Here's our summary of key economic events overnight that affect New Zealand with news all eyes are on how well, or otherwise, the end of year holiday retail season will progress. But we will have to wait for that data to start coming in.

But in the US, they could report outsized gains because shoppers may well choose to spend now at prices that will be lower, perhaps much lower, that when the new Administration imposes its promised tariffs. And that won't change until the incoming government realises what any high school economics student knows - that tariffs are a tax on yourself.

Japanese consumer sentiment recovered somewhat in November, still positive, but nothing like what they had from December to March yearier in the year.

Japanese retail sales rose +1.6% in October, recovering from the weak September expansion, but still much lower than what they have achieved monthly since early 2022. At least it is back heading in the "right" direction.

And Japanese industrial production rose +1.6% in October from a year ago, ending two months of retreat

South Korea's industrial production rose in October at a very strong +6.3% rate from a year ago, after the unusual stumble in September, returning to the average expansion they have had since September 2023. So it will be no surprise yo learn that their exports keptr rising strongly in October, as did their imports.

However Korean retail sales slipped in October to be -0.8/% lower than a year ago

India's economic expansion is 'consolidating', delivering a somewhat disappointing Q3-2024 result. Their economy rose +5.4% from the previous year, slowing from the +6.7% expansion in Q2-2024 and well below market expectations of a +6.5% increase. It was their softest pace of growth since Q4-2022. Still, even at the lates lower rate, it is rising on a per capita basis.

This miss adds pressure on the Reserve Bank of India to cut its policy interest rate which currently stands ar 6.5%.

The Indian currency fell on the news to a record low against the USD. Although not a record low against the NZD, it is has been close to that since the whole period from end of 2020.

In Canada, their Q3-2024 GDP growth came in +1.0% higher than a year ago, up +0.3 fr the quarter. This was not enough to prevent a fall in per capita GDP. On that basis it fell -0.4% in the third quarter, which was the sixth consecutive quarterly decline.

In Europe, inflation expectations in the euro zone for the year ahead edged up slightly in October to 2.5%, and stayed steady for three years out at 2.1%, the ECB's monthly Consumer Expectations Survey showed

EU CPI inflation rose to 2.3% in October, up from 2.1% in September, but still clearly in a down-trend that started in November 2022.

In Australia, private sector debt rose +6.1% in October from a year ago, driven primarily by business debt growth, up +8.3% on the same basis, but housing debt growth was up +5.3% too. Other personal debt only rose +2.2% in October. (From a Kiwi perspective, these are relatively fast rises. Yesterday equivalent RBNZ data showed business debt rising only +1.1%, housing debt rising only +3.5%, and personal debt up only +1.7% in the year to October.)

In Australia there is some scepticism that this debt tide rise will be maintained.

The UST 10yr yield is now at just on 4.18% and down -6 bps from this time yesterday and down -23 bps from this time last week. The key 2-10 yield curve is still positive, but only by +2 bps. Their 1-5 curve inversion is inverted by -23 bps. And their 3 mth-10yr curve inversion is slightly deeper at -43 bps. The Australian 10 year bond yield starts today at 4.36% and down -6 bps. The China 10 year bond rate is down -2 bps at 2.04%. The NZ Government 10 year bond rate is down -1 bp from this time yesterday at 4.47%, down -20 bps for the week, and back to where it was six weeks ago.

Wall Street had a half-day session today, but ended with a +0.6% gain for the S&P500. For the week it is up +1.5% to a new all-time record high, something that happens regularly now. Overnight, European markets were quite mixed again. London hardly moved, up +0.1% in its final session of the week to be +0.3% higher for the week. Paris was up +0.8% on the day but down -1.3% for the week. Frankfurt rose +1.0% overnight to end up +0.8% for the week. Tokyo dipped -0.4% on Friday to be -1.2% lower for the week. Hong Kong rose +0.3% to be 0.6% higher for the week. Shanghai was +0.9% higher yesterday for a weekly gain of +0.6%. Singapore only rose +0.1%. The ASX200 dipped -0.1% and ended up +0.5% from a week ago. The NZX50 rose +0.1% on Friday for a +0.2% weekly gain.

