Last year saw a significant improvement in affordability for first home buyers, allowing more of them to realise their dream of home ownership.

The improvement in affordability in 2024 was driven by three factors: declining mortgage interest rates, rising incomes and relatively flat house prices at the bottom of the market.

On their own, each of those factors may not have been that significant, but taken together they had a noticeable impact on affordability.

Prices flat at the bottom of the market

Interest.co.nz tracks the Real Estate Institute of New Zealand's lower quartile selling price each month.

That is the price point at which 25% of sales are below and 75% are above, representing the bottom end of the market that's the most affordable.

The lower quartile price typically bounces around, either up or down by a few thousand dollars each month. But over the course of 2024 it was remarkably flat, remaining between $570,000 and $607,500.

That was little different from 2023, when the lower quartile price stayed within the range of $567,000 and $600,000.

That suggests relatively stable prices, giving buyers the confidence to take their time to find the property that best suits their needs, without the urgency caused by rapidly rising prices.

Mortgage rates slide

Buyers would have benefitted significantly from falling interest rates in 2024.

The average of the two-year fixed rates offered by the major banks declined from 6.98% in December 2023 to 5.53% in December 2024.

The national lower quartile selling price was $586,000 in December 2023, and the mortgage payments on a home purchased at that price with a 10% deposit would have been around $908 a week with the mortgage rate at 6.98%.

If the home had been purchased with a 20% deposit the payments would have been around $718 a week.

In December 2024, the lower quartile price was $599,000, and the mortgage payments on a house purchased at that price with a 10% deposit would have been around $805 a week. That's a saving of $103 a week compared to a year earlier, even though the purchase price had increased slightly.

If the home was purchased with a 20% deposit the mortgage payments would have been around $630 a week, making the buyer about $88 a week better off compared to a year earlier.

Rising wages

As well as benefiting from steady prices and lower interest rates, first home buyers would also have likely benefitted from modestly rising wages.

Interest.co.nz estimates the average after-tax pay for a couple aged 25-29 and both working full time would have been about $2064 a week in December 2023.

By December 2024 it is estimated their after-tax pay would have increased to $2128 a week, helped along by a tax cut in the middle of the year.

That left them with an extra $64 a week in their pockets compared to the end of 2023.

That extra money, combined with the cheaper mortgage payments meant someone buying a home at the lower quartile price with a 10% deposit, would have been $167 a week better off in December 2024 compared to December 2023, and $152 a week better off they purchased with a 20% deposit.

So although 2024 was a year of challenges on many fronts, the fundamentals of home home ownership were in buyers' favour last year.

