There are tentative signs that home loan affordability has turned a corner for aspiring first home buyers, bringing the prospect of owning their own home slightly closer.

The latest improvement comes after many years of worsening affordability for first home buyers followed by a brief period of relative stability, and may mark a turning point in the market.

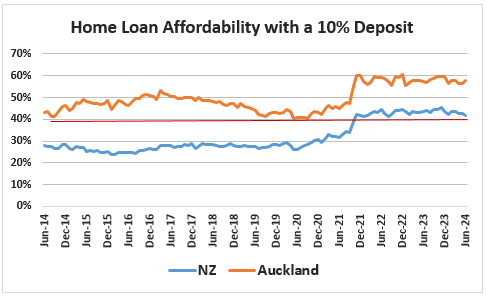

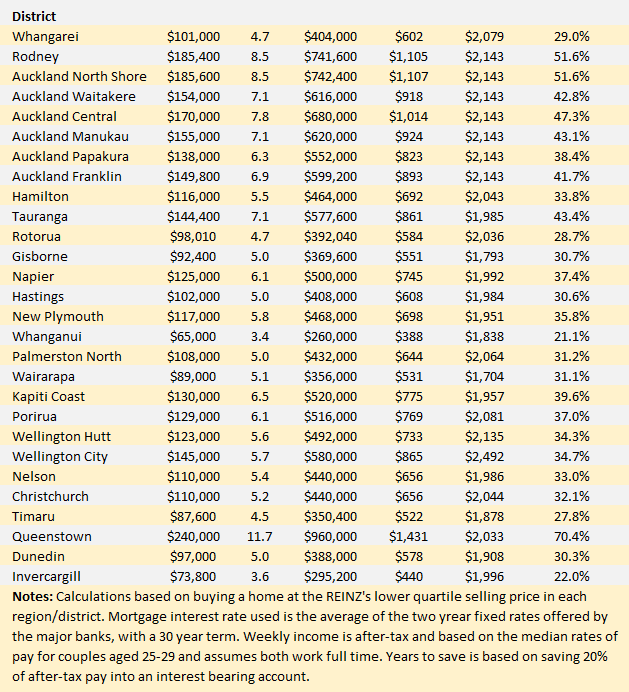

Interest.co.nz tracks the mortgage payments for a home purchased at the Real Estate Institute of New Zealand's lower quartile selling price in each major urban district, and compares that to the median after-tax wages of 25-29 year old couples.

Mortgage payments are considered unaffordable if they take up more than 40% of their after-tax pay.

That latest figures show the percentage of typical first home buyers' take home home pay that would be taken up by mortgage payments on a home purchased at the national lower quartile price with a 10% deposit, has declined for the last three consecutive months, from 43.8% in March to 41.9% in June.

That means home ownership for typical first home buyers has gone from being solidly in unaffordable territory at the start of the year to just marginally unaffordable in June.

If the current trend continues, then affordability at the national level would likely dip under the 40% threshold in the fourth quarter of this year.

If that happens, it would the first time that housing has been considered affordable for first home buyers at the national level since October 2021.

The recent improvement in affordability has been caused by a fortuitous combination of several factors:

- Small falls in REINZ's lower quartile selling price which has declined for three consecutive months, from $600,000 in March to $579,000 in June.

- Small falls in mortgage interest rates, with the average of the two year fixed rates charged by the major banks declining for seven months, from 7.04% in November last year to 6.72% in June this year.

- The drop in interest rates combined with falling prices has seen the mortgage payments on a lower quartile-priced home purchased with a 10% deposit, steadily decline from $935 a week in November last year to $875 a week in June this year, providing a saving of $60 a week in mortgage payments. If the same property was purchased with a 20% deposit, the mortgage payments would have declined from $740 to $690 over the same period, giving a saving of $50 a week.

- Ongoing increases in wages, although these have slowed considerably this year after substantial growth last year. Interest.co.nz estimates the after-tax pay for couples aged 25-29 and both working full time, has increased from $2078 a week in January this year to $2090 in June, giving them an extra $12 a week.

