Over half of the country's mortgage pile is due to have its interest rate reset within six months, according to the latest figures from the Reserve Bank.

We've reported previously on how mortgage customers have been stampeding to ever-shorter fixed-term mortgages in order to get the best bang for their buck as soon as expected interest rate falls come to pass.

This trend started in earnest at the beginning of the year and has continued at pace.

And it's looking like the moves are paying off for customers, with the Reserve Bank (RBNZ) having already now cut (since August) the Official Cash Rate (OCR) from 5.5% to 4.75% - and with more cuts expected.

Banks started cutting their mortgage rates even before this.

The advantage for going 'short' with a mortgage fixed term is that the mortgage holder gets to take advantage more quickly as rates come down - assuming of course that they do come down.

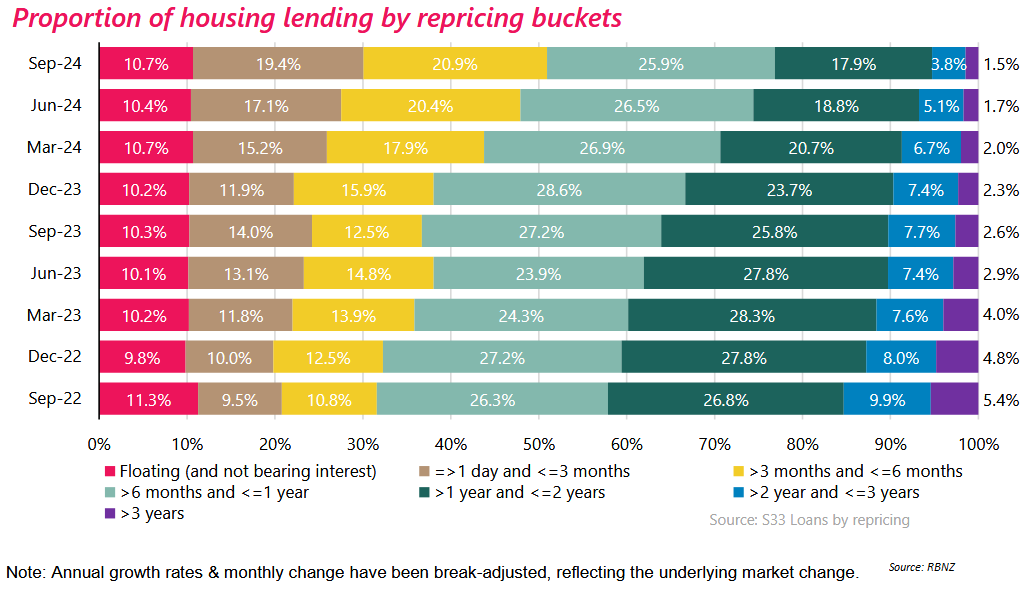

Latest RBNZ figures up to the end of September show that the stock of existing mortgages stood at nearly $364.5 billion.

Of this amount, $39.8 billion was 'floating' while some $146.4 billion was fixed for six months or less.

So another words $146.4 billion was due for refixing by the end of March 2025, which works out at a rate of $24.4 billion every month due for refixing. That's a lot.

Adding the $146.4 billion of fixed rate mortgages with those on 'floating' and we get a total of $186.2 billion - which means some 51.1% of the $364.5 billion total mortgage pile is either floating or is on a fixed rate term of six months or under.

This percentage of mortgage money on 'short' terms has absolutely rocketed in the past year.

If we go back a month earlier, to August 2024, the comparative percentage of fixed/floating up for an interest reset within six months stood at just 49.4%.

If we go back six months, to March, the figure was 44%.

A year ago the comparative percentage was just 36.9%. Two years ago it was 31.8%.

It means that mortgage customers have quite smartly anticipated the falls in interest rates that we are now seeing. And they are well placed to enjoy the benefits of lower monthly payments quite quickly. Theoretically that should help the country's in-recession economy to pick up more quickly than might otherwise be the case because obviously people will have more discretionary money available to spend - although we'll obviously have to wait and see on that.