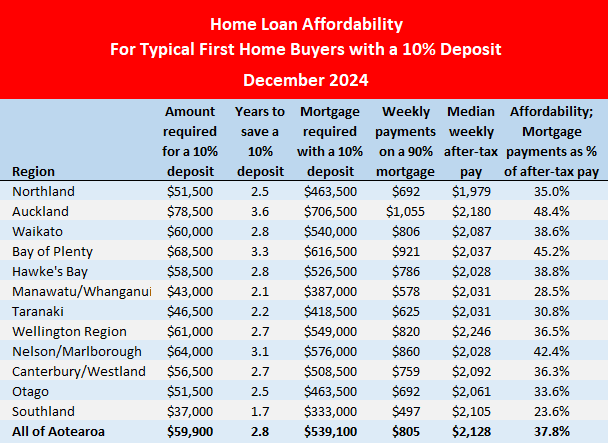

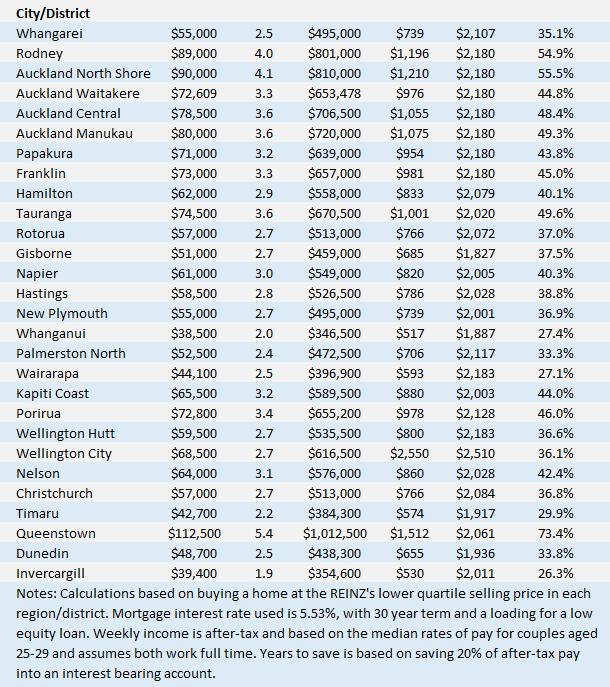

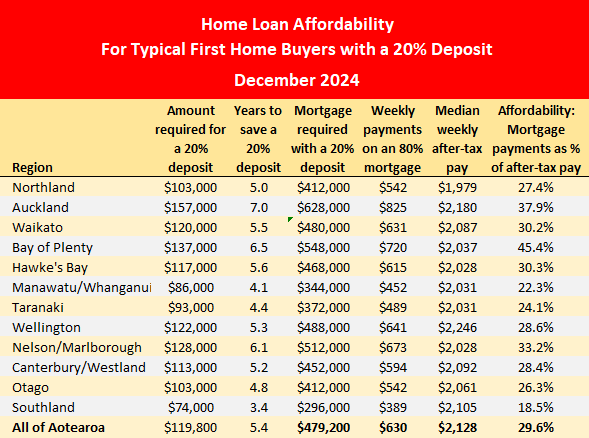

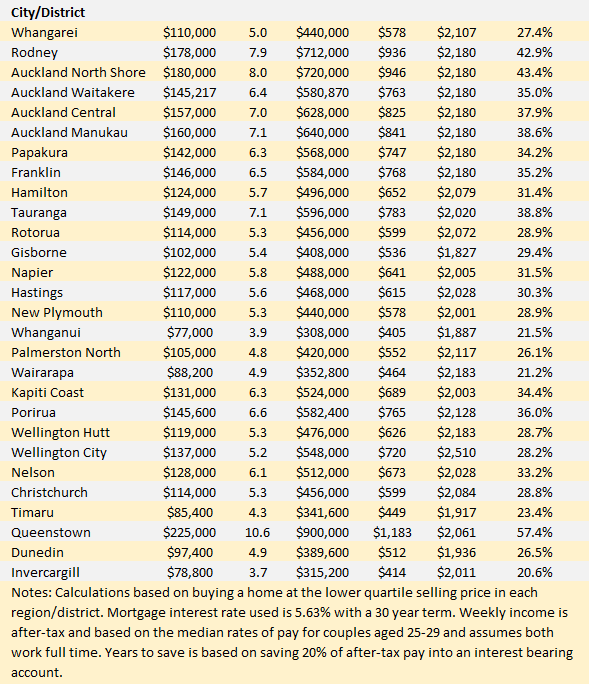

The tables below show the main affordability measures for typical first home buyers with either a 10% or 20% deposit in all major urban districts in December 2024.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

156 Comments

That's going to send the DGM's fizzing more than the Champagne.

It is such a shame that the first comment on an article like this is more often than not this pointless, childish drivel.

More of a case that the DGM's are a pretty sick bunch who cannot be happy for FHB.

Good to see FHBs realising their home ownership dreams.

TTP

Imagine how happy and dreamy NZ would be if housing was affordable.

Maybe our best and brightest would return to NZ rather then going offshore to achieve their housing dreams.

That is the dream, that is the dream. Imagine having your kids living in their country of birth and not having to move overseas to seek a better quality of life.

More of a case that you can’t admit that you got your views wrong so need to belittle and ridicule those who were right with childish terms like doom gloom merchant.

Zwifty has the Spruiker sickness pretty bad...

Lets face it, with the worst FHB situation in the OECD, could we expect that stats to get worse?

Not sure about that, just looking at OECD countries.

Switzerland, Portugal, United States, the Netherlands, and Canada all have higher house price to income ratios https://www.oecd.org/en/data/indicators/housing-prices.html?oecdcontrol…

So 6th worst, Australia is not far behind us at 9th.

I’ve realised DGM is a term used by people who can’t handle being wrong about anything - and then admitting they were wrong. Ie very low self confidence and almost no humility.

Instead of saying ‘wow I got it wrong those last few years and those I disagreed with weee right’ they have to belittle and ridicule those who were correct in order to avoid facing up to their own shortcomings.

(I don’t use either spruiker nor DGM terms as I don’t think they add anything to the quality of this forum - but each to their own as we each reap what we sow - ridiculing your enemy instead of showing them respect has a tendency to backfire in the long run as we all get things wrong are are never perfect in our views. I think this forum would be much better if both term were removed).

.

For example and to admit my own wrongs, I thought house prices were very expensive in 2015 and couldn’t imagine them getting to the extremes they did in the subsequent years to a peak in 2021. I was wrong. My views were not correct and those who were bullish at that time were right.

My views aren’t always right but I’m not going to call people DGMs or spruikers if I disagree with them and feel free to call me out and call me a hypocrite if I ever do going forward. Being wrong seems to be a good way to grow in humility as it is painful.

You don't have a deep-seated fear of being wrong, losing status or feeling inadequate. Calling people DGM or Spruiker is just a crutch to lean on when they can't form a solid argument.

Yes. I feel like owning your failures or admitting when you are wrong is a very important skill but seems to be rapidly disappearing from society. I work hard to instill it in my kids, but it certainly doesn't seem like is as widely encouraged as when I was a kid?

Because we seem to be living in a period of time where people like to ‘own’ the dominant narrative (or propaganda) in matters and bend reality towards their own selfish interests by silencing or ridiculing their opponents that disagree with them (and risk ruining the selfish/self serving narrative they are creating) - instead of seeking what is honest and truthful by being open minded about things.

To admit you are wrong means giving your opponents the opportunity to say ‘see they were wrong so listen to me because I am always right’. Eg those who are bullish on property (for their of self serving financial interest) spend their time ridiculing anyone who risks destroying their narrative that house prices always go up or double every 10 years (so ‘be quick’) by calling them doom gloom merchants - and people are afraid of being seen in a negative light by others, even in the pursuit of what is good and what is true. It’s a sad indictment of where we are at as a society. Definitely not the society I remember 20+ years ago where seeking what was true and what was good was greater than focusing on creating propaganda or narratives that best suited your own selfish interests. Eg ‘I have a housing portfolio so anyone who wants my net worth to drop is a negative person and must be a doom gloom merchant’ - instead of asking ‘is having such expensive housing relative to our incomes a good thing for the people of our nation going forward and if not, how do we correct that and am I culpable in the creation of that problem’.

We could call them "The group that cheers when interest rates rise" or TGTCWIRR for short, but it doesn't have the same ring to it. Do you have any good suggestions for a name? By the way, I don't think people here (except you) see it as a term of ridicule, but maybe I am wrong.

"Do you have any good suggestions for a name?"

Property price bears vs property price bulls

Bulls and bears are descriptions used in the share market.

Exactly - but when it comes to property, unless you are bullish you are full of doom and gloom

Why do we need to give view points childish names? Instead we could just argue positions without the name calling.

Why do we have left and right in politics? Why do we call Green Party supporters Greenies? Why do we call a dog a dog and a cat a cat? We name things, that's just what we do. It's not childish, it just is what it is. Does the commenter called Dgm feel ridiculed by being called a DGM? I doubt it.

There's names, labels that enable communication, and there's name-calling with a derogatory or negative energy.

There can be a distinct and substantial effect on the recipient depending on the tone and emotion used when delivering words.

