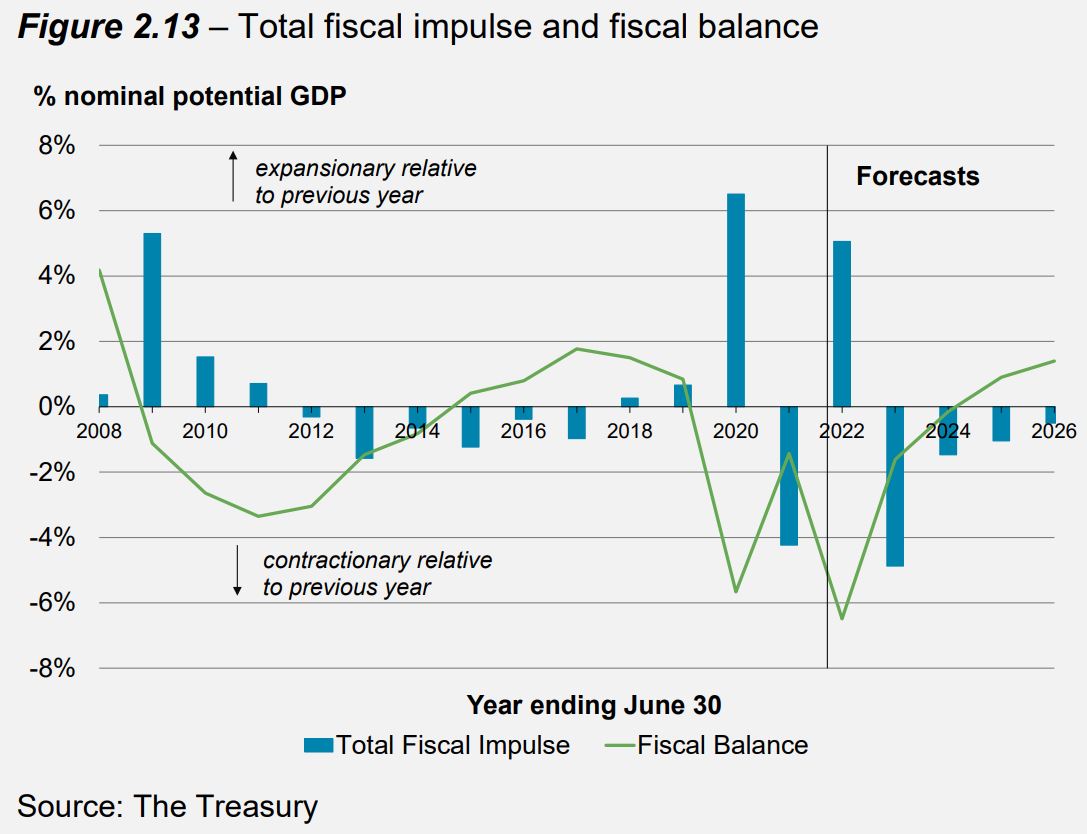

Kiwibank economists noted budgets beyond 2022 are expected to include “much more restrained increases in spending”. Accordingly, “Treasury’s fiscal impulse analysis indicates fiscal policy isn’t expected to pile on the pressure on aggregate demand beyond 2022”.

Council of Trade Unions economist Craig Renney (who used to advise Robertson) said his old boss shouldn’t listen to “the call of those who would cut spending without thought to the long-term consequences”.

“The medicine is working, and completing the course through continued investment in public services and infrastructure is essential to make sure we emerge with a more productive, sustainable and inclusive economy in the future,” Renney said.

Taxes as a share of GDP can only go up

However, ANZ economists said the economic landscape has “changed drastically over the past year or so”.

