Banks will likely soon be "constrained" in how much they drop their mortgage rates, Reserve Bank (RBNZ) Assistant Governor Karen Silk says.

Silk, who is also General Manager of Economics, Financial Markets and Banking, and sits on the RBNZ's Monetary Policy Committee (MPC) told a Citi Australia & New Zealand Investment Conference in Sydney on Wednesday that "reversion to pre-covid funding conditions" is under way for banks.

"...All else being equal", this will constrain how far lending rates will fall "as banks seek to preserve their net interest margin" she said.

Banks are currently engaged in a furious mortgage rate cutting battle as they fight for market share. Traditionally popular one-year fixed mortgage rates are now pushing under 6%, while the Official Cash Rate (OCR), set by the RBNZ's MPC is currently at 4.75%. This is an unusually small gap.

Silk said that in the current "low credit growth environment", home loan rates have responded to falling wholesale rates as markets have pre-positioned future OCR cuts.

"Likewise, borrowers have been fixing interest rates for shorter terms, which all else being equal, should reduce the time it takes for lower interest rates to be reflected in household and business cashflows.

"Our latest New Credit Flows survey shows that around 75% of new home loan flows currently carry interest periods of one-year or less and circa 70% of existing home loans will be repriced within the next nine months."

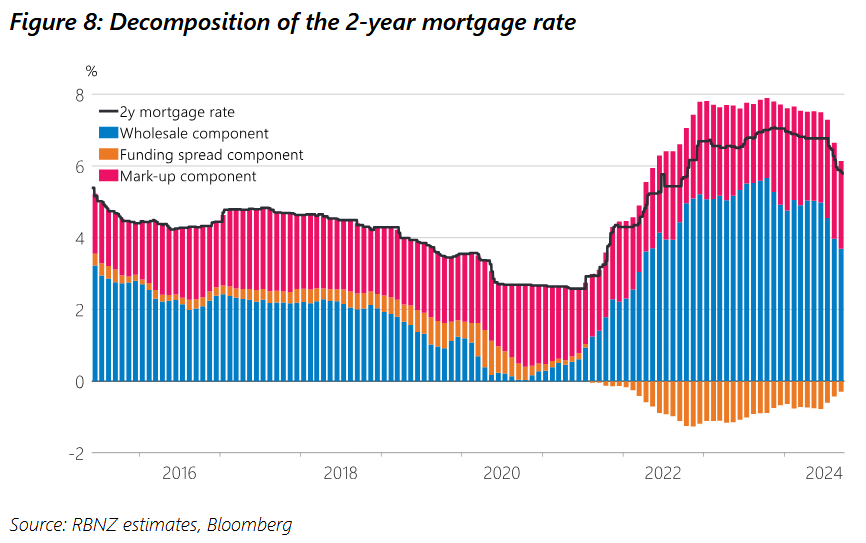

Bank funding spreads, however, have gradually increased this year, Silk said.

"And this is expected to continue as excess liquidity is drained from the banking system with the progressive wind down of additional monetary policy tools.

"Over time this is likely to influence the amount of the decline in bank lending rates, even in the face of lower wholesale rates, as banks seek to maintain their net interest margins."

Silk said the banks' funding spreads - reflecting the difference between the rates that banks pay for retail deposits and wholesale funding versus wholesale rates - "experienced a major shift from mid-2020" as a result of a higher volume of low-cost deposits within the bank funding mix.

"This shift has had meaningful implications for the pass-through of policy rate changes to home loan rates."

Silk said through the OCR tightening cycle [in which the OCR was raised from 0.25% to 5.5%], the trough-to-peak increase in the New Zealand wholesale two-year swap rate was 570 basis points.

"However, the lower cost of funding experienced through that period by banks, as represented by the funding spread, meant that this increase was not fully passed- through to home loan rates, with a trough-to-peak increase in the two-year mortgage rate of 450 basis points."