However the latest improvements in affordability should be regarded as a small step in the right direction rather than a great leap forward in home ownership measures.

Housing is still severely unaffordable for prospective first home buyers on average incomes in Auckland and is also particularly difficult for them in Bay of Plenty, Hawke's Bay and Wellington.

It would take a sustained decline in mortgage interest rates and house prices at the bottom of the market and an ongoing rise in wages to make home ownership an affordable option for typical first home buyers in those regions.

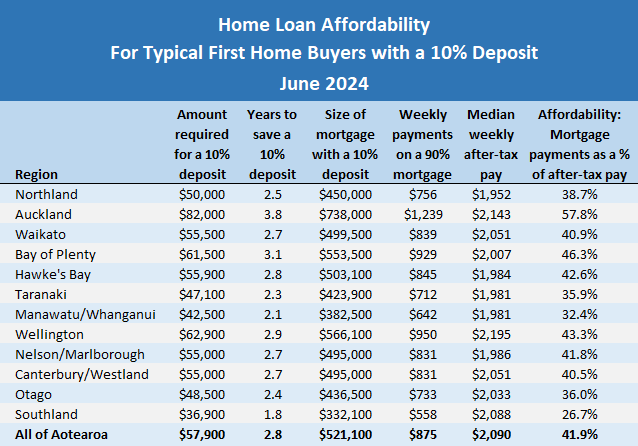

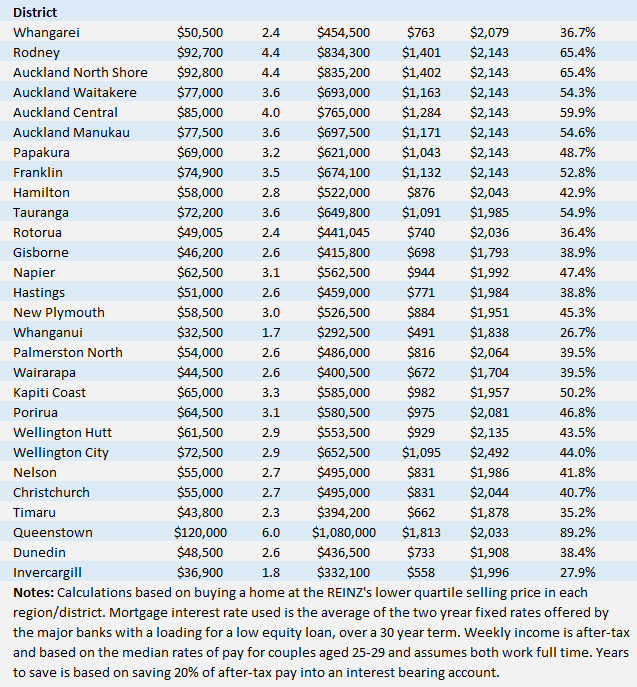

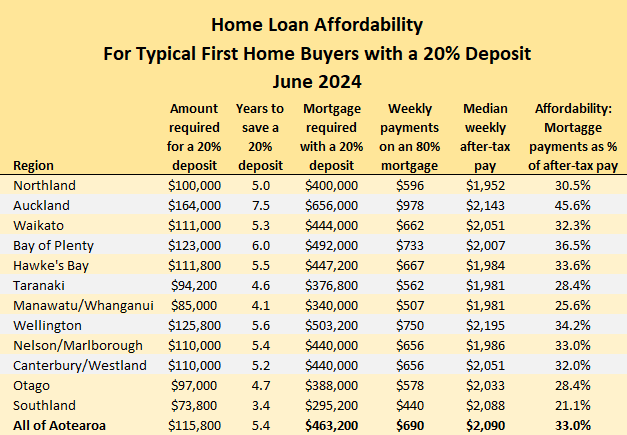

The tables below give the main affordability measures in all of the main urban areas throughout the country.