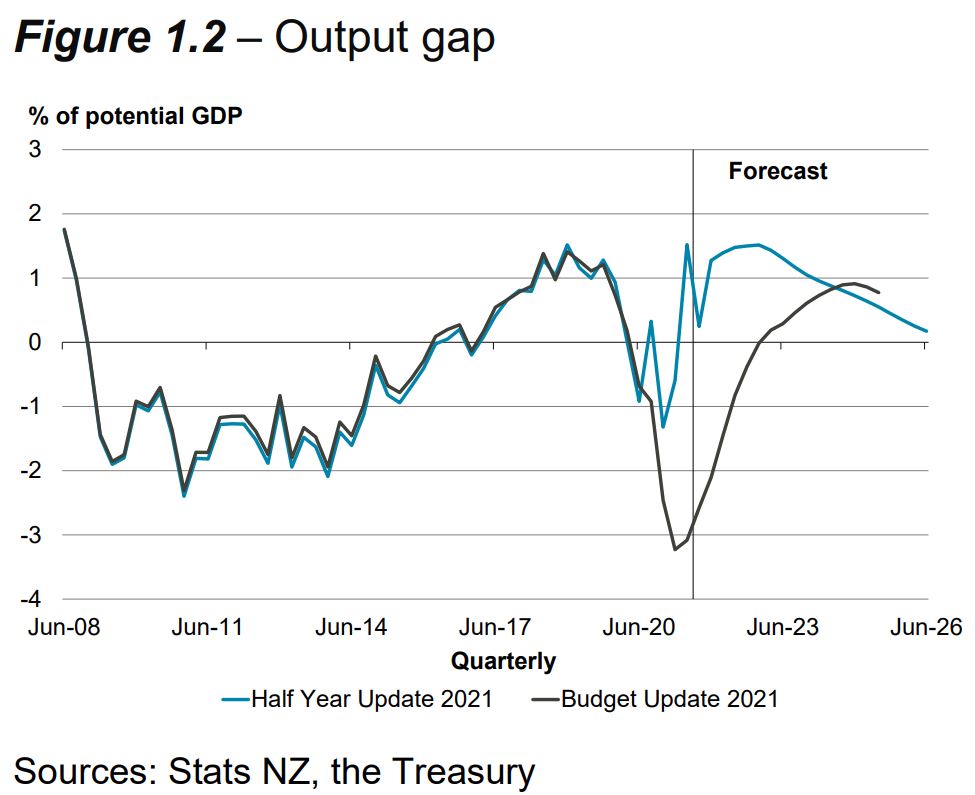

Treasury, in its Half Year Update released last week, noted, “The difference between actual and long-run potential economic activity, a key measure of spare capacity in the economy known as the output gap, has been more positive than previously thought. This lack of capacity is a strong indication of domestic inflationary pressure.”

ANZ economists said, “For many, inflation is outpacing wage growth, meaning if you’re not working longer hours, you’re going backwards.

“Further, high rates of inflation tend to hurt poorer people more, meaning some of the benefit of high fiscal outgoings is being offset. We’re certainly not saying the Government should stop helping those in need, but we are highlighting that the economic landscape has changed.”

They said now is the time for the Government to start preparing for the next crisis.

“If the Government is not rebuilding fiscal buffers during the peak of the cycle, they will have less ammunition at the bottom,” ANZ economists said.

“On top of the cyclical position, there are other good reasons to put fiscal settings under the microscope. Households and the Government have taken on a lot of debt recently. That debt will carry a lasting legacy, and leave us all exposed to higher interest rate risk.

“Add the costs of an ageing population and climate change (which, alongside the housing crisis, are goliath challenges from an intergenerational inequality perspective), and it’s easy to conclude that in the absence of some fiscal constraint today, taxes as a share of GDP can only go one way in the future; up!”

Running down Treasury’s cash account will add liquidity to the system

The large amount of fiscal and monetary stimulus provided since the onset of the pandemic has supported the economy, contributing towards gross domestic product (GDP) being much stronger than expected.

This has boosted the Government’s tax take and seen Treasury forecast a return to surplus in 2024 - sooner than it forecast at the Budget in May. The deficit currently sits at $4.6 billion.

The stronger-than-expected economy has also meant Treasury’s Debt Management office could cut its forecast bond issuance programme by a third in the period between 2022 and 2025. It plans to issue $20 billion of New Zealand Government Bonds in the year to June 2022, and then $18 billion in each of the following three years.

While this is a downgrade, it’s still historically high. Pre-Covid, Debt Management forecast issuing only $8 billion of debt in the year to June 2022.

While some government spending will be financed by newly-issued debt, some will be financed by previously-issued debt sitting in Treasury’s cash account at the RBNZ. As at November, there was $36 billion in this Crown Settlement Account.

ANZ economists said financing spending using these funds will add liquidity to the financial system, which should put downward pressure on short-term interest rates and bond yields “at the margin”. Remember, the RBNZ is trying to lift rates to cool inflation.

Opposition take opportunity to attack the Govt

National and ACT have seized the opportunity to attack Robertson for playing a part in boosting inflation.

Robertson has tried to deflect, by saying higher levels of inflation are a global phenomenon, sparked partly by matters outside of the New Zealand’s Government’s control.

He’s also noted debt as a percentage of GDP is similar to what it was after the Canterbury earthquakes.

Debt is expected to peak at 35% of GDP in 2024.

Credit ratings agency, S&P is comfortable with this, saying, there is “ample headroom within the current rating to address potential shocks, aided by its economic and fiscal recovery”.

