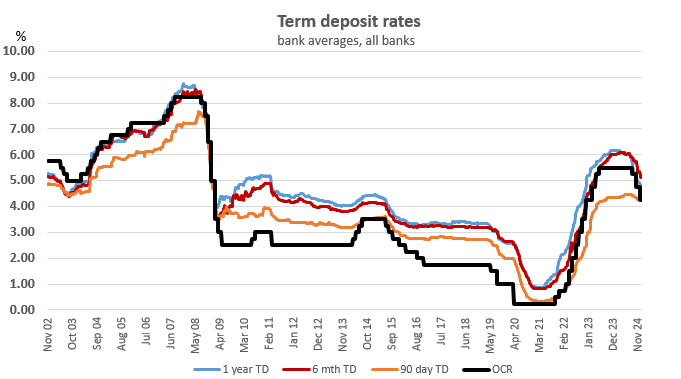

2024 has been a year when savers lost some of the big gains they got in 2023.

Those 2023 gains brought back fond memories of the very high rates savers enjoyed just prior to the GFC.

After the GFC, things fell apart somewhat and they had to suffer a long period of below-inflation yields. So the 2023 rise was a welcome development.

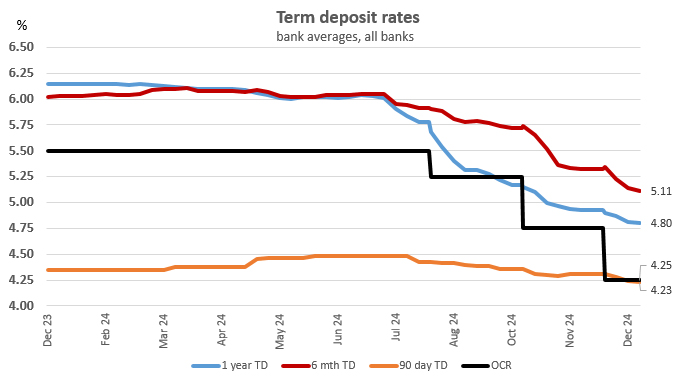

But 2024 was a roll-back year. Not all the way to the pandemic depths, but enough to grab some attention, and enough to wonder about what 2025 might bring.

Of course, the average shift varied between deposit-taker institutions.

The following table tracks the net change from where we started the year, to where we finished.

And we have now included the registered Non-Bank-Deposit Takers. And that is because there is less than 200 days until it will seem like they can front it with the banks, because they will be in the Deposit Compensation Scheme, which guarantees up to $100,000 won't be lost in the event of an institution failure. The taxpayer will make the depositor good.

Readers should note that the RBNZ will be charging institutions a fee for that protection. But the fee will be entirely risk-based - that is based on each institution's risk profile. A key risk they will be looking at is liquidity risk. The more risk, the higher the fee, and that may well impact Non-Bank Deposit Takers harder than banks. In turn, that will likely mean they will be unable to offer interest rate returns to savers in the way they did in 2024. Only time will tell how these factors play out for each institution. And there could well be risk differences between community-based institutions and finance companies.

