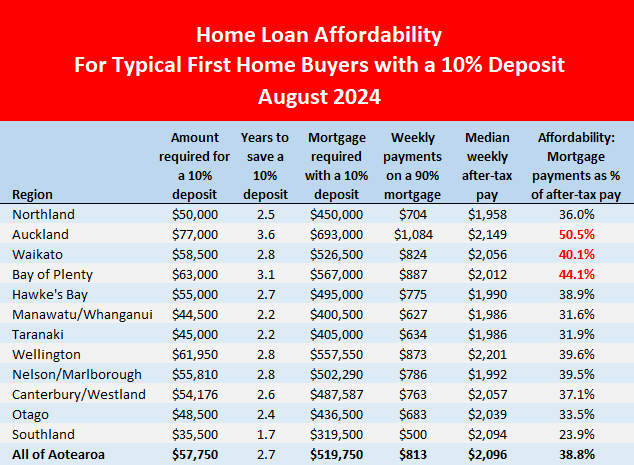

First home buyers are seeing the benefits of declining house prices and the recent falls in mortgage interest rates, with a substantial improvement in home loan affordability over the last six months.

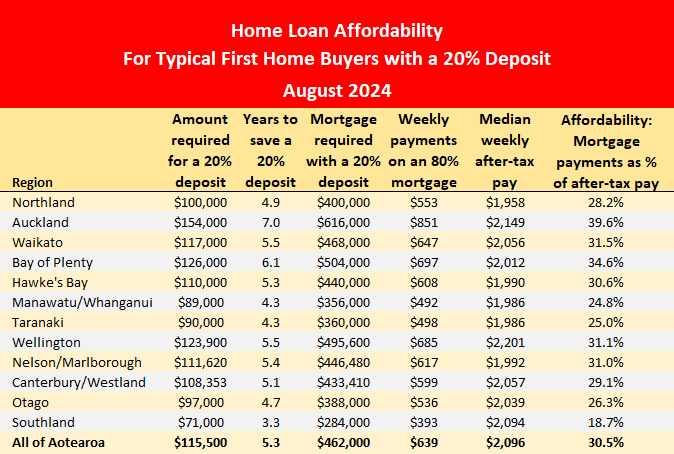

Interest.co.nz estimates the mortgage payments on a home purchased at the Real Estate Institute of NZ's national lower quartile selling price would have declined by around $81 a week between March and August this year, if the home had been purchased with a 20% deposit. If it was bought with a 10% deposit the mortgage payments would have fallen by about $97 a week.

That's because the national lower quartile price declined from $600,000 in March to $577,500 in August, while the average two year fixed mortgage rate declined from 6.77% to 6.00% over the same period.

That fortuitous combination not only reduced the amount that would need to be paid for a home at the lower quartile price, it also reduced the amount needed for a deposit, the size of the mortgage needed to make the purchase and the amount of the mortgage payments.

Interest.co.nz also compares the mortgage payments outlined above, against the median wages of couples aged 25-29, to get a standard measure of affordability.

A mortgage is considered unaffordable if the payments eat up more than 40% of a couple's after-tax pay.

The latest declines in prices and mortgage rates means all regions of the country are now considered affordable for typical first home buyers, provided they can scrape together a 20% deposit.

That is even true for the Auckland region, which slipped under the 40% affordability threshold for the first time in almost three years in August.

The last time Auckland housing met the affordability criteria was September 2021, when the average two year fixed mortgage rate was just 3.02%.