In terms of what happens between now and the end of the year, the move to shorter terms means there's even very considerable amounts of mortgage money that already has been up, or is up for refixing even within the last three months of this year.

As at the end of September over 30% of mortgage money was either floating or due for a refix by the end of 2024. In terms of amounts, some $70.6 billion of fixed term mortgages are due for refixing before the end of the year.

It all means a lot of people have quite a lot of thinking to do about what sort of term they go for next time.

Much will depend on how much further and how quickly interest rates fall.

The RBNZ has its last OCR review for the year on November 27.

It's widely expected that the central bank will cut at least another 50 basis points off the rate at that stage (to 4.25%), although at time of writing the financial markets were still pricing in a roughly better than one-in-four chance that the November cut will be a jumbo-sized 75-pointer.

Whatever the outcome of the November review, market pricing is heavily in favour of the OCR being cut to 3.75% by the end of February 2025.

Cuts to the OCR don't - as we've seen plenty of times - directly correlate to same-sized cuts for mortgage rates. And the banks have since earlier this year been front-running the RBNZ with mortgage rate reductions. So future mortgage rate cuts might not be as much as likely OCR future cuts might suggest.

Plenty to think about when that mortgage does come up for a reset then.

29 Comments

The effective mortgage rate on the total stock of fixed rate mortgage loans was 6.29% at the end of August 2024. It will almost certainly have nudged above 6.3% in September. The multimillion dollar question is when will this rate start to fall meaningfully - because that is when households in aggregate will get money back in their pockets to spend on other things.

Obviously, for the average to be 6.29%, there must be people below and above this rate. So, as people on slightly higher rates (eg 6 months fixed) move onto slightly cheaper rates, others on much lower 3 - 5 year fixed rates will be moving up. Will they cancel out? When will the balance shift enough to send that 6.29% moving downward?

The simple math here is why I am less than confident that we are going to get a surge in consumer demand as a result of falling mortgage rates. It is also a timely reminder that monetary stimulus is painfully slow, and the last 40 years of NZ data suggests, next to useless unless it is accompanied by fiscal stimulus or a sudden drop in import costs.

The simple math here is why I am less than confident that we are going to get a surge in consumer demand as a result of falling mortgage rates.

Similar thoughts. Think of it like this:

1. The drunken sailor syndrome is great when the tide is coming in, both for asset prices and for consumer spending. This is the state the ruling elite have high levels of hopium for.

2. Drunken sailor syndrome is not the same as the paycheck to paycheck lifestyle needed just to meet minimum expectations. I feel this is where we're at now. But the big difference is that we're trading down, not up. The nice-to-haves are not moving to the shopper basket as frequently as they were prior to Covid.

So unless all cylinders on the Ponzi are firing, we're stuck in a void. Honestly, I don't know what the answer is. Aussie has opened the immigration floodgates, but the trade-offs seem to wreaking havoc.

And with painfully slow stimulus, what will this mean for inflation over the short to medium term.

It's already threatening the lower end of the acceptable range and is only headed lower. RB still overly hawkish IMO.

Great stuff for those with a mortgage. Most people would have gone 6 months for a fixed term so its pretty much all going to roll over to lower rates in Q1 2025.

You reckon Z? What will it mean? An extra 12-pack of Kraft Macaroni cheese per week?

If you have 500k mortgage, a 1.5% drop (from ~7% to ~5.5%) is a saving of $7,500 a year or $144 a week.

Yes it's a significant saving. Some people have pretty bad math skills on here. I bet a few have a much larger mortgage than that as well, $500K plus a deposit wouldn't even get you into a decent house in Auckland anymore.

Depends where one sits on the debt distribution curve Z.

New Insurance premiums will suck that up. Climate events will see insurance go skyward.

If mine was coming up for renewal I would be going from 3 to 5.5, almost doubling. There will be lots of people on these rates that are expiring now, and so their net interest rate is going higher. Lucky I have my 3% fixed for another two years.

