Okay, so, the qualification first. One month is not a trend. Particularly not when it is a December.

But the latest Reserve Bank figures for residential mortgage lending by borrower type do feature a not insignificant drop-off in the share of mortgage monies taken by the seemingly (till now) bulletproof first home buyers, while the apparently moribund investor sector has just twitched a little.

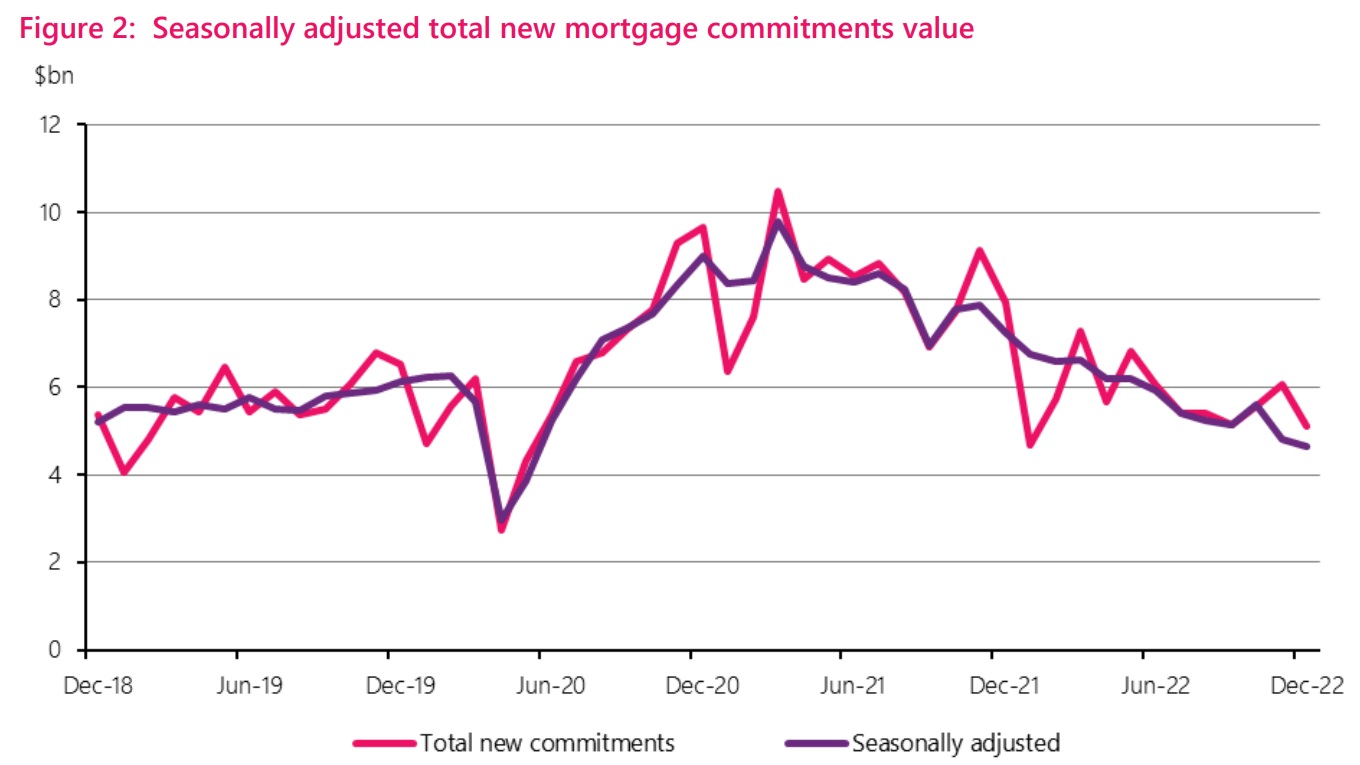

At a headline level, the $5.121 billion advanced in total for December 2022 was the lowest in the 2022 year apart from the always slow month of January. And beyond that, if you exclude January months and the April and May 2020 lockdown-affected figures, it's the lowest monthly tally since February 2019. And it is the lowest December total since 2017.

