As we approach a year since the Reserve Bank (it was May 24, 2023), somewhat surprisingly, called a halt to its extremely bracing cycle of Official Cash Rate hikes, we can say with every confidence that the forthcoming OCR decision will be another 'hold'.

There's been nothing since the last review in April to change the RBNZ's mind on keeping the OCR unchanged.

But while it is the safest of safe bets that the OCR will remain on 5.5% after the latest review on Wednesday, May 22, there will be much interest and intrigue around what the central bank has to say in its new Monetary Policy Statement (MPS), the first one since February.

The forecasts in it will be crucial.

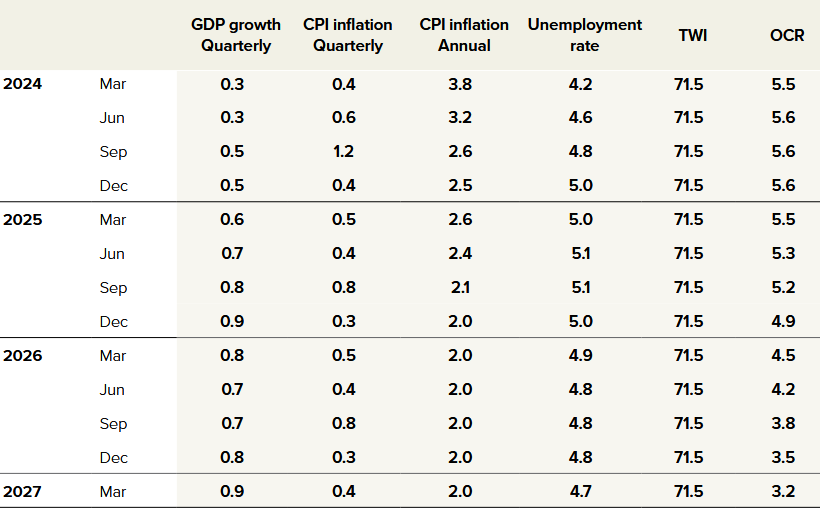

Here is an abridged version of the key forecasts from the RBNZ's February MPS:

The most anticipated figures in the new May MPS will be the OCR forecasts. There will be much interest as to whether or not the RBNZ signals through its new forecasts that it now expects the OCR to be cut for the first time earlier. Interest will also centre on whether it chooses to remove the possibility of of another hike before we get to the cuts.

As per its February forecasts the RBNZ was implying that the first cut to the OCR was likely to happen in the second quarter of next year. But it was also still forecasting about a 40% chance of another RISE of the OCR by the September quarter of this year.

I think the RBNZ could be justified in both removing the implied suggestion of a potential further rate hike and bringing forward the forecast time of the first OCR cut.

But I don't think it will, because that would not be the sort of signal it wants the financial markets to be given.

The markets like to run ahead of themselves - and of the RBNZ. At time of writing wholesale interest rates are pricing in NO chance of another OCR hike, but a very high probability of the first cut by October this year, with a pretty fair chance of TWO cuts by November 2024.

If the RBNZ does either or both of removing the chance of an OCR hike from its forecasts and bringing forward the time of the first forecast cut, the financial markets will run with that and will be quickly pricing in an even earlier start to the cuts. That would be very significant because it could lead to meaningful cuts ahead of time in mortgage rates.

So, the signal from the RBNZ's going to be important. Of course the RBNZ and Governor Adrian Orr are very well aware of how the the markets think and are not averse to wrong footing said markets with pronouncements and forecasts that 'the market' might not have expected. For example, the February media statements and press conference that accompanied the release of the February MPS were far more 'dovish' in their messaging than financial market participants had expected.

The RBNZ folk won't want to see mortgage rates falling significantly from current levels till they are very confident inflation is under control.

So, what of inflation?

Well, if the OCR forecast is the first thing economists and the like will look at in the new MPS, the RBNZ's latest inflation forecast will be a close second.

Importantly, people will want to see if there's any 'slippage' around when the RBNZ thinks inflation - as measured by the Consumers Price Index (CPI) - returns to inside the 1% to 3% targeted range. It's been outside of that target range for nearly three years now.

