These are rare times.

We now have our dairy industry and its biggest player, Fonterra, operating (possibly truly for the first time) in lockstep as farmers enter the home stretch of what's looking like a very productive (in every sense) season - and which may yet be followed by another of similar strength.

The farmgate milk price is high (it will be a record - likely around $10 per kilogram of milk solids), which is great for farmers directly. And despite the high price Fonterra's having to pay to access that milk, its profits are high too, which is great for farmers indirectly.

Fonterra's interim result and dividend were strong, while the high dairy prices also contributed to the recession-breaking 0.7% rise of GDP in the December quarter.

And this is all very good news for New Zealand's embattled economy. The performance of the dairy industry and indeed the meat industry over the next 12 months, when combined with a low Kiwi dollar, could yet drive our economy on rather more positively than the current fairly sanguine expectations would suggest. But that hope of course comes with a million caveats in the midst of such a volatile global situation.

I have long had an uneasy personal relationship with Fonterra. I disagreed with the creation of a super-co-operative that was charged with effectively being the guardian of our very important dairy industry. This therefore produced the odd conflict within me of resenting what Fonterra was, while wanting it to succeed for the sake of the economy.

My concern was that by putting all our milk in one pail we risked pouring our whole dairy industry down the drain if the folk running the operation got it wrong. Well, we can debate how close we got to that situation, going back to the 2015-18 period, but it was closer, I suspect, than anybody might want to think. (Here's two articles - Here and Here I wrote in 2019.)

Somehow it always seems easier to talk about what a business has done wrong, rather than how it has done something 'right'. And there was plenty 'wrong' to talk about with Fonterra.

Since 2018-19 though, we can talk in terms of 'right' things at Fonterra. I would point to an excellent transitional/transformational job done as chairman by John Monaghan, paving the way for the current incumbent Peter McBride and the instillation (under Monaghan's watch) of current CEO Miles Hurrell.

It's significant, I think, that Hurrell was an internal appointment.

It's a general comment I would make about businesses and the corporate world that there always seems to be the attraction of the glittery shiny CEO from outside the organisation, while the 'grunts' within the organisation are overlooked.

I mean, hey, I get it. There may be concern about internal appointments that they would be in a sense institutionalised, maybe not motivated, and without fresh ideas.

The other side of the coin is that an 'outsider' might be seen as having the fresh ideas and the drive to take a business in a new and lucrative direction.

Existing employees can't compete with the guy who comes from outside pointing a sharp suit in everybody's direction and presenting a powerpoint display that kills - outlining the courageous new strategy that's going to drive the company to new heights.

How often does that really work though? I can think of countless examples of CEOs who've blown into an organisation like a hurricane, changed everything, and then blown out again within say three years at maybe about the time, or just before, it starts to become apparent what a mess they've made.

An internal appointment knows the company, knows what is achievable and just may well take a more incremental approach - improving without breaking and reshaping everything. I think they used to call it sticking to your knitting.

Now, I don't exactly know what's happened inside Fonterra.

But look at the results.

The Fonterra conundrum was always that it performed 'well' financially only when the milk price - and therefore the direct return to farmers - was down. Once the milk price went up, Fonterra's profitability went down because it couldn't hack the high price it was having to pay for its key input - milk.

As we know, the milk price is at a likely record right now and yet Fonterra appears on track to pay a dividend this year that's right up there with the best it has achieved. It's paying the proverbial arm and a leg for its milk - but is still turning good profits on it. That's something the Fonterra of the past just couldn't do.

Why? Did Fonterra just simply see itself as too 'special' because of what it was and how it was formed? Did it try to be too many things? Did it believe it had to complicate things, to show us how clever it could be?

These days Fonterra looks to me like an organisation that knows what it is - and what it isn't. It understands itself and what it can and cannot do. And that's not necessarily a straight forward thing to achieve. It's taken Fonterra years. No distractions. Do what you are good at.

With the current tailwinds for Fonterra, and for milk, the question is can we now look to something more sustainable than has happened in the past? Are we entering a new era?

I'm interested to see what all the extra money pouring on to the farm will do for NZ Inc. We know that our farmers in the not distant past have suffered from ups and downs of returns, while on-farm costs have been going up. The break-even milk price is estimated to be something north of $8.50 per kilogram of milk solids.