Silk said the RBNZ estimate of the average bank mark up on a two-year mortgage through the same period increased from around 2.0% to 2.8%.

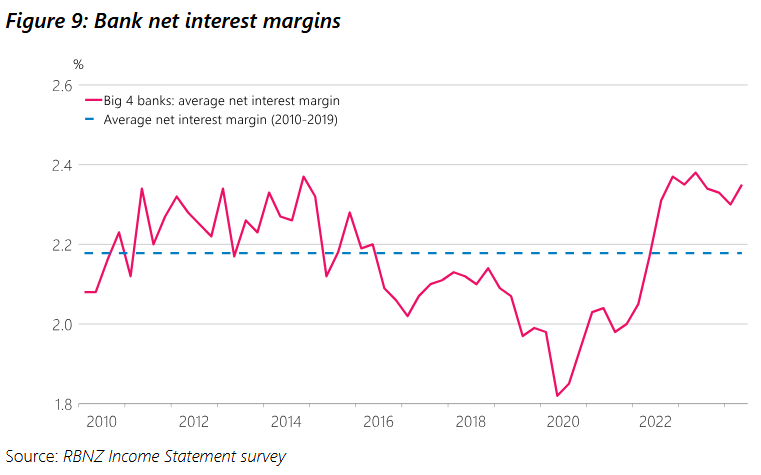

"As home loans account for a large proportion of total bank assets (currently around 50% on average), this contributed to an increase in the net interest margin generated by banks through this period."

From the first OCR increase in October 2021 to the last one in May 2023, the biggest four banks in New Zealand, on average, saw their net interest margins increase by about 35 basis points to 40 basis points, she said.

"The upshot of this is that financial conditions were less restrictive during the recent tightening cycle for the same level of the OCR when compared with previous cycles.

"However, through ongoing monitoring we have been able to identify and factor this into our decision-making to ensure that financial conditions have been where we needed them to be to achieve our monetary policy objectives.

"The OCR, and wholesale rates, have been slightly higher than they otherwise would have been to account for this."

Silk said, however, that given bank funding spreads have already begun to normalise, the offset required as the OCR comes down will likely be much smaller than was the case during the tightening cycle, "which will reduce the need to factor this into OCR decisions to the same degree in the years ahead".

The speech on Wednesday was given a short time after release of NZ Consumers Price Index (CPI) figures for the September quarter that showed annual inflation moving (at 2.2%) back into the RBNZ's 1% to 3% target range for the first time in three-and-a-half years and towards the RBNZ's explicit target of 2%.

Silk didn't comment on the figures, but said monetary policy is working, "and we have confidence that inflation is moving back to its target level".

"Over recent meetings the Committee [MPC] has become increasingly confident that monetary policy has had the desired effect, and that economic conditions are supporting the convergence of CPI back to the target mid-point of 2%."

Silk said, however, the RBNZ was are also "conscious of the broader set of economic conditions required to manage inflation back to target".

"We will continue to assess and respond to risks, on both sides of the ledger."

32 Comments

Banks are currently engaged in a furious mortgage rate cutting battle as they fight for market share. Traditionally popular one-year fixed mortgage rates are now pushing under 6%, while the Official Cash Rate (OCR), set by the RBNZ's MPC is currently at 4.75%. This is an unusually small gap.

so when banks are competing heavily, RBNZ steps in and says no, you cannot do that.

Um. No ...

Banks are fighting to protect their extremely (by OECD standards) fat 2% margins. Read again with that thought in mind - front and center.

No, it's simply an observation from the RBNZ, they will not "step in and says no, you cannot do that".

It’s insane, isn’t it? The RBNZ has to be one of the most repugnant organisations in New Zealand. Actually evil.

Quiet frankly a bit shocked on how appropriate it is for her to be defending the banks here....is she going into bat for the people of NZ, from these comments she comes across as a stooge for one of the big banks.