The past week saw some good news and some slightly less good news for the RBNZ on the inflation front. On the not-so good news front, Statistics NZ's latest new monthly Selected Price Indexes data, which covers about 45% of the things in the quarterly CPI, again pointed to some 'sticky' inflationary pressure - particularly in respect to things such as rents.

But against that, the RBNZ's own Survey of Expectations mostly showed another solid fall in the expectations of future inflation, with all timeframes (one-year, two-year, five-year and 10-year) being under 3% for the first time since the September 2021 survey.

In the February MPS the RBNZ was forecasting that the annual rate of inflation would return to under 3% in the September quarter of this year. It's very unlikely the RBNZ would change that forecast timeframe. It would be a bad look.

But there's no doubt there will be some fingers crossed as the latest forecasts are signed off - assuming that September quarter date for inflation going under 3% is retained.

In terms of the actual inflation figures to date, March quarter CPI rose by 0.6%, which was higher than the RBNZ's 0.4% pick. Annual CPI rose 4.0% (down from 4.7% as of the December quarter) against an RBNZ forecast of 3.8%.

The big 'miss' for the RBNZ forecasting was in domestic (non-tradable) inflation, which was much stronger than the RBNZ was picking. The RBNZ forecast quarterly non-tradable inflation of 1.1%, but it actually came in at 1.6%, while in terms of annual figures, the RBNZ had picked 5.3% but it came in at 5.8%.

Overseas-sourced, or tradable inflation, was -0.8% for the quarter (versus an RBNZ pick of -0.7%) while the annual rate was 1.5% versus the RBNZ's 1.6% pick.

The RBNZ won't want to be depending on continued low inflation or even deflation from offshore, so, it will want to see domestic inflation beginning to drop more quickly.

Other key economic data, however, are perhaps suggesting that more downward pressure is going to start coming for domestic inflation. December quarter GDP showed a 0.1% contraction, while the RBNZ had expected a flat (0.0%) result. Unemployment rose from 4.0% to 4.3% in the March quarter (the RBNZ had picked a rise to just 4.2%).

A contracting economy and a now quite quickly softening labour market would together suggest downward pressure on inflation through fewer wage rises and reduced spending. The soft GDP and labour market figures would therefore probably allow the RBNZ to be 'patient' with inflation for now.

The upshot is, I would be surprised if the RBNZ does change that forecast of inflation going under 3% by the third quarter of the year.

Likewise, I would be fairly surprised if the RBNZ makes much, if any change to its OCR forecasts. It won't want to give the financial markets the opportunity to start pushing down those wholesale rates and thereby, by implication, opening the door for large mortgage rate cuts.

As others have said, the RBNZ won't want to say it's cutting the OCR virtually until the time it does it.

So, for now it's likely we will get a largely unchanged message. But really, you can never exactly tell with the RBNZ. Anybody looking for clear signs of some significant mortgage rate relief coming before the end of the year is, however, likely to be disappointed.

Just as a final thought, however, I've seen some comments asking whether there is any chance of a cut by the RBNZ now? I say no. But the economic news is certainly worth keeping an eye on. There are definitely signs the economy is really starting to roll over. The RBNZ wants to slow the economy. Not break it.

The RBNZ's overwhelming priority is to smash inflation, and to some extent to hell with the consequences for the economy. But yes, I think there is some possibility if the economic news keeps getting darker and darker the RBNZ may yet have to compromise a little on its inflation target. Maybe. But we are not at such a point yet. Watch this space.

I'll finish with a quote from ANZ chief economist Sharon Zollner:

...We don’t see OCR cuts until the RBNZ has more confidence that the downward path for inflation won’t peter out before reaching the desired destination: not only back in the [1% to 3%] band, but also likelier than not to stay there. The timing and specifics of such a ‘confidence’ pivot are very difficult to pinpoint, as it will depend not only a bunch of inflation indicators, but also whether the economy is still going south or recovering. A range of combinations of data could meet the requirements. But the general theme is that the weaker the real economy is looking, the fewer inflation runs on the board the RBNZ is likely to require in order to feel confident about cutting the OCR."

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

106 Comments

Anyone else thinks that RBNZ should do the first 0.25 cut next week?

Nope. Hold and let the economy rebalance back to normal cost of debt. Yes that mean house prices continue fall, but that is the component that is out of balance.

It will also mean a lot people will lose their jobs and businesses will go bust. It's not just about houses Averageman.

