Here are the key things you need to know before you leave work today (or if you work from home, before you shutdown your laptop).

MORTGAGE/LOAN RATE CHANGES

SBS Bank cut its floating rate today by the full -50 bps. But it only cut its reverse equity rate by -10 bps. NBS cut its floating rate by -31 bps to 8.44%. All rates are here.

TERM DEPOSIT/SAVINGS RATE CHANGES

SBS Bank has cut between -25 and -50 bps to its savings accounts. Nelson Building Society (NBS) cut their by -25 bps. All updated rates less than 1 year are here, for 1-5 years, they are here.

BORDER APPROVALS STILL ELEVATED

About 15,000 work visas & 5000 residence visas are being approved each month. There were around 188,000 people here on work visas, MBIE figures show for September.

CONDITIONS EASE - FOR SOME

The RBNZ September Credit Conditions survey shows banks expect demand for debt to rise over the next six months - except by corporate, commercial property, and agriculture. The expected rise in debt demand for housing is largely as a result of regulatory change factors.

NZX EQUITY MARKET UPDATE

Check out our quick update of how the NZX is faring today, as at 3pm. Gentrack rise extends. Spark get a gain. a2Milk falls again along with Scales and Port of Tauranga.

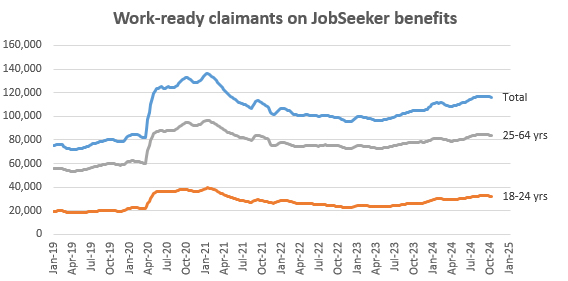

JOBLESS BENEFIT CLAIMS FALL

We are now monitoring New Zealand weekly jobless benefit claim levels. New administrative effort is going into getting work-ready claimants back into work. Last week (to October 11) the JobSeeker benefit totals fell by -366 (of which 255 shifted into jobs), after falling by -480 the prior week. There are now 116,100 "work-ready" people on this JobSeeker benefit, 32,300 under 25s and 83,800 aged 25-64. The 116,200 current total is +11,500 more than in the same week a year ago. Of course, the weekly data is seasonal and it is usual for the October weeks to show reductions from prior weeks. This chart helps put these changes in perspective.

{kind=link}

MINIMAL DETERRENCE?

An Auckland man who failed to declare income from building work has been sentenced to a year’s home detention. Kahdim Ali was sentenced in the Manukau District Court on October 4 after pleading guilty to 35 charges including evading or attempting to evade the assessment or payment of personal income tax, GST as well as income tax and GST of his company. The amounts involved were more than $348,000, although all has now been paid back. Ali worked in the construction sector for more than a decade.

DAIRY DISPUTE WITH CANADA GOES TO NEXT STAGE

New Zealand has today notified the Canadian Government and other Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) members that it has triggered mandatory negotiations in a dairy dispute with Canada.

TIME TO HEDGE?

Westpac NZ has released a research note for clients that notes that NZ swap rates have fallen sharply over the past year and are now at attractive hedging levels. "If we assume for a moment that markets have correctly priced the OCR path, then there is no economic advantage or disadvantage to hedging now vs waiting - the two are equivalent." Contact the Westpac Strategy team for the full details.

SERIOUSLY MISLEADING

In Australia, their Federal Court today ruled Latitude Finance Australia and Harvey Norman engaged in misleading conduct and made false or misleading representations in relation to a widespread advertising campaign for a 60-month interest free and no deposit payment method.

UNWANTED 9 YEAR RECORD

China’s new home prices in their 70 major cities fell -5.7% in September from a year ago, more than the -5.3% fall in the previous month. It was the 15th straight month of decrease and the steepest pace since May 2015. Second hand houses seem to have fallen by much more, by -10.7%. This sector won;t be helping China's "wealth effect".