Arguably the RBNZ is owned by 'the people.' Quite different to the Federal Reserve which operates as a unique entity combining public and private characteristics. The Board of Governors is a government agency, while the twelve Federal Reserve Banks function like private corporations. Member banks must hold stock in their regional Reserve Banks, but this stock does not confer ownership rights typical of private companies.

"Arguably the RBNZ is owned by 'the people.'" ... I enjoyed that joke - for about 3 seconds - then I got angry - very angry.

The vast majority of central bank shares around the world are owned 100% by their countries' governments.

There are only 9 in total that I can identify where the shares are not all owned by their respective governments. I have listed them here by country with the % of shares that are government owned...

United States 0%

Italy 0%

South Africa 0%

Greece 35%

Belgium 50%

Switzerland 51%

Turkey 51%

Japan 55%

San Marino 67%

That said, share ownership appears to have a very loose relationship in terms of policy and control. In my view, the only certainty is that none of them are, by any stretch of the imagination, genuinely independent.

62 countries CBs, including the RBNZ are paid-up members of the BIS (Bank for International Settlements) based in Basel, Switzerland - they appear to follow the BIS pump and dump playbook which always favours the parasitic financial economy at the expense of society and the productive economy.

Up until the recent Jan 1, 2023 reclassification of physical gold as a Tier 1 balance sheet asset, there was a powerful concerted effort within this club to try to hide the plummeting value of fiat currencies by manipulating the price of gold.

This orchestration has now splintered and the Fed is the only major CB that bet against gold. As such the world faces a looming and completely new paradigm in terms of central banking behaviour, sound money, and fiat versus hard-backed currencies.

NZ and Canada both have zero gold reserves - we will be left out in the cold as well. Any country with half a brain would have done at the very least a modest amount of gold-stacking during this prolonged period (some 50 years) of orchestrated physical gold price suppression.

After the BRICS Summit, due to be held in Kazan in 6 days time, we will know more, but at any stage, we could find that these countries revalue gold simply by announcing a buy price for physical gold at the Moscow and Shanghai exchanges.

They could back their main BRICS bloc national currencies with gold - whilst they prepare their new trade settlement-only currency instrument (the UNIT) - another new global paradigm - IOWs a brand-new reserve currency, that is the first in history non-national reserve currency alternative.

When that day eventually arrives, global financial markets and Western fiat currencies will face their day of reckoning. NZ, which has made zero preparations for this event and carries massive total debt, will not fare well.

Colin Maxwell

Since returning to NZ in 2012 Karen has held a number of Senior Executive roles with Westpac New Zealand including: General Manager Institutional and Business Banking; CEO of Westpac’s NZ Branch covering financial markets and international operations; CEO of Westpac’s insurance arm, Westpac Life; CEO of Westpac Funds Management arm, BTNZ and more recently as General Manager of the Experience Hub leading the design and delivery of products and services for Westpac’s New Zealand customer base.

People will make a lot of friends throughout their career. I assume she left Westpac on good terms.

Yes. Game of Mates. RBNZ, FMA, etc.

More like Game of Thrones. Oh. You've never played the game, J.C.? Or perhaps you have, and like me, you're disgusted by it?

You've never played the game, J.C.? Or perhaps you have, and like me, you're disgusted by it?

It's not my cup of tea personally. Too much independence has to be given up. But I understand why it's played.

"a bit shocked on how appropriate it is for her to be defending the banks here"

What gives you the impression that Silk is "defending the banks here" ?

Now explain why the Floating Rates are so much higher than the OCR

Seems insane RBNZ aren't interested in doing anything about the floating rate gouging in NZ. If we had similar levels of floating to Aussie our monetary policy would work much quicker

In other words Floating rates are likely to fall more than fixed rates

Floating rates change with the OCR - not always the case with fixed rates

Perhaps they are seeing too greater value of mortgage lending in fixed and want to change that. Ideally if there wasn’t so bigger difference between floating and fixed, we would be more responsive to OCR changes and the lag effect would be lessened somewhat.

