New Zealand's house prices will rise by a "modest" 4% over the coming year and by 6% in 2026, independent global economic researchers Capital Economics (CE) predict.

CE's Head of Asia-Pacific Marcel Thieliant says the recovery of the NZ housing market will be "muted" even though CE's expecting the Reserve Bank will slash the Official Cash Rate (OCR) all the way down to 2.25% in 2025. It's currently at 4.75%.

"While we expect the RBNZ to cut interest rates by the most since the GFC over the coming year, housing affordability was never as stretched at the start of an easing cycle as it was at the start of the current one," Thieliant said.

"Accordingly, we only expect house prices to rise by a modest 4% over the coming year and by 6% in 2026. A housing market rebound will boost consumer spending and dwellings investment and put some upward pressure on inflation. However, that won’t prevent the RBNZ from slashing rates."

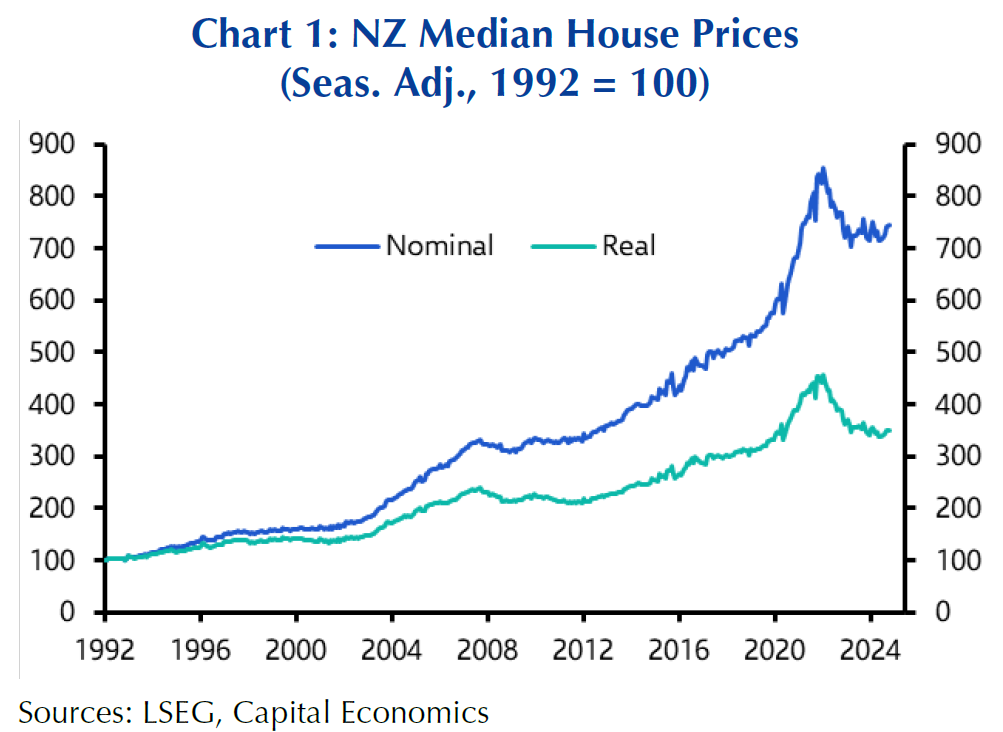

Thieliant said New Zealand’s house prices "have been on a rollercoaster ride" as they surged by nearly 50% between end-2019 and their peak in 2021 and then plunged by nearly 20% as the RBNZ lifted the OCR to 5.5%.

"Since early-2023, house prices have moved sideways even as home sales have rebounded a bit and mortgage rates have already fallen by more than 1%-pt," he said.

"If we’re right that the RBNZ will slash the OCR by 325bp [basis points] from its peak, housing affordability should improve dramatically.