"New Zealand's economy is robust and outperforming many peers, in our view," S&P said.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

82 Comments

It's a pitty Robertson spent all the money in the wrong places & ways...now look where we are.

Rings a bell.That story, way back in the primmers , the dutch boy with his thumb in the dyke.

I dunno, I thought the $10 million on bungee elastic was a great use of tax payers money.

Hopefully the government is considering and assessing the likelihood of a residential construction sector fall away in 2022 and 2023.

In two ways.

Firstly, in terms of the general health of the economy and employment.

Secondly, what a fall away would mean in terms of sector capacity. There's a risk that the same thing that happened in the wake of the GFC will happen again - a whole lot of capacity lost, companies folding, construction workers heading overseas etc. - then a sector being back to square one.

A wise and prepared government would be preparing for this by developing a massive backlog of consented (but not built) housing projects. If the private market collapses, damage limitation can be achieved with redeployment into 'shovel ready' social housing projects.

The Ministry of Works also used to play a role here in both pipeline of delivery and - crucially - smoothing the supply pipeline of skilled people. Training them followed by 2 years each in 3 different projects or disciplines.

The Reserve Bank is going to continue to pay lip service only to inflation.

The Labour Party is going to restart mass immigration from non first world countries to suppress wages.

If you have New Zealand dollars convert them to sound money or commodities as soon as possible.

Going to be hard to have mass immigration with Omicron...

Omicron won't be news by March.

Lol dreaming

Wrong. You are failing to math.

He's correct if you follow the math.

A polymath might suggest beware the Ides of March

Brock could be correct. We'll have shifted another couple of letters down the alphabet by then ;-)

I disagree.

While the signs are it is less severe, it's also highly infectious and I think we will see community transmission in the first few months of the year and the usual risk averse approach from the government with further lockdowns. Not saying that is the right approach, but that is what I think will happen.

Hopefully omicron is the start of the end, but we can't be sure of that.

It takes about two months from seed case to every single person in the country exposed when cases double every two days.

It will be not news in the rest of the world by March. It will be over and done with.

You're right about locally. God knows what idiotic path Jacinda will take to try to delay the inevitable.

Yeah, I mean locally.

Hopefully Omicron is Omega?

Yes and right now we have a lot of people leaving. Over 9,000 more people have left than arrived this month so far according to customs data.

Where are this mass of immigrants going to live and cheap labour are you suggesting minimum wage is going to stop. After this variant another will pop up , I also think a lot of people will be leaving for Australia as prospects for young couples are better for them ie housing cost wages higher.

Omicron or no omicron but didn't labour promise no Immigration when they came to power?

If people in NZ can work from anywhere on the modern connected world, then they can also hire anyone anywhere in time world and can deliver inherit products. There is no major need for IT guys to be in country. It's a different situation for bar servers, uber drivers, porters and laborers.

I guess we want to immigration for unskilled rather than skilled.

Skilled can work from anywhere these days. Just need a good internet connection and willingness to do the work.

It has always seemed strange to me that the Government didn't use the Pandemic as an opportunity to let the economy cool off somewhat. They could have filled up excess capacity with a massive infrastructure spend that would be transformational and not inflationary. Now they are trying to improve infrastructure and the private sector has taken the bulk of the capacity to build. Its like no one understands the concept that Govt spending should increase in a down turn, to reduce the scale of the down turn and ensure there is certainty for the construction and associated sectors. Now they have spent a lot with little to show for it and are about to spend a whole lot more in an overheated economy.

Agreed, instead consumers propped up the economy after Covid hit through the "wealth affect" of higher house prices and helicopter money used to buy consumer goods made offshore.

First year business Uni students would do a better job,

Always wondered why politicians, and not macro economists were posted as finance ministers.

Seemed the priority was always keeping housing up. A two-tier welfare scheme and a massive injection of Reserve Bank support to keep it so...just happened to over inflate the market too.

The quotes from the bank economists in this article are like a top ten of misinformed, self-interested, neoliberal, nonsense.

“Further, high rates of inflation tend to hurt poorer people more, meaning some of the benefit of high fiscal outgoings is being offset. We’re certainly not saying the Government should stop helping those in need, but we are highlighting that the economic landscape has changed.”

Nonsense. Inflation hurts people with financial assets the most. It is uncomplicated - if you have ten million dollars of financial assets and inflation is 5%, you have lost half a million dollars of purchasing power in a year. Meanwhile someone on minimum wage has seen (and will see) near-inflation level increases in earnings and will rarely have any savings at all. Who has been impacted the most? Could it be the people that the bankers care about the most?