Terrible allright. Imagine if the spec crowd had not blown up the largest bubble since tulips and that money had gone into productive businesses. Those people caught now using their house as an atm or caught as last bag holders would have far less debt and mostly be fine.

Thats the real problem.

'Imagine if the spec crowd had not blown up the largest bubble since tulips"

The bigger the party, the bigger the hangover.

House values reached $1.76 TRILLION in NZ at their peak. Remember, residential real estate is the largest asset class in NZ.

Look at other economies which had housing bubbles and the consequences on the economy afterwards - lost jobs, business closures, recession.

Some housing bubbles in history:

1) US 2006

2) Japan 1990's

3) UK 1990's

4) Ireland 2006

5) Spain 2006

6) Hong Kong 1998

7) Singapore 1998

What productive businesses. 95 percent are out of business in 5 years with most failing inside 12 months.

Would you say motels are productive businesses putting rough people in a room at high prices. Would you congratulate someone who went and bought or built a motel to cream it off the govt MSD. Creates some low pay housekeeper jobs who get govt top-ups for Fam support and Accom supp as well

Would suggest most recent motel owner were in it for the land. As in tax free speculation. Look at the covid motels just south of newmarket. The msd ripoff is just pre redevelopment cashflow.

Did you ever see smales farm before the buildings

Yes. Worked on the first development there and met the Smales family. Can say multi generational cows and quarrys have nothing do with recent motel acquisition and msd revenue abuse.

Things that create new goods or provide valuable services. No, landlordship is not a valuable service, it is just the more advanced form of ticket scalpling but instead of an upset tween not being able to go see Taylor Swift it's young families left with no housing stability.

SKF

The RBNZ unemployment track show a peak of 5.1%, they fully expect people to lose jobs ...

I think it may well peak higher BUT maybe some will go to Aussie if its holding together better....

Good work ITGUY creating negative vibes, rbnz is taking note

Didnt you know that when interest rates start dropping, its then the end of the beginning of the Crash. The asset investors will flee the market, asset prices will tumble. Is that correct?

My business, we were 15% down yoy to the end of March 24, currently 8% up on last year and 1 new staff member. Admittedly it's only 7 weeks in to the fy, hardly anything to get excited about. Import wholesale distribution business. Stacked away a fair war chest in case of trouble.

There’s always winners and losers.

Even if unemployment reaches 6%, 94% of those who want a job have one.

A lot of people may need to reskill - there is a shift in what skills are needed going forward. An opportunity for those that dont have the right skills - to make themselves more employable in the future.

I do a lot in the software space - and need to continually evolve. AI is shifting the game and so about 20% of working time is now spent learning new skills to stay relevant in a few years. I am not sure standing still is feasible for anyone in their career anymore.

"I am not sure standing still is feasible for anyone in their career anymore."

Anymore? Never has been. (Makes me wonder how old you actually are and what jobs you've worked in...)

For me - 50's. Always in software/tech in a variety of roles. and everything shifts all the time.

BUT - I am never short of work as I make sure to always be expanding skill sets and adding new ones.

If someone is made redundant and cant find work - the solution is always to look at themselves and their skill sets, and then to make sure next time they are always learning something to add more value.

NZs debt clock clicks over $90,000 / household tonight

Thanks Labour.

Yeah, so glad National are paying back the debt and not just borrowing for tax cuts for the lords of the land. Oh wait.

Or we could put mechanisms in place so that dropping the OCR doesn't immediately pump house prices back up? DTIs, restrictions to credit, tax dis/incentives?

CGT for all sales would be logical - NZ seems to resist what the rest of the world sorted years ago... to its detriment

"CGT for all sales would be logical"

That would incentivise existing owners to hold on so less inclined to sell - fewer houses for sale in existing house market. Look at pending change of brightline test - many are holding on until zero tax on capital gains. A CGT wouldn't necessarily reduce buying competition from non owner occupier buyers.

Singapore has a stamp duty system which prioritises citizen owner occupier buyers at the top. Whilst other buyers have increased rates of stamp duty (permanent residents, non owner occupier buyers).

Foreign buyers currently have a stamp duty of 60%.

Entities buying residential real estate have a stamp duty of 65% - that would catch most professional property owners renting in the long term rental market, syndicate buyers and trusts.