The Fear & Greed Index ends the week still in the 'greed' zone where it was last week.

The price of gold will start today at US$2659/oz and up +US$17 from this time yesterday, but down -US46 from this time last week.

Oil prices are little-changed, still just over US$68.50/bbl in the US while the international Brent price is just under US$72.50/bbl. A week ago these levels were $2.50/bbl higher, so a retreat from then.

The Kiwi dollar starts today at 59.2 USc and up +30 bps from this time yesterday. But it is up almost +1c from this time last week. Against the Aussie we up +20 bps at 90.2 AUc. Against the euro we up +20 bps to 56 euro cents. That all means our TWI-5 starts today at just under 68.6, and up +20 bps from yesterday, up +50 bps from a week ago.

The bitcoin price starts today at US$97,063 and up +1.9% from this time yesterday, but down -2.0% from this time last week. Another crack at the US$100,000 level seems to be underway today. Volatility over the past 24 hours has been moderate at +/- 2.1%.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

55 Comments

It was India's softest pace of growth since Q4-2022. Still, even at this lower rate, it is rising on a per capita basis.

A critical performance measure our country can do nothing more than aspire to....

Isn't India's GDP per capita much lower than NZ's? So if we had similar growth it would be regarded as phenomenal. A 6% increase on 10k would be 600 while a 2% increase on 50k would be 1000. Which would you prefer?

I don't know, I may be confused, but worth thinking about.

Uhhh yeah. You can grow a lot faster when you're going from a lower base. Industrial leaps are bigger, and a hungry workforce is more motivated.

That and you can capture foreign jobs with lower wages, that are still a lot higher than domestic ones.

Pretty sure most here wouldn't want to swap their life for the average Indians.

I agree in principle but doesn't take away the fact that NZ has plenty of room to improve.

We're at a smaller GDP per capita base than many Western countries and are falling further behind than many. The skills, capital and leadership required to compete on foreign or local jobs are absent.

My team here in NZ used to do a lot of the work on Aussie projects even half a decade ago. These days we struggle to find quality engineers to do local work properly.

I agree in principle but doesn't take away the fact that NZ has plenty of room to improve.

As do all of us. Pretty hard to actually identify how remarkable we have it, if all you're concentrating on is deficiencies.

Doesn't have to be either-or. I teach my young kids to enjoy the good life but also continually work on their deficiencies.

Not unreasonable to expect the same from grown-ups. Most sociologists would agree that humans are capable of such multitasking.

It's not really a matter of multitasking, it's the nature of how one is viewing the world.

I.e., your response to anything remotely positive about NZ, is "yeah but, check out these negative stats". Much of what we are seeing has a long tail, with limited options to resolve. We can see where it's going, try to prepare for it as best we see fit, and enjoy the ride.

Advisor would be better teaching kids post-growth skills.

Food-production, workshop familiarity.

They'll need it all, and more.

Get rid of Albanese - the man is tone deaf

Kiwi dollar defying those who see a direct, simplistic causal relationship between interest rates and exchange rates

Does the $NZ actually relate to anything?

Exactly...Pacific peso j

What we want is a currency that's value is related to when Elon Musk doest a fart.

Basic maths stuff.

redcows: "Does the $NZ actually relate to anything?"

The best correlation I've found - and it's not great - is dairy prices.

That is likely having an effect at the moment, I would imagine. Any idea on what is driving the rebalancing on US side?

During the 90s it certainly felt like it. Every time the milk price got on a slight upward movement brash would push interest rates higher and wed cop a double whammy.

The Russo-Chinese blatant and open cable sabotage under the Baltic needs a major response!!

