The country's bank mortgage pile grew by the biggest monthly amount in October in nearly three years, according to the latest Reserve Bank (RBNZ) figures.

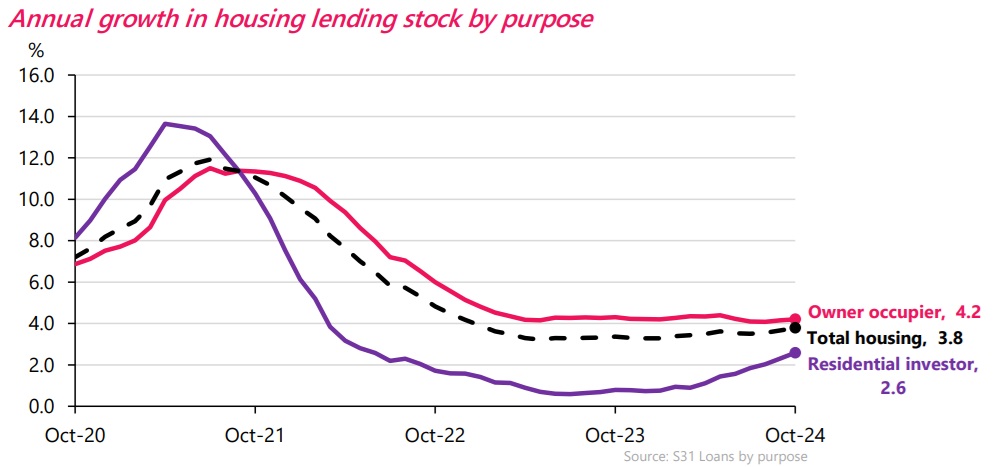

The RBNZ said the banks' total housing lending stock increased by $1.58 billion in October 2024 to a grand total of $360.58 billion. The housing lending annual growth rate rose from 3.7% to 3.8%

This was the biggest monthly increase since a $2.049 billion rise in December 2021.

In October 2024 owner-occupier lending increased by $1.187 billion (to $268.039 billion) while residential investor lending increased by $393 million (to $92.54 billion).

In the past six months to October, the investor mortgage pile has grown by $1.696 billion - and by $2.155 billion for the year to date.

This contrasts with an increase of just $345 million for the whole of 2023 and an increase of $1.4 billion for the whole of the 2022 calendar year.

In 2021, which included the tail-end of the pandemic housing boom, the residential investors increased their mortgage pile by $7.697 billion.

Separately, other RBNZ data for October shows the outstanding amount of money on floating rates rose by the most in a single month since June 2011.

The amount outstanding on floating rates rose by $2.966 billion to $42.744 billion in October. The total amount of money on floating rates is now at its highest level since March 2020.

In October the amount of mortgage money on fixed rates dropped by $1.356 billion to a total of $323.317 billion, which was the biggest monthly fall since December 2011.

Floating rates were much more popular than fixed rates in the wake of the Global Financial Crisis (GFC) because for quite some time they were lower.

More recently the fixed rates have been lower than the floating rates. However, with the Reserve Bank now reducing the Official Cash Rate (it's been dropped from 5.50% to 4.25% since August) there may well be some people prepared to wait on a floating rate to see what happens in coming weeks and months.

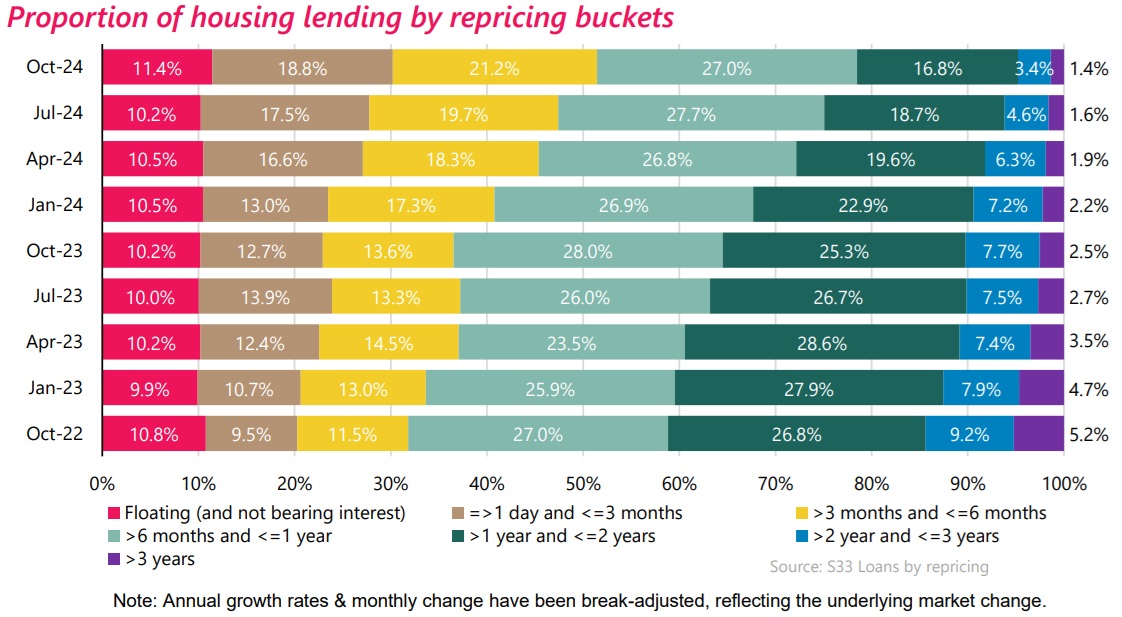

The general trend since the start of this year has been for people to go shorter and shorter with their mortgage rate terms in order to take advantage of likely rate falls.