BETTER THAN EXPECTED

Meanwhile China said its Q3-2024 GDP expanded by +4.6%, marginally better than the +4.5% expected. They also said industrial production improved to +5.4% and retail sales up 3.2%, on the same basis. Their jobless rate fell slightly, to 5.1%.

JAPANESE INFLATION EASES BACK - BUT STILL ABOVE 2%

Japan said its inflation rate fell to 2.5 in September from 3.0% in August. This was its lowest level since April. (It was also 3.0% in September 2023.)

SWAP RATES HOLD LOW

Wholesale swap rates are probably little-changed today at the shorter end. Our chart below will record the final positions. The 90 day bank bill rate is unchanged at 4.59%. The Australian 10 year bond yield is up another +6 bps to 4.35%. The China 10 year bond rate is down -2 bps at 2.08%. The NZ Government 10 year bond rate is up +5 bps from this time yesterday at 4.51%. And the earlier RBNZ fix was at at 4.44% and up +6 bps from yesterday. The UST 10yr yield is now at 4.03% and unchanged from yesterday. Their 2yr is also holding at 3.94%, so that curve is stays positive by +9 bps.

EQUITIES MARK TIME

The NZX50 is now up just +0.1% in late Friday trade. The ASX200 is down -0.7% in afternoon trade. Tokyo is up +0.3% at its Friday open. Hong Kong is up +0.5% at its open. Shanghai started unchanged at its open. Singapore is trading up a very minor +0.1%. Wall Street ended its Thursday session unchanged on the S&P500.

OIL LITTLE-CHANGED

The oil price is -50 USc softer from this time yesterday at just under US$70.50/bbl in the US, and just on US$74.50/bbl for the international Brent price.

CARBON PRICE FIRMISH

The carbon price rose marginally today to $63/NZU. But that is its highest level since March 2024. See our new daily chart tracker of the NZU price for carbon, courtesy of emsTradepoint.

GOLD AT ANOTHER NEW ATH

In early Asian trade, gold is up +US$22 from this time yesterday, now at US$2704/oz and a new all-time high.

NZD LITTLE-CHANGED

The Kiwi dollar is down -10 bps from this time yesterday at 60.6 USc. Against the Aussie we are little-changed at 90.5 AUc. And against the euro we are up +10 bps at 56 euro cents. This all means the TWI-5 is essentially unchanged from this time yesterday at 69.2.

BITCOIN GETS ANOTHER MODEST RISE

The bitcoin price is up another +0.5% from this time yesterday, now at US$68,108. Volatility of the past 24 hours has been modest at just on +/- 1.1%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

61 Comments

"Some banks reported that the activation of restrictions on debt-to-income (DTI) ratios has required additional documentation from borrowers to ensure compliance with prudential requirements. "

Good to see it's a noted factor. Now what we need is for the ratios to be reduced from their starting levels to more meaningful ones. Copy the UK for a start if necessary, but the ratios need to be lowered.

Axe them altogether. Converting a supply / demand system into a government knows best system is almost guaranteed to fail.

Have we forgotten the Sub-Prime Loans disaster, and the resultant aftermath, of not that long ago? Maybe we didn't get hit as badly as The States etc. But the underlying cause is still with us this very day.

Ignore JJ. It's quite clear JJ has absolutely no idea what he/she is talking about.

(See my post further down. This shit-posting is exasperating and just makes Kiwis more confused (dumber?) than they should be.)

If anything's confused, it's the zeal and enthusiasm being placed in this tool.

It *could* make the financial system more resilient to a crisis.

It likely won't improve ownership rates, make things easier for FHBs, or make houses more affordable.

It's like some of you were told by your cheap uncle you're getting a games console for XMAS. You're expecting a PlayStation 5, and what you unwrap is a knock-off labelled "Polystation".

I agree. DTI's aren't the way to go. As I've said before, make the stress test rates count for something and legislate these to be the maximum rate a loan can be charged for the full term.