"However, arguably the best indicator of the strength of any housing rebound during a monetary easing cycle is housing affordability at the onset of that cycle. Unfortunately, mortgage payments relative to household incomes were never higher at the start of an easing cycle as they were at the start of the current one."

Thieliant said another headwind to the housing market is the sharp slowdown in net migration, which has fallen below pre-pandemic levels in recent months.

"With the unemployment rate set to remain higher than in neighbouring Australia for the foreseeable future and the government having tightened immigration rules, population growth will probably remain muted."

He said the Coalition Government had "admittedly" made it more attractive for investors to purchase rental property.

"But investors only account for one-fifth of total home purchases and the available data suggest that any boost to investor demand resulting from the policy changes has already happened."

Thieliant said the "bigger picture" is that the longer house prices remain flat, the more attractive housing valuations will become.

"We expect disposable income per employee to rise by around 4.5% this year. If that pace of income growth is sustained next year and in 2026 and house prices remain unchanged, the house price to income ratio would return to its 2019 average by late-2026.

"What’s more, our view that the RBNZ will slash the OCR from 4.75% now to 2.25% by the end of next year means that affordability should improve dramatically, too. This is illustrated by the dashed blue line in Chart 3, which illustrates a scenario in which interest rates and household incomes evolve in line with our forecasts and house prices don’t rise any further. In that case, housing affordability would have almost returned to its long-run average by the end of 2026, too."

111 Comments

Rather than 'muted ', more like gutted.. this is based on the ovr being at 2.25.. bet its going to be higher

Capital economics seems like a reputable company.

So not only will house prices rise, interest rates will be lower, win win.

I assume we could expect 1 year interest rates in the range of 3.75% with a 2.25% OCR.

Is a higher cost of living really a win?

What part of the article suggest higher cost of living?

this?

"We expect disposable income per employee to rise by around 4.5% this year.

/Sarc

I assume we could expect 1 year interest rates in the range of 3.75% with a 2.25% OCR

I don't see how that would be possible based on the past mortgage rates:

Related to OCR:

Past monetary policy decisions - Reserve Bank of New Zealand - Te Pūtea Matua

With a OCR of 2.25% you could expect 1 year interest rates to be around 5.0%

Unless banks reduce their margins this time, but methink the reality is they have already priced in future cuts, or the current lower margins are only temporary.

Current OCR is 4.75% and I just refixed for 1 year at 5.59%. I don't see how the OCR could be cut to less than half what it is now and yet we only see a half a point drop in retail rates. If the OCR goes to 2.25% you will see rates in the low 4's, possibly even high 3's.

Seems you didn't read my message. Since OCR has been created 25 years ago, we've never seen rates "in the low 4's, possibly even high 3's" with it at 2.25%. Historically the lower the OCR the wider the gap with mortgage rates.

But if you have details supporting this time things are/will be different please do share them with us.

Looking back over the last 20+ years, the average difference between the OCR and the 1-year fixed rate is about 2.25%.

https://www.opespartners.co.nz/mortgage/interest-rates/interest-rate-predictions

so maybe not as low as my initial 3.75% but closer to 4.5%

I do recall hearing somewhere the margin between the OCR and 1 year fixed being around 1.5%.

"The reported rates are simple average new standard mortgage rates advertised by registered banks in New Zealand"

Taking an average of advertised rates is not a good way to understand what rates are actually on offer. You may not be aware but there's a significant delta between the rates banks will advertise and what they're actually offering. At the time I fixed recently for 5.59%, the best 'advertised' offer was over 6% and many were well over that which drags the reported average up way beyond what customers are actually paying.

Notice that the first graph RBNZ rates you link uses Standard Rates, not the <80% LVR rates. It has the 2 yr rate at 6.29%, when really, for most borrowers the carded rate is more like 5.79%, and possibly lower if you negotiate. Thats 0.5-0.75% of the difference gone already looking at todays interest rates table here

yea I picked up on this too, I don't think the RBNZ provides an accurate representation of actual interest rates.

