Table 1: Gold lost ground in US dollars, but the fall was mitigated in other currencies by the same dollar strength

Personal Finance

/ opinion

The World Gold Council explains what has been happening with gold since the US election, and what its prospects are from here

14th Nov 24, 12:25pm

by

Analysis by the World Gold Council.

The first week of November saw gold move lower after hitting a new all-time-high on the first of the month (Table 1).

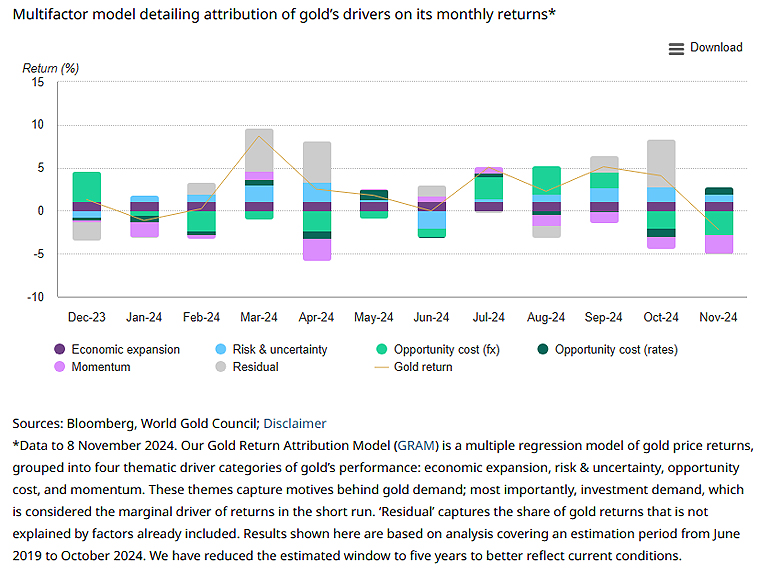

According to our Gold Return Attribution Model (GRAM), gold was pressured lower by strength in the US dollar and momentum factors including the lagged gold price, gold ETF outflows which were coming off an exceptionally strong month, and a drop in COMEX net managed money net longs – reflecting the likely unwind of pre-election hedges (Chart 1).

Global gold ETFs shed an estimated US$809mn (12t) during the first week of November, with the bulk of outflows stemming from North America, which were partially offset by strong Asian inflows. Potentially signalling renewed fears around the resumption of the trade war between the US and China. Additionally, COMEX net positioning also fell 74 tonnes, an 8% drop from the prior week.

November review

The start of November saw gold pressured by higher opportunity costs and a Republican clean sweep.

Looking ahead

Stronger bond yields and US dollar, risk-on in equities, a boost to cryptocurrencies and quelling of geopolitical risk might see a near-term retracement in gold.

Chart 1: Higher bond yields, a stronger US dollar and US election results took the sting out of gold’s y-t-d rally

Performance of gold in various currencies*

| USD (oz) | EUR (oz) | JPY (g) | GBP (oz) | CAD (oz) | INR (10g) | RMB (g) | AUD (oz) | |

| Nov. week 1 price | 2,691 | 2,511 | 13,207 | 2,083 | 3,744 | 73,003 | 622 | 4,088 |

| Nov. week 1 return | -1.6% | 0.0% | -1.2% | -1.7% | -1.7% | -1.2% | -0.7% | -1.6% |

| Y-t-d return | 29.5% | 33.4% | 40.1% | 27.6% | 36.0% | 31.3% | 31.0% | 34.0% |

*Data to 8 November 2024. Based on the LBMA Gold Price PM in USD, expressed in local currencies.

Source: Bloomberg, World Gold Council

Looking ahead

- The US election results have taken a bit of a knee-jerk sting out of gold’s impressive y-t-d rally. Suggested reasons are a continued strengthening in bond yields and the US dollar, risk-on sentiment in equity markets, a boost to cryptocurrencies and a quelling of geopolitical tensions

- These factors might presage a welcome pause, even a healthy near-term retracement, for gold.

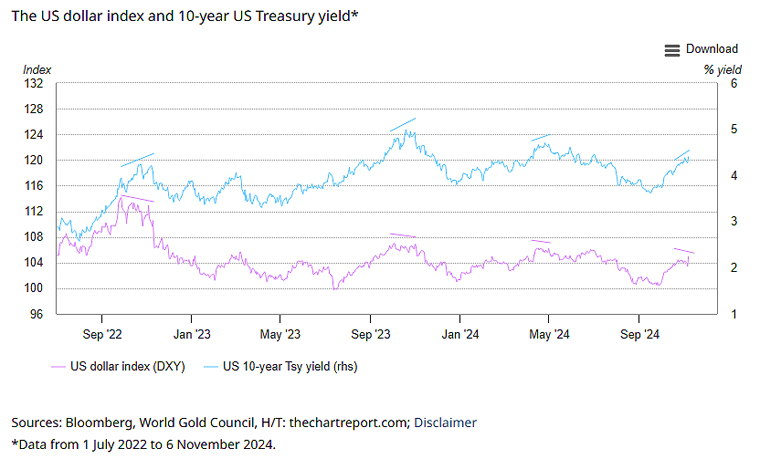

There was a sense that the pre-election run up in Treasury yields and the US dollar might have been exhausted and that a turn in the dollar might lead bond yields lower – as it has done on several occasions over the last two years (Chart 2). After all, the dollar is richly valued on a real effective exchange rate (REER) basis1 and a Trump administration is said to favour both a weaker exchange rate to encourage exports and lower interest rates to spur borrowing.2