It gets missed in text conversations, which leaves intent up to each reader, and how the labels or words are predominantly used.

The written word is great for communicating information, especially the English language as it's very technical. But it's useless for real communication, which includes many nonverbal cues.

It's why social media and even forums like these can have a more detrimental effect.

These are some good points you are making there.

Here is a thought exercise. Based upon your logic I could just reply to all your comments and call you ‘Tron the Retard’

It’s just a name right and I’ll use it day after day, week after week, month after month. Tron the Retard, it’s just name…who cares?

’Why would anyone listen to what Tron the Retard has to say? He’s just a retard’ Just as people constantly comment ‘who cares about what the doom merchants think, they’re just negative people..such DGMs’

Of course I won’t do this because I chose to respect you and be respectful to you. Are people who constantly call other people doom gloom merchants on a daily basis practising this respect in a mutual fashion? And if they chose not to be respectful to other people, why would anyone ever respect them in return? I have no respect for anyone in this site who calls other people doom merchants (or spruiker) repeatedly and endlessly as clearly they have no respect for themselves or others around them - I actually feel sorry for them that they have to drop that low in the manner in which they choose to conduct themselves (it’s what people with low self esteem/confidence do). If you respect yourself you have respect towards other people and it’s occurs in a reciprocating fashion.

But you are basically saying none of this matters - or to hell with having respect for anyone..we can call each other whatever childish names we like and there are no consequences - yes there are - a significant drop in social cohesion and peoples respect for themselves and respect for others. Basically how to try going about being a decent person.

Retard is a derogatory term, whereas the terms doom and gloom are not.

I do think we should have respect for each other, and like I said earlier, if you want to use a different term for those who want interest rates to rise to 10% and property to drop a further 35%, then be my guest.

I will call left wing people "lefties" and green party supporters "Greenies" - are you ok with that?

Calling someone a Doom and Gloom Merchant is still by definition derogatory. You'd have to be pretty thin skinned to be upset by it though.

Why aren't you calling someone a "rightie"?

I won't call anyone a greenie or leftie.

1. because of how both labels are predominantly used. They create separation and division which is political BS, and

2. is also a lack of respect if they haven't given consent to be called a particular name.

House prices were very expensive in 2015, just as they were in 2008, so you weren't wrong.

Not imagining them going higher and outright saying they won't are distinctively different. Thinking and/or suggesting that it might not be a good idea that they go higher doesn't make you wrong either.

Philosophy and wisdom teachings give an interesting perspective on the concept of right and wrong.

There's many reasons one may not be willing or able to admit they made a mistake. Ego and pride for sure, and one is putting themselves in a very vulnerable position and that requires strength.

The other nuance and probably the most difficult for humans is acknowledging if you have wronged another, based on their perspective.

Ideally, being wrong shouldn't be painful. That can suggest an unconscious hurt from a past experience if one was mistreated for being wrong.

The other side of humility is when one may have been right, is not to brag and boast about how right they were, to tell others how wrong they were.

The spruikers will applaud them for that comment

Zwifter 'it's OK to shoot a 7 year old in the head' chief cheerleader has spoken.

The Spruiker camp can count this type of person as their ally

They are all complicit in trying to destroy Israel right down to the 7 year old throwing rocks that got shot in the head by the IDF.*

*Zwifter in the breakfast briefing.

Zwifter must've had a much higher than normal exposure to lead based products as a child to come up with that tripe.

Zwifter have a read of my post further down. Been a great day hope you are enjoying the sun were you are stunning day here in Queenstown

"Weekly income after tax and based on the median rates of pay for couples aged 25-29 and assumes both work full time"

> So no babies/children during the prime childbearing years.

> If there are offspring then add the cost of childcare into the equation; assuming it is less cost than the gain from the additional salary.

Anyone else see a problem with this?

And don't even mention student loans, but at least they can withdraw their Kiwisaver funds to get on the ladder. (And probably realise Super will be the last rung the boomers pull up before they retire off planet).

Yeah - Good points I was also about to make. Young couple with children and one of the income is pretty much done. Using such income data is misleading.

The median age for a FHB is also like 35 in NZ now

And most marriages don't last.

anecdotally financial pressure is an aggravating factor

High housing cost = high mortgage payments = higher pressure to work in more stressful, high paying jobs to afford said mortgage. Add in much higher pressure on the one working parent if a child comes along, then pressure to earn more to support the family. Add in how WFF doesn;t abate earnings dollar for dollar, higher cost of living, and we wonder why marriage has a greater fail-rate than in the past when.....housing wasn't a major issue.

At 35, most women will be having kids while still renting. Forty years ago, it was normal to buy a family home at 24 on a single income, with the wife having the choice to be a full-time mum. Happier wife, Happier kids, happier life.

Better to have them while renting. Dont have to worry about how to pay the mortgage when mum is off on maternity leave. Then when she's back at work, can apply for a mortgage and go buy a house.

With current rents, and the cost of a child, which scenario do you think allows a couple to save a deposit fastest and be more financially secure in the long term?

1./ Save hard with a dual income while renting, with greater flexibility and mobility, then purchase a property and have a child after, knowing your financial position with the fixed costs to work on (which coincidentially have increased greatly in the last couple of years)

or

2./ Have a child while renting, and the associated cost of a child, lose a lot of one income as parental leave payments are peanuts compared to what so many women earn, struggle with finances of a single income, only to discover that you barely make any more money from her going back to work as the cost of childcare is so high.

If the price of housing and rent stagnated for several years, and income increased with inflation then yes your suggestion may make sense.

Even better to have them at a time when society allowed a single wage to buy a house and feed a family in one's early 20's. No need for this maternity leave nonsense.

