Table 1: April price strength seen across currencies that we track. Stellar y-t-d performance continues

Gold had another good month in April, posting a 4% gain and ending the month at US$2,307/oz. Unlike March, gold finished off its intra-month high from probable buyer reticence and profit-taking – reflected in falling Chinese premia, lower Indian imports and flat-lining COMEX positioning. On the flipside, the trend in North American gold ETF flows turned positive – albeit slightly – joining strong demand for Asian ETFs.

Turning to our Gold Return Attribution Model (GRAM), existing variables and their longer-term relationships to gold returns have, for the second consecutive month, failed to capture price strength in its entirety. Adding a geopolitical risk proxy as well as positioning in the Shanghai futures exchange offers an explanation for some of the moves in March and April, but one other major explanatory factor is still missing. In this context, we believe that central bank buying, as recorded in our recent Gold Demand Trends report and evidenced in higher LBMA volumes, was once again a significant contributor to gold returns.

April review

Gold hit new all-time highs in April but pulled back by month-end: Chinese buying and central banks appear major drivers of support.

Looking forward

Stagflation risks are on the rise: growth looks fragile while inflation remains problematic. Asian investors may continue to draw attention.

Chart 1: Central banks and Chinese investors likely drove April price strength

Multifactor model detailing attribution of gold’s drivers on its monthly returns*

Table 1: April price strength seen across currencies that we track. Stellar y-t-d performance continues

Performance of gold in various currencies*

| USD (oz) | EUR (oz) | JPY (g) | GBP (oz) | CHF (oz) | INR (10g) | RMB (g) | AUD (oz) | |

|---|---|---|---|---|---|---|---|---|

| April price | 2,307 | 2,160 | 11,679 | 1,845 | 2,117 | 61,885 | 537 | 3,556 |

| April return | 4.2% | 5.3% | 8.4% | 5.2% | 6.1% | 4.2% | 4.5% | 4.7% |

| Y-t-d return | 11.0% | 14.7% | 23.9% | 13.0% | 21.1% | 11.3% | 13.2% | 16.6% |

*Data to 30 April 2024. Based on the LBMA Gold Price PM in USD, expressed in local currencies.

Source: Bloomberg, ICE Benchmark Administration, World Gold Council

A sizable rise in volumes from Shanghai gold futures (SHFE) and other forward contracts has recently attracted attention. While short-term tactical traders may have contributed to the spike in volumes, most SHFE participants are industry users with hedging purposes.

Plugging SHFE long position changes into GRAM suggests a statistically significant impact on the global price although does not provide a major explanation of performance. The additional variable in the model only accounts for around 1% of last month’s return. The main question is whether Asian investor appetite for gold will remain well anchored given the macroeconomic dynamics or in a scenario where profit taking become more widespread.

Looking ahead

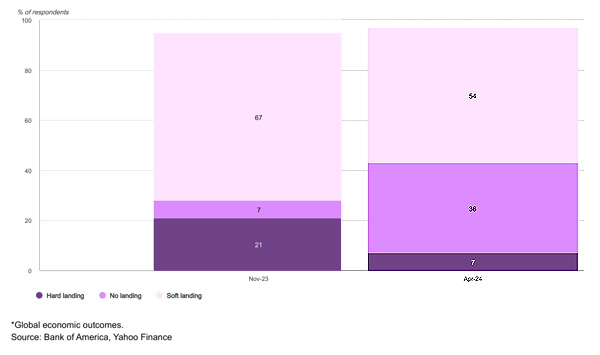

Chart 2: Material shift in economic expectations

Bank of America Fund Manager Survey responses*

H4L: from fringe to mainstream

The recent Bank of America (BofA) Fund Manager Survey revealed a material shift in economic expectations with the probability of a no-landing scenario for the global economy increasing from 7% to 36% (Chart 2).1 While a soft landing still gets top billing, this shift suggests market participants are expecting growth and inflation to stay strong throughout 2024; reflected in investors drastically slashing their rate cut expectations for - both in the US and Europe.

When we penned our 2024 outlook back in November the low probability of a no-landing was largely attributed to the power of the immaculate disinflation story, with falling inflation and a softening labour market. Taking a cue from consensus economic expectations, we too assigned a low probability to a no landing outcome in our outlook, which is now worth revisiting. Importantly, though, while our original no-landing and current higher-for-longer outcomes have things in common, there are also some differences.

Stagflation back in focus

In recent months inflation and growth have seen several consecutive up-ticks. The original expectation for seven Fed rate cuts during 2024 has now been slashed to one, and even that has been pushed back. And while this has been going on, gold prices have breached all-time highs multiple times.

Gold’s resilience is well noted by now. Central bank demand and investor demand – particularly in East Asia – as well as a persistent geopolitical premium have helped gold dismiss the challenges presented by the current investment environment. But even if some of the EM demand we’ve experienced to date wavers, there is an additional trend that warrants attention: stagflation. And it has historically been one of the best environments for gold returns, as we discussed back in 2021 and again in 2022.