Swedish PM says Baltic sea now ‘high risk’ after suspected cable sabotage | Sweden | The Guardian

About time those resident defanged Vikings get out of their Kategat slumber beds and resurrect their past, glorious, warrior spirit and get their "anger on" and deal with the Yi Peng3 crew, owners and backers, in serious ways!

What's become of the once fearsome Vikings?

The BIGGEST Battles | Vikings

This constant, Russian instigated, sabotage and destruction crap, can't be left to slide.

This latest incident would have been dealt with exceptionally 1000 years ago and it would have been aflamed and soon after, kissing the Baltics dirty bottom.

I like spirit in the hottie Lagerther and the Shieldmaidens in general! Bring them back!

Vikings: What Are Shield-Maidens? History & Mythology Explained

All civilizations in the past had gloriouse armies courageous to unfearless to all empire building. From the Spartans to the Ottomans to Genghis and so on even old Te Rapuhara could get a mention somewhere. The problem is the Vikings as you say if they went out and retalliated against a leader or two (putin, kim,jong) are more likely to increase ghe chance of ww3

No one wants WW3.....yet is ongoing appeasements a viable avenue against the thug regimes?

They should restrain and deal fully investigate this boat, people on board and assess the alleged crimes. Then hit this occurrence hard.

I very much doubt a Chinese ship with do the same in or near USA waters after Jan 20th. There would be no kid gloves used.

It's the end of 400 years of western imperial hegemony, just let it go into the dustbin of history where it belongs.

Be careful what you wish for. The alternatives may be a lot worse.

It's hard to know what to make of your comment without knowing your background. I think it is absolutely essential to maintain Western hegemony but then again I was born an Englishman.

If it is sabotage it is then of the most unsophisticated and clumsy type. With satellite surveillance the vessel, if it was the cause, was always going to be identified. So given that, what then was the motive. It’s moments like these you need Tom Clancy.

FG. I propose motive is relatively simple but clumsy is an understatement for the method, even from the Russians. It's scarcely believable that a cautious operator like Xi would knowingly allow a Chinese vessel to be used. Putin absolutely does not need Baltic states more motivated against his expansionist ambitions, which is what would have happened had the operation been fully successful. This has the hallmarks of a rogue operation. More Michael Palin and the death of Stalin cast than Clancy, I suggest.

Colin C,

All civilizations in the past had gloriouse armies courageous to unfearless to all empire building.

Your command of English is shockingly poor.

Have you never heard of, "stream of consciousness"? My main gripe is with Genghis getting a capital letter while Putin and Kim don't.

Consistency is key when it comes to capitalisation.

@gecko - some truths in there for sure hahah

Did you have this same vociferous response after the US organised destruction of Russia's Nordstream pipeline?

Your proof being?

Seems all western countries were dragging the chain at the start of the war. If the west actually wanted to crush Vlads Mafia mob, they would have gone all in immediately with weapons, instead of drip feeding Ukraine to the point of starvation for three years.

I don't pretend to have any more information than anyone else, but Ukraine seems to have the greatest motivation for stopping Germanys umbilical cord direct to Kremlin coffers? It seemed to work. Once the gas cleared, Germany slowly found the pieces of spine they had lost.

https://www.theguardian.com/world/article/2024/aug/15/ukrainian-team-bl…

Ukraine is an extension of the US deep-state - a sacrificial pawn.

The US did the blowing-up or was at least behind it. Hersh called it - and nobody has sued or imprisoned him in Guantanamo Bay...

Odds-on, even just given their track record.

"......He added: “Now we are careful about not accusing anybody right now of anything. We don’t know that this is sabotage. But we are investigating the matter very carefully......”

KH. Yes. In analysing the boilerplate Kremlin position, expressed here in the characteristic artificially perfect syntax of this contributor, that Western interests sabotaged the Nord pipeline one should not only examine motive and available means, but also consequences of the perpetrator being discovered. For the US they would be catastrophic. In this high surveillance age no sane president would sanction such an operation against the US's critical European allies.