The December 2022 total was a stonking $2.81 billion (35.4%) lower than the figure reported in December 2021 and some $4.531 billion (46.9%) lower than the mammoth $9.652 billion in December 2020 - which is the second biggest month on record, beaten only by the nearly $10.5 billion advanced in the heady days of March 2021.

In its separate 'Key Points' summary of the figures, the RBNZ says the total monthly new mortgage commitments in December 2022, were down $0.9 billion (15.4%) from November's figures.

On a seasonally-adjusted basis, looking to compare apples with apples, the latest month's figure represented a decrease of 3.3% from the figure for November 2022.

So, the December figures were pretty low, and as said above, we should never try to conclude anything from one month - particularly not one right at the end of the year.

However, back on those first home buyers (FHBs), a notable feature as the overall mortgage figures have kept on dropping over the past year is that the FHB grouping has stayed pretty strong in the market.

This grouping had its highest recorded (since start of the series in 2014) share of the overall lending in November, at 22.4%, but this dropped reasonably sharply in December to 21.7%. In terms of figures, the amount in December 2022 for the FHBs was $1.11 billion, down from $1.357 billion in November. It's the first notable drop in FHB share (barring a very, very slight drop in September) since June 2022. Is the unquenchable thirst for housing maybe getting close to quenched?

At the same time the investor grouping, which has seemingly been on the sidelines for some time now, did show an uptick in December 2022. The $913 million advanced to this grouping in December 2022 was down slightly on the $957 million in November, but the overall share of total advances blinked up noticeably from 15.8% in November to 17.8% in December 2022.

And that 17.8% share in December was the highest share for the investor grouping since the 18.4% recorded in February 2022.

Look, it is just one month, but it will be interesting to watch the next month or three and see whether any pattern forms here.

Separately, the RBNZ provided arguably some of the very good reasons why new mortgage monies are declining so much with the release of the quarterly mortgage loan reconciliation figures.

These showed that interest charged in the December 2022 quarter was some $3.549 billion, the highest figure since the RBNZ started this data series in 2014. The latest figure compares with the record low $2.323 billion interest charged in the September 2021 quarter (when the housing market was still raging).

In September 2021 the total stock of mortgages stood at $314,083 billion, while in December 2022 it was $337.395 billion. So, a 7.4% increase.

However, the rise in interest bill since September 2021, of $1.226 billion, represents an eye-watering 52.8% increase.

No surprise, perhaps, that the market has slowed, a little.

At this stage the overall loan reconciliation figures don't suggest borrower stress in meeting payments. But of course many people have not yet rolled over to the new higher mortgage rates now prevailing. And also, the overall figures will not highlight specific potential pressure points such as those who took, for example, million dollar mortgages (bearing in mind Auckland's median house price was over $1.25 million) at the height of the housing frenzy.

All of these figures are going to be well worth keeping an eye on in the coming months.

35 Comments

All points to a continued decline in house prices then...

I think what we should focus on is a trend. lending amount is on a down curve for some time now, the question is where does it hit the absolute bottom.

It could all literally depend on just the weather. I suspect quite a few Aucklanders just figured out that their house has been built in the wrong place and will be looking to move and this will result in price increases and not decreases.

Oh Carlos… that’s a true spruiker mind set right there. Rain will increase house prices…. That’s a new one for sure

so does a drought, ALL events = rise in house prices...... nothing holds them down they are like zombies

and will be looking to move and this will result in price increases and not decreases.

Lol, you can’t be serious!!!

My house is now in an established flood plain, therefor it is worth more when I sell it.

I do not follow this logic.

The resale value of the house in a flood plain is toast or else its uninsurable, nobody in their right mind will buy it or move into it, therefore you need to buy another house, therefore there is less houses available for sale in suitable areas going forward or it will need to be a new build so the prices go up.

At this stage the overall loan reconciliation figures don't suggest borrower stress in meeting payments

Our tight labour market is keeping mortgage stress low at this stage. Households start by cutting back on discretionary spending and the recent dip in consumer spending is pointing to that trend kicking off.

Sharp recoveries in tourism and net migration figures will ensure labour market remains tight albeit much of the job growth will be in the low-income category.

Our tight labour market is keeping mortgage stress low at this stage. Households start by cutting back on discretionary spending and the recent dip in consumer spending is pointing to that trend kicking off.