@RookieInvestor

"Capital economics seems like a reputable company.

So not only will house prices rise, interest rates will be lower, win win"

What a useless, unproductive comment.

You don't have anything to add to this comment section apart from mindless remarks...

i was pointing out that a company like capital economics is more reputable then a joe blog commenter.

Not just trying to insult people with different opinions by calling them morons.

"i was pointing out that a company like capital economics is more reputable then a joe blog commenter."

Not necessarily. You "perceive" a comment as being more reputable and valuable than from someone at a water cooler or a neighborhood BBQ.

But there's a big difference. With the latter, you are at least able to ask questions to go deeper or seek validation.

Why should I trust whatever the Vampire Squid or Jamie Dimon says just because of their power and "reputation"? First question you should ask yourself is whose interests are they working for. They may not be yours.

At times it seems like the whole point of the comments section is to have a dig at others...

Thieliant said New Zealand’s house prices "have been on a rollercoaster ride" as they surged by nearly 50% between end-2019 and their peak in 2021 and then plunged by nearly 20% as the RBNZ lifted the OCR to 5.5%.

That's a soft-landing .......

And signs of recovery are now emerging.

I hope interest rates don't fall too far or too fast. We can do without a continuation of the roller-coaster ride.

TTP

We've heard that one before.... re: % rise next year.

One of the key pillars of our housing marking is inability of the electorate to understand chart 3.

Yep. Pay mortgage/rent or feed self and children. Easy to see why youth are choosing to start in Straya.

That's the fundamental driving this but I think we can go further. The income interest rate multiple almost completely determines medium to long term house prices (and we know what this ratio is) and that we are currently well above this level.

The RBNZ used to have a similar chart going back into the 90s but I can't find it any more.

For those of us that don't know. Can you please explain further.

1) what is the "income interest rate multiple" and how do you calculate it?

2) "(and we know what this ratio is)" - what is the ratio referred to here? And how do you calculate the ratio?

Apologies, it's the income, inverse mortgage payment multiple. I simplified payments to rates.

The ratio is the dashed horizontal line on chart, 45%.

If you expand the values or units on the y-axis make them equal to ratio you can solve for house price, with algebra and the simplification. Without proper maths notation I don't think writing it out would help.

Remember that is based on gross household income. Think of the ratio of after tax household income.

I would think, such a high proportion of our taxes end up in housing that gross income is the correct metric to use.

Looking from a micro economic perpective and household level

Merely highlighting the percentage a median household income would need to spend on debt service to finance the purchase of a median priced home in recent years.

After tax deductions, and mortgage payments, how much is left for rates, insurance, maintenance? Then there are utilities such as electricity, gas. Then groceries and transportation. Nothing for leisure and entertainment activities.

Cripes what sort of state do they expect the economy to be in to go to 2.25?

I'll file this amongst the other crystal ball projections.

Yeah if things are that bad... just dropping the ocr won't be enough to save us.

That said.. I think things will be very bad for us.. and I am not sure there is much nz can do in the short term to recover.

If the govt don’t join the party with some fiscal stimulus then the OCR will need to be chopped big time…we are pretty screwed I think

"If the govt don’t join the party with some fiscal stimulus"

Is a tax cut considered fiscal stimulus?

The Budget 2024 tax relief package will cost $14.725 billion over 5 years to 2027/28

https://www.bdo.nz/en-nz/microsites/budget-2024/tax

$14.725 billion is approximately 3.6% of annual GDP

https://www.rbnz.govt.nz/statistics/series/economic-indicators/gross-do…

Perhaps the government could have spent the $14.725 billion more effectively?

Then there was also the $2.92 billion tax benefit given by the government to the non owner occupier owners of existing residential real estate.

That would total $17.645 bn over 5 years.

How were non-owner occupier owners given $2.92 billion tax benefit? That was money labour were planning to take off them and it wasn't a benefit it was restoring their right to pay tax on net profit just like every other income generating business does in NZ.