- The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

89 Comments

Good news. The question is... why did we allow affordability to get this bad in the first place, and what are we going to do moving forward to ensure it consistently improves for FHB? Putting a lid on crazy rent inflation is a good start. The self serving nature of our landlording culture push costs downwards... there has to be a better way?

Affordability became a problem, again, when we allowed property prices to escape in 2012; when we had them by the throat. One more push back then and Affordability was within reach. But no. We wanted higher property prices to make ourselves Rich. Now we have the worst of both Worlds. A Higher gross Debt to service and our citizens mortgaged past their eyeballs. Lower interest rates isn't the answer - they are the problem.

Unfortunately for a time it was the only investment path 'a generation' of people in NZ were rewarded with, hence they voted in mass for the government party that massaged that investment path the most, even to the detriment of the economy as a whole.

However, I believe that path is now well-trodden and that generation will be now cashing in their property chips, in mass.

Quite a prediction there! And when they cash up, they will invest in what? Crypto currency? Term deposits? Share market?

Hint - buy Ryman shares.

I will avoid these types of shares!

Anyway, your point is that rich elderly Aucklanders will move to a retirement village. They will sell their own property, and still have a million dollars left over, plus another million or so from the sale of their 2 or 3 investment properties. So where will they put their money?

fishers milford etc in conservative funds.

They'll probably give it to their children as an inheritance.Who will gleefully spend it or investment as they so wish.

Obviously why there is likely to be so much noise made about taxing it in the future.

I doubt Rymans is going to end up as a good bet for the coming future. I shall tell you why my opinion is such.

New Zealand's senior population is increasingly shunning retirement villages in favor of maintaining their independence in their own homes.

This trend is driven by a desire for autonomy, control over finances, and a sense of familiarity in their existing communities.

Myself and many of my peers approaching retirement and newly retired are of this opinion.

Retirement villages offer a convenient and secure living option, but they often come with hefty entrance fees and ongoing maintenance charges. Many retirees find these costs excessive, especially considering they may already own their own homes outright.

Additionally, some seniors feel that retirement villages can be more isolating and restrictive, limiting their ability to maintain their independence and social connections within their existing communities.

This shift in preference reflects a broader societal trend of seniors prioritizing active and engaged lifestyles well into their later years.

Many retirees are opting to modify their existing homes to accommodate their changing needs, allowing them to age in place while remaining close to friends and family.

Technological advancements in home care and monitoring systems further support this trend, providing a safety net while preserving independence.

The New Zealand government is also slowly recognizing this shift and is implementing initiatives to support in-home aged care.

This includes financial assistance for home modifications and increased access to community-based services.

The fact is the newer generation of "X" are not likely to be sold on these "villages " in any sense or form.

✅Comment of the day.

Some very broad and generalised statements here. Just your view of the World

It’s just that the newer retirees are of the most entitled generation in modern history, and will expect everything to be done for them wherever they decide to live

"Hint - buy Ryman shares."

Isn't a lot of Rhyman's wealth tied to real estate too ( retirement village real estate to be precise)?

Demographics - ignore them at your peril.

As for Rymans, I think they'll stand a chance if they meet the market instead of thinking they can dictate to it. To date it's been more a story of real estate exuberance, debt accumulation and more lately - denial.

Wrong. People who over the last 20-40 years have bought and held shares from all over the world are now very wealthy and happy people. People need to diversify.

why did we allow affordability to get this bad in the first place

So some could get rich and others could “feel” rich. Greed……it’s always greed.

I think you may get your wishes TomJ, rents are dropping. There arent as many high priced rents and more rental properties are available to choose from. The humble landlord HAS to negotiate or stay empty for longer

Great news for all those that waited patiently and for those that have a bit more patience

And let's not forget these hollow, politically-motivated words:

"Not only have house prices increased, but the cost of serving a mortgage has also skyrocketed in recent years.... Each week 760 people leave New Zealand to live in Australia....thousands of young New Zealanders have resigned themselves to never owning their own home.... Median house prices are now essentially double what they were six years ago.....if we are serious about protecting the Kiwi Dream of homeownership, then we need to get a better balance between those concerns and their eventual impact on home affordability. To not do so is to ignore a fundamental long-term driver of the housing affordability crisis..... The crisis has reached dangerous levels in recent years and looks set to get worse."