Yes. I know I sound like a broken record, but it all starts with discretionary spend first. People don't reach for the 'nice to have' cottage/boutique/craft FMCG items of the supermarket shelves. What's more, they start choosing the cheaper brand for products for which they have 'low involvement' (some people don't care about the brand of dish washing detergent; price is the key variable). Unfortunately, NZ does not have a proper discounter retail offer unlike Europe, U.S., Japan. When I worked directly on this phenomenon, I told P&G they were about to get smashed in the Japan market because the Japanese understood that the value / functional performance they were able to get from the TopValu store brand matched what they could get from Ariel. P&G didn't listen and they're fighting to hold market share through targeted discounting. Not a way to run a business unit.

As spending patterns change, so does revenue, profit, and income for the respective businesses (they fall). That is not so good for the property ponzi. The key lesson is that the wealth effect and the ponzi share a symbiotic relationship. One doesn't necessarily drive the other. They actually feed off each other.

Exactly, that spending (or lack thereof) starts with minor tweaks here and there, and can move in stages.

Ultimately people only have x amount of disposable income.

What many fail to grasp, is that competition for this $ isn't product or even industry specific anymore. Insurance are competing with Cafes who are competing with Gyms who are competing with Pubs who are competing with Gluten free health bars who are competing with consumer electronics.

Priorities will differ, but it is clear things are being dropped, switched, changed. It will just take a while for it to show in any meaningful statistical way.

What many fail to grasp, is that competition for this $ isn't product or even industry specific anymore. Insurance are competing with Cafes who are competing with Gyms who are competing with Pubs who are competing with Gluten free health bars who are competing with consumer electronics.

Not many people out there really understand, which I was surprised about the interest dot co article about the expensive bread. I think many people in NZ are stuck at the denial stage and are struggling with how things change.

It's the economic equivalent of heating the water slowly to boil the frog.

People will work it out eventually...

I know one early 2020 FHB who is preparing to sell, as they've looked ahead an cannot afford to refix. Interestingly, they've gone with the REA who 'appraised' the house 200k lower than the others. I'll be surprised if they get even that, but it would be a good surprise - the CG would be over double their salaries for the time they've owned it.

Great point. Particularly a challenge for NZ businesses when competing with international brands in an increasingly price-sensitive market. Business failure will be widespread as many buckle under high wages and overheads, not because of staff skill level or productivity but high living costs.

Particularly a challenge for NZ businesses when competing with international brands in an increasingly price-sensitive market

The Rockit apples in those little plastic tubes (4 miniature sized apples) are selling for approx NZD15 across modern trade retail in Asia. The shopper has the option of South African apples that they can choose at a 40-50% cheaper price. And to be honest, Asian consumers don't necessarily care about brand if the product is good.

Go figure.

100%, I'd upvote twice if I could.

If I look at my own household's spending, we have started a few gradual adjustments. To be fair we're very comfortable financially, but we just want to build some additional reserves.

Over the past few months we've made the following changes:

- When dining out, we just get soft drinks instead of alcohol.

- We only get takeaway coffees on the weekend, never on the way to work

- We get takeaways one night per week (used to do two ... sue me, I'm a bit lazy)

- Instead of doing Countdown online shopping I now get up early on a Saturday and do Pak N Save

- We've gone to some more basic brands from premium

- We were going to upgrade the family car, but dropped a couple of grand on improving the current one to keep it on the road for longer

- My partner dropped her gym membership and she just goes for runs now

All marginal stuff, but it adds up (sufficient savings to compensate for an additional $100 p/w in mortgage cost).

Do PAknSave online shopping., That way if they're out of stock of the cheaper options you chose their policy is to substitute only higher priced products. It has turned out to be a great way to get those expensive prawns (for example) or the luxury peanut butter. Like you said, marginal, but adds up.

Good for you. We also do Chinese grocery store and the Mad Butcher for certain items.

Yep I’m doing the same. Actually pretty much dropped alcohol, cut back on takeaways and reduced branded products. Also found savings reviewing phone & internet providers, insurance etc. I am also holding off purchasing electronics that could be upgraded to see how things develop politically in NZ. Currently looking at equivalent jobs in Australia - significantly higher pay for less hours…and extra super contributions. No interest costs and minimal commuter costs but I can empathise with the poor buggers dealing with these. To be honest I don’t see a future in this country anymore - and I 100% think this is a result of poor leadership (labour being by far the worst)

The story of this year, at least for the first quarter, will be an increasing number of house vendors competing for diminishing amounts of purchaser debt

The local GJs has a run rate of 5-6 house sales a week.

