Okay, THIS one is BIG.

Look, you might think we always say that. But this one IS REALLY BIG.

Statistics NZ releases the Consumers Price Index (CPI) inflation figures for the June quarter on Wednesday, July 17.

Why is this one in particular so important?

Well, it was always going to be hugely important, but the Reserve Bank (RBNZ) has actually upped the ante with some very unexpectedly 'dovish' remarks in its Official Cash Rate (OCR) review on July 10.

Financial markets never need encouragement to get ahead of the game and following the RBNZ comments there's been some aggressive moves in wholesale interest rates. At time of writing - and please, bear in mind this is a very movable feast - the financial markets were pricing in about a two-thirds chance of an OCR cut as soon as next month. An OCR cut in October is now fully priced in, while TWO cuts are now priced in for November.

I'm inclined to think that's all a little exuberant. But no doubt the rate cut buzz will only get louder if the inflation results this coming Wednesday are the 'right' ones.

So, what do we need to see? And where are the potential pitfalls?

We need to see meaningful falls in the inflation rate so that the Reserve Bank (RBNZ) can be confident inflation is under control and therefore can contemplate lowering interest rates.

This was always going to be the key quarter even before the RBNZ raised the stakes with its comments in the past week. This is when, I would argue, we can find out definitively if the inflation battle really is being won or not and therefore whether the current expectation of imminent falling interest rates is justified.

This quarter will either be the proof in the RBNZ's pudding - or it will be the bad egg that ruins the pudding.

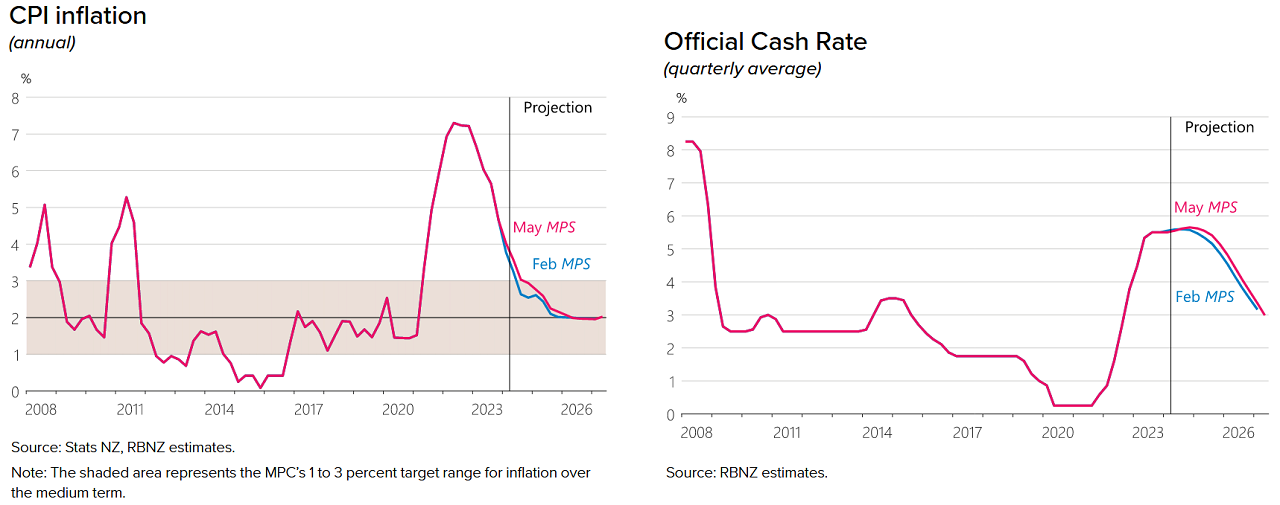

The RBNZ is charged with maintaining inflation between 1% and 3%, with an explicit target of 2%. All is well and good well if inflation behaves. But It has most certainly not behaved; having now been above 3% for three years. Three years. That is a long, long time.

Everything got out of hand very quickly. As of March 2021 annual inflation was 1.5%. Twelve months later it was 6.9%. Aaaaarrrrggggh, is I believe, the word. The peak of 7.3% was in June 2022. The trip back down from the peak has been nothing like as fast as the ascent was. In March 2023 annual inflation was still at a very elevated 6.7%.

Now we are seeing real progress though. As of March 2024 the annual inflation rate was down to 4.0%. It's been expected to fall further in the June quarter. How much further it HAS fallen will be the big drama in the coming week.

Annual inflation rate down to 3.6%? Lower?

The RBNZ is forecasting that the annual inflation rate will have come down to 3.6%. But that is a forecast made in May prior to its more dovish OCR comments in the past week. I didn't have all the major bank economists' forecasts in front of me at time of writing, but Westpac has 3.5% and both ANZ and ASB reckon just 3.3% - which is interestingly what the inflation rate was back in June 2021 when it first broke out of the 1% to 3% range.

So, okay. That's great. We've just about fixed this thing! Bring on the interest rate cuts! Well...as the RBNZ has been saying itself, until certainly the last week - not so fast.