The Right Honourable, Sir John Key - 2007

https://www.scoop.co.nz/stories/PA0708/S00336/key-speech-to-new-zealand…

The number of apparently intelligent people that I know who "miss John Key" is extremely saddening.

Will the FHB couple pictured above display the same doting pose once the vet bills arrive?

Made me go back and look at the picture. What the heck is up up with his hips/ legs.

You have to have big balls to buy at this point in the market?

best comment of the day

We are buying and selling at the moment, opportunities are as good as they have been for years.

If you are experienced and prepared to work then you should not be on the sidelines.

Yeah, but the point is those opportunities are only getting better. For those on the right side of the transaction…

Mortgage payments are considered unaffordable if they take up more than 40% of their after-tax pay.

Why is it 40% in NZ and only 30% in Europe and the US?

Because it's arbitrary, but NZ is more obsessed with property.

Because that extra 10% would knock another 100k off our soggy dog boxes.....

40% is a nonsense, way too high. Even using that speaks to the ridiculous mindset that we have in this country

Remember HM that 40% of the salery is in the first year, but goes down every year as salaries increase and and the mortgage gets paid off.

or goes up if interest rates go up (that was in very small print)

Exactly

also, 40% is quite doable on a high income, different story on a middle income

whether its 30 or 40% its a crude measure and not very useful

IT Guy, I am talking about the present, and interest rates are coming down, and will continue to drop.

IT GUY the horse-trading, futures and forex extraordinaire, announced before this weeks inflation number that inflation wont be dropping for a "long time". Hahahaha. He is also good with spreading horse shit

says the term deposit holding sad sack renter

Steady fella its only a larf... at the mo I watching the horsies run, you can get a sire with The Chosen One for only 4K. D Trump says he is The Chosen One, I sure hope they dont mix up which stud theyre using, we dont want an orange foal looking for a mirror

Btw we are in good company holding TDs like others here.. or are TDs just for losers now in your humble opinion

Are you drunk?

Hahaha nice try grandpa

As the banks all say politely "Term deposits are a core plank of our funding".

"Bank failures are caused by depositors who don't deposit enough money to cover loses due to mismanagement"

Wait - WTF?

Failures are caused by depositors seeking excessive returns without considering the risks enough. Institutions then spray the extra working capital around to property developers knowing their shareholders demand higher net profits and their staff and managers want higher bonuses

So you reckon mortgage rates are going to go lower than the normalised average? Why? (The answer isn't :"Because they have been so high, they have to come back down")

"Since recording began in June 1998, the average interest rate for the RBNZ average floating rate is 6.90%. The minimum interest rate was 4.50%, which occurred in October 2020. The RBNZ average two-year fixed rate is 6.47%."

We'e recently seen 'the lows'. What if we are about to see The Highs, again? (And there are many good reasons why we could. DJT being just one ie: Inflation is going to roar WHEN he lowers taxes , increases spending and imposes trade tariffs)

"the maximum floating interest rate observed was 11.20%. The maximum average two-year fixed rate was 9.80%"

https://www.mpamag.com/nz/mortgage-industry/guides/historical-mortgage-…

Short term - probably. But who knows in 3-4 years

The housemouse mantra. You can insure for most risks, if really worried you can even take out a 5 year fixed interest rate loan, but cant insure against inflation and rising rents.

Sure.

But there’s a wider point here. The higher the %, the less the buffer for a whole range of eventualities. Not just higher interest rates.