Things have changed though Kraker…we were raised in the 80’s with mum at home while us kids were preschool age…basic house, me & the older bro shared a room with bunks, one bathroom, one car, no mobile phones, one TV, the annual holiday was camping at the beach, the clothes were handed down through the family…we did not go with out by any means so don’t get me wrong, but shit it’s different now when I look at families…it’s impossible to disagree that house prices are mental & have made it immensely harder…but income creep & the lifestyle changes that follow also need to be taken into account as well 🤷🏻♂️

Possibly, but sometimes it seems we get the lifestyle creep elements a bit wrong too.

E.g. a phone today is for many a phone, computer, a stereo/radio and a camera. In the 1980s folks had separate ones (and/or a typewriter too).

China has made clothes incredibly cheap since then, and same with tvs, phones etc, especially if buying second hand.

Fish and chips pretty comparable (we had often on a Friday night), pizza much cheaper. A large Pizza Hutt pizza back then was the equivalent of about $50 now.

I completely forgot about the fish n chips on a Friday!

Fair call Rick, those are all good valid points, I guess I look at our life, & think my sons have no idea what it was like only one generation ago. If we made a change to live like that I think we could possibly get by on the one income…but it would seem like an Amish lifestyle to them 😂😂

Don't worry. The govt is still fully incentivising beneficiaries to pop out kids while forever living in state housing.

Not to mention that beneficiaries have access to free dental care, all the while, NZ kids are supposed to have free dental up to 18 years old (but dentists won't see them as they make way more profit from baby boomers).

The govt have no problem paying full market price for beneficiaries to have fillings and root canals, yet wont pay the same for kids.

No rates, power, insurance or maintenance either.

Hi Greg, is there anywhere I can download historical quartile level data for free?

Would be an interesting article looking at the different quarters and how they are performing, most articles talk mediums and averages, which hide a lot of distortions. many boomers would be interested in what's happening in the highest 2 quartiles, even the MAN in CHCH would probably be interested.

Compared with many trading markets, housing data here seems to be very very hard to get, what is the cheapest source of all sales per month across NZ?

This is the sort of article that helps put PDKs frustration with in economists into some sort of perspective. It ignores all the peripheral things, things that are really at the heart of affordability and sustainability as alluded to in comments above and concentrates really on affordability on a single given week.

Much like how we treat the environment.

$1/2m is rediculous for a bottom tier house, but it's "affordable" and that's all that counts.

I bought a villa in Ponsonby about 2003 for under 500k, it was a solid 4 bd rm one, not a wreck. It was on summer street.

That's how much housing inflation has destroyed the NZers purchasing power.

I'm sure more than 1 person will want to call me a DGM but these figures don't exactly make it attractive to buy a home IMO. Ownership costs so much higher than renting, FHBs seem to not always realise most of their mortgage payments in the first few years are interest and they are only paying down their loans by very small %s. Add to this flat or falling house prices and a tendency to overpay to get on the ladder means they are not building up equity. I don't see it as sustainable.

Yes and still listings flooding onto the market (at least on my Trademe watch list) while interest rates are falling and the asking prices dropping on a daily basis on my trademe notifications.

Why buy now if you think the house will be cheaper in 6 months?

So in Auckland half disposable income has to go on your mortgage - crazy - why young are better off starting off somewhere else as the numbers don't work in Auckland

In actual fact the numbers (income compared to house prices) in Auckland don't work for those at most stages in life

Be nice if RBNZ told us the deposit data for FHB (maybe they do and I'm too lazy to find the right series)?

Our bank told us only 20% deposit was available a a FHB 2 years ago - I wonder how that's changed?

C30 has < 11% of mortgage lending with <20% deposit. (By value, why can't they do by count, sheesh).

Edit:C31, 40% of FHB lending was LVR > 80%.

Interest.co.nz continues to show SBS term investment rates as if they were term deposits. They are preference shares that are much riskier. South Canterbury Finance preference shares were not bailed out. 5.35% is for 6 months is not a TD. Sorry for being off topic.

The SBS is a very stable and successful bank with a sound balance sheet and P and L.

South canturbury finance can't really be compared - good on Bill English for calling out South Canterbury Finance for what it was

Yes acknowledged SBS is a much stronger entity. It's a registered bank. But 5.35% for 6 months is NOT a term deposit. Preference shares aren't the same as a term deposit.

So why does SBS not offer TDs? Are preference shares in an unsecured deposit category?

Very good point. And I am not sure that preference shares will be guaranteed by the incoming depositor compensation scheme.

I've been saying this for a while but many more "experienced investors" here can't understand, even though they are the ones who benefited from the unaffordable increase in the 1st place. They are out of touch.

From 2018-2022 house prices were so unaffordable and lending so strict that it was not possible for many to buy a house to live in. Now we are in a position that a single income person can buy a lower quartile property with a DTI ratio of less than 5.

2 incomes... DTI ratios of 3. i get 2 incomes is not an ideal situation to rely on, but 1 income is more than manageable for moderately educated people with decent financial management.

I could understand there are exceptions to this. Just saying.

Do you mean - a single income above 150kpa - or <3% of people (and a lot above that are derived from already existing portfolios, so not exactly FHB types)?

Nope, 90Kpa. Quite common.

550k house with 20% deposit. 440k loan.

Those numbers do work, yes.

$1274 income vs $572 repayment/week.

What were the outgoings while saving that $110k deposit though, and how long to achieve? Assuming 30% saved after tax - 288 weeks, or almost 6 years. So, no children then.

Note 90k is top 13% income - so a little better - 1in 6 people. I will bet dollars to donuts a much lower % of young have that level of income (Note the figure given by interest equates to 64k without student loan repayments).

Annoyingly though, I searched on TradeMe for max 550k - and half the results do not match my max price criteria! Seems like a really easy thing to get right, so can only assume either TradeMe or sellers are desperate for listing views.

What does $550k get you now though? 1 bed apartment? As per IT mans comment above, 4bed villa in ponsonby 2003 less than $500k. Nuts. Immigration much to fast. 2003-2019.

What would the relative equivalent cost be today though adding cumulative inflation across the time passed since?

90k incomes are not as common as you think.

Also 550k is like what, a 2bd run down bungalow in Manurewa?