Nothing stopping the bank from testing its customers at 2% if they really wanted to, but if interest rates were to rise across the board the banks (not the borrower) would be on the hook for that difference.

I'd probably leave the DTI's from the perspective of anything that reduces debt is 'good'.

But I'm 100% on board with this:

make the stress test rates count for something and legislate these to be the maximum rate a loan can be charged for the full term.

"stress test rates" apply to each lender.

DTIs apply to the whole of a bank's lending, and not a single borrower..

Banks still have plenty of leeway as to which borrower they lend to.

On an aggregate level, the effect is about the same.

How many sub prime mortgages do you think would have qualified under a DTI regime?

Totally this. We need to make buying a house like buying any other consumable item.

Instead, it's a super special precious, and we think we can tinker tax and debt sliders to sort out what is a physical problem.

JimboJones: "Axe them [DTIs] altogether. Converting a supply / demand system into a government knows best system is almost guaranteed to fail."

Here we go again ...

Now for some facts !!!

- DTIs apply to the aggregate of a bank's lending on mortgages. In aggregate, they perform much the same function as stress test rates

- DTIs are a macro prudential tool. Same as LVRs which we've had for years.

- DTIs are implemented, set and (hopefully) enforced by the RBNZ.

- The RBNZ - once again (AND HOW MANY TIMES MUST THIS BE POINTED OUT !!!) is not part of 'the government'

None of that refutes Jimbo's claim.

And you can't produce a fact that shows DTIs make housing more accessible for FHBs, nor prevent bubbles.

Whatever ...

Its like trying to have a discussion about faith with a religious zealot.

Sorry Pa1nter. When you stop trolling with irrelevancies, maybe I'll respond. Until then, whatever ... Ramen.

I would've thought evidence supporting the efficacy of DTIs was highly relevant.

But I suppose like a lot of things, relevance is subjective. Like when I ask you to substantiate, it's a troll, and when you do, it's just good old fashioned inquisativeness in the spirit of intellectual honesty.

Must be choice to make all the rules up as you go.

Pa1nter:

I would've thought evidence supporting the efficacy of DTIs was highly relevant.

But I suppose like a lot of things, relevance is subjective. Like when I ask you to substantiate, it's a troll, and when you do, it's just good old fashioned inquisativeness in the spirit of intellectual honesty.

Must be choice to make all the rules up as you go.

Might I suggest you to do some work on your own - spouting drivel and then demanding others do the work for you is extremely tiresome.

You could start here. I expect they have many documents explaining the efficacy of DTIs.

Ramen.

Usually the burden of proof is on the claimant. For someone who feels so strongly so as to promote something for months on end (maybe years even), good evidence should be readily at hand. It's what you usually source BEFORE making such a strong claim.

I don't see DTIs (or similar) making housing more affordable, or accessible overseas, nor preventing bubbles.

Then again, housing affordability isn't mentioned by the RBNZ as one of it's aims in implementing a DTI. But I suppose that won't prevent people from continually falsely ascribing that feature to it.

I see it as fairly obvious how DTIs would be useful in some circumstances, particularly the very low interest rates we saw over COVID which are associated with a very unstable pop in house prices.

An effective DTI refine effectively caps lending capacity in that case, so the amount that the market as a whole can borrow increases with income, rather than inversely with interest rates. Maybe there'd still be price rises driven by things like working from home changing dynamics etc, but it is intuitive to me that DTI restrictions would take the sting out of such unsustainable rises.

Not a knock-out blow, or an instant anchor to prices, but a smoothing function which is exactly what a body charged with financial stability should be pursuing.

I don't have reams of evidence to show you, but if I had the time and energy I would be looking at the evidence that the RBNZ presented when they argued for the government to add DTIs to their toolkit.

Yeah I mean their main aim with a lot of these measures is to add stability to the financial system.

But if we take LVRs for an example, now just over 10 years old, aside from making deposits way harder for FHBs, what has it improved? The housing market didn't get better (many would argue it's worse than ever). Having double the threshold for investors hasn't curtailed landlording. And on top of that, in 2020 when the government dropped the OCR, they also lowered the LVR requirements.