“If the Government is not rebuilding fiscal buffers during the peak of the cycle, they will have less ammunition at the bottom,”

Nonsense. if we have learned one thing during the last two years it is that fiscal space is not an issue for sovereign governments. Lots of other countries have debt to GDP three to four times higher than ours - and when Govt does increase spending in times of crisis, we have seen how quickly that spending comes back as tax revenue.

"ANZ economists said financing spending using these funds will add liquidity to the financial system, which should put downward pressure on short-term interest rates and bond yields “at the margin”. Remember, the RBNZ is trying to lift rates to cool inflation"

Nonsense. let me translate.... "When Govt spends from the surplus in the Crown Settlement Account, we get even more cash in our institutional settlement accounts - this cash only earns crappy OCR rates of interest. We would rather swap the $37bn we already have earning OCR for juicy Govt bonds that we can sell for a tidy profit "

“Add the costs of an ageing population and climate change (which, alongside the housing crisis, are goliath challenges from an intergenerational inequality perspective), and it’s easy to conclude that in the absence of some fiscal constraint today, taxes as a share of GDP can only go one way in the future; up!”

Nonsense. The solution to the challenges posed by our ageing population, climate change, housing etc is to invest the real resources in the things we need today so that we can meet those challenges tomorrow.

“On top of the cyclical position, there are other good reasons to put fiscal settings under the microscope. Households and the Government have taken on a lot of debt recently. That debt will carry a lasting legacy, and leave us all exposed to higher interest rate risk."

Nonsense. Firstly, Govt liabilities are non-Govt assets - so if Govt liabilities have gone up, then non-Govt assets must have increased. And, they have. Household net financial wealth is now at a staggering $1.1 trillion. The challenge is not household debt per se - it is how wealth and debt is distributed. https://www.rbnz.govt.nz/statistics/c21

Don't even get me started on that stupid debt graph. Who would assess their financial health by looking only at their 'liabilities'? It's like looking at a Jeff Bezos credit card bill or mortgage statement and concluding that poor old Jeff is financial trouble.

Nonsense. Inflation hurts people with financial assets the most. It is uncomplicated - if you have ten million dollars of financial assets and inflation is 5%, you have lost half a million dollars of purchasing power in a year. Meanwhile someone on minimum wage has seen (and will see) near-inflation level increases in earnings and will rarely have any savings at all. Who has been impacted the most? Could it be the people that the bankers care about the most?

Get what you're saying but isn't the intent of the 'inflation hurts the poor harder' message about how 5% inflation to a poor person has a greater impact in that their already stretched finances can mean significantly more difficult conditions when they face the 5% inflation haircut ie less food, shelter, warmth. Whereas, for someone that has $10m of financial assets, they're crying in their second Mercedes - not third Mercedes - about inflation impacting their wealth?

Agreed. Lots of strange stuff there from Jfoe. Poor people spend whatever they have on life's necessities like food, shelter, power, and water. Just because that monetary value is less than a 1%ers' assets falling $500K is beside the point. The impacts on the former are most definitely more important.

Hey, don't get me wrong. I am always going to side with those that have been left behind but I get wound up when bank economists pretend that their concerns about inflation are driven by a sudden concern for the poor and unfortunate. I prefer to look at the 'what and who' of price increases before deciding that one group is more affected than another.

People on low wages have seen wage increases of 3.5% to 4% over the last 12 months (skill level 5 LCI and minimum wage). This is more than food price increases (2.7%) housing costs (2.6%), stock rental costs (3.2%) and a bit below increases in passenger transport costs (4.2% - noting fuel cost increase). I am not saying that people on low wages are not doing it tough - but their income has risen broadly in line with the cost of things that have (a) increased in price the most and / or (b) the things that make up the bulk of their spending. If prices do stay high, and the labour market stays tight, wages will have to rise to meet both pressures. In other similar periods of history, this has led to larger increases to lower wages and the reduction of wage inequalities. What I am saying is that inflation is not necessarily the enemy of the poor!

The wealthiest people in NZ on the other hand are sat on significant financial assets, which are being is devaluing at a rate that they will find uncomfortable. Similarly, the banks have significant liquidity at the moment - $37 billion in cash earning OCR for example. Again, inflation is devaluing these piles of cash. So, ask yourself, are the banks concerned about inflation because of the impact on the poor?!?

I get wound up when bank economists pretend that their concerns about inflation are driven by a sudden concern for the poor and unfortunate

Oh yes. So do I.