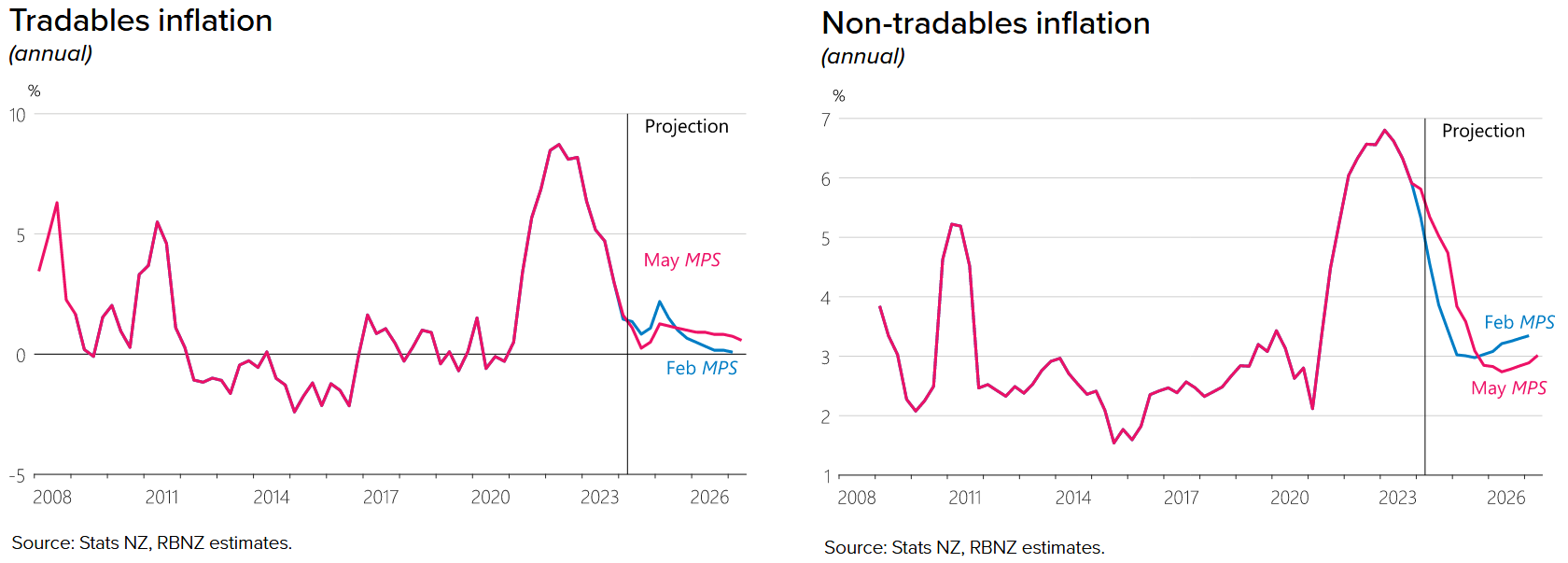

There's a few potential plot twists here. Inflation is measured in several ways. The point of saying that is: While the so-called 'headline' inflation figure might be looking good, there could be other inflation measures that are not.

Enter 'tradable' inflation and 'non-tradable' inflation. Very loosely the 'tradable' figure refers to 'imported' inflation - think things like petrol prices. 'Non-tradable' inflation is, again very loosely, domestically generated inflation - think things like new home building costs and rents.

In very simplistic terms our post-pandemic inflation battle has actually been conducted in two parts. First we had to fight through incendiary levels of 'tradable' inflation, which peaked at an eye-watering 8.7% annual rate in June 2022.

More recently as global supply chains have been painstakingly unbroken again and various other things have come back into equilibrium, the tradable inflation has retreated like a fast-running ebb tide. As of the March quarter the annual tradable inflation figure was down to 1.6%. The RBNZ's forecasting the figure will be just 1.1% for the June quarter and there's some thoughts from economists it might even be lower than that, with petrol prices having dropped meaningfully recently. (All the graphs here come from RBNZ's May MPS).

And non-tradable inflation? Ah, well, you spotted it. There's the problem. Part two of the inflation fight. Non-tradable inflation.

After the first wave of imported inflation hit us, local NZ prices were put up across the board in response. And this domestic inflation has proven 'sticky' as the economists like to describe it. Non-tradable annual inflation was 6.0% as of March 2022. By March 2023 it had actually risen to a new peak of 6.8% and it has fallen only very, very gradually subsequently.

The domestically generated inflation has been very much on the minds of the RBNZ folk. The RBNZ had forecast non-tradable annual inflation to be 5.3% as of the March 2024 quarter. But the actual figure when released surprised very unpleasantly on the upside. It was 5.8%, barely down from the 5.9% annual figure reported for the December quarter. All this meant that even though the so-called 'headline' figure had dropped nicely from 4.7% to 4.0%, the RBNZ, as Governor Adrian Orr expressed it to Parliament's Finance and Expenditure Committee, was "annoyed".

It means the RBNZ - notably until this week - has kept pushing back with 'hawkish' sentiments against those who would like to see interest rates coming down soon. In terms of inflation, the RBNZ can't do much about the imported stuff. It's the domestically generated inflation it takes aim at with higher interest rates in order to slow spending and take steam out of the economy.

As we know, the RBNZ's reaction to the inflation explosion was to rapidly hike the Official Cash Rate from just 0.25% at the start of October 2021 to 5.5% as of May 2023. At which point the RBNZ called a halt to proceedings.

Bring on the cuts!

According to its latest forecasts made in the May 2024 Monetary Policy Statement (MPS) (see page 50) the RBNZ hasn't seen the OCR being cut till the second half of 2025.

The financial markets have not agreed, even before the RBNZ's 'dovish' turn in the past week.

We don't get new forecasts from the RBNZ till its next OCR review on August 14 at which point a new MPS will be published. Given the RBNZ's comments in the past week, it is to be assumed it is certainly changing its mind about when the cuts will come - but in terms of what it actually decides, that will depend hugely on the inflation figures and to some extent also on the forthcoming labour market figures on August 7.

The public of course are more than just politely interested bystanders in all this. Many mortgage customers have been 'going short' with their fixed mortgage rates - as short as six months - in the belief that rates are coming down sooner rather than later. So, will rates come down soon?

What do we need to see from the inflation figures? Well, obviously they need to come down. As a corollary to that the inflation figures need to show that the RBNZ is on track with its forecast that inflation will be back under 3% by the end of this year. The May MPS forecast was for annual inflation to be 3.0% in the September quarter and then 2.9% in the December quarter. Interestingly in its OCR review in the past week the RBNZ talked about inflation getting back under 3% "in the second half" of the year - which suggests it's thinking this might now happen a bit earlier than it thought - probably in the third quarter. A number of economists think sub-3% WILL be achieved in the September quarter.

But where things might go wrong is if the 'headline' figure is good (and I think it will be), but the domestic, non-tradable figure is still super sticky (which it may or may not be, but my best guess, and to some extent hope, is that it might this time have 'unstuck' itself and dropped accommodatingly).

The RBNZ has previously been taking out its frustrations about the stubbornly high non-tradable inflation figures by pointing out some of the main 'culprits' - such as local authority rates, energy prices, rents and excise duties on cigarettes and tobacco. There's not a hell of a lot that the OCR can do to 'reach' those kinds of price rises.