People are falsely viewing these tools as saviours. If real change is desired, as Jimbo says, it'll take a hell of a lot more than this sort of tinkering.

I think there's a lot more work involved in assessing LVRs than what you've got there. We're not comparing today vs 10+ years ago, we need to compare today vs the hypothetical today without LVRs. Beyond my pay grade in afraid.

There may be a whole cohort of 2021-2 would-be FHBs who aren't currently suffering from terrible negative equity because LVRs were in place to keep them safe, for example. Most of the current negative equity stories are of the 'our 20% deposit has gone as the price fell 22%' type- quite different to the GFC-style 'i borrowed 95-110% of the value and now my net worth is horribly negative'.

I'd tend to agree with you, it's likely dulled the number of underwater or defaulting mortgages.

The take home should be though that none of these measures lead to increased home ownership rates. More likely the opposite.

"I think there's a lot more work involved in assessing LVRs [and DTIs] than what you've got there."

And you'd be right, mfd.

Some people overlook a few things ...

- The RBNZ sets an OCR that applies to everything, not just mortgage interest rate.

- When the OCR is higher than the neutral rate - everyone, including and especially NZ's businesses, takes a hit.

- But when the OCR is lower than the neutral rate - everyone wants debt, but the RBNZ needs the levers to control whether too much debt gets directed at housing, and both LVRs and DTIs are required to control where debt is allocated. Neither ratios, used in isolation, is effective in this goal.

- The LVRs and DTIs serve similar purposes, but operate differently. (Those who invest in commercial property will be much more familiar why both are required, and how both are key to understanding the strength of a commercial property company)

- For both the LVRs and the DTIs, there are two separate restrictions.

- One set applies to owner occupiers (and FHBs) and the other set applies to residential property 'investors'.

- In effect, by tweaking the LVRs and DTIs, separately for OOs and 'investors', the RBNZ can loosely control how much debt is flowing into our residential property market.

- The RBNZ's tweaking of the 4 separate ratios is tricky because of the competing interests.

- They have to balance where debt is allocated, i.e. mortgages vs all the other places, including NZ's businesses. And the need to balance the financialization of property, between those that need somewhere to live vs. those that are after the income and the tax free capital gains.

It's going to be an interesting decade or so as the RBNZ gets to grips using all 4. I expect they will get better as time goes on.

Yes would be good for the NZ financial system if the DTIs could be adjusted back to 6 max. If housing investment ever looks like its getting out of control again the trigger needs to be ready. The big advantage will be the OCR for everyone else including real business wont have to go so high.

Drop the DTI by 5 basis pts a month for 60 months and markets will price that in.

Aren't DTIs slightly different in the UK? I thought they were (total monthly debt payments) / (total gross monthly income) rather than ours which are done on total debt to total income?

I'm a bit out of touch with the UK regulations ... But my understand is ...

... that loan-to-income ratios (LTIs as they're known in the UK) of 4.5 or more are limited to 15 per cent of a UK lender's new residential mortgage lending. So in effect, they're quite similar to what the RBNZ has implemented ... albeit quite a bit tighter. Our DTIs are higher, and our banks have greater leeway. (Sorry, can't remember if they have one for OOs and another 'investors' like we do.)

They did have something on an individual borrower level but I think it was removed. (Introduced after the GFC (circa 2013?) and removed during / after covid?)

David, MSD case workers started moving people off jobseekers work ready and onto jobseekers health and disability a few months ago (around same time they stepped up application of sanctions). So, jobseeker work ready numbers are going down, and health and disability numbers are going up. I would report on the combined total. Goodhart's law in action here!

Not surprising. I heard from an ex-manager that the Key government also had to deal with the public sector going rogue in their early years of power.

A big reason why his government side-stepped bureaucrats and outsourced a lot of policy work to consultants.