Being more explicit about what the central banks and govts have done to protect asset prices might also help change sentiment - a headline such as:

"Value of pensioners' savings massively eroded as their wealth transferred to property investors"

Household net financial wealth is now at a staggering $1.1 trillion

Do you mean 'non-housing' related financial wealth? Remember, the bubble is the be-all-and-end-all and is the result of the commercial banks lending into existence for non-GDP qualifying assets.

Yes, I mean financial assets (pension funds, shares, equities etc). Net housing and land wealth is another $1.1 trillion or so on top of that. NZ Household net wealth in total is a cool $2.3 trillion (about $600k per adult).

As you note, housing and financial asset classes are both grossly inflated. However, financial wealth will reduce as the value of shares falls as quantitative easing tapers out in many countries. People holding financial assets will therefore face losses in the value of those assets and inflation. This is one of the reasons I do not see housing and land values dropping significantly next year - where else would you put your money?.

QE will never taper out.

Interesting views, to say the least. I will address the inflation one.

Nonsense. Inflation hurts people with financial assets the most. It is uncomplicated - if you have ten million dollars of financial assets and inflation is 5%, you have lost half a million dollars of purchasing power in a year. Meanwhile someone on minimum wage has seen (and will see) near-inflation level increases in earnings and will rarely have any savings at all. Who has been impacted the most? Could it be the people that the bankers care about the most?

Wrong. Inflation is the phenomenon of your currency being able to purchase less goods for the same price in the future. Because it has lost value (due to dilution from money printing) then it appears that the cost (or price) of goods has gone up.

Now if you are a rich person and had $10,000,000 in CASH then yes, 5% inflation hurts you a lot, to the tune of $500,000 to be exact, as that is how much purchasing power you have lost.

But do rich people have their life savings in cash? No, they have it all invested in ASSETS. That is because, if you cash is loosing value, you get rid of it as fast as you can, and where do you put it? into assets that are scarce, or that are likely to go up in price because people think they have value (such as the stock market). And because assets are a safe haven to maintain your value/purchasing power, the prices of assets go up FASTER than inflation. Look at the stock market (S&P500 up 24% ytd) property (also 20%+) Bitcoin (150%+). So does 5% inflation affect them if all of their assets have gone up 20% in value??????? NO.

Now a poor person:

Has a preset salary, usually for a small amount less than 100k say. This may get increased once or twice a year if they are lucky, and it may match the rate of CPI inflation (or maybe not). So 1) they have had to eat the increased costs between the pay increases 2) everyone has a personal inflation rate and because they spend a higher portion of their expenses on living costs such as food or housing, this is more than likely to be above the official CPI rate (closer to 10-15%).

Because they spend all their free cash flow on basic living costs, they get hit the hardest by price increases.

A rich person might spend 100k a year on living costs for example, and this might increase to 120k. But as this is only 1% of net worth, the 20k increase in costs only represents a .2% increase in living expenses.

Where as a poor person might spend 50k a year on expenses (or 50% of their income) and if that increases even by only 5k, that is still 5% increase to them. Ergo, a 5% increase compared to a .2% increase as a portion of available funds hurts poor people a lot more.

They are also less likely to have any sort of financial assets as they have less savings, and dont have the inclination to risk the small amount they have managed to save. So all of their savings are in 0% yielding cash and so are getting wacked. So as you said, "they rarely have any savings at all" that can keep up with or outpace inflation so they are literally going backwards.

You need to distinguish between where the rich and poor people have their savings. Is it in financial assets that increase in value faster than inflation, and cash savings that is getting devalued by money printer go BRRRR.

Also go and google the Cantillon effect and why those that get the fresh money first can spend it before the rest of the population even knows it is in circulation and prices havent accounted for it yet.

Brilliant nail on head

Because it has lost value (due to dilution from money printing) then it appears that the cost (or price) of goods has gone up

I nearly stopped reading at 'dilution from money printing' - that theory has died a hundred horrible deaths and still people try and resurrect the corpse.

I agree with you on your property assets point - but even with our stupidly inflated housing market, half of household financial wealth is in financial assets. The value of those financial assets will come DOWN in the next year or so as QE subsides. Everyone thought QE was pumping up house prices, but anyone who understands the mechanism will tell you that it is share / financial asset prices that get inflated by QE. Set an alarm for this time next year and let's re-start this conversation.

Cantillon effect and Blackrock!