The October data shows that including floating rate mortgages, over 51% of the outstanding mortgage pile is due for a rate reset within six months, with over 78% due for a reset within a year.

Meanwhile, non-performing housing loans increased by $88 million (4.4%) to $2.109 billion in October, which is the first rise in three months.

The non-performing total rose $690 million (48.6%%) in the 12 months to October 2024.

The amount of non-performing loans represents 0.6% of the outstanding stock, up from 0.4% in October 2023.

In the aftermath of the GFC the non-performing loans percentage frequently hit 1.2%.

21 Comments

Investors are back.

Construction crumbling.

Rates down.

Buckle up for the boom bitches!

🥂

you can't deny that's a turn in the market...

I wouldn't make any claims until statistics showed the situation clearly. But I am not a spruiker.

I can and I will. The honey trap has been set. Watch and learn.

You need bees for a honey trap...many fleeing the hive this time..

Recent history reveals spec-investors weren't the smartest bunch. I say this based on when lending last took off 2020/21 and what happened straight afterwards. It's now easier to see. Will this time be any different? Momentum could create more momentum and draw in more debt addicted fools and invite an even bigger downside risk.

If this transpires to be a bottom of this cycle (which personally for the good of our country hope not) then it's from a still vulnerable and stretched valuation vs incomes point. From here the risks of an even bigger correction will only grow.

Plenty on here will try Rookie. I did say you had until December to buy.

Out of curiosity, what happens to people who aren't in a position to buy? Let's say anyone under the age of 25 today. Are they just screwed in your framework? House prices will continue to rise in real terms above wages so kids today are basically SOOL?

Do you not have kids yourself? Are you not concerned what the market will look like for them if we get a repeat of the last 20 years?

Personally I believe house prices will rise to the point it will trigger blowback in the form of land taxes, private landowners capturing public/business investment based price rises in their land will flow to government. But I can't imagine you believe that so what is the 10/20/30 year view on this for you?

Someone under the age of 25 buying a house these days is pretty unrealistic. I didn't buy until I was in my early 30's. The market is what it is, no point complaining about it, not everyone gets to own a house, nothing has changed. You buy in with friends, another couple or get flatmates like I had to. You simply have to get a decent education, a decent job and put buying a house at the top of the priority list. Its just unfortunate that a whole lot of shit has evolved now in society now that interferes with the basics of owning a home.

Greg Ninness thinks it is reasonable to assume 25-29 as the age for FHBs. I think the average these days is around 35

The scenarios are so varied from the young professional couple under 25 with great jobs that get married and have well off parents both sides that throw them $100K each for the deposit and boom they are in the million dollar house to someone who is single and late 30's before they get into the market and are prepared to make some serious compromises to do so for the next 15 years. It must be closer to 35 these days, the "Must have" university education has pushed it way out.

Anyone buying a house with parental help is effectively just experiencing hyper local wealth redistribution from boomers/genx downwards. More than 50% FHB are already tapping bank of mum and dad for large chunks of deposits and I know many anecdotal cases of further support from parents in paying off the loan.

So the gains that middle class property investors got from buying early is being recycled into...housing for their kids. This is a highly unstable housing structure is my analysis and highly vulnerable to legislative and taxation changes as an investment strategy. The lack of options to realise gains without selling also further distorts the market in financial terms.

FYI FHB age is 35-40, up 10 years from the 70s. And 1971 is of course when the Nixon shock occurred and global monetary economics started its current (unsustainable) trajectory.

Not only the education - it also takes longer for many to save the required deposit

I'm early 30's most of my friends either have a house or could have one just don't want to, id say 2/10 of them couldn't afford it.

I don't mean someone under 25 buying, I mean when those people reach the age of FHB (which has steadily risen for decades).

Fundamentally something doesn't add up here just based on the maths. Housing cannot perform the same way over the next 20 years as the last 20 in real terms without more and more people not owning homes leading to political blowback and things like land taxes etc (as land price rising is what has driven the housing market up, not improved properties which depreciate like manufactured goods such as cars etc).

As soon as private landowners can't capture that land gain, the willingness to leverage via mortgages tanks as people will be massively overpaying for the asset in real terms.

I don't think people really grasp how the housing crisis globally is fueled by NIMBY style regulation and private capture of land value rises. If those two foundations change (as it is already in many countries) the whole investment thesis for property gets upended. And the dynamics of rising prices (faster than real wage growth) mean more voters with less investment in protecting property gains.

Anyone buying now based on realising the investment more than 15 years away is going to end up disappointed IMHO. The 40 years from 1930-1970 taught bad lessons on how to invest from 1970-2020. I expect the same will be true from the 2020-2060 period.

‘Construction crumbling’ - lol, as desperate as Mr Ed (McKnight)

huge number of completions over the past few months that haven’t managed to sell. Massive overhang.

As I correctly predicted two years ago, consent numbers have collapsed and eventually new dwelling completions will too. But that’s at least 3-4 months away. Maybe in 2-3 years lower levels of new housing supply will start to become a factor supporting higher prices.

don’t forget that net migration is much lower than it was last year

This is so often compared to the GFC, but once it is over what will we call it? The Chinese Financial Virus? CFV?

Orr Overstimulation Syndrome (OOS).

i feel like its not unique to NZ, maybe slightly exaggerated.

Nice work

The period from 2008-2030 will be known as the period fiat went hyperinflationary and collapsed. Arguably already has gone hyperinflationary when looking at global asset prices (which arent included in inflation figures for this reason).

World moves from the post Bretton Woods system that has existed roughly since 1971.

Things will be split into pre/post crypto dominance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.