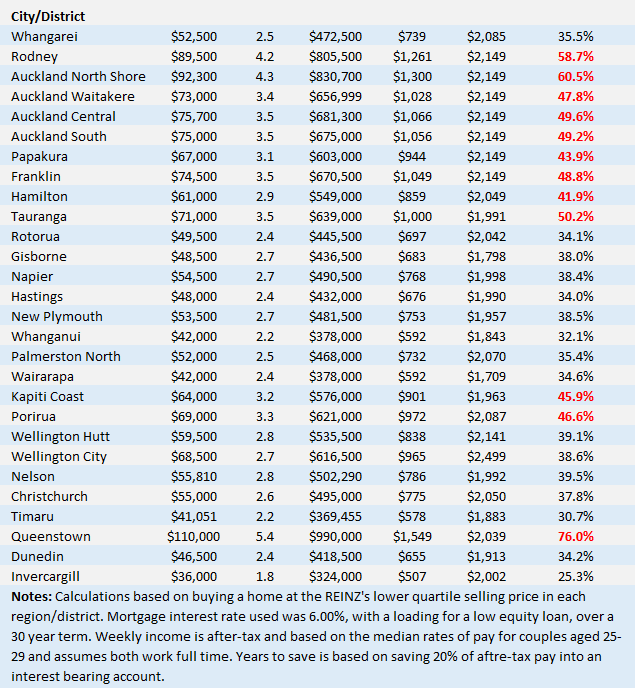

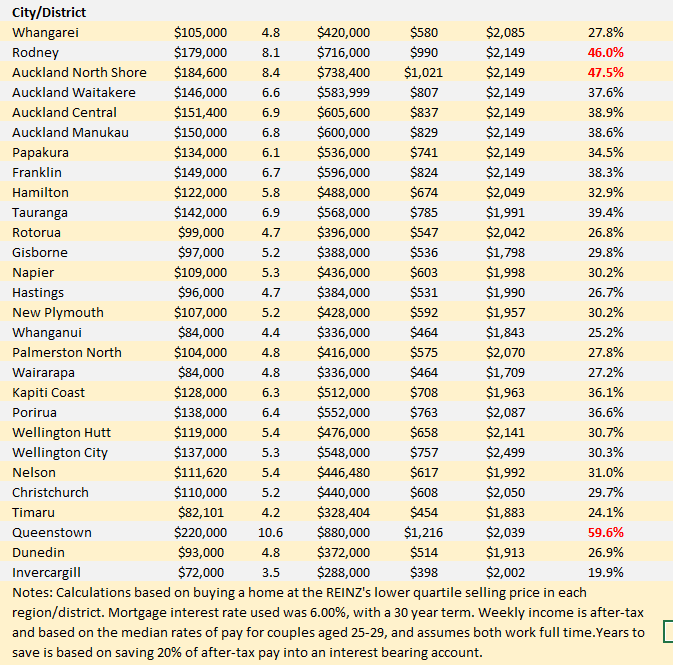

In fact the latest downward movements in prices and interest rates mean the only districts now considered unaffordable for typical first home buyers are Queenstown, along with Rodney and the North Shore in Auckland.

However, getting a 20% deposit together will not be easy for most first home buyers.

Someone buying a home at the national lower quartile price of $577,500 would need $115,500 for a 20% deposit, while around the regions a 20% deposit would range from $71,000 in Southland to $154,000 in Auckland.

Getting a deposit together is likely to be the biggest hurdle facing potential first home buyers on average incomes, particularly in the main centres.

Those struggling to find a 20% deposit could consider a low equity mortgage with a smaller deposit, however banks charge substantially more for low equity mortgages because of the higher risks involved, and that has the effect of significantly increasing the mortgage payments, which in turn reduces their affordability level.

Although there is no easy path to home ownership, the trends over the last six months would certainly have provided a slightly smoother path for many first home buyers.

The tables below give the main affordability measures for typical first home buyers in all of the country's regions and main urban districts.

- The comment stream on this article is now closed.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

55 Comments

Future, much better, affordability is coming, wait till 2027 to 2028 to get a reasonable deal from a very Ponzi drunk and liquidating Landlord.

Only offer prices in the old 2015 to 2018 valuation price range, as that's where prices are headed (or lower??) as those many thousands that are in the horrors of NEGATIVE EQUITY.....dont recommend it, as all their deposit money (+some) has evaporated, like a fart in the wind!

Better affordability is here. Sorry Gecko prices are already rising.

Your favorite bouncing financial cat, must be really bad shape now??

Man alive, that must be the forth Dead Cat bounce? you spruikers have born false witness to and proclaimed since early 2023.......

Still I love your gumby positivity and guile, in the face of undoubtedly the biggest property cash in NZ, since the 1970's! This crash is no way done its good work, in teaching housing speculators a lesson in moral hazard, that will last a lifetime:)

Give it up mate you cannot even predict next month let alone 2027 to 2028. If interest rates dive another 75bps before Christmas property prices will start to rise, do you agree ?

Nice start.....but you need to add yet another 325bps, to reanimate the dead and decaying corpse, that is the NZ property market.

Financial confidence is shot to pieces.

The world is flooding into the safe havens, have you been asleep?

Read, Learn and weep, housing punters:

Commodities - Bloomberg

Precious and Industrial Metals - Bloomberg

BofA’s Hartnett Says Buy Bonds and Gold as Bubble Risk Returns - Bloomberg

You are all very welcome!

You cannot live in a gold bar, its a waste of time and a double waste of time if you have gold and are still paying rent. Sure its a good investment to pour into IF you already own your own home with no mortgage.

NZGecko is starting to sound desperate.

Own the miners with long mine life / low cost/AISC - paying increased dividends. Small part of my diversified assets.