Fiscal fuelled growth

US GDP and PCE inflation data on 25 April surprised markets. Following consecutive months of strong economic data and middling inflation, these two prints nudged stagflationary, with a dramatic drop in GDP (1.6% vs e2.5%) and an unwelcome rise in core PCE inflation (3.7% vs 3.4%). As we pointed out in March, growth and inflation surprise indices had been flirting with such a dynamic.

Chart 3: There’s significant fiscal support behind US growth

US Federal spending programmes, share of GDP*

Admittedly, net exports were a major contributor to the lower US GDP figure, but we believe fiscal assistance is supporting an economy more fragile than meets the eye. After all the fiscal spending announced since COVID is almost four times the size of the Marshall Plan post WWII (Chart 3).

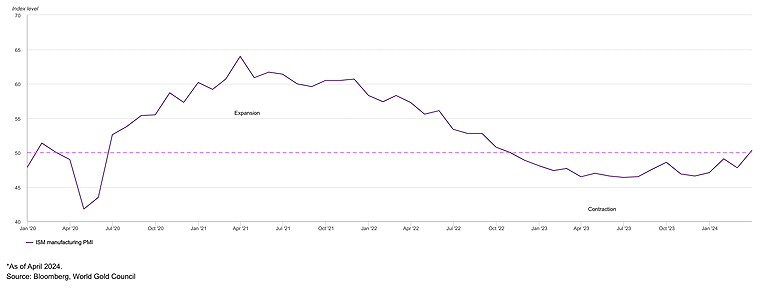

One of the visible beneficiaries of fiscal support is manufacturing via the US CHIPS Act2 – supporting the technology sector among others. Manufacturing PMIs recently crept into positive growth territory (Chart 4). In addition, the PACT Act for veteran health and Inflation Reduction Act are boosting investment in infrastructure, healthcare and manufacturing – the sectors that have been visibly strong via GDP and ISM, as well as the components of US non-farm payrolls.

Chart 4: Manufacturing back in growth territory

US ISM manufacturing PMI index*

So, while fiscal support is often welcome, it does create concentration and event risk if the underlying economy isn’t strong. And indicators of labour market fragility are plentiful:

For now, consumer spending remains solid, driven it seems by the more well off.9 But for the rest of the economy things aren’t so bright and this has created fragility.

Meanwhile inflation remains problematic, largely due to the shelter contribution to core inflation. A stagnant housing market is driving demand for rental accommodation; a situation unlikely to be resolved in the short term and one which keeps shelter costs high (Chart 5). There is also an uncomfortable expected pick up in used car prices and insurance costs. In all, inflation looks set to stay well above target and growth hopes are pinned to a fragile economy and labour market. This is likely why US Fed Chairman Powell noted that it is “unlikely that the next policy rate move will be a hike.”10

Chart 5: Core US inflation set to stay sticky

US Shelter contribution to inflation with forecast*

Sources: Zillow, Bureau of Labor Statistics; Council of Economic Advisers, Vanda Research

As of April 10, 2024 at 8:30am

The levels of inflation and growth deceleration we are seeing now are not as precarious as those experienced during the 1970s period of stagflation. But our analysis suggests that we do not need a repeat of those extreme conditions for stocks to be under pressure. Conversely, gold will likely respond positively to the combination of sticky inflation and less-than-stellar growth.

As we move from soft landing to higher-for-longer, and while the Fed is not in any rush to cut rates, the rest of the economic picture may provide more incentives for Western investors to join their Eastern counterparts in adding gold to their investment strategies.

Footnotes

1Investors increasingly expect 'no landing' for US economy, Yahoo.com, 17 April 2024.

2The Chips Act has been surprisingly successful so far, Financial Times, 25 April 2024.

3 A Tale of Two Surveys, Wells Fargo, 29 April 2024.

4Traders Pull Forward Fed Rate-Cut Bets on Soft Jobs Data, Bloomberg, 3 May 2024.

5Survey of Consumer Expectations, Federal Reserve Bank of New York.

6A Closer Look at Full-time and Part-time Employment, Advisor Perspectives, 9 April 2024.

7Small Business Job Openings Rise in April, NFIB, 2 May 2024.

9Affluent Americans are driving US economy and likely delaying need for Fed rate cuts, AP, 29 April 2024.

10Fed’s Powell: It’s ‘Unlikely’ That the Fed's Next Move Will be a Rate Increase, WSJ, 1 May 2024.

This article is a re-post from here.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Some more discussion about central bank buying via The Telegraph and Yahoo

Some commentators have spent decades predicting the imminent demise of the US dollar’s special status as the world’s international reserve currency.

Eventually, they will be right, and that day may be drawing much closer. As usual, China could hold the key.

There is more upside to go given the current and future global economic and geopolitical environment. This current bull market is far from over.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.