By pointing these out as inflation miscreants, the RBNZ has almost been giving a little plea to the likes of councils to just ease up. (Before you jack your rates up, think of the country!)

The economy 'has let go'

Little wonder when you look at inflation culprits like those named above that some economists think the RBNZ should be looking past some of them and not worrying as much about the 'non-tradable' inflation figure as much as it has been.

For what it's worth, my feeling is that the economy has 'really let go' in about the last eight weeks or so. The RBNZ seems to be getting the message now too. I think, for sure, GDP will have contracted again in the June quarter after showing an anaemic 0.2% gain for the March quarter.

What that means is that inflation should be heading off a cliff about now. Prices can't be raised when people either can't or won't afford them. And that's where we are now, I think.

As mentioned earlier, the RBNZ's picking a 'headline' annual inflation figure of 3.6% in Wednesday's CPI results, with a 'tradable' figure of 1.1%. Then there's the non-tradable figure, which remember the RBNZ picked to be 5.3% in the March quarter and it was actually 5.8%. Well, the RBNZ's picking 5.3% again this time - so, if the figure comes in at that level or lower, it might just be about time to start heading for the fridge to get that bottle of champagne out. We. Will. Nearly. Be. There.

Fingers crossed for the CPI figures on Wednesday then. We need them to be down. And we need the RBNZ to be fully convinced that inflation is getting the elbow.

If the RBNZ can be suitably placated then there's really every reason we can have a nice OCR cut (or two!) before Christmas. The economy might need that even more than the RBNZ is beginning to realise.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

Consumer prices index

Select chart tabs

132 Comments

Can you imagine a Council thinking of mortgage rates when they up their rates bills?

Not a chance!

In Ak it was the (Len and John) train tunnel and interceptor which has done the damage. Cemented it in.... And of course AT and its largess etc etc.

We urgently need to have a law imposing a nation-wide limit on rates increases - no more than 1% over the inflation rate, say, maybe with also a provision for mandatory yearly auditing of all major councils by an independent authority with the power to investigate and highlight areas of waste and potential savings.

Regarding AT in particular, you could quite easily sack a third of its personnel while maintaining existing service levels.

Was in Taupo at the weekend. They have a 10 km (approx) highway where they are installing a central barrier.

To do this they had about 3 workers working and 7k of cones in 4 lanes along with 2 of those fancy cone laying trucks with another 4 staff driving down the road moving each cone about 5 cm wider than their previous placement.

Given the news one would think the contractors would be being frugal for a bit... but no.... rubbing it in the faces of the public who pay their bills.

In the uk I never saw a cone placing lorry and they have about 5 to 10 cones at small work sites.

I am all for safety.. but seriously.

How about we have a law imposed that councils need to maintain public infrastructure to sufficient levels and bill property owners who are the economic beneficiaries of that infrastructure through rates?

So you want people to pay by the benefit they derive from the council infrastructure rather than by the Property value? Would be popular with homeowners in Parnell and Herne Bay, but West and South Auckland homeowner might not appreciate their rates doubling or tripling. Ditto with rural Northland etc.

To restrain local and regional council over spending and improve efficiency Binding Citizen Initiated referenda is a method of control with power of recall as coucillors then have the incentive of being removed for avoidable mistakes and wasteful or poor value expenditure ratepayers do not approve of. Once shown to be sucessful the referenda can then be applied to central govt.

Any chance of an August rate cut? Then October and November? 0.75 this year.

Been picking August for over 6 months now. I think we will get 50 bps this year and more next, OCR down 100bps by the end of next year.

What happens if CPI falls below 2% (could happen once the 1.8% from last September falls out). Even a 1% OCR cut will make it well above neutral. The RBNZ may find themselves with the brakes still on, the country in a terrible recession, and CPI below their target, a triple fail.

Yes, a triple fail with zero clue how to get out of the rut. That's been my (doomladen) prediction for a while.

Outside of forward guidance, the RBNZ don't usually declare whatever reactionary tools they're going to deploy until they need to deploy them.

Even with the inflation target, we only get told a 1-3% range, and not a definite trigger of what inflation percentage needs to be hit, for how long, before they will adjust the OCR.

Need to know basis, and us punters don't need to know.

Lol, you really think RBNZ have any cards to play on economy rescue? What will they do, some press conferences to raise recovery expectations?!?

They have a history of deploying stimulatory vehicles to juice activity. QE, fiddling with deposit (and likely now DVI thresholds), FLP, that sort of thing.

So you think they'll never do anything like that again?

I think they probably will but those tools will make zero difference in the real economy. FLP and QE are just mechanisms to hold market interest rates down (and bond prices up).

Now if RBNZ made banks offer 0% loans for green tech and productivity investments, that might do something. But sadly I think we will just see RBNZ using low rates to encourage banks to pump credit money (poor quality stimulus) into the economy (while sending house prices up 10%)

So you don't think our economy (and many others) haven't been stimulated and propped up by these sorts of tools in the past?

Having targeted stimulus along the lines you've mentioned have issues because they don't impact the broad economy, and often don't result in the sorts of long term benefits people hope they will.

If we're talking about juicing "productivity", there's no assurance you're going to get a decent level of lasting benefit, because for the productivity to be genuine, invariably it needs to stand on its own two feet - the fact you need to subsidize it via fiscal subsidy make it a tenuous investment.

Likewise with green tech investment, the very nature of much of this isn't often of a net financial benefit, because a green alternative is often less economically efficient than an incumbent.

This isn't to say the previous fiscal stimulus has been wise either, but whichever way you slice it, they're all mechanisms to try and avoid the realities that our ability to grow our economy organically is fairly tapped out.

If we're talking about juicing "productivity", there's no assurance you're going to get a decent level of lasting benefit, because for the productivity to be genuine, invariably it needs to stand on its own two feet - the fact you need to subsidize it via fiscal subsidy make it a tenuous investment.

Likewise with green tech investment, the very nature of much of this isn't often of a net financial benefit, because a green alternative is often less economically efficient than an incumbent.