I have not paid rent for over 25 years lads!

Agree on owning lots of pet rocks, expecting to sell for more, is like being one of the dumb Landlords speculating on CGs (as they all do!!).

Whoever the next government will be they will have to raise taxes to pay for infrastructure.

The most palatable new tax at the moment is CGT.. which simultaneously slows house prices growth and thus solves two or three issues at once. once one party makes it policy to intro cgt and sees swing voters approce of it....the other will have follow (else they won't be able to afford the same stuff).

Guaranteed CGT from next election. Property investment is yesterday's news.

Capital Gains Tax does not slow price rises at all!

Quite the opposite, if a comprehensive CGT is ever brought in, all it will do is ensure further rises in both prices and rents!

You tax anything and the tax is passed on, there is always consequences!

People calling for further capital gains taxes are those that are generally not financially savvy or successful and it is an ENVY Tax!

Capital gains tax is just another distraction. Every policy so far has only driven up rents and house prices, yet people don’t seem to realise.

The system will never change.

No. Your arguement misses the point that people will only pay what they can afford.

Adding cgt thus reduces the profit for the seller and rightly means they contribute to the country as does everyone else.

I can assure you that if people can not afford to pay then they will be without housing from private landlords.

Landlords are currently subsidising tenants living costs and without capital gain they will soon get the stitch!

The catch 22 in your arguement is that without tenants willing to pay the high prices and with a CGT most landlords will be sell their houses. So someone else will buy them and live in then ir rent then out with - but with NO change to the total number of houses or occupiers.

The fact that most poperty investors rely on capital gains for their profit isn't really a problem for nz. Noone will shed a tear if they lose money .. in fact if the house or rent drops in value/cost it's a net benefit to everyone who isn't a landlord. If people choose to stay landlords and pay a cgt that's great too.

We don't need more landlords or even to keep the ones we have. We do need more affordable housing. Landlords exiting is thus an overall benefit for most people in nz. As is cheaper land as is cheaper build costs... etc. Etc.

CGTs are coming down the pipe.......deny it at your financial peril!

Def not an envy tax. Every other oecd country has a cgt.

Nz is short on tax and it's a very fair way to get some more.

If it will not be paid for by the sellers... but the buyers.. then why would you care?

Sure because everyone who sells a house then goes and lives in a cave. We don't need a CGT and any party who suggests one will go down in flames.

Come on. There are industrious, financially savvy people proposing CGT.

Who?

The 'experts' here?

Nope just people that work hard to derive their income from things other than the housing market.

A CGT will stuff everything.

we are a small country and taxing property gains will kill industry big time.

Instead of trying to take money off the financial savvy people the government needs go get the less savvy people to stop relying on the taxpayer!

I can guarantee that if a cgt ever comes in there will be an exit from the country from the successful people.

Good riddance. Leave your houses at the door.

There will be a net gain from all the young, smart, educated, hard working people returning who have skills other than property speculation.

You tax anything and the tax is passed on, there is always consequences!

If the vendors think putting the tax onto the price will be palatable by potential buyers, they are sorely wrong. Nobody will buy the house and eventually they will have to drop the price from lack of sale. The market dictates the price, not the vendors hopes and dreams.

Zwifter - it is possible, but it is also possible that if interest rates are dropping that amount it is a reflection that the economy is really in the s%**. And this could mean asset prices are taking a hiding - because asset prices don’t go up when businesses are failing and people are losing their jobs.

Do you agree? Or do you live in some fantasy land where the economy gets worse but house prices go up simultaneously?

Go easy on these numpties IO.

It is hard for someone who has not been part of the real economy outside of brick-and-mortar in a while to understand you require a steady income from a secure job to take on a huge pile of mortgage debt.

Many construction and engineering companies are looking to cut several thousands of jobs between the sector after being on hiring freeze for a while because of how sharply private and public purses are shut.

But nothing interest cuts can't fix, eh?

Yep the economy is in the shit, this is the primary reason they are having to drop rates because money being paid in interest to banks is pretty much 100% wasted as its not flowing into the wider economy in the form of goods and services. Unfortunately people cannot pull their heads in so the RBNZ engineered a recession to rein in the house buying spree that they created. The fact remains that history will repeat if rates fall too far, cheap credit equals increasing house prices so the RBNZ now has to walk the line between recovering the economy and house prices going nuts again.

Uou hit the nail on the head. There is no way out.. we are just avoiding two bad outcomes

There's plenty of real places where the economy gets worse and asset prices rise. We live in one and It's been accelerating since 2008.

All it takes is a wealthy minority to stop investing in new stuff and start buying existing stuff.