I read the first one and that was about as far as I could go. It missed a key point as everyone does when trying to push an agenda. Anyone with 10 million in cash would lose 5% purchasing power with a 5% inflation year.. But if you are in fixed assets, those are the very things that are inflating along with the CPI. I believe if the assets were property, you would have made 25% gross approximately, A very different situation from the person saving for his first house or other big purchase, who is getting pinged 5% at least and 25% if he is saving for a house. Now if you are trying to differentiate between financial assets,(bonds, savings etc) then the statement is accurate... but anyone with 10 million in cash has fixed assets(gold silver houses, art) so they net off in a far better position than the poor or the saver.

Absolutely. I was just about having kittens by the third banker’s predictably neoclass myopic assessment. Do you live/ work in Wellington?

“Tempting as it might be, pumping up Government spending risks driving inflation even higher. The RBNZ would then have to work harder to cool the economy and raise interest rates more aggressively”

We had a decade of low inflation/rates and we did nothing productive with the opportunity. Now we need to build out a "green" economy which will include major infrastructure like renewable generation, charging infrastructure on every street, electrified light and high speed rail to serve cities. Government just needs to get it done at any cost.

Have you ever used rail in NZ? It is vulnerable to rain (landslips), wind (trees and power cables falling), earthquakes (lines bending), heat (tracks expanding and warping), lightning strikes (take out sub stations). If it isn't already installed it is cost prohibitive to create new corridors (Public Works Act requires land to be purchased). NZ doesn't have the population density for rail to be a viable option. That's why we're seeing headlines like "Government issues 7.1m of press releases but builds 0m of light rail track"

...get it done at any cost

Think about it for a second. The Auckland light rail is expected to cost $6k per metre of track. Would you be comfortable with $20k per metre of track? $6k/m isn't a perfect metric, but it still gives me the heeby jeebies.

Mill Road at its last re-cost was set to be $3.5 billion for 21.5kms of road, and Judith was still keen as mustard to proceed with that. That's an almost $163,000 cost per metre, which makes $6,000 per metre for rail look incredibly cheap in comparison, one 27th the cost.

There's certainly no reason not to be improving our existing rail network - and intensifying significantly around it - or considering rail (or a suitable mass alternative) in existing available corridor space. Individual car trips will need to reduce over time. Not saying the present proposed light rail is a good idea, just that we need mass transit and intensification as a more cost-effective approach than sprawl and roads.

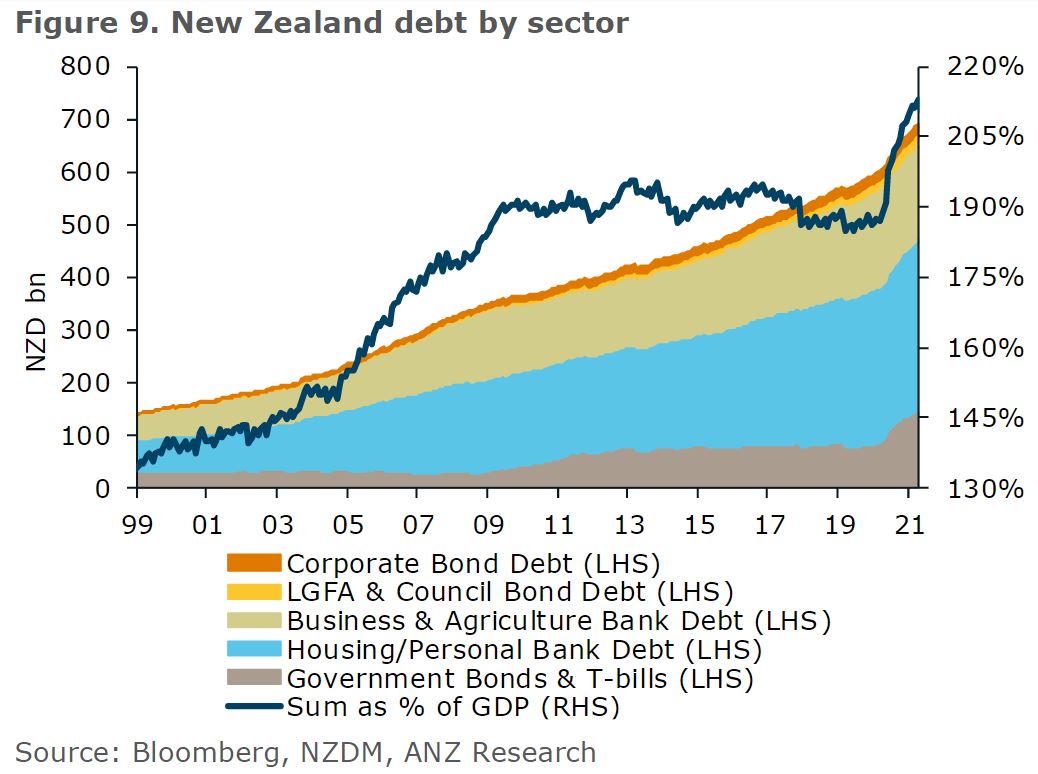

That's an impressive run-up in debt by a range of sectors. The government's share is relatively small for now.