MSD don't need much encouragement to be mean to be fair. What appears to have happened is that MSD had people who were clearly not 'work ready' sat on 'work ready' jobseekers benefits. So, when it came to getting tough on people to come to interviews and reviews, show evidence of seeking work etc, there were people near death in hospital at risk of being sanctioned. So, case workers moved those people onto 'health condition and disability' where presumably they don't come under as much scrutiny. We have also see some movement from jobseekers health condition and disability to 'supported living' health condition and disability.

would be good to see numbers side by side to make conclusions... Where should one look JFoe

Presumably they would need a doctor's certificate to sign off on the health condition?

For the supported living variant, yes. You have three levels - js work ready - js health / disability - supported living health / disability. The latter is very hard to get

The latter needs signoff from some form of regional health or disability or entity ive been told by a GP who does some work in that space.

Hi David, Re JOBLESS BENEFIT CLAIMS FALL "There are now 116,100 "work-ready" people on this JobSeeker benefit, 32,300 under 25s and 83,800 aged 25-64. The 116,200 current total is -11,500 less than in the same week a year ago."

It should be 11,500 more than in the same week a year ago.

Thank you, yes, you are right of course. My mistake. Para is corrected now.

In early Asian trade, gold is up +US$22 from this time yesterday, now at US$2704/oz and a new all-time high.

Ray Dalio says "if you don't own gold, you know neither history nor economics." Food for thought. Take your pick: Ray Dalio or the Aotearoa BBQs and bank economists.

Ray goes on:

"We are currently in the late and perilous phase of the long-term debt cycle. The levels of debt assets and liabilities have soared to such heights that it has become challenging to offer lender-creditors a sufficiently high interest rate in relation to inflation."

https://www.jpost.com/business-and-innovation/precious-metals/article-8…

We are currently in the late and perilous phase of the long-term debt cycle √

The levels of debt assets and liabilities have soared √

We may witness a significant economic contraction and a restructuring of debt and finance that will catch many unprepared. √

This could lead to either significantly higher interest rates or extensive money printing √ √

These are currently unfashionable views that Ray is talking. The economerati seem to think everything is hunky dory. Even better than before.

Half a trillion dollars has been printed in a matter of days leading up the US election. It's unclear as to why. Funding new govt jobs? Covid coming back? New war?

Humongous reckless govt spending and an exponential rise in debt. More units of debt required to drive each unit of GDP.

https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-…

This is 2022 Ray "China's going to eat the US' lunch" Dalio?

Lol

Spot on if you ask me. Two years later they have finished eating it.

Most of the most well known and reported names work for the big NZ Banks.

everything is hunky dory.

Look at this another way. What level of savings do you think are required for the future? Let's assume that people need two to three percent of GDP put aside as savings so that they can buy what they need in the future when they are no longer working. Having made this assumption you now, by mathematical certainty, need debt to increase by at least this amount. That's just to provide for domestic savings needs. If as a country you run a trade / current account deficit then you also need to satiate offshore savings needs. Let's say that adds another two or three percent of GDP of annual debt required.

From 1990 to 2008 we used liberalised banks, the housing market and business credit boom to get this debt flowing - taking private debt from 60% to 150% of GDP. Since 2010 we have used gradually reducing interest rates to squeeze the last out of the private debt fuelled economic strategy.

We need to get back to a circular private sector economy in which money is kept moving domestically - that means not letting financial assets pool in the savings of the few, and it means addressing our current account deficit. Govt needs a strategy to achieve this shift, which will definitely involve taking private debt onto the crown balance sheet. I'm not holding my breath.

Govt needs a strategy to achieve this shift, which will definitely involve taking private debt onto the crown balance sheet. I'm not holding my breath.

I get you. So once the pvte sector debt shifts to the crown balance sheet, what happens then? Assume there is no kind of monetary reset, do we simply wind into the private credit cycle again? What is the trigger that indicates that this should start? And what are the implications for the peasants? What happens to the fruits of our labor that we store for our own security?

First, it is important to note that we have just dropped private debt levels back to around 137% of GDP, so we are good to go for another round of low interest rate fuelled 'growth'. We could repeat this a few times I guess, although I am not sure it will play the same unless we also get another round of oil / import deflation (as we did between 2010 and 2020).