40% is too high

Try to see a bit of hope, the why instead of the why not

Some here are steaming up their windows at the thought of interest rates dropping dramatically. These same individuals expressed zero caution near or at the height of cheapest credit, price froth and risk. Once rates started rising, there was little understanding of the time lagging economic impacts higher interest rates, cost of living and employment uncertainty would eventually have on consumer and business confidence. The common expectation was that people would simply adjust by getting a pay rise, a higher paying job or even a second or third job with minimal societal impact. The fact is, unless they lose their own job, I doubt they'll really appreciate the impact. The prevailing circumstances that will accompany lower interest rates is much higher unemployment, lower rents and house prices. This will prove a wake up call to the selfish.

That happens with 30% of the salary too. Doesn't change the fact that 40% is a crap measure. I guess we could change the measure to 50% in an attempt to breathe a little more life into the market.

Just thinking about it some more, the hideous cost of living in NZ suggests rather than bring higher than 30% (40%), maybe it should be lower than 30% in NZ

It really depends on what you are getting for your taxes and what other major costs you have like paying for education, healthcare etc.

30% seems to be the standard in the US too. Who let the RE industry push another 10% in there??

It turned, yesterday, and not for the better. And to flog a dead horse, one more time,

“Insanity is doing the same thing over and over and expecting different results.”

Remember when the mortgage payments are considered unaffordable if they took up more than 35% of their after-tax pay and is lower still in countries with more truly affordable housing,

But someone somewhere thought that they would redefine the term to miraculously make housing more affordable.

Every $ less in interest payments, you have left to spend on kids swimming lessons, eating out, donating to charity, Hobbies, recreation, learning and education.

So many great things , its better if we spend less on paying banks back.

For those who still aren't willing to put their pesos back into property... has anyone opened a TD with Xceda finance, and if so how was your experience? They're offering 7.75% for 12 months, for 100k or more.. (noting their credit rating is B+.)

I would look at it like this, they probably have a 180bps net interest margin so they are lending at 7.75+1.8 = 9.55%

OK so what person is lending at that rate?

someone who cannot lend off a big 4 bank at 7% for 6 months...

There is simply more risk involved, but its your money and they have fairly stated their credit rating. All the NZ Finance companies where offering higher rates then the banks before the GFC.

i've been saying this for a while, there are affordable houses out there for couples, most that think they are not affordable are either in auckland (understandable) or want a dream, home for there 1st house (slight exaggeration)

RookieInvestor. Bang on just had offer accepted on a property (32 Augustine St Waimate) 3brm solar wet back etc etc got it at 340k here's the big bonus a quarter acre easy subdivision cost 30k I will build my basic 4brm on it same floor plan as last 3 will rent old house out in front for 430 a week plus the new build once down from 500 plus a week. There is so much opportunity out there if you are prepared to look

Good deal! well done.

I like how you do this, buy a property, subdivide and add another house (as long as you leave enough space for some grass and garaging for both properties - taking the renters perspective here rather than the owners obviously). Your situation is unique though in that you're a builder so have the skills, and you have the time (you're in your 70's from memory and this is your job). Out of interest if an owner occupier bought this property what are the work opportunities in and around the area? I see there are only 5 rentals on Trade Me so you won't have a lot of competition to rent them although 2 of them have been available for over a month.

26@Main Am only just in 50s so way short of 70. The last property I did was all raised gardens and tenants didn't want any grass actually out of all my rentals 90 percent don't want grass or a garden to maintain. This new buy (and I haven't got it yet still got to get finance) the old house is very appealing also with the solar power and wet back power bills are around 50 dollars a month a very warm older home. Yes it does need some touch up which a vast majority of people could do like painting etc. Work wise you have two freezing works wanting workers at starting rate 36 dollars an hour you also have two dairy factories wanting workers at similar starting rate. Also being 40 ks either way to Timaru or Oamaru which being South Canturbury and North Otago are quickly becoming the food bowel of NZ the growth in and around Timaru in the last two years since I have been here is vast. My surveyor has 5 years of work ahead of him. Wether you can build or not buying a quarter acre you can still subdivide so like this one 340k 30k to subdivide the surveyor/legal/council contributions, sections at a push 170k so say 150k there's 120k profit in today's money take that off your purchase price plus the 30k. Don't even subdivide build a 60 sqm granny flat on the back. The saying they don't make more land well this is the closest thing to making more subdividing. The potential is there just got to think outside the box. Finally Gary Rooney (look holiday up) local guy is spending big in town has done the last few yrs and is continuing to do so Why, and rather than bitch and moan about things like a lot do he is putting his money were his mouth isn't.