I agree here. "Green tech" is often an attractive buzzword that needs subsidies because it isn't really more resource-efficient so not really more "green" in general. Green tech is great and works in lots of places but pursuit of "green" is often chasing dragons.

What would work imo would be repairing infrastructure. Govt using fiscal policy to spend on things like repairing pipes nationwide, insulating houses, building public housing, stuff like that. Cause at least we know the demand for this stuff is real and there so would be overall a goodish use of the money.

These are also nice to haves though.

Ideally what we're ultimately wanting is net positive return, i.e. getting out more than what we put in. This has fallen out of vogue for quite some time now, across the width and breadth of most modern economies. Money being spent on tangential values (such as the green tech, as you've mentioned), hell, much current stock valuation doesn't even relate to a companies ability to generate net positive returns.

Much of this actual net growth historically has been achieved by application of new technology, population growth, and a relative development monopoly over much of the rest of the world (i.e. only a small handful of countries had the social, political and economic system development to catapult actual growth).

The best compromise situation for NZ would be some form of tech investment to augment our inherent natural advantages, and increased disencentive of consumerism. But it's very hard not to be cynical that our place in the sun from a prosperity perspective is setting (and much of the developed world).

Every country that has ever transformed has done so with a plan and targeted public investment of some kind. They have often used trade barriers and outright protectionism too.

We will not achieve the step change we need in how we live and work by wiggling interest rates around and using other impotent monetary policy tools.

Every country that has ever transformed has done so with a plan and targeted public investment of some kind.

I'm actually of the opinion that most of that was more lucked into than the result of any actual deployed plan. There is currently a fortune being spent by countries the world over in attempts to plan a more profitable future. Most of it will be wasted.

We will not achieve the step change we need in how we live and work by wiggling interest rates around and using other impotent monetary policy tools.

Agreed, but we probably differ in what that change to life and work looks like.

Indeed we will not ,and certainly not under the direction of the RBNZ..that is the role of the Government (which has the ability to direct the RBNZ) and to achieve such they first need to formulate a plan and create the policy to implement it....and then convince enough of the voting public that its both workable and desirable.

We havnt had a political party that has offered such for a very long time.

And the last ones we had that did, helped send us broke.

This is because actual innovation and net returns involves decent levels or risk and an ability to see what most can't. Which is the opposite of how most government operates, at best they are just applying vague formulaic mimicry, i.e. education and infrastructure development = economic improvement, so the more you spend, the better the returns. It only works so far then has diminishing returns to the point of malinvestment.

Even if we look at nations with more recent rises in fortune (so the likes of China, or Japan earlier), much of what they have achieved is through more rapid implementation of methods first deployed elsewhere over longer periods of time.

Who were the last ones that did?

So you are suggesting that it is preferable to leave the development and allocation of resources to the whims of those largely unknown and not necessarily part of the society that nominally possesses them (including their abilities) as opposed to agency?

With agency we at least stand or fall of our own volition.

Clear signs of severe economic stress is already baked in and the continuing increases in mortgages being refixed at much higher rates, increasing unemployment, insolvencies and reduction in sales etc is damaging the country and Orr either doesn't care or doesn't see, time for National to suggest Orr resigns.

I'm not so sure. I think with climate change, government debt, political instability, trade wars, China, etc the new OCR neutral could be about 4.5% for the medium term. Be glad.to be proved wrong.

If quarterly inflation is at 0.5%, we still need to wait another quarter before rbnz realize annual inflation will already be in it target?

Seems like 3 quarters of 0.5% ish should be enough to say that and waiting that extra quarter is just doing more damage....

In our little corner of Northland we’re told we getting a 16% rate hike, those bills are due this month. Whangarei council has flash shiny new offices to pay for, our roads are still shit. Our rubbish rates have also increased from 2.60 to 4 a bag. Yes we pay that on top of the rates.

Just got the house insurance bill, that’s gone up 10.2%. Last year it was 19.9%, year before 6.1%. Car has gone up 6% last month.

Sure Broccoli is 2 for $3.50 and carrots are $2/kg. But that part of our spending is many thousands below those Rates & Insurance bills. I guess they have a weighting in the inflation calculations?

I know, well I read here how y’all want rates to drop, but everyday prices where I live certainly haven’t dropped for us and I deplore the ignorant call to ‘look-through’ rates and insurance because we can’t really opt out of those as everyday punters.

I wouldnt recommend dumping the rubbish down a deserted road or off the side of a country stopping area. Thats what some low lifes do and if I let council know about it they kindly will come and clean up. The cleanup cost wont be cheap. To keep people compliant tip fees and rubbish collection fees should always be minimised

This is just how our money works. Always has and always will. Every time humans run the fiat experiment, it fails and collapses. We're just watching it play out again.

Every economy eventually fails, regardless of whether there's a fixed or inflationary currency. It gets inflated in a fiat monetary system, or consolidated in a fixed one (i.e. all the hard currency ends up in a small amount of hands).

I'm at the point where my rates and insurance is now so high that I am financially and in lifestyle quality, better off swapping my Christchurch home for a luxury apartment on the Gold Coast and paying body corporate fees. Or I could save 75% of what I am paying and buy a similar value standalone house on the GC. Its ridiculous how much we are being ripped off here, and nobody does anything about it (except those who get brassed off enough and decide to leave for Australia). We shouldnt have to leave the country to be financially better off - that applies to both wages, and the sums of money we are forced to pay in things like electricity, rates, and insurance.

It humours me that economists think the RBNZ should "look past" known future inflationary pressures in rates 10%+, insurance up 20% again on this years bill. I live in the real world where I am going to have to pay these costs, where do the economists see counter balancing reductions in domestic inflation coming from? or do they only see this as a RBNZ problem whose only tool is the OCR. It is interesting that only people with mortgages are considered, what about savers who need the extra interest income to help cover the ever rising costs.

It humours me everyone seems to think it’s only mortgage holders and savers…I’d love to know what amazingly robust bulletproof job you & a lot of your likeminded commenters have to think that crushing the economy is a good idea 🤦🏻♂️

More affordable lending is vital, good management of debt control is vital, used well we could keep the wheels turning without spiking house prices.