| January 2024 | December 2024 | |||||

| 3 mth | 6 mth | 1 year | 3 mth | 6 mth | 1 year | |

| % | % | % | % | % | % | |

| Main banks | ||||||

| ANZ | 4.20 | 6.00 | 6.10 | 4.15 | 5.05 | 4.75 |

| ASB | 4.20 | 6.00 | 6.10 | 4.15 | 5.05 | 4.75 |

| BNZ | 4.20 | 6.00 | 6.10 | 4.10 | 5.10 | 4.75 |

| Kiwibank | 4.20 | 6.05 | 6.15 | 4.20 | 5.10 | 4.80 |

| Westpac | 4.20 | 6.00 | 6.10 | 4.30 | 5.05 | 4.75 |

| Challenger banks | ||||||

| Bank of China | 4.90 | 6.00 | 6.15 | 4.50 | 5.35 | 5.00 |

| China Construction Bank | 4.70 | 5.85 | 6.00 | 4.30 | 4.95 | 4.80 |

| Cooperative Bank | 4.20 | 6.10 | 6.20 | 4.15 | 5.15 | 4.80 |

| Heartland Bank | 4.25 | 6.05 | 6.30 | 4.35 | 5.15 | 4.85 |

| ICBC | 4.90 | 6.00 | 6.15 | 4.50 | 5.35 | 4.95 |

| Rabobank | 5.05 | 6.15 | 6.30 | 4.35 | 5.10 | 4.80 |

| SBS Bank | 4.20 | 6.05 | 6.15 | 4.15 | 5.10 | 4.80 |

| TSB | 4.25 | 5.90 | 6.00 | 4.15 | 5.05 | 4.75 |

| Non-Bank Deposit Takers | ||||||

| Christian Savings | 4.40 | 6.05 | 6.15 | 4.40 | 5.15 | 4.85 |

| Finance Direct | 3.95 | 6.50 | 3.95 | 6.50 | ||

| First Credit Union | 4.75 | 5.75 | 6.50 | 4.25 | 5.45 | 4.90 |

| General Finance | 7.00 | 7.50 | 4.20 | 6.30 | 6.50 | |

| Gold Band Finance | 4.00 | 6.75 | 3.75 | 6.40 | ||

| Heretaunga Building Society | 4.35 | 6.10 | 6.25 | 4.30 | 5.15 | 4.85 |

| Liberty Financial | 4.75 | 6.60 | 7.10 | 4.25 | 5.85 | 5.50 |

| Mutual Credit Finance | 7.00 | 6.50 | ||||

| Nelson Building Society | 4.20 | 6.00 | 6.10 | 3.90 | 4.85 | 4.55 |

| Police Credit Union | 4.10 | 5.95 | 6.00 | 4.10 | 5.05 | 4.75 |

| UnityMoney | 4.20 | 6.00 | 6.00 | 4.15 | 5.00 | 4.55 |

| Wairarapa Building Society | 4.20 | 6.00 | 6.25 | 4.05 | 4.50 | 4.75 |

| Xceda Finance | 6.85 | 7.50 | 6.50 | 6.40 | ||

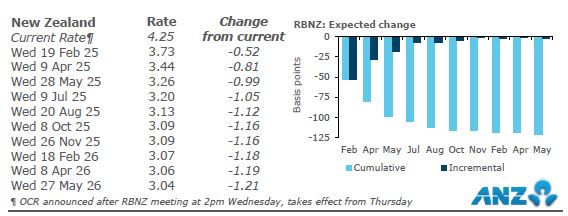

So then the question becomes, what will happen in 2025?

Regular readers will know that we don't predict or forecast future rate levels. But the financial markets do, by setting forward pricing. This isn't infallible, and as each circumstance changes, that pricing in adjusted (as it should be). In 2024 there were many adjustments, so what these markets priced for 2025 at the start of 2024 turned out to be quite different to what they priced at the end. No-one should be surprised. That is just how financial market pricing works, and always has done.

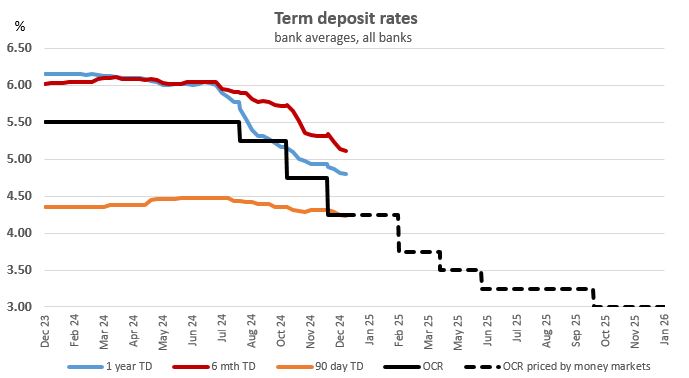

This is what is priced in as at December 20, 2024, for the year ahead when looking at the OCR.

We can add that to our 2024 charting. That might help you think about what could be in store for term deposit rates in 2025. Stay short? or go long from here? Nobody knows the future, especially spruikers pitching their products. Your judgment will be as good as anyone's, and probably better than anyone conflicted by salesmanship. If it seems to good to be true, it almost certainly is.

The above chart has been updated/corrected.

30 Comments

Very happy with my chunk of TDs. I don't try to maximize the return too anxiously but do pay it some attention. Currently most on six month rollovers.

Agree fully with David about not trying hard to predict.

Reliable and available. They have their place as part of the bigger scheme.

Not worried about recent rate drops. Largely the interest rate / inflation relationship. It's much the same.

I'd put good money on that OCR track being completely wrong by at least 1% - possibly even 1.5%.

;-)

TD rates will be high 4's for 2025. Of course if it all turns to custard and we follow Venezuela then we will be rolling in it. I'm currently on a 6 month with interest paid monthly. 50/50 call on the rates going up or going down, depends on the carnage Trump is about to unleash.