AKL is not a good place for a single income to buy a first home, it is unreasonable to expect that

Things will always be the same in that a percentage will never be in a position financially or else they do not have the attitude or are able to do what it takes to buy a house. Too many over think it, you just get in and start paying a mortgage and in 10 years time its like wow, thank god I did that instead of renting.

There is a little thing called a banking cartel gate-keeping who gets to participate.

This article is speculative drivel about what it may take to get in, based on stats that have been pointed out time and again not to apply to the real world. But they won't update their FHB profile to match real FHBs.

[Edit: just remembered- didn't your parents give you a considerable sum towards your deposit?]

If things double from here debt be 5-600 billion and monthly interest 3-3.4 Bil, where will 3.4Bil a month come from Zwifty?

or do you not consider the required funding to expand this Ponzi anymore....

Incomes would have to increase at the same pace ie 7.2% per annum, how will the RBNZ hold inflation at 2% with incomes rising at 7%?

The Spruiker sickness is impacting your ability to model the required banking environment for a double to occur.

The more likely situation is that Property in NZ falls back towards OECD norms, its called reversion to the mean. Did you study Stats or Finance at Uni?

"Reversion to the mean" is a statistical concept that states that if a variable is significantly far from its average value (mean), it is likely to move closer to that average value in subsequent measurements, meaning extreme events tend to be followed by less extreme ones; essentially, a system will naturally return to its typical pattern after a deviation.

Exactly, the key driver that allowed annual house price growth of 7% with genre inflation and incomes growing around 2% was decades of falling interest rates.

If rates don’t fall mathematically that growth isn’t possible as the discounted future cash flows don’t add up in higher future prices. Certainly not 7% growth on a long term basis. It worked from 1980’s - 2020’s in the biggest drop in global interest rates seen in centuries or even thousands of year ( No exaggeration)

If you are living in a home and renting - you can afford a home as YOU are paying for it. The problems is you pay for it but don't get get legal title.

Sounds a rip off - of course it is.

The affordability to buy a home issue is based on tax and lending structures - not on one's income. If you can pay the rent you have the income.

Traditionally, but many rentals are currently well cash flow negative, landlords have been topping up because the capital gains have made it worthwhile. They believe that Capital gains will return, this belief structure we be well challenged over the coming decade as they continue to subsidize their renters lifestyle.

Without capital gains, topping up is dead money.

Its why investors are not snapping up bargains here. As The Comb says, they cannot make the numbers work.

Yes basing their strategy on an old model. These things work fine when a limited number of people have worked out the strategy. Once the masses pile in it continues for a while as a ponzi and then collapses. The smart money have moved on - if I knew to what I'd join them!

Clearly its not transferring their wealth into "productive" NZ Investment... to achieve "Growth, growth , growth"

Sometimes the best thing to be in is something that just holds its ground, and wait for opportunities, Buffet is reportedly high cash right now, though it will be in short term something. Treasuries are great as they could be lent or sold instantly as required due to liquidity.

Their are some some great funds such as

https://milfordasset.com/funds-performance/balanced-fund

10 Year Fund Return

118.78 %

as at 31 Dec 2024

(After fees and before tax)

Ta. I'm mostly in cash but decent amount in equities. If I find the right property then it might be house land and water. Then the markets can do what they want and i will live as a peasant!

Maybe someone has the numbers, but Milford has seemed pretty solid to me. I've often wondered what they invest in, mind.

My wife's KS is with them, and if I recall correctly, they were the only KS provider during the first 4 years of KS to achieve a positive return for their clients (over the GFC).

NZ KS providers are all pretty solid, Milford and Fisher have a longer record of good returns. If you have a mil or more give Jarden a ring.

There is a lot out there, many property nuts are so hot on it because the banks will lend on there existing equity to fund more property but will not lend on anything else. The CFD guys like CMC Markets, Saxo etc will leverage on anything but i do suggest you know what you are doing.

There are leveraged ETFs if that's your fancy. You can lose everything. You can loose everything in housing with leverage as well.

Definitely won't find that affordability in AKL or TGA to be fair.

My girls are more likely to move from Auckland to Melbourne then out of AKL to an NZ Region....

Its no good pointing at the affordability of our regions if there are no aspirational jobs in these locations, they are cheaper then Auckland for that very reason. We cannot fix this , our kids will keep leaving and that action and removing themselves from the buying pool will in time set of the correct solution.

Today is a great day. Sold one house in Christchurch today. The tenant wanted to buy it we cut out the Real Estate Agent she got a 4brm home for 475k about 30k below valuation. She sent me a thankyou text saying how I helped her (single mum) and her kids realise their dream of owning their own home and helping them thru the process of it with time and paitence. There is always demand for homes in the no collar suburbs. Owned this one 5 years brought as a mortgagee sale brought it up to healhty homes standard so it provided a house to a tenant for 5 yrs an now a first home. Now I could have sat around bemoaning how bad things were how the govt needed to do this or the economy is going to do that or interest rates will do that. Or only evil people buy rentals etc etc. Maybe you that knock people like me need start backing up with action rather than wasting your life looking at a screen

What is a no collar suburb?

He means cheap, though in my office people code in T Shirts and ripped jeans...

An old concept that a suit and tie meant something.

White collar is flash (or think they are) Blue collar middle management like a safe secure job.

No collar is tradies non qualified jobs

Professionals - white collar (reference to shirt worn with a suit). Skilled or semi-skilled workers - blue collar (reference to shirt worn with pants/jeans). Beneficiaries - no collar (dont work at all, wear pyjamas all day).

Beneficiaries...clutch gold card, take up seats in buses and very slow to get off.

No one is knocking you Colin. It's the ones that buy, do nothing and then expect to make big cap gains from no effort or value added.

This^

While expecting the working plebs to pay the taxes so they don't have to.