@ J.C - For every .5% to 1% that interest rates decline ads around an extra $50-$100 a week back in mortgage holders pockets.

Given peak interest rates were around 7.5%, & it looks like it'll be comfortably heading towards 5.5% shortly with ease, it'll give back around am additional $200 a week back to sole mortgage holders. That's one expensive pack of Macaroni cheese.

Gotcha. Savings will equate to a garage full of Kraft Macaroni Cheese.

But how about a winter holiday in Fiji or Queenstown for a gamily of 4?

@ J.C - "But how about a winter holiday in Fiji or Queenstown for a gamily of 4? "

I'm sure refinancing with a bank you could get them to throw this in. They're handing out cash incentives to those that refinance or switch right now.

a 5.X% mortgage is still higher than pre-covid interest rates. it would be back to 2014/2015 level I think.

Okay, so I bothered to read an article and don't see how you got to this conclusion. Plenty of those due for refix in the next six months could be on lower rates now (i.e. the tail end of a 3- or 4-year fix). Those people with a mortgage are about to start paying more.

As usual, it's the comment section that get to the crux of the matter (which may not support the narrative being peddled for the economy):

Will they cancel out? When will the balance shift enough to send that 6.29% moving downward?

We need to know the terms of those mortgages that are now down to the last 6mths to get a read on the likely answer.

Exactly. We get monthly data on the effective mortgage rate (next release is this Thursday) so we can track what actually happens. The media should ask the banks when they think their effective mortgage rate will start to come down - will it be next month, 3 months, 6 months etc. You can bet your bottom dollar it will be a lot slower than people think. Look at the monthly mortgage interest costs - do they look like they are suddenly going to plummet?

do they look like they are suddenly going to plummet

I thought definitely not suddenly, then I looked at the link and it might not decrease at all yet. Mind you, that is to August so it *may* be peaking now.

It's just frustrating that the article is content to tout a shot in the arm for the economy message, that has clearly been latched onto by some commentors here, without also highlighting the gaps in data that cast doubt it. It's not helpful.

Ahhh but we are going to have to pay for the privilege to comment next year. That is, pay to add value to the most valuable part of this website…

Why wait HM? A couple of months ago you posted that you will contribute "soon".

thank goodness

Thank dog for that!

A lot of mortgagors will be coming off low interest mortgages taken out three years ago when their properties were worth a lot more. They are going to be hit with a huge increase in interest payments, surely? And possibly some of these borrowers will be first home buyers who have now lost their equity. Will their mortgages be renewed?

sounds negative / or lucky maybe they read the news and tapped in a basic calculation - who knows

Well of course higher interest and no equity is negative. Do you see a silver lining somewhere with this? I didn't comprehend what the last part of your statement was referring to.

Didn't David Chaston run an analysis of what was the best way to fix. A strategy. Based on history?

Could have been a couple of months ago.

One poster here says fixing for a year worked out best over time.

Another way was to take the best rate on the day.

There are always wins and losses in the short, but the long term win is what you want.

Yes DC did run a good article about interest rates. It may have shown 2-3 months ago that the 1 year rate was EXPECTED to be best, but it wasn't. Why? Because interest rates dropped by more than expected, something that some who advised to fix for 6 months, predicted correctly.

It would be good to find that again.

Of course any decision you make on the day might not be perfect. But the point I was trying to make, and David was perhaps saying, is there are set ways of behaving that in the long term are better than others. And you can work that out by analysis historicallly of what actually happened.

So it's a relying on a method rather than being clever on the day.

Me with term deposits just go for the best interest rate on the day it comes up, And I don't look at the period.

This article implies everyone is a winner which is incorrect as many fixed rates 2-5 years in duration are at 3% or 4% so those customers won't be celebrating as they will move on to higher rates.

The reserve bank must be disapointed with itself to end up with an average interest rate of mortgage holders of 6.29% in order to fix up their mistakes

Manwhile

Longer-term rates could even rise if global long-term interest rates keep rising

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.