A bit to unpack here Colin but I'll give it a red hot go. For the benefit of Rookie Investor and any other would be property investors I looked up some of your previous comments and you've mentioned 2nd tier lenders, specifically borrowing from Avanti at a floating rate of 9.1, there will be reasons for this. Last year you also commented that you left Auckland 35 years ago and you owned rentals (outside Auckland) at that time so if you're not of the boomer generation you can't be far off. You've had the benefit of investing in property when it was much more affordable

Grass and gardens I agree about the maintenance side of it. Garages you didn't mention so I assume you don't add them. Renters would forgo them in a tight rental market but if there were a few rentals around a property with a garage would likely win out every time. The Works are closer to Timaru than Waimate and in your opinion why would people prefer to live in Waimate when Timaru has more amenities? I found 69 results for properties priced $300k - $400k in Timaru and a couple of them looked to have developmental potential.

If say I bought that property and subdivided off the section to sell would there be much interest in it? I wouldn't think there would be a lot of demand to live on a back section in Waimate (may well be wrong). Granny flat I get, but again, I'd probably choose Timaru and see if I could do it there.

Gary Rooney is a success story for sure and is involved in a few industries - dairy farming, earth moving, transportation and property development, a diversified portfolio. Agree that subdividing makes perhaps better use of land (rather than necessarily making more of it) and I like how you're adding to housing supply. As far as moaning instead of doing something about it, I think a lot of people on this forum are property owners who just want their children and grand children to be able to own property like they did, and sure it's still possible, but it's not as easy as it was to do in the 80's, 90's and early 2000's.

If you get an anonymous delivery to Augustine Street in future it will be a thank you because we have bought an investment property as the result of looking at Timaru property. I asked the partner where we would buy an investment property if we were going to buy one (not Timaru as we don't know the areal). We agreed on a location, looked at Trade Me, found a property we really like in a location we're familiar with and in a price range we can easily afford so we're going to the open home this coming weekend.

It's all good don't need a delivery again look at Ashburton rather than Timaru closer to Christchurch people travel to work from there pro council similar to timaru in money. Alot going for it. If this deal falls over will most probably look there myself

Timaru is a bit harder to find the bigger sections to subdivide, so more exspensive also council contributions.If I was you I would look at Ashburton. As the section sizes can be as low as 350 sqm so a quarter acre gets 3. Yes I always put a garage on use to a dble but that limits house size so now go to single allowing that 20 odd extra meters can go into the house. All thou talk to a insurance company most garages these days are only used to store more crap. 2nd tier for a couple of reason although I do have mortgages with ANZ Avanti at mo I got 8 percent because high equity. Looking at pepper. As don't want all eggs in one. First rental was paying 18 percent interest so hardly affordable didn't have mortgage brokers had to go to bank manager kiss their arse . Didn't have the competition in the banking industry like now and couldn't have easy access to knowledge like now. So while there are disadvantages for young people today in buying a home there is also advantages.

Giving it more thought I get that it makes sense to go to those smaller places where you get bigger section sizes for cheaper prices and you can subdivide and build. Also, I see what you mean about Gary Rooney and his specific investment in Waimate. It's great he's doing that and reinvesting into his community to rejuvenate the place, we need people just like him all around NZ. I hear you about the garages, I walk past double garages often that are filled with everything but a car. Good point about the changes in the banking industry and access to knowledge. If we do buy another property it will be in the North Island and likely close to home so we can easily keep it in good order and find tenants where necessary. Thanks for adding to housing supply.

This shows why AKL is so out of whack to invest in....