With those rates of stamp duty, that would be unattractive for many non owner occupier buyers leading to reduced buying competition for owner occupier buyers. Remember how many non owner occupier buyers were effectively borrowing 100% of the purchase price through equity recycling techniques and outbidding owner occupier buyers?

This would make any new purchases for non owner occupiers potentially uneconomic (especially for those focusing on capital gains), thereby reducing buying competition for owner occupier buyers in the existing house market. It would be less financially attractive to use residential real estate as an object of speculation for non owner occupier buyers.

https://www.iras.gov.sg/taxes/stamp-duty/for-property/buying-or-acquiri…-(absd)

Don't know if there would be sufficient income for government tax revenue compared to a CGT, which might be more of a constraint in the government's policy making criteria.

I would like to see August but it will probably be November at the earliest.

Its going to be August, the cut will be 25bps. New Zealand has a very low pain threshold.

You are confident on this call.

He's got no idea. And like most, is just echoing what the loudest voices (bank economists!) are saying.

If it's meant to be a joke then it's worthy of an answer

"Anyone else thinks that RBNZ should do the first 0.25 cut next week?"

I do.

But it should now be the second (or even the third) cut of the same size beginning back in November 2023.

Agree

But they won’t.

I think first cut will probably be November. The economy will be a mess by then.

So you don't think it's a mess already? How odd ;-)

I also agree they should cut now. Inflation is in the pipeline, and the economy is a mess on the ground. As usual, the RBNZ will be too slow to react and then a knee jerk reaction will follow later in the year.

Yes, the last quarter saw 0.5% inflation. Annualized, that's 2%. I know it is a little bit more complicated than that but the OCR can start to be slowly wound down.

They should have started easing Nov '23. Why? Because the oil shock had passed (less core inflationary pressure) and a cut in Nov '23 would have had six months with less inflationary pressures due to wages catchup to pay for mortgages and businesses needing to pass on the costs of more interest on their working capital. I could go on. But our RB just looks more and more foolish if I do.

"But the general theme is that the weaker the real economy is looking, the fewer inflation runs on the board the RBNZ is likely to require in order to feel confident about cutting the OCR."

Let's hope the RB adheres to this logic. Major consequences if they don't.

This has only held true because NZ use to follow the USA into recession.When the USA went into recession commodities prices collapsed. Commodity prices collapsing caused a fall in inflation. Think 2008 and 1997 Asian financial crisis. However the game has changed NZ no longer follows the USA economy. It is effected by a myriad of factors. So it is plausible our economy can go into recession and inflation and commodity prices will both stay high.

"Let's hope the RB adheres to this logic. Major consequences if they don't."

And what about the major consequences we're already experiencing? Isn't a Recession and over 2 years of very sub-par growth, plus contracting businesses with negative outlooks, enough?

I don't buy an inflation narrative that has the annual inflation returning to under the 2% mid-point this year and that's when I think RBNZ might ease the OCR.

Base effects my friends, last quarter of this year they start to work against you. That's when the conversations about how tough "last mile inflation" is begin.

I doubt they will drop the OCR until they have a sub 3% CPI print.

They don't seem to understand that the OCR now - relative to the inflation rate - is now way, way higher than when it was first set at 5.5% over a year ago. Think about it. You'll get what I mean.

Will be surprised if there is a change in tone yet, maybe from August, we'll get a sense of direction

As ANZ say he will Deny, deny, deny... CUT!

I think cuts August or November if things go the way I think they might... if things are as rosy as some on here think, then no cuts at all are needed... many here think a single cut will set the house market off again... If the RBNZ thinks this way they simply will not cut. Following this logic you Spruikers should keep those opinions to yourselves, least you get a wider following and the RBNZ form your view as well.....

So I would be looking at the economy more then the RBNZ forward track etc. RBNZ forward track GDP look very optimistic to me, not sure how they see twi staying stable, we will see.

Whats the progress on the build, hopefully not working sunday

I am putting gutters on horse stables, will have most of it done today, water tank is in already.

The horse market is interesting, ponies for younger riders are moving but slowly. Good dressage horses are selling really fast, sometimes the day or one or two days after listing (25k upwards horses) . These appeal to older ladies not wanting to jump. Time waits for no lady it seems.... As you know, these boomers have often done very very well from property and have cash rather then debt, with term rates where they are its good times for them. Bottles of Otago red and pizza from the pizza oven....