"How were non-owner occupier owners given $2.92 billion tax benefit? That was money labour were planning to take off them and it wasn't a benefit it was restoring their right to pay tax on net profit just like every other income generating business does in NZ. "

Yes that is the commonly repeated argument and juxtaposition used by those with their vested financial self interest to re-introduce interest deductibility and associated tax benefits. Perhaps there is an undisclosed vested financial self interest with the associated inherent bias?

It is a tax benefit to non owner occupier owners in the existing residential dwelling market compared to owner occupier buyers. Remember under the previous policy, interest deductibility was allowed by non owner occupier buyers in the new build market and social housing.

The two governments (current and previous) had different policy objectives:

1) the objective of the current government policy is to address issue of affordability by tenants in the RENTAL market

2) the objective of the previous government policy was to address the issues of affordability by owner occupier buyers in the existing residential dwelling OWNERSHIP market

Should ownership of an existing residential dwelling be given priority to

1) non owner occupier buyers?

2) owner occupier buyers?

Which should be the government policy objective? Does the country want more tenants or more owner occupier owners? Vested financial self interests will have their own preference due to their inherent bias.

What are the potential unintended consequences when prices are unaffordable in the existing residential dwelling OWNERSHIP market?

- lower rates of home ownership

- lower birth rates

- older average age of first home buyers

- higher housing insecurity for renters

- increased wealth inequality between asset owners and non asset owners

- concentration of ownership of residential real estate by a smaller proportion of owners https://www.stuff.co.nz/life-style/homed/housing-affordability/30041526…

- increased emigration out of NZ

Here are the two regulatory impact statements. Read the problem definition.

1) current government: https://www.treasury.govt.nz/sites/default/files/2024-07/ris-ird-ridrip…

2) previous government: https://www.taxpolicy.ird.govt.nz/-/media/project/ir/tp/publications/20…

This property in the existing dwelling market was purchased in the last couple of weeks by a non owner occupier and listed for rent. A first home buyer on a single income (a single mother) was outbid by the non owner occupier buyer.

https://www.realestate.co.nz/property/21-dampier-avenue-awapuni-palmers…

21 Dampier Ave, Awapuni, Palmerston North. Listed for rent at a 6.7% gross rental yield.

https://www.trademe.co.nz/property/residential-property-to-rent/auction…

Do people prefer to see the single mother as a tenant or as an owner occupier of this property?

This is the potential unintended consequences of the reintroduction of interest deductibility by the current government. If there was a zero interest deductibility policy that would have been phased in under the previous policy,

1. would the non owner occupier buyer have bought (and provided a public service as they claim)

2. would the single mother have been less likely to have been outbid?

From the regulatory impact statement - Page 13

"Restoring interest deductions for residential rental property is likely to put some upward pressure on property prices, making buying a first home somewhat less affordable"

https://www.treasury.govt.nz/sites/default/files/2024-07/ris-ird-ridrip…

Fiscal stimulus, monetary policy, either way we're still on the path of insanity, doing things the same way expecting a different result.

TPTB have a result in mind and it most likely does not align with the force fed masses, trained to align with the status quo, BAU indoctrination.

Cripes indeed....and 5% average income increases in that economy....heroic!

Some people think that interest rates in NZ are going to rise. 😂

Not 'Some people', most Central Banks are forecasting interest rates will be under pressure due to new US blanket tariff policies. NZ won't be an exception.

CM, it's hard for morons to understand that.. they would rather pass ignorant comments

What a useless, unproductive comment.

You don't have anything to add to this comment section apart from mindless remarks.

You had nothing to say to yvil's comment yesterday..

Shows what a gutless creep you are.. or are you yvil

.. won't be surprised

How many $ MIllions have you made from property through your "predictions", DGM ?