I expect when the wheels fall off the housing/ business/ agro sectors, the government will then take over as the largest indebted sector through bailouts, unemployment benefits, and outright fiscal stimulus.

It will then have to default somehow as there are simply not enough easily obtainable resources or net energy to keep this economy growing above the rate of debt accumulation.

NZ is not alone in this regard.

I think the wheels have already fallen off the housing sector. 1 house sold, 17 Passed In. High brook room 1 B&T today.

Now at 1 sold, 23 passed-in.

Be quick!

Be quick indeed!

Houses selling like hotcakes, and you know, house prices *never* go down.

Now is always the best time to buy blah blah blah blah blah blah...

Inflation is a form of default for governments.

NZD tanking again this is going to exacerbate inflation. The interest rates should be raise so we don’t lose purchase power of NZD . This will be another crisis they did not see happening .

Yep. Unintended consequences. There's a lot of exceptionalism expressed around NZD. And the ol' "it'll fatten our export receipts." To be honest, I think exports are important but in the context of the NZ economy they've become a side gig to the bubble.

ANZ economists commented “it’s easy to conclude that in the absence of some fiscal constraint today, taxes as a share of GDP can only go one way in the future; up!”

This conclusion highlights that the government’s plan is to increase taxes as a % of NZ’s productive output. Why isn’t this ringing alarm bells?

This short-term gain / long-term pain financial model says NZ can tax its way to economic prosperity rather than grow the economy.

Give me one example where this type of model has worked?

This short-term gain / long-term pain financial model says NZ can tax its way to economic prosperity rather than grow the economy.

Pretty similar to how we've become dependent on inflating asset prices and essentially passing costs of our "economic prosperity" to the future rather than growing the economy.

Both are false and run out of runway if we're not actually doing something productive to grow the pie.

Can't tax productive work more either...most of the wealth has already been transferred to assets (especially houses).

Just stop investing in infrastructure and stop building homes. That should stall the economy, keep inflation in check, and also serve their ultimate purpose of boosting house prices!

"New Zealand's economy is robust and outperforming many peers, in our view," S&P said.

hehe, the Kiwi Tiger Economy;

We also have Kiwi chicks: This wiki article from 2027 explains:

~noun Kiwi Chicks: The name given to children born during the boom years in Aotearoa (the country formally known as New Zealand) Reference to a generation of Kiwis born in the boom years just prior to 2021, who were raised in a period of economic abundance fueled by debt. A generation apart, they have grown up with a strong sense of entitlement, privilage and consumerism. This contrasts with the Kiwis urge to ascend through struggle. With the debt crisis of late, they have been left adrift in a world of hardship they cannot comprehend. And have no experience to draw on that the generations before them and those following will have in simply making do.

Tiger economy or a feral cat......

Looking through some graphs online the historic relationship between the OCR and CPI over the last 20 years is very interesting. Focusing only on the occasions where CPI was >4% the OCR was as follows:

2000 = 5.75

2006 = 7.25

2008 = 8.25

2011 = 3.0

2021 = .75

I know its a simple comparison and there are a lot of variables but I find those numbers quite alarming in that our current trajectory is taking inflation well above anything that we experienced in the examples above. The CPI is currently sitting around the 2008 level but we have an OCR of .75 as opposed to 8.25 in 2008.

"Real inflation". The increase in the cost of goods and services + the change in asset prices / incomes will be the worst in many people's lifetimes.

Debt is expected to peak at 35% of GDP in 2024.

Credit ratings agency, S&P is comfortable with this, saying, there is “ample headroom within the current rating to address potential shocks, aided by its economic and fiscal recovery”.

"New Zealand's economy is robust and outperforming many peers, in our view," S&P said.

This government has failed on a number of fronts and as Matthew Hooton wrote, the failure to deliver on many key policies verges on the comical. However, criticisms on our debt levels from has beens like Steven Joyce and Bruce Cotterill are just ludicrous. Most countries would give their eye teeth for our debt/GDP level and our unemployment rate, not to mention our deaths from Covid.

And very little to show for it. Look at Japan. Huge public debt. But look at the infrastructure. And they're still a net creditor nation.

The problem might be pressure on the taxpayer to bail out speculators and banks, assuming massive debts. Of course, it should not be countenanced.