This general population is 4 parts

- Older some wealthy, some not

- Struggling middle

- Disillusioned young

- Recent Migrants

The boomers may have to gift there wealth to their children, as the children and others do not have the ability to buy it off them. the children are heading off overseas, increasingly so are young families, being replaced by immigrants.

Interesting times with so many immigrants, so many kiwis leaving, the ethnicity makeup is changing rapidly (most rapid changes in the OECD believe).

What bottle of red will you be opening tonight?

Doesn't answer my question.

To answer your question about spruikers staying quiet, I think its more about the responses from suppliers about where they see inflation heading in the short/medium term that rbnz takes note of

TA seems to have gotten the message....

Bottle of Toi Toi Sav tonight it goes better with the Thai than a red.

Surprised David didn't mention the 'elephant in the room' that will be making an appearance on May 30th.

30 May Greenhouse gas emissions (industry and household): Year ended 2022

This release?

You're funny.

I was telling my mate last week I have some elephant droppings for him to shift... he hasnt done it yet so maybe he is waiting for the elephant to come back first

You're funny too.

I'm surprised nobody made a sensible comment about the Budget on May 30th.

I think the promise of tax cuts will influence the RBNZ's decision significantly (or at least they'll say so) and will ensure the OCR isn't cut for some time as the RBNZ will want to reassure themselves the tax cuts aren't 'inflationary'.

(They won't be. But the RBNZ hasn't worked this out yet.)

Does it appear odd to anyone else that we supposedly live in a democracy, where the government is supposedly accountable to its citizens, but for some reason we have an unelected body accountable to almost no one but an artificial statistic that that body made up for itself?

And someone, we?, they?, granted that body the right to destroy lives, wealth; waste years of people's live; enrich the wealthier; take from the younger trying to establish themselves in the world; and we accept this as normal? The way it must be?

Are we just slaves to be toyed with by this mysterious body? Are we in fact following a religion? It's not much different. The religious try to define their gods, but they never can because their gods 'act in mysterious ways', and are capricious and unpredictable.

Reading David, Liam's, etc. thoughts above and other media on this subject I am reminded of what I've heard from too many preachers who try to help you understand their gods. They never question if the god should should exist, only that it does, and we must all seek to understand them while remaining completely servile to them.

So now we await the words from the High Priests.

No one knows what they will say.

Nor who will be sacrificed.

But we must accept their edicts.

We have no other choice.

There is a reason they are independent.

Should Lucky Luxon appoint himself head of rbnz, then juice the economy to ramp it to new heights. Poll approval ratings willl shoot up like 1987.

I hear that Trump has said he would appoint himself that role over the fed reserve. IF it happens, the US economy will be the turkey by next thanksgiving.

Some obvious observations to that response:

1. Why does the RBNZ have so few tools to work with?

2. Why do they persist with obviously unjust tools?

3. To whom are they accountable?

4. Who else should be working with the RBNZ so far fewer suffer? Why aren't they?

5. When people a few generations hence look back, will they ask: "What problem were they really trying to solve? Weren't the rich, rich enough already?"

How do high rates increase inequality? To my mind low rates do that far more than high.

https://www.imperial.ac.uk/business-school/ib-knowledge/finance/how-cen…

I have an issue with average people investing instead of saving. Doing so drives up stock prices, and benefits those with the majority share, like Bezos or Gates or Musk etc. So yes they invest the money, because it's earning so little in interest rates in the bank.

I get the feeling most don't have an issue with Bezos earning $2B per quarter, as long as they get their $15,000 .

Obviously this RB management is now very questionable and one can see an addition to the unemployable ranks in the coming months,if not Mr.Luxon,you're not likely to see a second term,treaty in tact or not.

The recession has already got away from RBNZ and Govt - like it has every single bloody time we have had an imported price shock - 1970s, 1991, 2000 (wobble), 2008, 2021. The pattern is depressingly familiar. The price of a key import like oil spikes upwards, that drives price increases throughout other imports and our economy more widely, RBNZ respond heroically to desperately lagging indicators (rent, wages, etc) and our economy leaps happily off the cliff cheered on by reckonomics ghouls with very little understanding of what is actually going on.