60 years ago an individual in the wealthiest 10% had 4-5x (depending on region) the wealth of your bog standard 50th percentile in NZ. Now that same 10th has sixty eight times the 50th percentile. I don't see any major industrial changes to account for that, unless we've suddenly bred a crop of tech geniuses?

Tbf the only thing that's been happening in this country for decades is the economy getting worse whilst house prices go up.

Pretty much. My question is with all the posters calling out "bottom now, buy now etc etc", how many of them have taken their own advise and bought more or any property. Would hate to think they are just ticket clippers trying to throw others under the bus for their own financial reward.

Meanwhile... manufacturing closing left and right, Fletcher's announcing bonds to reinflate balance sheet, construction in the toilet, energy security crisis due to green magic policies that delivered nothing, Civil roading projects at a standstill as Coalition of Chaos killed all the development work, educated youth with little job prospects and tired of being held hostage by housing speculators are all leaving in mass to Straya, and on and on...

So dead cat bounce...that cat has so much lead in it, its close to being a black hole and creating its own gravity downwards.

2015 prices? I could barely source the materials of my house + driveway in 2024 let alone the land and labour to build it. Go ahead and offer 2015 prices but all you’ll get is laughed at.

‘The Chinese economy keeps imploding from within.

And we should pay attention.

The Property Price Index for Chinese tier-1 cities keeps making new lows, and it’s now approaching levels last seen 8 years ago!’

https://x.com/macroalf/status/1837131285468246284?s=46&t=MUwQeKa7MkEJ7r…

Could be coming to a city near you soon Rampart.

Bazinga Rampart......I've seen many markets where the product goes well below the common cost of production....

Its coming, unless we get mortgage rates well below 3%.

You couldn't build my first home for what I paid for it in 2017 ($200k). A1 homes have a similar layout/plan with a base build price of $250k and that's just the house.

Our current place (200sqm 4 bedroom 2 bathroom on 1/4 acre) previously sold for $360k in late 2016. Both sales were just prior to regional contagion in the property markets.

Two ways in which Chinas falling house prices are different ours. They have a plummeting birth rate and over supply of housing. Yes our birth rate is falling as well. I just can’t see house prices getting much lower than they are now.

Chinas days of an economic super power appear to be coming to an end. Peter Zeihan sheds light of Chinas economic woes. https://youtu.be/mqA5NODRnQI?si=wwEMGzeL2LSmFFEz

With respect you are seriously deluded with your comments!

If people were going to be accepting 2015 prices, then I would be buying hundreds of properties!

Reality is that prices are still very good value, and nothing surer is that the market prices are going to increase!

Well..... your track history has been miserable. Constant Dead Cat bounce caller.....Who would believe you now, Spruiker?

I called the NZ property crash in 2021/2022 . Here we are now, -30 to -40% Down in REAL terms. Its Not over yet!

Game, Set, Match.

From where The Man is investing, prices havent dropped!

There have been plenty of opportunities in the last couple of years and experienced knowledgeable investors have been making very good profits.

Nothing surer is that prices in CHCh are increasing, maybe not in other areas, but then I am not involved in those areas.

CHCH has been recording drops in the latest results. It's possible that it is just beginning a second leg down, as it tends to lag behind Auckland.

The average price in CHCH increased something like 40 percent over the post covid credit bubble, and the real economy underlying the market has not increased 40 percent, so go figure. Despite not having blown up to the levels of unaffordability as Auckland, how can you not look at a 40 percent increase in valuation, mostly based on an unprecedented credit injection, as anything other than a speculative bubble.

I guess that you can only manage that feat of intellectual gymnastics if vested interest determines that you must...

Prices have not dropped in Chch.

There have been a lot of 2 bedroom townhouses built snd sold and therefore skewed the prices.

No one I know including ourselves that have sold in the past few years have indeed done quite nicely.

I do know that there are vendors who do allow their property to be undersold!

Like the photo

"Baby, aren't you so happy we listened to poppy and waited 9 years for market conditions to be slightly more favourable? Now we can start a family"

"But Steve, I'm 45 now, and we're up for 10s of thousands of dollars in IVF. And you just lost your job"

9 years ago FHB had their ability to purchase a new home smashed away from them by the banks' indiscriminate application of the government's new LVR rules - deposit requirements went up 6x overnight. In the ensuing void, specuvestors filled the gap - personally, we went from house shopping to watching our landlady purchase other houses on the block leveraging equity from capital gains, all the while crowing about no competition.

While the FHB rules were later eased, the damage to our young had already been done. All the people in my friends and family group of my age who have since bought houses have one thing in common - outside help to purchase (inheritance or deposit from forward-thinking parents or lived at home tull 30+). Without that help - nada.