Chart 2: The US dollar index has peaked before yields

However, the Republican sweep has gone hand-in-hand with an acceleration of the run up in yields and a quick reversal higher in the dollar index as well – driven by a sharp and nervous move lower in the euro and yen.

Turning our focus to the move in yields and the dollar. A confluence of factors are at play:

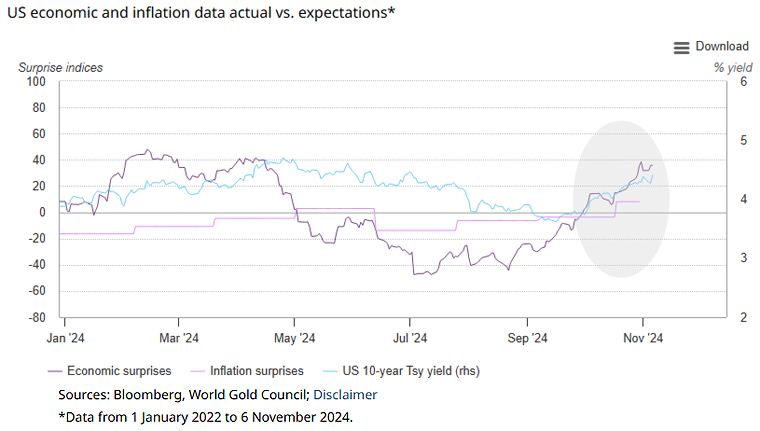

- Positive US economic and inflation surprises (Chart 3)

Chart 3: Data has been hotter than expected

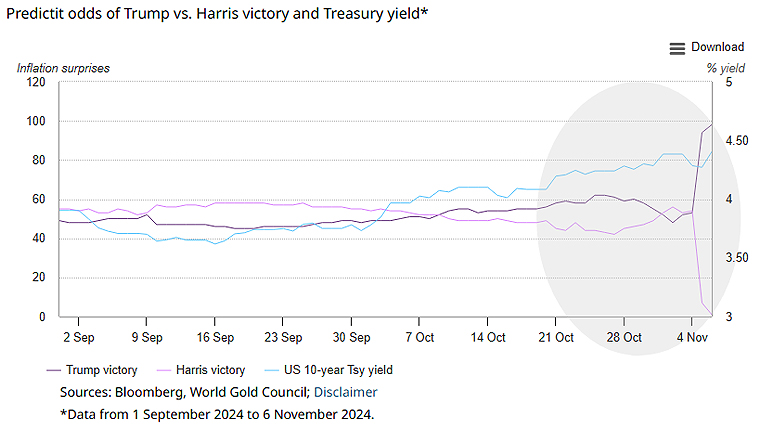

- Expectations of a Trump victory (Chart 4), with inflationary policies including tariffs, tax cuts, cuts to immigration and high levels of spending, are another factor. For example, infrastructure spending likely generates a GDP multiplier of about 1.4 vs tax cuts at 0.2.3 Trump’s policies sway towards the latter so debt might become an even bigger issue if not productive.

Chart 4: Republican odds increased opportunity costs

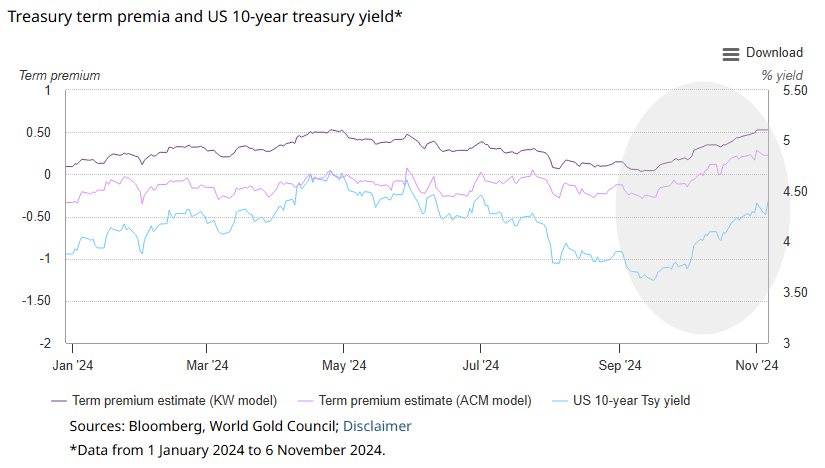

- A rising term premium whereby investors saddled with US Treasuries need higher yields to be enticed into holding them (Chart 5).4