Why the heck would I tell you that.. I wouldn't bother asking you that.. knowing how much shit you talk..

Was the commenter above making a disguised attempted flex?

Personally I wouldn't go on public forum bragging about how many millions I have made from properties trading. I'd leave that to the financially insecure individuals.

Lol. Yip.

Why was Razor chosen as All Black's coach ? Because he's had lots of success coaching other teams. Why should we listen to financial advice from someone with no experience in making money like DGM?

You're not obliged to read my comments if it doesn't suit you.. just as many ignore the crap you keep posting

by Dgm | 20th Nov 24, 1:55pm 1732064135

"You're obliged to read my comments"

No I'm not, and this has nothing to do with giving advice which is more like an ignorant opinion on a topic one doesn't have any experience on. I wouldn't dare posting and giving advice on a cooking site, as I'm very aware of my own limitations in the kitchen.

and your list of experience, Yvil?

You are comparing apple vs kumquat here.. Razor has real proven achievements and is a public figure..

Here, all we have is some gloatings of success from some random strangers in some random websites..like "I have made 2 millions from selling in Riverhead"..

I am sure you are a wise investor and make your own investment decisions.. if you are based on the comments here, you are a bigger fool than I thought!

These comments are detracting from the overall value of the comments section.

"and your list of experience, Yvil?"

I'm a qualified Architect and I have owned my architectural business for 18 years in NZ. For the last 25 years, I have invested in mostly commercial Real Estate and some occasional residential and holiday Real Estate. Understanding interest rates is of utmost importance to me, as it drives yields and values as well as cashflow.

DHM, less than 24 hours, and interest rates have been cut by 0.5%. Are you man enough to apologise for calling me a moron for saying that rates are going down, not up ?

Hence 0.75 cut this wed :) - not just for homeowners and most NZ's remember **i speak under correction** housing is the 2nd biggest industry in NZ

I doubt it, I'm honestly expecting a 25 bps cut, rubbish economic and spending data over the summer period and a "panicked" 50 bps cut in February.

The RBNZ were slow to raise and screwed it up on the way up, you can expect them to be slow to cut and screw that up on the way down.

It doesn't help that the data they work off is rearward looking.

@theghost - you do have a point - the way i see it another timber plant is closing / manufacturing in NZ is laying of people up to 25 % of Staff - NZs back is broken - this once again is my opinion - its not to devide or anger anyone -

I think you're being unfair - they are also quite capable of cutting too fast and screwing it up that way.

@MFD "unfair" what did I do?

Don't worry, my comment was both a joke and not addressed to yours.

The Spruikers have called more bottoms then Freddy Mercury over the last 3 years.

Meanwhile our kids keep leaving for Sydney and Melbourne uni's.

For the Spruikers buying houses in South Auckland here, what is your exit strategy ?

My kids don't fancy South Auckland so as returning ex pats they are never your buyer. I guess you could turn them into townhouses to house the minimum wage workers? Can't see how the economics would work. I know developers who have had to move into prime city sites (Over 4k per sq m ) and sit it out waiting for funding to become cheaper and prices to recover.

Probably no exit strategy, just relying on Auck to become a reflection of the cities many have recently 'escaped' to NZ from. Overcrowded slums with landlords extorting higher and higher rents as they pack the next plane load in.

I wish I was wrong, but that's he trend of the last decade or more.

And those most affected think the Treaty Bill is their biggest worry.

It will look like what Melbourne currently looks like. Anyone who has been there lately will know what I mean. Its no wonder that Victorians are moving to Queensland like New Zealanders.

.

South Aucklamd is good and improving ( this aint the 80s/90s), and will become more desirable place in future given the istmus is becoming unlivable (drivable).

prime city sites (Over 4k per sq m )

At the peak price for a recently constructed townhouse, the implied price for land in central Auckland reached over $21,000 per sq m (i.e price per acre of over $85,000,000)

I have 40 acres, bit further out but could cut you a deal here.... little bit of fast track and bobs your uncle

I'm rural but walking distance to the local supermarket, and I fancy becoming a multi-billionaire. Cc me on the MP/council emails please.