"if ... we follow Venezuela "

And why would that happen, Zwifter? Once again, you don't say why.

Suspect inflation will remain and possibly increase if Trump applies tarrifs, knock on effect on mortgages and consequent further reduction in discretionery spending makes 2025 an unpredicatable year with more downsides then upside.

South Canterbury finance 2?

Very possible when you look at some of the names....Cant understand why the bar is so low.

Why? Where?

Neither you, Justa comment, nor Uninterested, provide any substance. Maybe stick to "X"?

I don't like to give the names on a public forum. Let's just say look at the 3 that are offering 1 year TDs now for 6.4 & 6.5%. I suspect that uninterested may be over 50 like myself and have seen finance companies like these fail many times over the years. I don't think the government guarantee should be given for B grade finance companies. They are there for riskier loans and thus deposits which is fine, but the taxpayer should not have to bail them out.

And 1 yr Kiwi bonds at 4.25% 1/4rly compounding are looking attractive at present too.

But they will have to be because otherwise with their security advantage being nullified, nobody would go for them.

Government bonds will always be lower risk than insured deposits. Cyprus had deposit insurance during the GFC, but when everything blew up they just decided not to pay out. If a government doesn't make good on its bonds then it bankrupts itself, which is far less likely to be allowed to happen.

A bit academic perhaps, but still true. If Kiwibonds and insured TDs were offering the same return, I know which one I'd prefer.

Cyprus vs. NZ? Are they similar?

hey David, do you have any coverage on Jardin Direct lately? I got some emails saying their brokerage business has sold to Hatch.

Yeah, and they say it happened back in 2022.

I was thinking I'd forgotten that but also thinking maybe Jardin had forgotten to mention it.

Term Deposits are not an investment that gives good enough returns to keep up with inflation.

Unless you have large amounts amounts in them they do not return enough to make them worthwhile.

If you want to park money up with little downside with a Trading Bank then they are ok.

Personally know there are far more rewarding returns through other investment vehicles.

Merry Xmas to all.

Listen to The Man. TDs are basically just treading water, if you're lucky. What you really want is an investment that keeps its value and generates an income. TDs do not keep their value if you spend their return. If you don't spend the interest then you are not really getting a return. Kind of a bottom tier investment when you think about it.

Yep but as safe as houses.

TDs have their place because they are pretty safe. To me there is lots of value in that "safety" and the guarantee of a set return especially when it's beating inflation relative to your goal (such as buying a house for example, with houses having decreased in value while your house deposit parked in TDs increased during the same period).

TDs also make sense for retirees, etc.

Yes they are not bad for retirees only paying 17.5% tax, and they don't do things like FBU $12 to $3, or RYM $16 to $4, or ATM $20 to $6 etc etc etc. Oldies don't need stress!

HI Mystery.

Your comment suggests that you are perhaps not familiar with 'The Great Taking"?

The risks involved in all paper assets including Term Deposits have been exposed by David Rogers Webb in his very brief but epic book entitled 'The Great Taking' - see PDF download link -

It turns out that the DTCC (Depository Trust Clearing Corporation) and its nominee company Cede & Company are now owners of a huge percentage of the stocks/securities/bonds etc around the world and that most of us are merely beneficiaries at best, not owners of these paper assets.

The very name that the acronym DTTCC stands for is dodgy enough, but how sinister is the name 'Cede'? - the definition of this word - TO SURRENDER POSSESSION!

Cede & Co. is now the owner of record of all of our stocks, bonds, digitized securities, mortgages, and more; and it is seriously under-capitalized, holding capital of only $3.5 billion, clearly not enough to satisfy all the potential derivative claims - this massive anomaly appears to be deliberate.

Furthermore, the fact that the derivative holders have first call on these assets in any crisis, and can in fact just sell them off without any due process whatsoever, even perhaps simply in a situation of perceived risk, adds another layer of risk to owning/buying paper assets.

Add into the equation the international bail-in laws and all of this looks like a nasty accident waiting to happen.

Some time ago I worked out the derivative/equity ratios on some of the largest TBTF banks - what I saw was a shocker, especially in regard to Citibank and Goldman Sucks.

GS 1,117:1

Citibank 330:1

JPMC 187:1

BOA 103:1

Wells Fargo 97:1

With these totally outrageous levels of derivatives on their books, this situation poses an enormous risk to holders of paper assets all over the planet in any sort of financial crisis, let alone a systemic meltdown that could eventuate from the Western money casino at any stage.