And those savers needing higher rates…I’m assuming you mean TD’s…explain to me how that’s a better use of money than “the ponzi”…a lot of you moan how the ponzi takes money that could be invested in more productive businesses yet no one cries foul when that some money is squirrelled away with a bank on a TD…who’ll use it to loan to the spruikers to spend on the ponzi anyway 🤷🏻♂️🤣

Uhmmm....Lending has been very affordable until 2021. And where was it used for.........to pump up the Ponzi! Your comment about TD's doesn't make sense at all.

You are 100% right Pete, up until 2021 it was very affordable…great observation. We are looking at the current affordability of lending & how it is impacting our economy 🤦🏻♂️

Businesses loan money, councils loan money, the cost of lending impacts deeper than mortgages vs savers…use tools like LVR’s/DTI’s to limit house price growth & then reduce lending costs to try & keep things moving forward.

Ah well, it does make sense….just maybe not to you, & that’s sweet as.

You can't just goose your wealth in the direction you want by manipulating the ocr.

Who is this "We" who are so desperate to want the interest rates down?

It's them who believes in an economy that runs on debt rather than ownership. Always a bad move.

Mortgage holders....heard of them?

That's precisely who the ocr raises target. And why it's vital to 1. Borrow well within your means, 2. Be sure to have a war chest of savings 3. Pick a career and job that are safe.

We have to get inflation under control. Then find ways to stimulate the economy without putting upward pressure on house prices. Else we will be back at square one.

"That's [mortgage holders] precisely who the ocr raises target."

Um. No it's not. Back to school for you.

The RBNZ was responsible for all of housing inflation and now expects the borrowers who could not expect a more than doubling in interest rates to pay for their mistake - there was a reason France used the guillotine with fervour!

At this point I'd say 'we' is anyone reliant on a functioning economy. You know, people with jobs they don't want to lose and businesses who need customers?

Does your 'functioning economy' work for savers and renters or just those with debt?

Have you been advocating for decades about how our housing and immigration policies of the last 20+ years were going to lower the standard of living for the existing citizenry?

What you're seeing is just a taste of what our 'consumer demand' growth policies will deliver at some point in the future. The only question is timing, why should we push it out onto the next generation when most of the benefits have been had by those present here and now?

Does your 'functioning economy' work for savers and renters or just those with debt?

It provides varying levels of compromise for everyone in the economy.

Without the debt based system, the lifestyles, incomes, and material goods enjoyed by many/most would not be possible. Lower consumption, and significantly higher unemployment (or just lower wages I guess).

So the choice (not that we're actually given one), is a debt based system and the complications within, or some sort of fixed money supply enforced and subsequent diminishment of the lifestyles we think we can afford.

It's all a balance between the two. It's impossible to keep borrowing and spending beyond our means.

Because we outdid ourselves in rates and borrowing last time there is more pain associated with resetting the economy in a sustainable way.

Everyone seems to be itching to get back to the good ol days of 2 to 3% interest rates and spending wildly..

it can't happen.

We have an infected wound that we are currently pouring alcohol on. Yourself and others are screaming to pickup the dirty bandaid and put it back on to save us all, yet we will only be in the same sitaution but with far more inequality, poverty and decline in living standards.

Are we going to clean out this wound and deal with some hardcore pain for short term, or just continue the drug of ever cheaper borrowing to offset the hangover?

You ever spare a thought for the next generation? I know the previous ones haven't but someone at some point has to.

What’s the solution for the next generation? Higher interest rates won’t make houses more affordable, DTIs might but by removing many FHBs from the market.

Supply and demand Jimbo. We have been making houses scarce by increasing population. Stop that and half the house price battle is won. Plenty of other things such as an LVT to stop people hording/land banking could be done too.

DTI's could be done (to a lower level) as could the poster on here Kate's rent regulation. The risk with those is that you end up with cheap housing BUT not enough available at the new low price point. Enter poster Dale's ideas on ensuring supply is available and let people build themselves. We've regulated our way into much of the housing affordability problems with our land usage, immigration and taxation rules. It would be easy to fix if we weren't worried about offending the current winners - I'm up for it.

NZ's exports have flatlined because of China's macroeconomic woes, so there won't be any extra export dollars driving economic recovery.

Successive OCR cuts could deliver a short-term sugar hit to our GDP 6-12 months from now but those spikes in consumer spending are likely to be short-lived in the absence of productivity growth.

Agree on both counts. Which is why I want NZ as a country to live within our means and stop growing population/debt for the sake of it. I fear the vast majority of the population is not actually productive in the sense of making NZ wealthier (I include myself in that group now I'm no longer exporting).

Living in your means are dirty words. We want the trappings of finery to make ourselves feel wealthy instead. Way faster.

Hence around half of Louis Vuittons income is from the lower and middle classes. If one looks rich, they must be.

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

{kind=link}

Central banking is a form of central planning. My base assumption is they will get it correct about as often as central planners got it correct. The downside is that the money supply and interest rates are so fundamental to all incentive structures in an economy the impact is inevitably massive and flows through onto both government and private sector decisions.

"Central banking is a form of central planning. My base assumption is they will get it correct about as often as central planners got it correct."

Bingo! Great comment.

Exactly. You'd think we were in the 80's again and paying north of 20% like my father was.

It's pathetic wanting all of the gains (land 'wealth') and none of the pain that our unproductive get rich scheme must necessarily deliver at some point to occur on our watch. "Please push it out another 10 years until I've retired/sold up, I just need a little more [time]...".

The economy could try serving everyone in society instead of just those who 'own' - I don't know any renters or those with cash in the bank complaining about current interest rates.

So much of what business owners are willing to grind through now depends on how their feel about their future prospects.

That's why so many restaurants are in the news as closing. It's not that things are bad, it's that with the RBNZ only looking backwards, things likely won't get any better.

If the only way to prop things up is to put your own home up as collateral then decisions get very hard.

depends on how their feel about their future prospects

Yes, if they can no longer sell residence for up to 50k a pop and get what is effectively a bonded 'slave' working for them, those prospects will certainly be looking less profitable. Changes to the Accredited Employer Work Visa | Immigration New Zealand

Let me share something about those business owners. From a RNZ article:

"Commissioner Peter Mersi said 90 percent of taxpayers had no tax debt but some people had difficulties meeting their tax payments."