Rastus but they do. From a former PM all the way done but predominantly they are people that want something for nothing or the govt to give to them. At the rate I am going I will build more homes by my own hands that Tywford/Adern did with the ehole kiwibuild fiasco

Hence the problem. During the mad phase you could probably make more just flipping multiple props with a quick tidy and dodgy cosmetic. Now you need to real improvements - so you model still works, old one not so much.

That doesn't happen very often at all.

I would suggest that investors that make money on buy and sells normally put extra money into the property and improves it.

They should be commended for putting the money up and improving the quality of housing.

From what I see there are so many people that either own or rent houses that are just lazy and dont do a lot of improving of their property.

You only need to drive around and see how many just let their lawns grow long and dont bother to spray the lawn or garden weeds.

Just as well not everyone thinks and lives like you otherwise there would be no need for rentals or buy/sells. Just as well you have lazy people in Christchurch who you can rent or sell to. If there wasn’t you would only own your home. Or so you say.

I am not just talking about tenants, Ex Agent.

There are heaps of owner occupiers and many immigrants that think that dandelions are pretty flowers in their lawn and clover is good for the bees.

What I firmly believe is that those that look after their own property well are more likely to be successful in life.

Isn’t is wonderful you had the capital/cash 5 years ago to buy another home as a do it up. Not everyone does. And up to 2021 house prices and the required deposit were regularly rising faster than people’s wages - meaning people who already own property could release their equity to buy even more property (like yourself) and make themselves even wealthier! While others sat in the sideline getting depressed as their wages were getting destroyed by their price inflation in housing and their interest in their savings was getting decimated by low interest rates and taxation - while property skyrocketed and in most cases no capital taxation to be paid.

I understand your point Colin and well done for exploiting the situation for your own financial gain - but it isn’t you who we need to worry about. It is those who wanted to by but couldn’t and who have decided to leave instead - that is the problem. Great that you’ve help your tenant to get into a home.

Yes us boomers have been lucky with prices and timing. It does however mean many of us need to help our children to get on the ladder. I am happy to do just that.

Who you calling boomer aint no where close ti that.

You forgot one thing Work. Had to climb under a floor .300 space with mould on the joists and liquid faction while putting insulation and mositure barrier down. Since the previous owners left a leak running so the ground was drenched. Plenty of cat and rat s...t to roll around in. And lot of other things most people wouldnt do

Don't forget the spider webs! (PS. I've done it too, but never on my own house as deposit requirements rose during the 2010s faster than we could save as our rents also rose).

Well done Colin - 10/10 for effort and I’m sure the new owner appreciates your work in improving the property,

Yes we know you worked hard. All boomers say that. First home buyers work hard also and face well over 3 times income loans when they buy their first home. You would not have.

Again I anit a boomer. Year born for boomers 1946 to 64. And i am 1970s so aint a boomer. And the first house I brought was 18 percent interest. But I didnt waste my money on buying lunckmhrs coffees everyday or flash new phones or clothes just today brought two new business shits to wear on site in the heat flom the sallies. So much opportunities out there just get out of Auckland

You certainly talk like the average boomer. I worked hard. I didn’t waste money. Interest rates were high etc etc. My interest rate peaked around 20.5 in 96/97 but only for a few months. My loan was around 100k then and it was on the home I bought in 96 and am still in it. Worth around $3m now. Shit the boomers and X have been very fortunate.

Christ now its how you talk. Maybe because I got kicked out home at 15 an half left school and ended up managing a dairy herd very young. Got told by mother dont come to me for anything. Maybe the younger generation need a bit of that

The more you talk the more you sound like a grumpy old boomer. The young ones today face far bigger hurdles than you ever did. You never had a 10 times income loan. You had it easy Colin. Assets were cheap, the cost of living was low and loans were small.

Yeah right. Any excuse you can find . Cant even find it in yourself to say great what you did. So lets see what you do for someone most probably not alot just looking for the excuse why you cant

Don’t fool yourself old fella. You did it for the dollars not for her. You sold her an expensive shit box in a shit area. She will have a ten times income loan something you have never had. You are part of the reason why property is so expensive in NZ. For the record I retired in my late 50’s and I help a number of charities with governance and voluntary work. Unpaid of course.

" You did it for the dollars not for her."

There are a number of profit motivated people and businesses who attempt to position themselves as doing a public service or public good to be seen in better light by the general public. The property investor's association (i.e lobby for property investors) has repeated this narrative to it's members.

Imagine if the privately owned supermarkets in NZ claimed that they do a great public service by providing food to households.

So tell me, CN-new, what you do?

What did I do?

I highlighted the difference between a benevolent enterprise and a profit motivated enterprise attempting to masquerade itself as a benevolent enterprise via spin.

What is the primary motivation of the activity? Profits or benevolence? One is selfish and the other is selfless.

So says an ex agent

I am no more an ex agent than you are a benevolent investor Colin.

@ ex-agent

"I help a number of charities with governance and voluntary work".

Good for you, ex agent. Now can you stop bullying Colin with statements such as "you are part of the reason why property is so expensive in New Zealand" cos it isn't true. As he said, he isn't a boomer, but it seems that you are, and have made millions from property.

By the way, your boasting about charity work sounds a bit narcissistic.

He sounds very rational to me Tron, someone working with charities narcissist? Pot calling kettle?

It's the boasting, Baywatch. People who do good works shouldn't have any need to boast about them.

If ex agent is such a good person, why are they persistently attacking Colin Cameron on the forum?

It's the boasting, Baywatch. People who do good works shouldn't have any need to boast about them.

You could apply that to Colin as well, he didn't need to come on this forum to say 'Today is a great day, sold one house today ....

Colin has a chip on his shoulder as well 'White collar is flash (or think they are)'. Plenty of people do valuable work whether it be on screens, driving trucks, voluntary work etc, valuable work is not just done by boomers who build houses.

You are very immature for an experienced investor and so called grandad, you don't sound easy to be around, I hope that's not the case...

Colin inferred I do nothing for others. I simply outlined what I actually do to help out as I have a lot of spare time. If that makes me a narcissist I would hate to meet a real one.