David Webb's summary of this very short freely available PDF book...

It is about the taking of collateral (all of it), the end game of the current globally synchronous debt accumulation super cycle. This scheme is being executed by long-planned, intelligent design, the audacity and scope of which is difficult for the mind to encompass. Included are all financial assets and bank deposits, all stocks and bonds; and hence, all underlying property of all public corporations, including all inventories, plant and equipment; land, mineral deposits, inventions and intellectual property. Privately owned personal and real property financed with any amount of debt will likewise be taken, as will the assets of privately owned businesses which have been financed with debt. If even partially successful, this will be the greatest conquest and subjugation in world history.

Regards

Colin

And Google Books lists it in the conspiracy theories category: The Great Taking - David Rogers Webb

True to form, Colin. Keep up the good? work ... /sarc

Define the amount you call large The Man 3 ? Its all relative to the amount you have invested. Its like Crypto and raving about the returns but if you only have $1000 in it, who cares.

Its like Crypto and raving about the returns but if you only have $1000 in it, who cares.

Term deposits and crypto are fundamentally different Z. A term deposit holder is a creditor to a bank whereas a crypto owner is not necessarily a creditor to anyone (however crypto can be used as collateral for loans).

F'more $1000 is not a lot of moolah, but important to remember that approx 50% of retail bank accounts only hold that amount (The NZ Banking Association states the average savings account balance in June 2024 was $15,800).

Cut the techno crap, J.C.

A holder of TDs will get 100% of their money back almost regardless of what happens.

Holders of crypto? Sorry, all bets are nonsense. Confidence, like in tulips, can evaporate extremely quickly.

Furthermore ... statements like ...

"$1000 is not a lot of moolah"

... are simply a classic case of pumping the crypto ponzi. I.e. the ponzi collapses if fools aren't encouraged to pump in any amounts, no matter how small, to prop up the ponzi before it collapses.

Shame on you.

A holder of TDs will get 100% of their money back almost regardless of what happens.

In Aotearoa term deposits are generally classified as 'unsecured investments'. This means that they do not have specific collateral backing them, and in the event of a bank's insolvency, depositors are treated as unsecured creditors.

Depositors, as unsecured creditors, also rank in liquidation behind covered bond holders and other creditors preferred by law (e.g. employee entitlements and taxes). Specifically, covered bond holders have both an unsecured claim over the bank and an interest over a specific pool of the bank’s assets set aside from unsecured creditors, including depositors. Positively for depositors, the RBNZ has limited each bank’s covered bond issuance to 10% of its assets.

I am very happy with TDs.

But ya gotta remember both BNZ and Westpac turned very marginal thru to broke within recent memory. And you can be sure they won't be telling us about it if something again gets perilous. But still watch them as best you can.

On the other hand JC seems to live in fantasy land. Specifically (a) overcome plus plus, and seized by the idea of exploding value. And (b) tells us it's a store of value. Both contradict.

On the other hand JC seems to live in fantasy land. Specifically (a) overcome plus plus, and seized by the idea of exploding value. And (b) tells us it's a store of value. Both contradict.

Describing TD holders as creditors to banks is not fantasy. I suggest you carefully study about this if you think otherwise.

Also, that digital assets are not necessarily the same as TDs in terms of being a 'creditor' is also not fantasy.

When individuals deposit money in a bank, they enter into a creditor-debtor relationship. Legally, once a deposit is made, the funds become the property of the bank. Essentially that is fundamentally different to most digital assets.

Above about $2,000 or $5,000 depending on bank, the amount on term deposit does not change the % return.

If you are on the 10.5% tax rate, term deposit returns are really quite good in my view.

Unless of course get-rich-quick is the aim.

Lot of opinion here. Why don’t you tell us how quickly you made your last million and what strategies you employed for our education?

I'm not a qualified financial advisor so don't hold me responsible to what I say below:

A week or so ago the NZX published an announcement advising that Milford had purchased just under 14 million Spark shares at about $2.86 per share from my calculation.

So lets look at the current status of Spark shares:

The current net dividend yield is around 9.7% ( they have recently reduced their dividend to 25 cents a share from around 28 cents a share as their net profit has understandably dropped somewhat because of the recession.)

The lowest price per share over the last 52 weeks was $2.76 per share.

At today's close the share price was $2.83.

They do pay a sizeable imputation each dividend payout.

Make of this what you will....just saying...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.