"Individuals' income tax debt had increased from $1.1 billion in March 2023 to $1.6b this March. For non-individuals it lifted from $540 million to $773m over the same period.

GST tax debt increased from $1.9b to $2.6b." An total of almost $5billion currently.

Employees (PAYE) don't pay GST and their tax is automatically deducted. My estimate is that the 10% the commissioner referring to are business owners and that would be about a quarter of all SME's/Contractors. Pretty scary I think. Some rate relief will also help the taxman.

"Employees (PAYE) don't pay GST".

Of course they pay GST when purchasing goods or a service. We all do !!!

GST tax debt increased from $1.9b to $2.6b." An total of almost $5billion currently.

Since when were Employees/consumers in GST tax debt?

I dont think theres enough wage surplus and while many propose lower rates will drive growth Im not convinced relying on credit will solve anything . Tax cuts throwing an extra 20-40 a week just dont cut it in my book. Is the real reason we have low productivity in some sectors because the wages are not sufficient once rents/mortgages are paid? Its mighty fine for the FIRE industry to call for lower rates but that only looks after a portion of society. For example lower rates wont help renters or those with credit card debt or those that do their weekly shop with whatever residual earnings they have . No surprises then that retail is taking a hit and the idea that a lower OCR will turn it around for them seems somewhat whimsical. I suspect a hefty blow needs to come via wage rates and the fallout will be higher unemployment but the upside should logically be improved productivity as employers are forced to thin out those less productive. Better to have quality over quantity surely? I dont for a moment imagine anything will change as folk will run to regulators crying wolf and howl for lower rates knowing full well it is those low rates that drive nothing but a false economy which very rapidly creates distorted values and eventually causes even more inflation to bubble up. Im all for a 5% OCR default setting.... and working on other aspects of our economy to drive growth....my 10 cents

The inconvenient truth is that stressed mortgage holders could have, and still can, reduce their weekly payments just by fixing-long. The lending curve is negative, and has been for many years. All this, "we need a lower OCR to take the pressure off mortgage holders" is pandering to those who want one thing, and one thing only - their property prices to rise, so "Inflation will pay off my Debt". Some very misguided and prejudiced writing from supposed 'experts' in the economic industry misled ordinary New Zealanders to ignore that option. And that, my friends, is why we are in such a mess. Our economy can only run on speculation fuelled empty for so long (we buy more than we sell). Then we end up like Pakistan, for instance. " Pakistan reaches $7bn loan deal with IMF..... to secure debt-stricken country’s 24th funding programme."

Make no mistake about it, rising property prices is just as 'inflationary' as the rise in a price of a tomato - but far deadlier. Because it necessitates the true meaning of Inflation - an increase in the Money Supply; the amount of non-productive Debt required to pay the increased prices.

If mortgaged landlords do not get interest rate relief shortly, there is nothing surer that tenants are going to be facing rent hikes that they have never seen before.

I know many landlords who have one or two rentals that have put their rents up over the past year, they have told me that if interest rates do not come down shortly, then they will be raising their rents by at least another $100 per week at next review.

The cost of holding a rental now compared to its value and rent received does not make sense financially.

I also hear that the rental market is quiet. Good luck with those hikes!! Sounds to me like a bad investment, rather than a cost that can be currently passed on. Personally it's quite amusing to hear what you heard...

TJ- Im one of those mortgaged landlords that did that recently to my tenants. Ive benefitted immensley from stable tenants 5yr - 13yr tenures who genuinely treat the places as their own. All bloody amazing people. Previous rent reviews have been at rates slightly lower than market rates to reflect the benefit I get from having such reliable tenants. I was forced to put the rent up to market rates as interest and other costs have ballooned as we all know. Biggest single increase in my 24yrs as a landlord. Thankfully nobody has moved yet, but suspect many other tenants out there are quietly suffering the same fate. Still limited listings on trademe in my areas (AKL). So to your point, I know a few tenants out there that actually do care about interest rates now!

If you have had them so long then your equity must be quite high so your rent should be covering remaining interest and other costs comfortably.

Unless you have leveraged the equity based on the extra speculative gains that people have made.

So long as its market rent the tenant has no choice - they cant move because all the other rentals on the market cost the same. I suppose they can downgrade to a smaller property in a worse suburb, but most people don't want to do that because it involves moving their kids to worse schools.

The rental market in ChCh is very busy and plenty of applicants for anything.

It is just a matter of checking all tenants out that you put on the short list.

our rents have gone up between $50 and $150. This year and tenants know they have to pay or look elsewhere and that is not happening with us .

we are not buying to rent out at the moment as returns on the increased prices does not make it worth it.

I thought so. You are highly leveraged.

you are highly concerned about making others feel bad, useless comment.

No one does that better than him. Look at me. I have made millions. Why haven’t you. If we can in fact believe him.

Gordon?

Ex agent, you want us to believe that you have made millions, yet you openly admit that you lie about ever having been an agent...

Greed got the better of them. Interest rates were always going to go up. Do you expect us to feel sorry for such a foolish decision. Are you one of the concerned landlords?

“The cost of holding a rental now compared to its value and rent received does not make sense financially.”

Is the rent received too low or the value too high? I’d argue interest rates affect the value of the property, not the amount of rent that can be charged.

Genuinely two sided conversation above, brilliant

Austrian business cycle theory - Wikipedia

Read the "Mechanism" section of that wikipedia article and tell me it doesn't sound remarkably like the situation the world & NZ have been pursuing since the GFC. Global debt levels have just topped $300 trillion on a global GDP of around $100 trillion....This is highly unusual, even unprecedented, historically.

According to the theory a period of widespread and synchronized "malinvestment" is caused by mis-pricing of interest rates thereby causing a period of widespread and excessive business lending by banks, and this credit expansion is later followed by a sharp contraction and period of distressed asset sales (liquidation) which were purchased with overleveraged debt.

......