Chart 5: A rising term premium contributing to yields

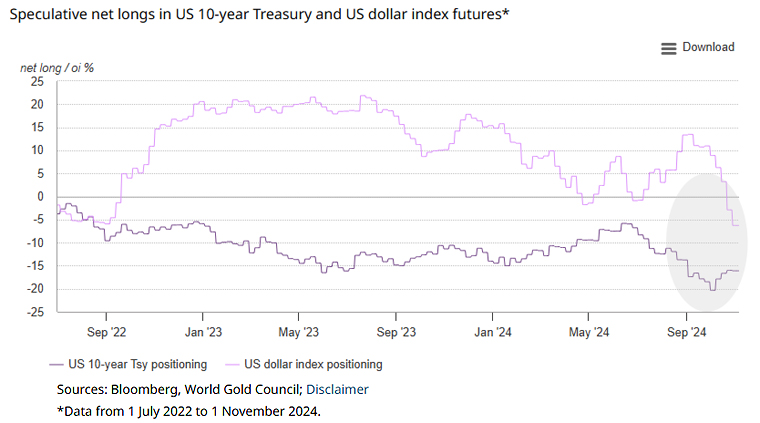

- Overly dovish outlook as positioning in Treasury and US dollar futures had become somewhat stretched (Chart 6).

Chart 6: Futures positioning got over-extended

Added to the dollar and yield impact are concerns that cryptocurrencies are now currying more favour with the incoming US administration. And equity markets, particularly in the heavily weighted technology sector, have been given a further boost from expected ‘business-friendly’ policies.

Finally, murmurs that sanction risks might have been reduced given the incoming administrations purportedly less combative stance could also weigh on sentiment towards gold.

Yet despite these headwinds, we believe there’s still fundamental support for gold. And if it’s a retracement, we don’t expect it’ll develop into a rout:

- Gold has been taking fewer cues from US yields and the dollar of late with most of the returns in October (as well as during much of 2024) taking place during Asian trading hours. Some of this buying may have been ‘sanctions-related’, but central bank buying slowed in Q3 so it’s likely investor-led too. And now, Trump’s tariff policies have the potential to put more pressure on Asian equity markets. The weakness in China’s CSI300 index has been one factor contributing to stellar gold investment demand in the country during 2024

- The fiscal policies under a Republican sweep are likely to be inflationary: tariffs, immigration policy, tax cuts and a desire for low borrowing costs (although strictly, this fall under the independent purview of the Federal Reserve) have the capacity to weigh on inflation readings. In addition, excessive deficits will continue to exert pressure on the creditworthiness of US Treasury bonds, a suggested driver alongside sanction risks of global central bank gold demand5

- And for bond investors, c.4.5% nominal yield on offer for long bonds will probably continue to look insufficient, given inflation’s smouldering embers and the continued positive stock-bond correlation

- Equity markets are already richly valued. Any adjustment to valuations from expected favourable tax policies should be priced in quickly. Should there be a cut to the CHIPS and Science Act,6 for example, that would likely result in a downward adjustment to the technology elements of the US equity indices. If the administration doesn’t roll back those expenditures,7 deficit concerns will continue to pose an issue and that is – all else being equal – gold friendly.

In summary

In summary, gold’s negative reaction to both the US election results and a continued move higher in bonds yields and the US dollar is in our view a near-term phenomenon. Other drivers including lower sanctions risks, a renewed bullishness in equity markets and cryptocurrencies mask the underlying – and in our view – more fundamental concerns of:

- A world where protectionism is likely going to be more acute and current conflicts see no signs of abatement

- Equity markets are heavily concentrated and richly valued during the end of a business cycle

- Cryptocurrencies continue to be a marginal consideration and not a replacement for gold

- Western investors have, outside of futures, not added much gold this year and so there is unlikely a slew of sellers in the wings.

Footnotes:

1. The US dollar ranks at the 97% percentile relative to historical values since 1989 using the CITI real effective exchange rate index from Bloomberg.

2. Trump Wants a Weaker Dollar. That Will Be Easier Said Than Done. - WSJ

3. Investing around the election and debt issue | BlackRock

4. The term premium and the bond vigilantes

5. Goldman sees potential for gold prices surging above $3000 amid geopolitical risks by | Investing.com

6. FACT SHEET: CHIPS and Science Act Will Lower Costs, Create Jobs, Strengthen Supply Chains, and Counter China | The White House

7. Trump likely to uphold CHIPS Act despite his campaign rhetoric, experts say

This article is a re-post from here. All references and Notes are in the original analysis at that link.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

1 Comments

I suspect the US dollar rise is short lived as the DUMBsters insane and totally dangerous and ineffective cabinet appointments and flawed policies will cause the US to implode and Gold will have a meteoric rise..and it won't be long. The only alternative is something that cannot be voiced here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.