Revenue Minister David Parker is confident his policy to prevent property investors from writing off interest as an expense when paying tax will dampen house price growth.

Parker is so confident; he believes the policy will result in the Reserve Bank (RBNZ) keeping interest rates lower for longer than would otherwise be the case.

Batting off criticism from National’s finance spokesperson, Andrew Bayly, around how much the removal of interest deductibility will cost investors, Parker made the point the cost would depend on the level of interest rate.

Parker has previously made the argument now is a good time to introduce the policy because interest rates are low. Accordingly, the interest expenses investors are writing off are relatively small. So, removing the ability for them to make this write-off won’t be as painful as would be the case if interest rates were higher.

However, conventional economic theory suggests if Parker thinks the tax policy will put downward pressure on interest rates, he implies it will dampen economic growth. Central banks keep interest rates low to fire up sluggish economies.

But talking to interest.co.nz, Parker denied the assertion he was admitting interest deductibility would dampen economic growth. He argued it would dampen house price growth, but not economic growth.

His rationale was the economy would grow if some of the scarce capital being poured into housing was directed towards more productive parts of the economy.

Put to him that if this happened, the RBNZ would likely increase interest rates, not keep them lower for longer, he said central banks “put up interest rates for a variety of reasons, including stability of financial markets if they think housing property markets are running too hot”.

The RBNZ is required to use monetary policy (IE manage the cost and supply of money) to ensure annual consumer price inflation is between 1% and 3% and maximum sustainable employment is maintained.

In doing this, the law requires the RBNZ to “have regard to the efficiency and soundness of the financial system”.

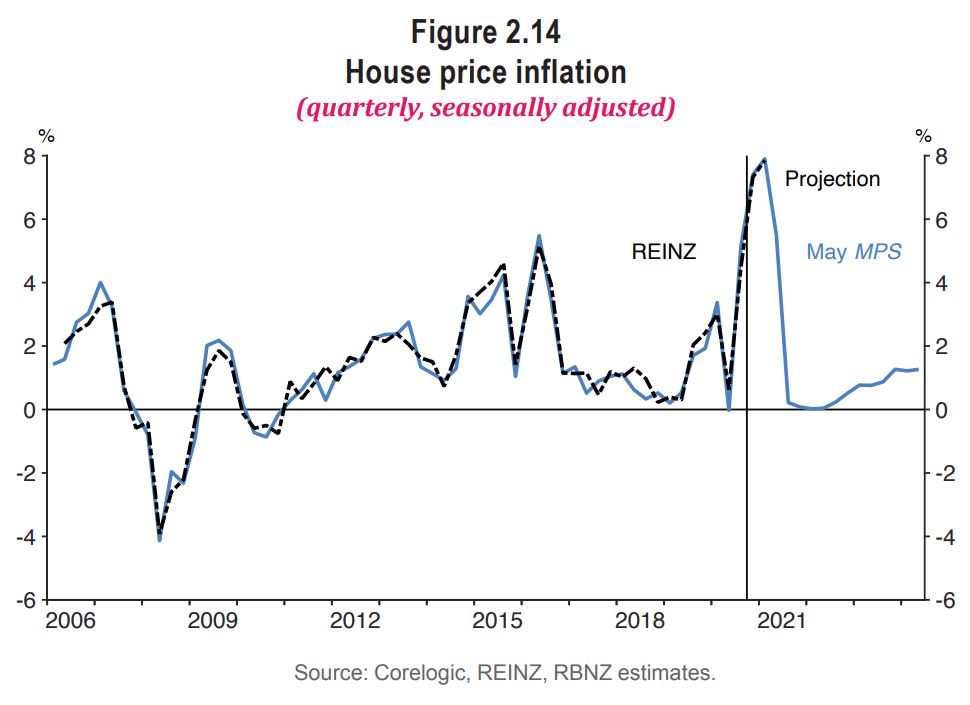

The RBNZ, in its latest Monetary Policy Statement released in May, projected house price growth dropping off completely, due to the Government’s tax policy changes, as well as the reintroduction of loan-to-value ratio restrictions, strong residential construction, slower population growth and the “waning impact of interest rates declines over 2019 and 2020”.

The RBNZ said: “The extent of the dampening effect of the Government’s new housing policies on house price growth and hence economic activity will also take time to be observed.”

The RBNZ also projected two Official Cash Rate (OCR) hikes from the second half of 2022.

Most bank economists believe the economy is recovering well enough for the RBNZ to raise the OCR sooner than from mid-2022.

There is still a question mark over whether interest rates will structurally remain low by historic standards in the medium to long-term, as globalisation and technology continue to put downward pressure on consumer price inflation.

41 Comments

Have they actually done any behavioral research as to how investors will react? It's not actually as difficult as it sounds but I very much doubt they have. If they have, they would actually cite the findings.

If you structure it as a company presumably your allowed the deduction.

Why?

Not sure the interest deductibility will apply to companies or just residential rentals.

Companies might be able to continue to deduct.

Of course not, they havent even done any financial or economic research into this policy, let alone something so esoteric as human behavioural responses.

Consequently it will come as a big surprise to the Govt when they realise that investors will simply switch to pouring money into their own homes, and selling them every couple of years to buy something bigger and better, until they are all living in $5M tax shelters. Not sure how that will force prices down though. However, it will make a boat load of low income tenants homeless though.

This policy is an absolute shambles. How can you introduce such a policy without any benefit/cost analysis & without any support from IRD/Treasury officials?

The big losers will be tenants. The government has totally ignored the impact on renters & how many will be forced into expensive emergency motel accommodation as they can no longer afford the rent or find a rental property to live in.