Ex Agent, you are talking rubbish!

Far easier nowadays to borrow and buy and do up and sell, and repeat!

On average there would be 5x the profit in a renovation than what there was say 10 years ago.

It is all about attitude, work ethic and knowledge, and if

you have not got that then yes, you will not go forward financially.

I could start out now with very little and become financially wealthy inside 5 years, but probably not from being in Auckland!

You aren't a boomer? Are you sure about that Colin because you and I exchanged some commentary a few months back and you commented you were in your 50's.After that exchange I remembered you commenting that you used your actual name on this forum and could be found online, so find you online I did and if you're not a boomer then I'm the RB Guv'nor. Good on you for building/renovating homes but be honest about your age and advantage of being a builder and being in the game a long time.

So what age is the youngest boomer at 1964 which is the end of the boomer era. 60. Now if born 70 what age coming up would i be earlymid 50s.

I know someone who has this and got off having to do healthy homes as the "floors were too low". They then proceeded to up the rent $150 per week between tenants. The place wouldn't keep 17 degrees in winter with a blowing southerly when the heat pump was maxed out.

Yeah but thats not me

Never asserted it was 🙂

You seem to have this preconception that all young people are afraid to get their hands dirty doing some DIY on an entry level property. What you're talking about is nothing special, I've done plenty of renovations on both my first home and current home. Under the floors, in the roof space. Not something you'd expect a war medal for doing.

Spent 4 hours last weekend grinding down a concrete pad in our kitchen where the old fireplace was, to make the salvaged Rimu flooring we picked up sit flush with the rest of the Rimu flooring that was hidden under 2 layers of Vinyl/Underlay and 1 layer of tiles on top. The triple skinned brick fire place with a 200mm thick concrete lintel filled with 16mm rebar starters at 100mm centers I knocked out 6 months ago.

I'm not even a tradesperson I smash a keyboard for work every day. I have plenty of friends who own homes that are doing their own DIY projects and also aren't in trades.

The difference being Colin that you produce houses also, and do most of the work yourself. Many investors pay a property manager, don't upkeep houses and find ways around healthy homes obligations, charge max rent, and want a pretty profit on sale thinking they have done tenants a favour.

Colin, your property mustve been on the East Side and in pretty poor condition to let it go for $475k?

Aranui average price range 505k for suburb as said i took 30k off. As didnt use agent. I made good the tenant/buyer made good everybody a winner.

Thought it mustve been Aranui or close.

The prices have climbed significantly ver there in recent years.

I dont normally like to deal on the East Side of ChCh but have and % profit margins are rather attractive.

Discussion with Ex Agent tends to be a waste if time, as he has a huge chip on his shoulder and is a passive investor supposedly rather than a hands on doer.

He goes on about retiring in his late 50’s which I wouldnt do.

Too much fun and money to be made after that, but if he is happy not contributing financially to the country then so be it!

Obviously you do not have enough capital to be able to retire with and are jealous . I am not surprised as you continue to rely on poor old Christchurch residential property to get ahead. Why would I waste my time mucking around with shitty old houses when I have more than enough to retire well resourced capital and income wise.

Correct, personally own very little Ex agent.

As for property investment in ChCh it is without doubt the best market to be working in and that continues to be proven.

Anyway stick to your TD’s you will become very wealthy and bitter.

Thanks for acknowledging I am wealthy. Thirty years of looking after clients certainly paid off. I started investing for retirement as soon as I started working. The last 11 years have gone by so quickly just confirming that the sooner you retire the better off you will be. Your health is your wealth. No one dies wishing they had worked harder or longer than they needed to.

"personally own very little"

Does that mean that most of your assets are owned in trusts and other entities?

So use your Kiwisaver to pay the 10% deposit and then pay 38% of your wage in repayments. That sounds easier then when I bought my first home 18 years ago!

And that is at 5.53%. Westpac will give you 4.99% for 3 years.

Office of the Prime Minister, 2011 (re: 2006):

Rising prices have contributed to lower home ownership rates and constrained the housing market choices available to a growing group of New Zealanders

All measures of affordability have declined. By 2006, only 29% of renting couples and 2% of renting non-partnered individuals, with both groups including those people with and without children, could afford to buy a lower-quartile-price house in their region, and pay a maximum of 30% of their income in mortgage repayments. At current incomes and interest rates, even small falls in prices are unlikely to make a marked change in affordability. There is a growing group that cannot afford a mortgage on a house and is ineligible for state housing assistance

And note at that time, HPI was 6 (compared to 7 now, and 10 in 2021), and you could still get a 5% deposit.

Looking at the graphs is grim reading - something changed in ~1999/2000 and we jumped very quickly from HPI of 3 to 6. Millennial and beyond were quite literally screwed over by Helen Clarke's Labour government, and no one has wanted to fix it since.

This sounds so crazy now, but there was a point when Westpac would lend 105% of the purchase price for FHBers so they could buy a furniture package.... (terms and conditions applied). I think it was around 2005-7.

Yeah. Countrywide also offered 100% mortgages in the mid-90s before they were bought by National.

I was young and dumb ( I admit it) - I could have been like some of my peers and bought a house with no deposit, a DTI of 1.5 and had flatmates in to pay the mortgage - but I knew nothing at all about finances when I left school. (I earned well but spent better).

"I was young and dumb ( I admit it)"

Everyone is born into the world young and dumb, however every adult has the choice to become older and wiser or older and dumb.

The most difficult learning is being sufficiently curious, open minded, combined with critical thinking skills to learn to undertake paradigm shifts (i.e. unlearning previously held beliefs / ideas and replacing them with new learnings). Here are some examples of mantras repeated frequently and marketed by those with their vested self interests which were commonly believed by most of the general public leading up to peak property prices in NZ in 2021:

1) house prices double every 10 years

2) you can never lose with property

3) house prices don't go down by much

4) buying is better than renting

5) owning your own home is better than paying your landlord's mortgage

6) they're not making more land, and there is population growth

Here are some more:

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_pid=IE79655584

"but I knew nothing at all about finances when I left school. (I earned well but spent better)."