Austrian business cycle theory does not argue that fiscal restraint or "austerity" will necessarily increase economic growth or result in immediate recovery.[10] Rather, they argue that the alternatives (generally involving central government bailing out of banks and companies and individuals favoured by the government of the day) will make eventual recovery more difficult and unbalanced. All attempts by central governments to prop up asset prices, bail out insolvent banks, or "stimulate" the economy with deficit spending will only make the misallocations and malinvestments more acute and the economic distortions more pronounced, prolonging the depression and adjustment necessary to return to stable growth, especially if those stimulus measures substantially increase government debt and the long term debt load of the economy.

NZ should desperately be trying to position itself well for serious debt issues around the world and the economic impact of this. And to be clear this isn't the loony PDK "End is nigh on resource consumption" falsehood, it is a financial crisis caused by central planning. Because let's not forget that central banking is a form of central planning and central planning always blows up in the end. Especially if it is (attempted) central planning of something as important as the money supply.

EDIT: Few interesting and relevant charts.

US interest payments on Federal debt: Federal government current expenditures: Interest payments (A091RC1Q027SBEA) | FRED | St. Louis Fed (stlouisfed.org)

US deficits at govt level as % of GDP: Federal Surplus or Deficit [-] as Percent of Gross Domestic Product (FYFSGDA188S) | FRED | St. Louis Fed (stlouisfed.org)

US govt debt level as % of GDP: Federal Debt: Total Public Debt as Percent of Gross Domestic Product (GFDEGDQ188S) | FRED | St. Louis Fed (stlouisfed.org)

US private debt to GDP %: United States Private Debt to GDP (tradingeconomics.com)

Expect rate cuts and expect resurgent inflation would be my view on the next 10 or so years. You can look up similar charts for all the G7 and other major economies and the exact split might be different but the level of debt is historically unprecedented in peacetime (to put it lightly). And the other side of the balance sheet (e.g. offsetting assets) are valued at amounts that can only be sustained by keeping these debt levels steady. Which will mean adding more to the debt.

Maybe a currency crisis won't happen but imho you'd have to be nuts to not prepare yourself for that very real possibility.

How is debt 300% of GDP?!? I think you are adding govt and private debt together - you can't, they are opposite sides of the balance sheet. The world's net debt is precisely zero (unless we have been borrowing from aliens).

How is debt 300% of GDP?!?

Leverage.

I'm more interested in what's going on with unemployment than inflation. That's the number more likely to catch a few pundits out.

Exactly. Something snapped a few months ago. Treasury and MSD forecasts are normally pretty good, but the beneficiary numbers are leaving the forecasts for dust now. There are plenty of countries who have kept unemployment low and exited their inflationary episode without throwing people on the dole. NZ is about average as of March 2024, but we've still got our fiscal and monetary settings firmly fixed on growing the dole queue and the next two unempoyment figures could be very, very grim indeed.

"Something snapped a few months ago."

Could it be that many decision makers took the RBNZ at their word and believed them when they said there would not be any reduction in the OCR until late next year?

Any decision maker carrying idle labour would dump them real fast rather than having to carry them for another year.

They didnt have Jacinda Ardern destroying the country for 4 years. Except Victoria in Australia, who had Dan Andrews in charge. And if you dont think that Govt Covid decisions made a difference, you only have to compare the economic performance of Victoria compared to Queensland, Western Australia, or NSW. NZ is in exactly the same boat as VIC.

Interest rates are the same for all Australian States, but only one is in trouble. Cant blame interest rates for that.

The resident garden variety Spruikers/Rentiers/Debt Junkies, don't care one bit about the major economic imbalances in the NZ economy.

The just want a new set of more "Usefull Idiouts" to load up on still more DDDEBT, onto their shoulders, so they can unload on them, the piles of unimproved dirt and shacks they have accumulated.

"One last rerun of the 2020-2023 madness please", they beg, "we just need one more massive extract from the NZ populous".

The max it can ever go now is 6 times income dti

"The new DTI settings allow banks to make:

- 20% of new owner-occupier lending to borrowers with a DTI ratio over 6; and

- 20% of new investor lending to borrowers with a DTI ratio over 7."

https://www.rbnz.govt.nz/hub/news/2024/05/reserve-bank-activates-debt-t….

Even a 6xDTI is far too high a Debt loading imho.

Then 1 in 5 Borrowers can potentially be loaded up at 7, 8, 9, 10xDTI.

When this NZ Property Crash has finished its falls sometime in 2026/2027, the RBNZ should lock in a DTI range 3.5 to 4.5xDTI as the Irish did, after their massive post GFC, 60% property crash.

The falls are already over, this is it. All the RBNZ needs to do is take 1% off rates and the housing market will turn. The whole of NZ runs on the state of the housing market, with prices going up people spend more money as they feel good. Watch for a lift in the market before Christmas.

"The falls are already over, this is it."

Please explain your rationale for this false statement.

The whole economy is based on peoples state of mind, just drop the OCR its that simple, people will begin spending money again. Lets come back in August, if the rate drops 25bps you have your answer, it could even be a shock drop of 50bps by then.

"The whole economy is based on people's state of mind"

Actually, it's not. It's based on people's Capacity to Pay/(Spend), not their Desire to Pay (State of Mind). And in most cases, that = the capacity to borrow, and the Cost of Borrowing (related to the OCR) is just one of several components to Lending. You could lower the OCR to 0%, but if the banks aren't lending, no transactions are going to take place. (The most obvious change that's possible is a change to the RBNZ Lending Ratios, making residential property Debt just too prohibitive for them to lend any further on their current balance sheets.)

Our economy shouldn't be based on "How much more Non-Productive Debt can we issue!", but it has been for decades. And at some stage, that ends. Either we do it, or our creditors; those who lend to us and trade with us, will.

If the banks lower the OCR to 0% you will see the biggest spike in property prices ever so that's not going to happen. The OCR needs to drop to like 4.5% and hold. Long term average mortgage rates are in the 6's so that's "Normal" going forward.

100% agree

Actually it is, sentiment and expectation underpin spending, they underpin virtually everything in economics. Fiat currency is also based on people’s trust on it. State of mind is everything.

It’s unbelievable how stupid your comment is.