"I have 40 acres, bit further out"

Does this potentially impact you?

https://www.watercare.co.nz/home/about-us/latest-news-and-media/buildin…

https://www.watercare.co.nz/builders-and-developers/consultation/networ…

https://promising-sparkle-d7f0c0cfc9.media.strapiapp.com/network_capaci…

https://www.newstalkzb.co.nz/on-air/heather-du-plessis-allan-drive/audi…

"My kids don't fancy South Auckland so as returning ex pats they are never your buyer. "

South Auckland is a large area with a wide social demographic.

A couple of friends are returning expats and bought in Karaka.

Another friend who is an expat owned several properties in Manurewa. They are a non owner occupier owner. Unsure if they still own them.

A couple of other friends are owner occupier owners and live in the Flatbush area.

Another friend who is an expat owned several properties in Manurewa.

I know an expat lawyer who grew up in Manurewa. Has a home in the Hamptons.

Just saying.

House prices to Income ratio has doubled in 20 years from about 4 to 9.

A terrible statistic that affects all of us especially our children so I don't feel good about that

The downside of banks money creation and the reserve bank rates Yoyo

Yip and in inflation adjusted terms, houses prices are still 3-4x more expensive than they were 30 years ago (so value for money now is bloody terrible compared to what it was 3 decades ago).So it’s possible it’s still a massive bubble in real terms (not even considering nominal terms).

Remember that in most of the west, house price rises were more or less inline with inflation prior to 1990 for the 100 years or so prior. The past 3 decades have been a significant anomaly from that trend.

Humans are an interesting species.

The next successful species on this planet will study us and wonder why we imploded and all worked so hard to acquire expensive stuff and then destroyed ourselves - instead of simply playing and enjoying the planet.

We have gone nuts.

"The next successful species" assumes the current species has been successful.

With all our science, technology, data, academic knowledge, experts, how did we not already see this? I know many did, but they were considered primitive.

Fact is we already had the knowledge and teachings. We chose to be arrogant and ignorant? Or too many rulers and no leaders?

Those 3 decades would correlate with the timing of Chicago school economics, the FIRE sector taking over, and the masses brainwashed into treating homes as financial assets.

"House prices to Income ratio has doubled in 20 years from about 4 to 9."

Meanwhile in Australia, the house price to income has reached 8x.

Add stamp duty tax to that ratio in Aus and it'll probably look closer to 9x, like NZ.

I seem to recall all banks making predictions that house prices will increase somewhere between 5 and 15% in 2024.

That went well.

@Toye - whats your prediction ? I am saying 8%

I am saying 8%

Can you explain how you arrived at that forecast?

Some forecasts use supporting facts, reasoning and experienced judgement while others are just a gut feel.

8 is a lucky number I guess.

For 2025? I'd also say 8% but I'd make it a negative 8%.

I predict.

- Trump put massive tariffs on imports

- Europe implodes trying to agree how to sort ukraine when Trump pulls the USA budget for ukraine war. Possibly some more smaller more wars/skirmishes but Trump refuses to help and divides nato. Euro citizens choose peace over actually fighting themselves and give ukraine away

- China invades Taiwan as a way to refocus its citizens from an economic meltdown caused by Trumps tariffs smashing their manufacturing base

- Trump smashes the unions and addresses the deficit... but in doing so creates massive social unrest.

- australia economy sinks as China stops buying from it.

- rbnz refuses to drop rates locally.... saying it can't due to the trade wars. Points to government to have to solve it... infight and do nothing.

- in turn nz economy sinks.

House prices in nz revert to align with salaries. Drop by a further 40 to 50%. Everyone says it was obviously a bubble and wonders why we didn't sort it ages ago.