"...no sane president would sanction such an operation"

OK.

Nice comeback, point noted. Poor choice of words.

Aussie housing credit growth is just catching us up after our 2021 madness. Worth noting that the only way RBNZ economic forecasts make sense is if our housing credit growth gets back to the glory days of 7% to 8% annual increases in the latter half of 2025.

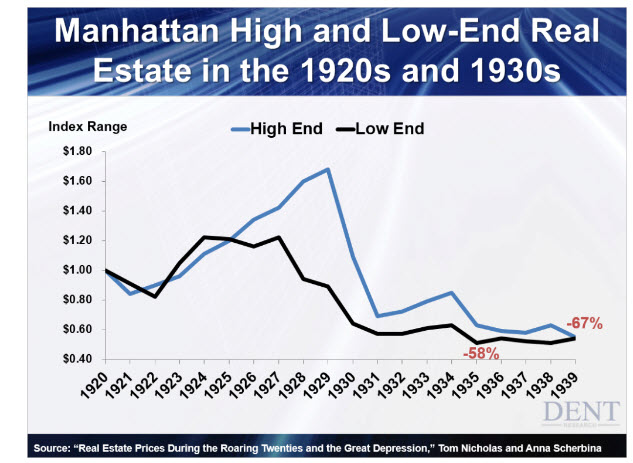

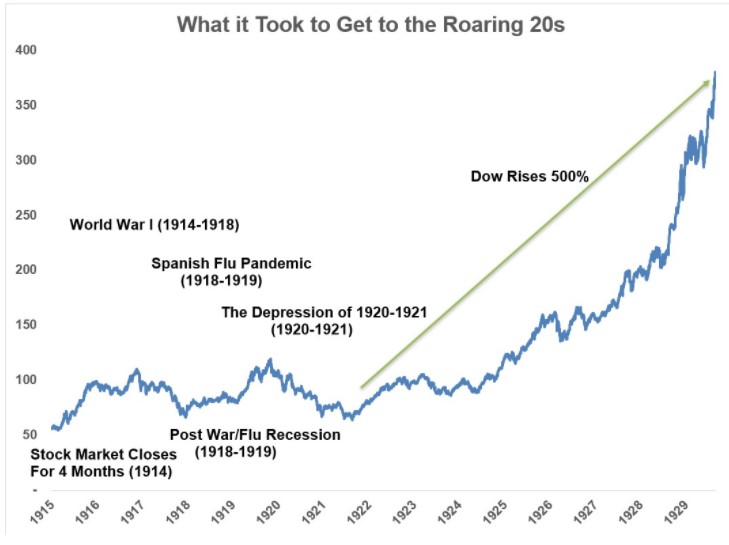

Worth keeping in mind that property prices absolutely boomed in the 1920s as the rich got seriously carried away. This also 'underwrote' much of the stock market foolishness. And in 1929 it all collapsed. How bad? Even 10 years later property hadn't recovered.

{kind=link}

What is it Split Enz says? History never repeats? ... 2029 isn't that far away now. ;-)

edit: Here's a fun little historical graph of that period. Spooky, ay?

{kind=link}

Exactly. The RBNZ are full of s#%t. How manny boffins they have working there? 600?

Just an unbelievably bad institution.

Well this is sickening ...

And it [the second Covid Inquiry] has explicitly excluded the inquiry from looking into the Reserve Bank’s decisions. That exclusion could limit the ability of the royal commission to investigate the inflationary and economic impacts of the Covid-19 pandemic response - which both the National and Green parties called for.

During the pandemic, the Reserve Bank undertook a $30 billion quantitative easing programme which injected money into the economy.

Source: Why is there a second Covid-19 royal commission of inquiry?

Something very, very disturbing is going on here. Given the vast sums of money involved ... well ... you join the dots.

Agreed. Lack of accountability is leading to a loss of faith in the government and RBNZ, and this alone is the foundation of what allows a government to function.