Everything looks forward. Why do you think swap rates tanked and Wpac dropped their short term rates, our FX dropped after a few dovish words from Orr.

Nothing in your absolutist world changed.

A truly pathetic response. Your false claim is unraveling the more you talk.

You were talking past tense (the falls are already over), but are now talking in future tense (August). And you haven’t provided any factual evidence, just more biased speculation as expected.

If we look at the evidence, we can see that mortgage rates have already dropped 25bps. And while mortgage rates have dropped, house prices have dropped further and faster. They’ve done the opposite of what you expect with a 25bps rate cut.

Surely you can both see each others perspective, chalkboard rates dropping won’t have the same effect as an OCR cut, the OCR cut will bring confidence to potential borrowers that the rate has passed its peak. That said the lag effect will play a part & any cut would take 6-12 months to play out so prices to continue falling over that period maybe?

We’re debating the fallacy that “the falls are already over” and the housing market will turn at the first rate cut.

Like me, you’re in agreement that interest rates will have a lag effect (maybe 6-12 months) and during this period house prices could very likely keep falling - the opposite of what Zwifter claims to believe.

Most here are aware of the lag effect, however speculators commonly refuse to address this elephant in the room.

I never claimed sentiment won’t change after a first 25bps rate cut. I’m simply warning that house prices may keep trending down while rates get cut and the lag effect plays out.

It sounds overly optimistic that cutting rates alone will bring our economy back on track recovery. Our economy is a hundred thousand-plus young skilled Kiwis lighter since 2022.

Wouldn’t that lead to no houses being built?

Is townhouse building still going gangbusters near where you live?

There are still some being started surprisingly. They seem to be getting better sections these days, so probably lower build costs a bit to make up for lower asking price.

Yes it’s not totally dead. Though I struggle to see how developers can make things work right now. Some might start to take the punt on interest rates being much lower in late 2025 as they near completion. Aiding sales nearing completion. But that only works if you can work off no pre-sales.

are they KO or private?

In my town they are almost all KO!

I would caution the comments about supply chains being fixed. There is increasing shortages of equipment (containers) in Europe due to lack of capacity to reposition from Asia due with the Red Sea issues. Additionally with USA tariffs coming in there is a large rush of products heading there soaking up capacity. We are seeing 4-5 week delays in transshipments through Singapore. As such rates are on the way up.

Remember you have quarterly figure of:

1.1, 1.8, 0.5, 0.6

If you get a read akin to the last two quarters again you'll probably have a better argument for rate cuts in after the December quarter figures have been announced. If you get a lower read though you'll have a better chance of bringing that forward.

The RBNZ are getting paid to be able to see what's happening in the market in 6 months time, not just waiting for the figures to come out for the last quarter, any idiot can be reactive. They need to start cutting rates right now.

Genuine question: What will you do if the OCR is cut?

(From yours, above: "drop the OCR its that simple, people will begin spending money again.". And if you were, say, a tomato grower and you thought spending was going to come back again, what would you do to the price of your produce? I'll tell you - put it up. And that's what will happens to everything if the OCR is dropped - prices will rise and then the RBNZ will have to do what? Yep. Chase a higher CPI with ...ta-da, even higher interest rates)

Adding to that, if we drop before the Fed, our exchange rate will drop, importing more inflation, the RB can't risk that. In my opinion we won't drop before the Fed.

Agreed. The rock and a hard place.

Speculators bleeding equity as negative leverage cuts deep, smoking opium won't stop the blood loss.

RBNZ are in the sweet spot. Quarterly figure of 0.5 to 0.7% get them to exactly where they need to be in when the December quarter numbers are announced. This is as close to a smooth landing as it gets.

If those figured dipped substantially in this next reading they might trim rates but why start cutting when they are on target?

100% agree, finally someone realistic.

according to my employer, who owns a manufacturing plant, he think businesses with cash are planning to invest in capital as soon as there is a hint of recovery (or lower rates), we have been limited spending as much as possible currently, i assume this will change in the next year.

I agree.

But you are deluded if you think doing so will result in an uplift in property prices in 2024. At most, it would halt the decline

Yes and if the new land supply polices are allowed to work, even as demand increases, supply will be able to keep pace and thus prices will be far less likely to increase because of any speculative pressures.

not 2024, slow increase in 2025 maybe.

Slow increase from spring 2025

In real or nominal terms?

Is it really clear what the RBNZ are paid for?

"Purposes

The purposes of this Act are to—

(a)

provide for the continuation of the Reserve Bank of New Zealand; and

(b)

promote the prosperity and well-being of New Zealanders and contribute to a sustainable and productive economy."

https://www.legislation.govt.nz/act/public/2021/0031/latest/LMS286982.h…

I thought the order was interesting.

The order is important for when (a) and (b) are mutually exclusive!

On current trend, if they don't do anything and inflation persists at the current rate, they'll probably be at about 2.3%.

i.e. Exactly where they need to be, the mid-point of their target.

if the CPI is below 0.5% this announcement i think they should

A lot of boomer and dgm nonsense in the comment section to this particular article. Sadly, many are seemingly hoping for the continued deterioration of the economy for self-serving reasons and therefore the ongoing suffering felt by many and particularly the younger generations.

You ask why do we want rates to fall? Well the answer is obvious- inflation is beaten, and for the sake of society and the well being of everyday people and families, rates need to come down.

I totally agree Piggy. Many New Zealanders are struggling financially. We need lower interest rates in order for them to be able to just pay for the basics such as food and power.

While we may want to lower the cost of living, it’s then a fine line to transferring asset wealth and starting asset inflation again which causes far more people to suffer for a very long time... this is actually what you are seeing now as rates are not high. Rates are correctly still on the lower side of the bell curve.

A third rent so no help to them and another third are mortgage free, again no help.

You want to take away from the savers and give to the borrowers.

I dont care about interest rates. I want prices to be lower. I would choose lower inflation over lower interest rates.

I'm due to re-fix mid August. What should I do?

Go 6 month fixed.

But this one IS REALLY BIG

that's what she said

Here is an admittedly very small inflation fact.

Product X I need to buy cost $55 last year now cost $73.

That is a 33% inflation in a year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.