I keep surfing daily .. and stocked up with lots of.. popcorn watching peoples reactions as their real estate retirement funds collapse

China is quite happy to sell into the 85% of the world which is not part of the US/UK western bloc. And the US will have to keep buying a lot from China anyway despite any tariffs simply because the US simply does not make flatscreen TVs and laptops any more.

The Us exports $12b to China and imports $40b

The biggest economies in the world are

-us (27t gdp).

- eu and China ($20t ish gdp each from memory).

- Next nearest is Japan i think at $5t ish.. (whi don't like China one bit). Then it's rats and mice that china already deal with.

Given the USA and Eu (and other western nations) will end up collaborating in a trade war (eu and co will have to buckle to the Usa demands and sideline china).. China has nothing to really bargain with except hot air... sure in the short term they can cause some pain to the us supply chain and consumers if they really want to push their luck. but long term without usa and eu as customers.. Xi and the one party.. is toast. And if the us population gets onside and wants to sideline China... it will all happen fast and chinas government would topple with their economy.

Trump is right to impose massive tariffs and to sort the trade and financial deficits that threatens the US and the west by calling chinas bluff. China is playing childish games with no substance behind it.. and needs to fall in line and work with us.

Include Russia in that last line, and the whole world will be better off.

Russia has to fall in Line with China. It's only other potential mate is India.. and they aren't known for their loyalty.

Russia has roughly seven billion people worth of partners outside of the western aligned bloc. From Saudi Arabia to Indonesia to Iran. And of course you mention India: Russia (and previously the USSR) have had a very loyal and longstanding partnership with New Delhi other over many decades.

China is playing childish games with no substance behind it.. and needs to fall in line and work with us.

I think the time for western colonial hubris along these lines is long over. There is no reason for Global South nations to work closely with western partners who have proven time and again to be two faced and double dealing. By that I mean, US and EU countries consistently walking away from signed deals and treaties whenever it is convenient for them to do so. From Ukraine in 2014 to the Ukraine Minsk and Istanbul agreements, to the US walking away from the ABM treaty to Washington completely ignoring the One China basis of its relationship with Beijing in order to arm and strengthen the independence movement in Taiwan.

Where do you surf oldskool? I might join you, if you don't mind, and bring extra popcorn.

Not sure why so many think that house prices are going to drop in NZ?

Reality is that some areas in NZ have had reduced prices, due to the debt servicing criteria be used by the Banks!

Truth is that overall, NZ house prices are still pretty cheap and with interest rates be lowered to where they should be, prices in many areas will continue upwards.

Watch Sky News Australia and you will see that Australia’s housing is so much higher than NZ,

Investors/ Landlords in NZ are generally doing a fantastic job in providing accommodation to those that require it.

The unfortunate thing is that it is not currently financially viable to purchase a property and rent it out, and certainly hasnt helped by the previous Labour government stupid and wrong policies.

The unfortunate thing is that it is not currently financially viable to purchase a property and rent it out

This is where i think the price of ownership is, where it is not financially viable to buy and rent it out.

The fortunate thing is that it is not currently financially viable to purchase a property and rent it out.

This raises the point that there's no point in house prices coming down unless rents come down with them.

"Not sure why so many think that house prices are going to drop in NZ?"

Simple, if mortgage is getting harder to get, fewer people will be able to buy. As always, banks have to source their funding to lend out from terms deposits and on international market. If that orange guy carries out his promises, it will be harder to source funding.

I don't know why people think Trumps tarifs will increase interest rates.

do some research and expand your knowledge.. simple economics

My question was not "I don't understand" my question was " i don't understand why other people think"

Maybe if your comment was more directed around giving your opinion on the subject you would add value to the forum, since you took the time to respond.

What is going to require mean attention/ have a bigger impact?

NZ Loss of GDP and struggling economy = lower rates

Imported goods inflation caused by higher USD/NZD price = higher rates

Chairman, recent experience in ChCh is that property is selling and people are getting mortgages.