Might correct you a bit?

Floating rates change with the OCR when the bank's shareholder's profits say they can - not always the case with fixed rates.

Let's be clear, shareholder returns come way, way before just about everything else they pretend they're saying. This shouldn't be a revelation to anyone. This is how it is, and has been, for as long as you've been alive. This is banking.

Quite extraordinary really to have the RBNZ telling the Aussie owned Banks it's ok to charge more!!

Just highlights how completely out of touch the RBNZ is.

I'm confused - thought we wanted more competition in the banking sector?

Or if the RBNZ holds up rates, new entrants come in but the customer is no better off?

Somewhat true.

When rates are high, new entrants are priced out. But when wholesale rates start to fall, new entrants have an opportunity. (But at this time, it is way more complex than that. New regulations ... )

"Quite extraordinary really to have the RBNZ telling the Aussie owned Banks it's ok to charge more!!"

That's not the case, bank rates will be decided by competion for business share, not by what Silk thinks will happen.

ANZ seems to understand how to break the "constraints" kiwibank is floundering

The banks are not, it would seem, so constrained when it comes to what they are willing to offer savers for their deposits. Deposit rates very quick to move down.

The same goes for business rates. I spoke to my bus manager, od rate down to 10.5%, no chat yet about loan I have on floating (currently 8.75%)... he said it won't happen overnight, but it will happen.... look a squirrel !

Silk is a newish member at the RBNZ's f'up committee. (Sorry, that's caustic.)

Banks are currently engaged in a furious mortgage rate cutting battle as they fight for market share.

This is the only sentence worth reading, minus the word "currently". It's a confused speech by Silk, and going by some comments, several posters seem to think that the RBNZ is dictating where bank's interest rates should be. That is simply not the case, forget about Silk's blah blah. Retail banks compete for business or marketshare, and their NIMs (Net Interest Margins) will be dictated by how many loans they can write, not by what the Silk says.

If you want my opinion, there will still be strong competition for banks to write new loans because the NZ economy is weak and buyers of RE will be scarce. I think the low NIMs (less than 2% above the OCR) will remain for some time.

A load of waffle to justify the RBNZs incompetence? To blame shift to the banks?

To summarise to the plebs -

Your hardship wasn't so bad...

Ultimately commercial bank rates, bank profits and financial stability are outside our mandate or our area of expertise, even if that's what we breathe out at every opportunity...

We know what we're talking about and we have fancy calculations that prove us to be the supreme master...

Everyone back to work for your wealth illusion...

You can’t make a silk purse out of a sow’s ear

The Landlords are freaking out on the property (ponzi) pages........cannot get tenants.....

Then humanity is doomed and LLs money centered belief system (along with the local scrotes - TAs and ACs promises of eternal land hoarding riches) is in total tatters, as they are needing to drop rent by big amounts to even get the poor peasants in, to even look over their dingy, for hire digs.....

This market crash has merely had a breather, the next down leg has begun.

Our economy is royally roggered and the signs of life are faint. The worried Doc sighs, the life support, may not bring it back....

This market needs mortgage rates of 2.5% to just hold on to 2017/2018 pricing.

Soon 2015 prices will soon be the norm.......if that holds? - is anyone's guess!

An overshoot in rental supply. Just because you've converted homes into rental properties, doesn't mean the tenants are going to consign themselves to renting. It does not override the demand for owner occupied housing.

The RBNZ is simply saying the exact same thing that I said a few weeks back. It is fact that the banks are front running the OCR rate cuts, and this means that upcoming rate cuts wont be passed on to customers in full. This has always happened - I remember in Australia customers maybe got half to two thirds of the cut, the banks took the rest. All those n00bs who dont remember the last interest rate reduction cycle, who have been fixing short in the expectation that another full 100 bp cut will be wiped of their mortgage rate in a couple of months, are going to be bitterly disappointed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.