They haven't sold one in 3 months.

Mate works at a used car yard. Usual turnover 50-70 per month. In December they sold 15.

I work in the finance sector. People are stretched die to the Cost of Living crisis. As a result, many are failing affordability. Christmas is usually bad. This year it was terrible.

I have just had an email from my RE agent saying he will present me with an offer tonight, will see how much for...

Also as valuations come down, banks will not lend purchasers much above valuations unless they have a sizable deposit.

A lot of people are deleveraging. I am. Loans are locked in for a while, wages are improving, don't really need to upgrade just yet so I'm letting it play out and paying down debt.

How much of that $5.121 billion advanced for Dec 22 was just refinancing? Assume a change in bank lender means it gets reported as a new commitment? As December 2020 was huge month. There would have been some refi in Dec 21 from those that only took one year fixed rates. More rollovers for Dec 22. But now those borrowers have less paper equity and probably denied completely by prospective new bank lenders (if they even tried) or had low LVR penalty rates requested. So potentially they are stuck with existing bank until their situation improves.

Reality will be starting to set in for these borrowers now. March 23 will be interesting.

Would like to know from Mortgage Brokers if they are getting many refinancing requests from people trying to save a few points in interest and how many of those deals are getting over the line.

In September 2021 the total stock of mortgages stood at $314,083 billion

The comma needs to be changed to a full stop. Big difference when comparing $314,083 billion to $337.395 billion 🙂

All predictable really, one more rate hike and all the FHB are going over the cliff. This is why I think the RBNZ have finally come to the cross roads and what they do on Feb 23rd will be a true reflection of their intentions. The time for jawboning is over, inflation is still here are they finally going to crush the housing market and try to put everyone out of a job or are they just going to go into a holding pattern ?

One could say "The time for speculation ahead of all else is over".

The many would be those with no mortgage, most of NZ, and those being hammered by inflation, also most of NZ. Could Labour role over and start playing for the election..sure, but then they are just the Rose Party -National lite so to speak. They will never win on that basis. They would be better to stay the course on the anti debt speculation and anti bank profit to maintain a clear point in difference. The spin off is continued house price decline, which Labour can say the don't want but most kiwis do.

Central banks around the world seem to still be raising interest rates, really following the FED's lead. Inflation is still raging, and the effects of previous hikes is still yet to be felt as owners roll off of fixed rates. It looks like a lot of people will be burnt later this year

Yes i believe there was a survey last year where 80% + kiwis wanted house prices to fall. I know I do - i am over the crime, suffering, healthcare system failures, poor kids, disillusioned professionals... all stemming from the greed of a few.

I reckon Labour just need a strategy to please everyone by saying they dont want prices to fall then blaming inflation, world events and RBNZ when they do fall... Chippy will grab some of all voter groups.

Until National come out with some decent policies of their own they will be on a gradual decline. Chippy is all over business, crisis management and about to reshape or can all the unpopular stuff.

Chippy is already more popular in the polls than luxon (x2). So Once labour have rearranged the deck they can go after Nationals policies which (when there are any to speak of) are pretty weak to terrible tbh.

I am a traditional conservative/NatVoter but see nothing in their policies to want them over a reformed labour.. in fact they will make things waaay worse for everyone but landlords and super wealthy. Need to see proper climate change policies, how to make housing affordable for my kids, a proper health strategy, a proper crime prevention strategy (some childish idea of more prisons and bootcamps is a dumb-trump style plan... we are educated now My L and know that just makes criminals worse when they finish).. a strategy for productive business that is export led.. currently National are a party of jokers hoping a bad economy gets them in to enact their nonsense....

Gotta keep the buyers in place.

Stop plaguing the poor vendors!

https://www.oneroof.co.nz/news/its-embarrassing-165000-west-coast-shack…

You may find low ball is what some can afford. Regardless of location fantasy numbers still in place.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.