Pull lever this way, ugh, tame inflation, yeh, yeh, pull it dis way, boost economeeee. Idiots.

Just when we needed them to be focused on fighting inflation they (as HDPA says)

Went off self identifying as a tree.....

Imports are $100bn. Our total consumption expenditure is $300bn. So, what happens when imports go up in price by 25%? Yep, pretty soon CPI increase by about $100bn/$300bn x 25% = 7.5%.

Now, what on earth could RBNZ have done about that? How high and quickly would they have had to hike interest rates to stop people filling their cars with petrol, or to stop businesses buying the diesel they needed to ship stuff around, or the fertiliser they needed to grow food? The RBNZ mandate and toolkit means they are incapable of suppressing an imported price shock. In fact, piling $6bn of extra interest cost onto businesses (cos that's what we do) has probably made 'inflation' stickier.

I would prefer it if RBNZ had spent 2020 to 2024 literally standing around pretending to be a tree. In fact we should have given them a bonus to do exactly that.

Jfoe, do you remember both of us guesstimating when the RBNZ will cut, a year ago? You steadfastly predicted May 2024, I equally strongly predicted August 2024. We may well both be wrong...

Ah. But when should they have started easing?

Guessing what foolish people will do, or more correctly in this case, guessing what the High Priests will do after they have read the entrails, is a futile exercise.

Yes, a very slow track back to 3% (ish) - starting late 2023 was the smart move. As we have both said many times before, the collapse was obvious back then.

Yes, I think you might end up being right though. We get a tonne of data out between 22 May and August (retail survey, GDP, etc) and it will all be awful.

Indeed and that data is likely to be awful.

"Pull lever this way, ugh, tame inflation, yeh, yeh, pull it dis way, boost economeeee. Idiots. "

What I find astounding is that we - most Kiwis - just blindly accept that that is the way it has to be.

We follow what we are told by the High Priests and their army of acolytes without question, never once stopping to ask if there aren't better ways. And we never even question exactly who is benefiting from this system as as we see first hand the middle classes being gutted while the rich grow richer.

Doesn't that make us Kiwis the idiots? By golly. It does!

Could it be much more by design this time rather than incompetence?

With the ensuing instability, surely now is a good time to push through a parallel currency to beneficiaries and let it trickle up(or down lol) before we really need it....

If it is "by design" ... Ask yourself who the designers are benefitting the most.

(The answer is just awful. And why guillotines will become necessary in the not too distant future.)

I will still stick to my forecast made a year ago of a first cut in August 2024.

Second quarter CPI will have been released bringing annual inflation to between 3 and 4 percent, currently 4 percent

Low fruit and veg prices, but chips and chocolate are rapidly rising. I imagine the guvna will side with the junk food and not the healthy options

The point you miss when the current inflation rate is mentioned - and most other commentators (so you're in fine company) - is whether inflation would continue to fall had the RBNZ started easing earlier.

I expect you, like other commentators, will trot out the logic that we must endure an unchanged OCR until inflation is crushed, or slayed, or defeated, or some other words that inspire us to fight and die to the last breath.

I'm fine with that. Just so long as you recognise that you're doing so without evidence that it is required, or necessary, when the early signs that the economy is crumbling were so crystal clear some six months ago.

Its what the guvna will do that matters, as I said. Adrian is more cautious than you might be, but definitely more cautious than me. That doesn't stop me from seeing some sense in his approach.

Methinks you're confusing caution with an absence of wisdom.

Tell me - if RBNZ started dropping interest rates 6+ months ago, as you would have preferred - what would that have done to the NZD? Would it not be decimated, leading to higher costs (in NZD) for imported goods? AKA more inflation?

Let's bump the OCR up to 100% then. Or maybe 200%. Then NZD will be strong and inflation gone, right?

Strawman much, lmfao. It's a fact that if we left the OCR as it was, while the Fed ramped theirs up, that our currency would be worth a whole lot less. Didn't think it was a contentious question tbh.

It's a fact that if we left the OCR as it was, while the Fed ramped theirs up, that our currency would be worth a whole lot less. Didn't think it was a contentious question

That part is not contentious.

Small adjustments in the OCR have historically had little effect on the NZD.