"Interest.co.nz tracks the mortgage payments for a home purchased at the Real Estate Institute of New Zealand's lower quartile selling price in each major urban district, and compares that to the median after-tax wages of 25-29 year old couples."

So two full time employed earning median wages and lower quartile property...and still over 40% of take home....best hope no one gets made redundant anytime soon.

thats not true, lower quartile in hamilton is 533K with 20% deposit thats a 430K mortage.

with 2 median incomes at 60k each (120K) you take home $1683/ week and mortage repayments are $654 a week.

that is 40% of take home pay pretty much.

"That latest figures show the percentage of typical first home buyers' take home home pay that would be taken up by mortgage payments on a home purchased at the national lower quartile price with a 10% deposit, has declined for the last three consecutive months, from 43.8% in March to 41.9% in June."

National lower quartile is skewed by auckland prices.

People with 10% deposit either haven't been committed enough or are going for houses outside their price range.

This isn't reasonable data to go by. Couple in the 25-29 yera range should atleast have a 20% deposit.

Tbh I pretty much exclude auckland for fhb, but kudos to anyone who can

It's tight everywhere you look. We crash landed the plane during covid & tried to print our way out of it. So far, it's... mostly working. I'll give it a C. A pass with a push. That shouldn't detract from the fact that the decision-making processes during covid were utter crap at both political & financial levels, thus creating the current environment. Sigh. Way too much meddling for me.

If you can get approved for a loan.

I work with 16 people, who are all 20's to early 30's.

Two have bought houses this month. One FHB, the other replacing FH red stickered in Akld Anniversary floods.

Others in the team have already bought recently. For the first time in a long time this age cohort now believe property ownership is possible.

Great to hear!

Whats your take on how each feels about their house buying, happy/pleased, concerns/regrets

It is a major topic of discussion around the coffee machine, excited and nervous. Daunted as they come to grips with the purchasing process and work out all the large and small details, from finding a lawyer for the first time, through to working out what school will be best in the new area.

It is ultimately a feel-good process for everyone to watch this next stage of life that we either went through, or hope to go through.

So this is for a couple and after saving 20k each year for 4 years then have to put 57% of wages to maintain a mortgage in Auckland for maybe a two bedroom cheap flat or house totally unaffordable the house price crash will continue.

Life goes on, FHBs strive to make a better life for themselves and their families, and the desire for home ownership is still part of their DNA.

I'm surprised to see the amount they can tap from their Kiwisavers. A bit like our parents capitalising on the Family Benefit.

The boomers in these comments trying to prove NZ still offers great opportunities for 20-30yos are extremely out of touch.

Do you have any clue how many are leaving NZ or the ones that are staying put, what their realistic understanding of getting a property is?

Leaving for places that are just as un affordable

Really?

Housing is somewhat more affordable in Melbourne (for example), than Auckland.

Salaries are higher, and cost of living significantly lower.

Be honest mate its not cheaper, at least for the places people would prefer to live. You end up doing massive travel distances. The prices of anything was a total joke when I visited there many years ago, it was like Ponsonby on steroids for anything central. Australians also treat Kiwi's like shit, you would have to be pretty desperate to head over there, anyone top of their game can make it over here.

Zwifter house I just put offer on the vendors are selling as daughter who is a nurse and is coming back from Aus as it didn't measure up to what she was lead to believe. So they are all going into a house together

This is just demonstrably untrue. To don’t even need to go there. You can just look at a real estate site

Unless they’re going to Hong Kong or San Francisco (or maybe Sydney), they’re not.

Depends on where you choose to live!

The happiest city in NZ is still affordable but prices are going go increase.

The reality is that the main cities in Oz are more expensive so it is what it id.

I can assure you if you buy well, improve and sell and move up the ladder, then things will be fine.

I can also assure you that if you do nothing and just want to sit on the sidelines and moan then things will never ever be better financially unless you inherit .

The main cities in Aus are not more expensive at all. Sydney is on par, but the rest are definitely more affordable.

Your advice only works in a reliably appreciating market. The ladder is falling over.

This is just vapid boomer BS

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.