"And that won't change until the incoming government realises what any high school economics student knows - that tariffs are a tax on yourself."

One also hopes those same high school economics students would point out the obscene additional profits that will be made by local suppliers when they raise their prices to be 'just below' the products subjected to tariffs.

This is nothing more than outright market distortion for the benefit of 'Merica's rich.

Tariffs are a proven way of supporting local industry, entrepreneurs and technology. The globalists and multinational corps hate them.

"Tariffs are a proven way of supporting local industry, entrepreneurs and technology. "

... And ensures the local owners get richer too, right? Let's not forget that one, ay?

"The globalists and multinational corps hate them."

So most big US companies, right? And not a few offshore ones that operate in the US too.

And PDK can take this one up ... Tariffs at the levels proposed also results in an appalling misuse in resources.

Have you thought your assertions through?

".. And ensures the local owners get richer too, right? Let's not forget that one, ay?"

Well perhaps many would prefer local owners to get rich rather than overseas owners.

I'm old enough to remember when NZs oligarch of "local owners" (typically a few well known family dynasties) were massively enriched by tariff protections which were enabled by impoverishing everyone else in the country.

Tariffs true enough, but the import licensing is where the control was exerted and the enrichment distributed. Historically tariffs were imposed usually in conjunction with quotas. That provided control as well by way of quantity, alongside price. For instance in 1999 President Clinton imposed both a quota and tariffs on NZ & Australian lamb exports to the USA.

Correct, I missed the ubiquitous import licensing (= license to print money)

"Tariffs are a proven way of supporting local industry, entrepreneurs and technology"

and increasing costs, if that's what you want. Especially when the world does not want inflation to speed up.

Does anyone else think it's hilarious that Trump has just found a way to increase taxes on Americans with Americans joyfully believing that someone else will pay them?

Con of the century !!!

"The UST 10yr yield is now at just on 4.18% and down -6 bps from this time yesterday and down -23 bps from this time last week."

What is driving the change in direction? Everyone seemed to think Trump's policies were going to push it up and up?

Select the 'All' time period. (Back to 1985).

- One way traffic down until recent events. Methinks normal service will resume.

Select the '5Y' time period.

- Lots of peaks but none broke through upper resistance.

Select the '1Y' time period.

- Methinks we'll be testing the most recent trough soon. A breakthrough down would be noteworthy.

But with Trump? I think he'll make a lot of noise that'll result in short term fluctuations with screeds being written and talking heads going apoplectic. (And not a few insiders walking away with billions more.)

But the US bond market is far mightier than Trump (and US stock markets).

"And that won't change until the incoming government realises what any high school economics student knows - that tariffs are a tax on yourself."

Does anyone else think it's hilarious that Trump has just found a way to increase taxes on Americans with Americans joyfully believing that someone else will pay them?

Con of the century !!!

Agreed, Chris! - this is what I wrote yesterday - from the only comment made on this article...

https://www.interest.co.nz/banking/130979/howard-davies-wonders-if-base…

... quoted...

"THE WESTERN NARRATIVE - how vulnerable the Chinese economy is - Yeah right!

Brad Setser, a senior fellow at the U$ Council on Foreign Affairs, is saying that China needs to provide more information on investment income from FDI (Foreign Direct Investment) - IOW on investments, bonds and bank loans.

Why would they show their hand? - especially when the U$ has effectively declared financial war on them, and now that it is all set to be ramped up massively by Trump signalling his idiotic tariffs* - all of this is tragically reminiscent of the Smoot/Hawley debacle from the era of the Great Depression, where this strategy contributed to a 70% reduction in global trade.

*(Trumpster declared the word 'tariff' as his favourite in the entire English language - seemingly even eclipsing 'bigly' and 'warp-speed' !)"

Cheers

Colin Maxwell

Trump is utterly illiterate when it comes to macro-economics and geopolitics.