Hold on, help is on its way.

The burning and flaming overleveraged landlords, are running for cover and a cold lake to douse their burning financial ruination with.

Prices to tank and abate into 2028!

You might have to wait another 10 years Gecko, the can will be kicked, it’s started…while the effectiveness won’t be as grunty as the last boom cycle it’s hard to think it won’t start to turn…maybe the next bust will be the fatality…but if they slash rates like what is expected it’ll start to push 🏡 prices again 📈

If they do as you suggest I think inflation will rip once again and mortgage rates will be on the rise once more and then house prices will be flat/falling like they have been after the last stimulus.

We will have further cost of living issues and still have an overpriced housing market - basically no gain to anyone.

Until we get our private debt vs GDP figure down, we are up shit creek and find ourselves living beyond our means (ie completely unsustainable situation). Our housing market becomes the straw that breaks the camels back - it’s like a self licking ice cream that destroys the whole economy. Our need to protect it at any cost means the parasite kills the host.

IO, I agree with you that it’s not a good thing for NZ but if the govt continues with austerity then the RBNZ will slash rates to get things moving and undoubtedly that will lead to an increase in house prices. I don’t think 20-40% stuff, but it will see it increase once the lower rates take effect, less of a lag with people fixing shorter later so maybe 12 months? Hopefully they use DTI/LVR wisely to somewhat cap growth, but I wouldn’t be surprised to see restrictions eased/removed when they realise it’s not booming quickly enough.

I also don’t think we see inflation flare up again like you’ve mentioned, how much of the inflation we saw was genuinely demand pull driven…the stupid house prices, yep for sure on the back of cheap $$…almost all of the rest of it was cost push driven with climate events, supply restrictions…and toward the latter end, higher costs of lending.

But hey, it’s all crystal ball stuff…next 12-24 months going to be fascinating to watch

Yes it is crystal ball stuff unless you know for sure that this is definitely the bottom - which a few commentators on here know with 100% confidence. No doubt. Market has turned.

Also see Jfoes posts - if governments holds its austerity position while the RBNZ drop rates, the housing market won’t be going anywhere. There will be a massive hole in our economy and it will continue to contract until government spending turns the tide again.

Globally the brown stuff is about to hit the fan - ie the recession is about to hit but people think we’re coming out the other side of it! It hasn’t even started yet!

Here’s a chart of what is probably about to play out in the US - rate cuts and sharemarket weakness:

https://x.com/gameoftrades_/status/1837180018415554841?s=46&t=MUwQeKa7M…

NZGecko I can assure you this landlord ain't over leveraged or burning up. All properties are rented all properties are paying their way. And am about to start a new build on the back of my recent purchase. Remeber people like you said back in the day when tax incentives were taken off residential rentals. There was going to be a glut of landlords abandoning their rentals. Then when the bright line was dropped a few months ago again people like you said LL will be abandoning rentals in their droves hasn't happened

Well done on out bidding the young FHBs years ago, when the average DTIs were 3 to 5x incomes. This was not a bad gamble (but shutout good Kiwi FHBs) at those low DTI metrics. Go you CC.

However, I know of some financially inept people, who are "Topping Up" rentals that they believe are "Investments" - at the rate of $200.00 to $600.00 per week.

They purchased at crazy metrics of 6 to 11x DTIs. Fools and their money are certain to be parted.

This lunacy is accepted as "investment"??? The nutters are running the asylum, if this is an investment.

Simple: its CG gambling and will end in tears. The banks are making the Overleveraged sell, in large numbers now...... but don't want it public, as to keep the horses calm.....

Is 40% an affordability metric that should remain static? Other (non mortgage) living costs seem to be taking an ever increasing chunk of people's salary, be it food basics or avo or toast, rates and insurance, fuel, and so forth.

Good point.

And it’s higher than commonly used worldwide.

And they persist with the absurd age assumption of 25-29 for FHBs.

As a minimum, they should use age 29-33, and as a maximum 35% as an affordability metric.

But I have said this many times before like a broken record

It's supposed to include all housing costs except utilities. So rent or mortgage PLUS other associated ownership costs (rates, insurance, maintenance).

All aboard folks, exactly as predicted.

And you're going to see a lot more activity in the property sector later this year and early next year. The bottom's in.

BTW, any govt. dumb enough to invoke a CGT is going to push property prices even higher, so if you think a CGT's just around the corner, and would like to make a poultice.....start buying property.

And that sort of narcissism is why it should be a land tax, paid quarterly in advance, on the full developable value.

Get on board then, make your fortune if it's so easy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.