If we want to get off the ever-growing debt track, we also need get off the ever-growing savings track. They run in parallel. To do this, we need to build the capacity and capabilities we need to make the future easy and cheap. We can absolutely support our population to live good lives, but we will need more people doing useful things, and fewer people doing bullshit jobs. This obviously requires a plan and collective action - a warlike effort. We might make this effort when the waves occupy Parliament Grounds!

First, it is important to note that we have just dropped private debt levels back to around 137% of GDP, so we are good to go for another round of low interest rate fuelled 'growth'

Sure. But if we go into another wave of cost of debt suppression, ultimately it's going to dilute broad money even further. More destruction of the value of labor at a time in history when labor demand, particularly across developed nations, is falling.

So's the supply though.

Extremely so, in certain fields.

"we need to make the future easy and cheap. We can absolutely support our population to live good lives, but we will need more people doing useful things,"

The money shot, or whatever the literary equivalent is, because the system we currently have is doing the very opposite.

A successful economy is producing more things, of a better quality, at a lower price. And as part of that, everyone benefits - those at the Top and those at the Bottom and Everyone in between. This "we must have 2% price rises every year" policy is part of the problem. All that does is mandate more Debt.

A successful economy is producing more things, of a better quality, at a lower price. And as part of that, everyone benefits - those at the Top and those at the Bottom and Everyone in between.

Bingo

Sitting in on the RBNZ consulting for the inflation target, I was struck by how they literally discarded a 0% target rate.

0% would imply a balance between consumers and producers, but instead we want to [slightly] shift to more consumers. If each person is both a consumer and producer, this then implies consumers taking out forward bets (debt) to overconsume their production.

I get that a debt correction is what should happen, but you have to believe that the Reserve Banks also agree.

Instead what actually happens is we keep kicking the can down the road. At some point Ray Dalio may be right, but this time? Maybe, maybe not.

Instead what actually happens is we keep kicking the can down the road. At some point Ray Dalio may be right, but this time? Maybe, maybe not.

Agree. What if Ray's wrong and this time is actually different?

This is summed up by Chuck Price, Citigroup CEO July 2007

“When the music stops, in terms of liquidity, things will be complicated,” Prince said. “But as long as the music is playing, you’ve got to get up and dance.”

Its all about the music and the band.

Yes indeed. BTW, traders who have been 'long gold, short LT UST futures' since 2014 have been returning 12% CAGR on low volatility. This correlates with global central banks stopping the growing of holdings of USTs in favor of gold.

Very few Western bond investors have had this trade on.

Bloomie takes on how entering the middle class is increasingly out of reach for Americans. Quite well done using property and education as two measures of why so many people are screwed. They stop short at pointing out why this is really happening.

That represents a repricing of the American Dream, in which some of a family’s biggest expenditures — the ones that are foundations of long-term economic security and also the coveted rewards of hard work and striving — are often overwhelming.

Some of this is the legacy of a now-unwinding period of tight monetary policy, with the Federal Reserve’s campaign of rate hikes making mortgage and auto loan payments more daunting. But many of the forces bearing down on consumers have been gathering strength for much longer than that. College and child-care costs have been escalating for a generation, while eye-watering housing prices reflect a supply shortage more than a decade in the making.

https://www.bloomberg.com/news/features/2024-10-17/costlier-housing-car…

"Existing homeowners, who secured ultra-low mortgage rates during the pandemic, are still reluctant to put their properties on the market"

And why would they if they've locked in at 30 years fixed at 2.5% ! Unintended consequences are yet to play out.

That Westpac swaps bit is weird. What's going on?

Yes,I also hoped some wise commentator would expand on that.( As I am mainly invested in bonds), I read it broadly as a prediction that rates on mid / long bonds may not fall much more and the cost/ risk profile of hedging mid- long is about even, so not worth the cost.

Can anyone expand more technically than " my reckons " ,please.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.