Meanwhile looks like the housing market is fading fast

30 houses in the Mangere region all under the hammer today and only 2 have sold . Making it a clearance rate of just 6%.

15 lots attracted no bids (50%). It seems there is a definite lack of buyers at the moment

The housing market is a goner - pure and simple.

I've been wrong about housing markets for 15+ years, so never say never.

However credit crunch appears more likely with this FCCA(?) new legislation. For example just tried to apply for a $1k limit credit card with my bank of 25+ years (on line purchases, separate from other existing credit card). I applied on-line but the robot had "carefully considered and declined my application". I spoke to a real person but the hoops that they wanted me to jump through and know all my expenses in a 30 minute interview was just ridiculous. I gave up and said I just can't be bothered and got a debit card instead.

Yet, I have no debt and a good track record plus sizable liquid savings. I actually used to work for the bank and credit was pretty much my role for 27 years in finance industry so I have a good idea that I am good for it!

I reckon the CCCFA is massive.

Whether it was actually designed, slyly, to knock the stockings off housing (and take pressure off the OCR tool) or not, it looks like it is...

Watch this space.

Yes, as I previously commented, politicians had to walk back this similar legislation in Australia (after the findings in the "Hayne Royal Commission" prompted it) as it was causing real problems with their housing bubble (on brink of bursting). UBS study also suggests a fair amount of lying on loan applications in Oz too.

It’s bloody frustrating when they won’t lend to you even though there is no risk to them because you have like 70% equity. Meanwhile some PI has 30 houses and no income but that is OK.

I had a similar experience yesterday, seeking a small increase to a credit card limit, not happening.

Oh well, just dug a bit more into my reserves.

Things appear to have changed at the ASB. I used to just login and move a "Slider" up and down to adjust my credit limit online. Adding another $1000 was not a problem. Cannot seem to find that function anymore.

That feature wouldn't be able to be used with CCCFA, they need to evidence that you can afford the increase...

Holy crap you’re right! Maybe they should be able to do a one off financial competency test instead of assuming everyone is a moron and can’t control their own lives.

I suspect alot of kiwis wouldn't pass the test

There's a side people don't focus on - When prices are rocketing up, logic says you should jump in when you can. So you do, and you ride the wave up, and leave savers far behind. But the thing is, if a market downturn occurs, you'll have nobody to sell to if you need to sell. So it's not just savers who suffer, it's recent buyers who find themselves with no safety net.

For instance, I'm a saver who has been left behind. Prices will need to drop 50% before I have a chance at buying.

Total of all B&T Auckland auctions today. 10 properties sold out of 76 listed. 13% sale rate. There are going to be a few hungry real estate agents this Christmas. The poor things don’t even get minimum wage.

What's the bet there is no coverage of this in the Herald / One Roof over the next few days.

Wouldn't want to spoil the illusion just on the doorstep of Xmas, would we now?

It is strange isn’t it. It would be an easy and interesting story but they choose not to report it. It’s almost as if they have a vested interest. I really enjoy listening to Heather Du Plessis Allan on ZB, but it does frustrate me that when she comments on the housing market, she never informs listeners that both her mother and her brother are B&T real estate agents. I have not heard her report any negative news on the subject.

They're talking about it now, maybe trying to make vendors more realistic for agents... https://www.oneroof.co.nz/news/passed-in-passed-in-passed-in-bidders-di…

I love the spin. “Vendors who would have made $1 million are now making $750k which is still good money”. They don’t mention the poor buggers who bought in the last month who must have lost $250 000 if this statement is correct.

They've only lost money if they're planning on selling again quickly.

That's from 4 days ago which was better than today...will be fascinating to see if they report today and if so how they spin it.

"This always happens leading up to Christmas" or "It's been a long year, kiwis are thinking about other things and will be back into it in the new year"

So even after covid our debt is only 35% of GDP! That is quite impressive, it must be very low by world standards.

I think having a focus on percentage of debt without understanding what you have done with the debt is misleading...... Debt at 35% of GDP and a massive infrastructure deficit in New Zealand.

"ANZ economists Sharon Zollner, Miles Workman, David Croy and Finn Robinson recognised there are still people in desperate need of government support. But they worried elevated expenditure in a capacity constrained economy risks raising prices at a time the Reserve Bank (RBNZ) is lifting interest rates to try to put a lid on inflation."

You have to laugh (if you didnt youd slit your throat)....the bank's greed has created the problem and now they want saving....fuck em

I find it hilarious that they think he has a tough gig....

When the RBNZ printed $100billion in the first place and supported QE for years... and then start worrying about the inevitable inflation that would occur as a direct result

What else do you expect when you print money like crazy?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.