Financial literacy is low amongst the general public and even lower with certain cultures. Most people are unaware of their ignorance, and just don't know what they don't know.

If these figures and percentages were for one person it would be acceptable but alas it’s for a couple and still way over valued market,wait a year or two save thousands over the years.

Much to celebrate? I am sure that for many there would have been a sense of relief, but they are still having to pay absurd prices for the privilege of getting their own home. They are now shackled to mortgage payments that for most will eat much of their combined incomes. I am old-almost 80- and when I and all my friends bought, we were able to find properties at 3 times our income and our wives did not have to work, though almost all did, but stopped when children came along.

Now a second income is essential and the children have to be farmed out very early on. I am certainly not saying that everything was better in the old days, but somethings really were better in my view.

Exactly and many of the new Mums I know (now age 35-40) are extremely stressed, often suffering from burnout or chronic fatgue, a number are the primary household earner (as more girls than guys go to uni now), don’t really have the energy or capacity to deal properly with the kinds when they get home as their heads are elsewhere (or vice versa can’t be fully focused at work as they are worried about the kids), and a number are on antidepressants because of the strain they are under.

"we were able to find properties at 3 times our income and our wives did not have to work, "

Relatives working in a bank in the late 1980's told me that mortgages at the time were limited to 2-3 times household income (when it was mostly a one income household).

Lots of people had to get a second mortgage.

‘Much to celebrate ?’

Exactly, tone deaf headline

Good time to be looking/buying but too damn hot out there and I am lazy…

Now if only we had built a ton of brand new family homes for First Home Buyers to buy, instead of tiny 2 bedroom shoeboxes with half kitchens, no storage, no yards and no garage. Instead we built cheap and crappy townhouses designed to be sold to investors and rented to people who just got off a plane with nothing but a suitcase - except that there are fewer investors and fewer people getting off planes. But they still take up all the precious space in suburbs endowed with good schools and other child friendly facilities - all going to waste as these properties sit unsold and unoccupied on the market. Meanwhile we force FHB out to the far flung suburbs where there are no good schools or child friendly facilities. What an upside down state of affairs.

They will get sold and occupied. Many renters consider them a step up from traditional uninsulated, old fashioned, high upkeep NZ homes.

Those old homes made great flats. Rent a room for $150 a week. Young people could afford to move out of home and start adulting. Those townhouses are about $300 a room. Young adults are stuck at home with their parents until they're 30+ and become DINKs and can afford to move into a townhouse.

"Young adults are stuck at home with their parents until they're 30+ "

A consequence of housing unaffordability - in both the ownership market and the rental market.

Other consequences of housing unaffordability that people may not see:

1) average age of couples having children is increasing

2) average age of first home buyers is increasing

3) increasing number of households requiring accommodation supplements (and impact on government financial resources for other areas of government spending such as healthcare, infrastructure, social housing, etc)

4) increasing number of households requiring social housing

5) falling rates of home ownership over the long term

6) increasing wealth disparity between those who are born into families with financial resources and those without financial resources

So wages rising , affordability improving , prices flat , an extra $64 to squirrel , 3 to 10 years to save that deposit depending on where you want to live... and thats where the problem is I think , How many actually have the 20% deposit ? If the answer is not many ,if any ...Then it could be some time before the dead sea rises....lol

"How many dudes you know ,roll like this? ("Scribe" 'Not many', remix ... )

Not mentioned here, but the unemployment rate for those aged 25-29 has increased from 4.1% in Dec 2023 to 4.7% in Dec 2024 and was up to 5.8% in the June 2024 quarter. It is unlikely to have been a good time to buy for those that lost jobs last year.

Re Home Loan Affordability...Wonder how many over 60s easily have say a 30% deposit but cannot get a mortgage due to inability to complete the mortgage by say 75 ... Against this, What is the likelihood of house prices plunging negative 30%? Ive met a few older (60plus) motorhome lifestylers that have capital but dont want all of it drained into an excessive house deposit ...Yet many of them probably would be in a more equitable position on the banks books if they took out a mortgage today than some that bought during the FOMO era... Are banks just happy to have Capital tied up in TD's with older clients ? .... Maybe they need to be a tad more creative in their offerings towards those that have capital parked because it seems to me that with a 30% deposit the loan would be Low risk , Is it even necessary for the older lender to be scheduled to make a final payment because as we know many that play the market often complete payment on sale before purchasing another property ? For example 'Old Bob' rents but has 350k locked in a TD ... Should it not be possible for 'Old Bob' to whack down say 225k as a deposit and make his normal rent payments or clear his mortgage via sale ? Seems low risk to me....Thoughts anyone , because my guess is the bank will want all of his TD as a deposit...and that just seems likely why some older folk that have capital dont want to play in the sandpit...lol

because it seems to me that with a 30% deposit the loan would be Low risk

Sometimes old people disassociate with reality and forget to pay bills, I saw it with my own mother.

Banks hate negative publicity, throwing families or old people out of a home is not a good look. They are not just wary of credit risk, its reputational risk as well.

Banks hate negative publicity, throwing families or old people out of a home is not a good look. They are not just wary of credit risk, its reputational risk as well.

Funny how they don't want to get the publicity for throwing people out who have not been able to service their debt, even though it is their job to assess risk and cut losses when it gets too bad. They want to be reputable, reliable, trustworthy and able to fun peoples dreams, but don't want to be seen to be managing risk appropriately by calling in debt and showing that they are being logical instead of extending and pretending.

That headline is a bit tone deaf

Good news for NZ Inc.

But only in the very short term. (i.e. 6 months)

If 'investors' aren't subject to to the same DTI & LVR rules rules that owner occupiers are ... - ideally more restrictive - ...

Then is is just a blip. And a destructive one at that !!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.