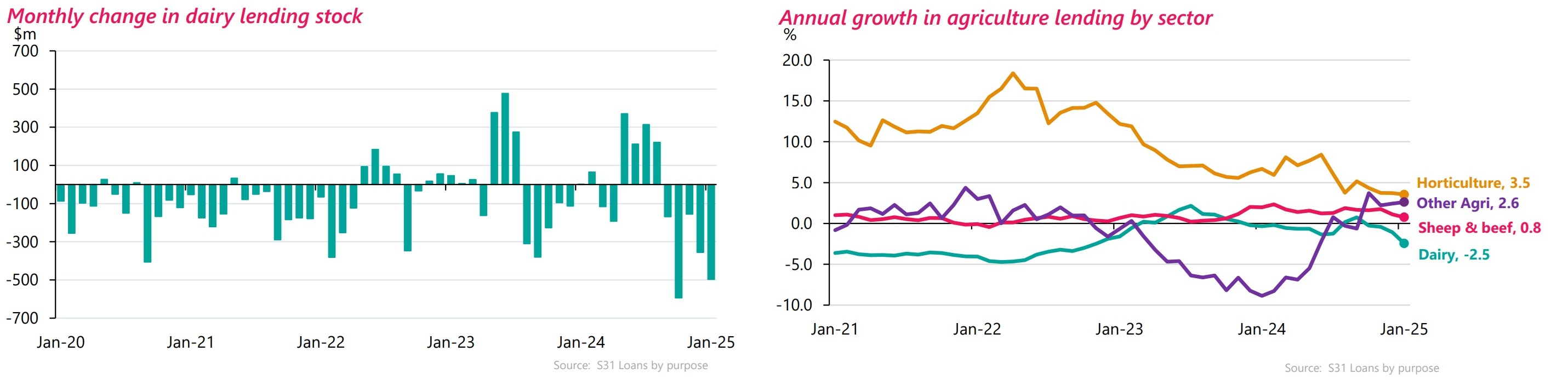

Debt repayment's likely to continue being a priority this year.

Reserve Bank monthly debt figures show that from August 2024 through to January this year (latest available month at time of writing) nearly $1.8 billion of dairy debt has been paid down, meaning the total outstanding is down to just under $35.5 billion - which is the lowest outstanding dairy debt figure since at least 2016, when this particular data series started.

Assuming this debt repayment continues for the moment, what does happen next year if milk prices stay high? It must be good for all of us surely?

DairyNZ, the sector organisation representing New Zealand's dairy farmers, compiles an excellent "Econ Tracker Tool", which among other things provides detailed financial estimates based on farm median figures.

The information in the tracker tool is updated quarterly - and it's just been done again now.

DairyNZ Head of Economics Mark Storey, (while adding all due caveats), says "right now we are seeing strong market fundamental indicators that, for the first time in 25 years, show there is a good chance we will see two $10 payouts in a row, rather than a peak followed by an immediate trough".

Working on an example of a 165 hectare farm with about 450 'peak' cows milked, the tracker tool points to potential "discretionary cash" of around half a million dollars being generated in each of both this season and next season, with cash surpluses for in each year of in excess of $65,000. As recently as the 2022-23 season cash deficits of that magnitude were being recorded.

With this kind of spending power being applied in regional New Zealand, it's got to be good news - and suggests strongly that our economic recovery, of whatever magnitude, is likely to be led from the regions.

How long may this continue? Can it continue?

Can Fonterra continue to surprise on the upside?

The next key thing to watch with Fonterra is the sell off of its consumer brands businesses, including such household names as Mainland and Anchor. The newly-named 'Mainland Group' will either be sold in one piece to a trade buyer or possibly sold to the public and then listed on the stock exchange through an initial public offering of shares (IPO).

I have previously expressed disappointment at the decision to sell these assets as I wondered if it pointed to a lack of ambition. But I think the Fonterra of the recent past and the present has earned the right to be given a certain amount of trust that it knows what to do for the best.

An IPO would be interesting, particularly if Fonterra retained a cornerstone shareholding. And there's no doubt it would be a popular listing. Regardless of whether that happens or if Mainland Group is sold in one piece, there will be a nice windfall for farmer-shareholders. It has been estimated as possibly as much as $2 per Fonterra share if all the assets are sold.

So, the immediate future for dairy and dairy farmers looks bright - a standout in a very dull economy. And the potential to help resurrect said economy.

Time will tell but this is a big bright spot for the economy.

One thing’s for sure, right now the question: "What will Fonterra do next?" is no longer being asked with trepidation, but with interest, and perhaps a bit of hope too.

*This article was first published in our email for paying subscribers first thing Friday morning. See here for more details and how to subscribe.

1 Comments

Hi David, great article on Fonterra as an outsider, thanks for being honest with your thoughts over the formation & evolution of the co-op.We as supplier/shareholders have also waited a very long time for the original vision to finally come to fruition.I believe the current management team have turned this huge ship which is Fonterra around,to what it is today- a very profitable co-op that everyone in NZ benefits from,by paying a fair & competitive milk price which all other dairy companies have to match to keep supply.Fonterra's profits & therefore farmers profits are redistributed amongst the rural communities, the increased export earnings,the extra taxation the Government receives all contribute to the standard of living we as a country we all desire.I now believe that the time is right to offer an IPO of the consumer brands - this a win,win situation again for NZ Inc as everyone can have a vested interest in known brands & keep them a tightly held investment that everyone will benefit from.Also another benefit would be a better understanding of our industry through education of owning such an investment.Regards

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.