Depends on how motivated to buy people are.

Non motivated will not get mortgages

I am talking about future here.. going forward to 2025-2028

I disagree that Australia's housing is more expensive like for like. What Australia has is a lot more high end homes than NZ does, which pulls up the "median". NZ doesnt have many rich people therefore it doesnt have many fancy houses. Apart from in Queenstown and few in Paratai Drive. There are also no high rise luxury apartments in NZ like you have in Sydney, Melbourne, Brisbane, Gold Coast etc.

Australia also has a lot of cheap apartments and townhouses. If I swapped my current home for one on the Gold Coast, I could buy a waterfront 4 bedroom home, with its own private jetty. If I didnt want the water view, I could spend roughly two thirds of my NZ house value to get a similar standard to what I have now. And my Council rates would be less than a third of my current rates bills for either property.

KW, with respect I believe that you are incorrect if you think NZ houses are more expensive than Australia.

Australia housing used to be cheaper than NZ but not in the major cities anymore.

You only need to watch the online auctions from Australia and you will see what has happened over there.

Go to Domain and it will give you a much clearer picture.

If you are a non owner of property in Australia, you have a lot less chance of buying your first home than in NZ, unless you are wanting to live in a crap Place?

KW is right, not you. I follow both markets. Like for like Australia is cheaper.

Like for Like?

Example please?

What cities are you comparing with?

I have travelled various parts of the world!

Lived in Australia for a wee while and holidayed in many parts of Australia and been there on at least 30 different times.

Christchurch you can buy a reasonable 3 bedroom house for under $700k within 10 minutes drive of the CBD, can you do that in Sydney or Melbourne or Brisbane nowadays?

Maybe not, but you can in Adelaide. A city that is still 3 times as large as Christchurch. And Newcastle, a city of similar size to Christchurch. As I said, like for like. Not comparing small town Christchurch to a city of 5 million people which is home to a lot of very rich people.

Compare Auckland prices to Brisbane.

This is what I could trade my house in Christchurch for on the Gold Coast. Its an extra 100 sqm bigger, has a pool, and resides in one of the GC's most prestigious gated communities with private security, two golf courses, and a marina

https://www.realestate.com.au/property-house-qld-sanctuary+cove-1466327…

Or how about a waterfront property with its own private jetty

https://www.realestate.com.au/property-house-qld-helensvale-146600020

KW, we will agree to disagree, NZ house prices are now cheaper than Australia in the cities.

The average price in Adelaide is now close to $900k

They have all sorts of property taxes over there as well.

The Sanctuary Cove property will be selling for s big price dont expect it to sell for the estimate.

I know the Gold Coast property market and it is a helluva lot more expensive than it used to be, as it used to be very cheap.

Christchurch is the most desireable NZ city currently and that is why we are not seeing decreasing house prices.

Auckland is the most desirable NZ city . As some people leave it those arriving more than make up for those leaving. It’s better weather and more work and business opportunities are the drawcard.

Give them time, Oz has been behind us in the same rollercoaster of real estate boom. They are now getting the social consequences of mass immigration, higher cost of living and diminishing infrastructure.

We’ve been here before and nothing will change. Anticipating more bad news to fuel further rate cuts.

Hmmm ... A lot of these predictions are based around "a return to mean". ("mean", in this context = long run average). Not sure I think that's completely the right approach. Take care.

So back to 60% to 100% increases every decade? Just what everyone needs.

Interesting. 4% might be "modest", but add to that another 4% in rental yield and that's an 8%p/a gross return, (or closer to 10% expected in 2026). That's in line with the historic stock market averages of about 8%p/a.

As always, the question is, will property prices actually go up by 4% next year and by 6% in 2026? and once you add rental yield to that will it prove to be better than investing in the stock market index fund like S&P500? Only time will tell

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.