Some of his recent ravings...

"TRUMP THREATENS BRICS COUNTRIES WITH ‘100% TARIFFS’ UNLESS THEY ABANDON PLANS TO REPLACE THE US DOLLAR

“The idea that the BRICS Countries are trying to move away from the Dollar while we stand by and watch is OVER.

We require a commitment from these Countries that they will neither create a new BRICS Currency nor back any other Currency to replace the mighty U.S. Dollar or, they will face 100% Tariffs and should expect to say goodbye to selling into the wonderful U.S. Economy.

They can go find another ‘sucker!’” Trump said on Truth Social. Trump added that any country that attempts to replace the US dollar in international trade will “wave goodbye to America.”

Russian President Vladimir Putin previously stated that it is too early to talk about the creation of a common BRICS currency, and that there is no such goal at the moment. Putin explained that creating a common currency requires greater integration of the economies of the BRICS member countries and their structural similarity. The Russian president also noted that two-thirds of Russia’s trade turnover is conducted in national currencies — and with BRICS countries, that figure reaches 88%.

(Trump needs to look after himself. He is going to suffer apoplexy because a new currency will come. And in the meantime, the Dollar is abandoned via payment in local currencies – that one is done and dusted! Remember what Putin said? We did not leave the dollar, the dollar left us!""

................................

All these threats by the Trumpster will do is erode the use of the U$ dollar as the reserve currency of choice even faster.

A NEW PARADIGM IN GLOBAL RESERVE CURRENCY MODELS

The situation is coming to a head now that China is painfully aware that a hybrid war with the U$ is already full on, and that a hot war is being openly and explicitly planned by the flailing U$ hegemon.

The Chinese know that dollar-denominated assets are becoming increasingly risky for a multitude of reasons, but with the caveat that sudden divestment, as opposed to stealth, would be an irresponsible destabilisation of the global financial architecture that would not benefit any of the parties involved.

What has transpired now is a situation where China can use the U$ dollar for capital control, but principally in the context that it too is a tool to be deployed as the new global financial architecture takes shape.

China has moved hundreds of millions of dollars out of Western financial systems and banks, and into its domestic institutions.

All of the distrust of the U$ hegemonic status quo went onto steroids when they effectively stole all Russian dollar-denominated assets held in Western banks - there could be no clearer signal, that if a country doesn't want to be victimised for pursuing genuine economic sovereignty, then they needed a completely new strategy - QUICKLY!

As tranches of U$ treasury bonds mature, they now collect the face value of those bonds in dollars. The combined surplus heads relentlessly to $1 trillion and beyond, particularly after the overt theft of over $300 billion of Russian reserves held in Western Banks, which in turn put the entire global system into disarray.

The new situation is that the BRICS+ countries will now use dollars to their advantage. They don't mind using dollars - what they hate is the Western private banking system and the risks of keeping dollar-denominated instruments in these banks.

The new game in town is that China and BRICS+ will hold these dollars within their own banks. They will now sell U$ bonds, and U$ companies in the U$, and lay off workers so that they can bring those dollars back to China too.

Meanwhile, China's FDI (Foreign Direct Investment) continues to rise dramatically - just not into the U$.

The trade deficit for the U$ with China hit a 2-year high in July of 2023, at around $27.23 billion for the month (that's almost $1 billion per day). Not only is China not using this surplus to buy treasuries - they are selling them in the U$ and in other places too - and where are these dollars going?

They are lending most of them to their global trading partners - a massive gut punch to the U$ hegemon. These dollars were, in reality, loans made to U$ taxpayers who have to pay them back, including accruing interest.

These same dollars are now being deployed in a new financial system that generates billions of dollars of real economic activity that benefits China and the giant BRICS bloc.

Trump is far too thick to realise it, but all his threats and ravings will do is accelerate the now inevitable de-dollarisation process.

Time to break out the beers and popcorn

Colin Maxwell

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.