Investors will reduce their holdings in lower quartile rental properties & pour money into their own homes. Rents will increase much faster as rental properties become more scarce & landlords will try to recover some of the extra cost costs incurred from healthy homes legislation, interest deductibility rules, increasing house prices etc.

Grant Robertson should focus on doing his job rather than playing childish games as displayed in his recent "humorous" outburst in parliament.

I think you're right KW. The top tier suburbs should go parabolic while the ghettos go sideways or down.

dp.

dp.

Incidentally, Parker refers to quote "head off the risk of an out of control housing bubble". Does that mean the govt thinks that a bubble doesn't exist as yet? Does the govt unanimously support this description? Madame Xindy and Robbo?

The housing bubble only exists as an existential threat when you're in opposition and trying to get elected.

Once you're in power, it's called the 'wealth effect'.

I see. Like a "nice problem to have."

Don't you dare assume their genders.

NZ politicians have big mouths and small brains.

Haha.

One of the few statements you have made that I agree with. :)

Especially in Parkers case

We vote for them

" Most bank economists believe"

Couldn't have put it better myself.

There is nothing but houses, and filling them with c--p, then chucking it so they can fill them with more. That's all 'a productive economy' - the thing DC lauds morning-in, morning-out - is. We can describe it as: extract, consume, discard; or from low-entropy to high entropy. All being attempted at exponentially-increasing rates.

So it doesn't matter much whether Parker is right about the speed of the deckchairs if they pump out the forward hold, or someone else advocating the aft hold; the bl---y thing is sinking under them.

What happens to all the unrepayable debt? is the question both Parties should be asked. It's not complicated. Because at some near point, the unrepayableness of the debt is going to shatter mass belief in the value ov money. And at that point, all bets are off.

I often contemplate how bad it will be. On a scale of ten. With say 1 being the gfc crises of 2008, 10 being say ww2, or the bronze age collapse.

I mean scary thought, when we consider current climate change velocity, are we about to (next 100 years) re write what bad means.

The reason why we are all largely ignoring it is because we think it will be 100 years. What if it was guaranteed to be 10 years ? Would people wake up and change then ?

(Parker) said central banks “put up interest rates for a variety of reasons, including stability of financial markets if they think housing property markets are running too hot”.

Seems the RBNZ never got the memo.

In fact they lowered rates, causing the housing market to take off.

I don't know if the minister has looked at labour productivity or lending recently but revaluing housing is our economy now. This has been a housing lead recovery.

The outlook is for an ongoing affordability dilemma for FHB - if the housing market does cool /is cooling, FHB still may not necessarily be better off if interest (and mortgage) rates increase.

There is some evidence that the housing market is cooling (i.e. rate of growth slowing) but there is seemingly no evidence of a major a correction . . . and RBNZ signals are that in the medium term there is upside to the OCR and consequently mortgage rates.

but there is seemingly no evidence of a major a correction

You mean to say there's no evidence that a major correction will 'happen'. Like a media celeb or a politician.

Capital Gain = easy and fast money = greed will not be dampened by any tax = only economy in NZ = supported by RBNZ and Jacinda Arden government.

Capital Gains Tax easy fast taxation money especially as they wanted to apply it to annual charges in value.

New Zealand is such a sprat in a large ocean. When things move in the US is going to move here. The reality is nobody can predict the medium term and everything is now so distorted that things could get really ugly.

Anecdotal I know, but up where I live property is still going gang busters. 0.5% term deposits vs 2% yield and capital gain a no brainer, even with the tax changes.

Why is someone that buys multiple houses called an investor?

Should be called thieves.

Agree. The govt owns heaps. They're certainly thieves.

Incorrect - and spin. Common bedfellows....

The Government is us. We own.

Only those selfish enough - and it often goes hand-in-hand with an inferiority complex - to want to have more than others, make such comments. Easier to solve the personality flaw, perhaps?

So "our" houses don't meet the new standards. Is the interest deductible? If it is then the government has skewed the game in their favour.

State homes for all, UBI is next. Socialism here we come.

In the face of reducing energy and resource supplies, and increased demand/conflict for/over same, you might find socialism preferable to tumbrels. When folk have nothing to lose.......

Because Labour has executed every other policy they have with perfection.

There's still pent up housing demand we apparently need 200000 houses. Where's the 100000 gone?

I wonder if they've removed interest deductibility on their own housing stock.

Labour, destroying the dreams and aspirations of NZers since 2016.

Parker is talking nonsense. The money that goes into housing is overwhelmingly borrowed from banks. People aren't sitting on $800,000 in savings and weighing up whether to buy an investment property that someone else can manage or quit their job and buy a business that will take up 60 hours/week. That money will not be reinvested in other parts of the economy, it simply won't exist.

Decreasing or increasing interest rates by a notch or two will make next to no difference to the *real economy* - anybody who still believes this is guided by ill-informed doctrine rather than evidence. If our Govt continues to place its faith in monetary policy, we will be left behind as other countries use fiscal tools and smarter planning to transition to green infrastructure, address entrenched poverty, train young people with the skills the country actually needs in 10 - 20 years time, build self-sufficiency etc (sawmills!)

Incidentally, an increase in interest rates might slow down house price increases a bit - but it would take a full 2% increase to get total interest payments on home loans back to the same level as they were in 2016 ($15bn vs $9bn now).

I did my monthly study of rentals on Trademe. The number of rentals advertised through our NZ is the lowest it has been for 5 years. This a direct result of the Government action

Would be interesting to know how many in Labor also agree with the IRD and treasury that the removal of interest deductibility from residential realistate is a bad idea.

Theres a big difference between serviceability, the ability to pay your mortgage, based on interest rates and affordability, which is largely based around your ability to save a deposit.

That's the way David....smash them with a new tax you said you would not introduce and then smash them again when interest rates rise...That will teach you to try and be successful in NZ!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.