Big ones - or lots of small ones that must be done rapidly - have had an effect.

Guess where we are now?

Interesting with you prediction Yvil,as Rabobank has predicted August & November for OCR cuts- hopefully as an indebted dairy farmer these predictions come true as interest on borrowing is most farmers highest cost,and our annual inflation was running more like 16%, although is dropping with reduced fertilizer & fuel costs.But all is not lost as a Fonterra shareholder,we are in for a so called 300k windfall in 12- 18 months as our board of Directors & CEO convince us to sell Fonterra silverware & step into a more profitable future?🤔

With precision fermentation looming I'm not sure that giving up the value-add products to focus on ingredients (aka milk powder) smart. It's milk powder, for use in chocolate etc, that can be replaced by new technology. But there will always be a market for quality ice cream and cheese, made from fresh milk.

"an indebted dairy farmer these predictions come true as interest on borrowing is most farmers highest cost,"

This is a telling statement and I was unaware that interest on borrowing is the highest cost for most farmers. Is it perhaps they paid too much for the farm so had to borrow a lot?

Let's see is the free fall in the US commercial property market causes a domino in US banks. Risk of rate increase in that scenario.

Pity for those who have picked up a commecial

They can just hang on to the next boom, its time in the market remember............

Cheer for them they

- Pulled the trigger

- Ignored the DGMs

- Took no notice of short term.... noise....

- Aren't focused on the near term anyway...

- Had a sound cashflow plan

Good post ITG, smart guys who know how to create value will be fine, better than just fine actually.

Be smart buy off the overstretched, .... see this one, he was not smart guys

https://www.trademe.co.nz/a/property/residential/sale/waikato/thames-co…

CLIFF TOP LUXURY - Mortgagee sale.

28 Radar Road, Tairua, Thames-Coromandel, Waikato

Ba-you-tiful

Not my thing, dont like tairua

Not Tairua

I think there is some possibility... the RBNZ may yet have to compromise a little on its inflation target

I can't be bothered searching my previous posts, but I have long been predicting that inflation won't get back to 2% but that the RBNZ will be forced to cut the OCR to resuscitate the economy. (The RB's mandate to focus on inflation won't make a difference)

Yes and that's a slippery slope. We decide on 3% this year, what about 10 years down the track? 5%? then 10%?

You are right but if its all imported, killing the NZ economy will not stop it, I think this is also why gold is going up, people realise CBs cannot stop it now, too much money printing has occured

There is going to be some sort of crash - the only question is what will finally tip it over. The boom was too large for too long and the debt level is absolutely frightening.

i suspect the sharemarket will go first when people realise the 'overhype' of AI and that China has already overtaken the west in Technology and its too late to stop the slide. USA and Europe are now desparately trying to stop China from destoying their economies by selling better products cheaper...

Unfortunately for us - reducing the OCR wont .. anything we do to try to stoke the economy by simply enabling more cheap debt will just make things worse. The only way out is to start to rebuild the western economies properly which requires a long period of pain and being humbled

"Higher for Longer!"

https://www.waikatotimes.co.nz/nz-news/350275955/military-vets-worked-t…

Boomers who've seen high inflation. But you can't criticise the old or a female or question someone's accountability

I see they're paying $287 per week in subsidized rent, surely they can cut back on a few luxuries. $85 per f/n on Internet/Phone? More than I pay for a 1 gigabit plan with mobile phone. $462 per fortnight on groceries? More than our household of 2 adults 1 children spends, and we're not broke.

He supports people receiving government money when they are sick, old or cannot find a job, but thinks a lot of money is wasted.

Oh I agree, maybe we could find $1b p.a. in savings by income testing Super at $100k p.a., and redistribute the savings to these unfortunate souls.

Everyone should stop thinking of another OCR plunge. People were deluded that debt was ok because it was so cheap. Debt needs to be serviced by income, otherwise it is toxic as many are finding out.

The current rate is the new normal.

"The current rate is the new normal."

So being in an ongoing Recession is the new normal? (My god some people talk a lot of crap.)

Long term mortgage interest rates have been around the 7% mark, so they are not high now.

The problem is we took on too much debt at 2.9% so it is now a struggle to service it.

A great time to re adjust and get back to basics, maybe reflect on how our parents managed without all toys such as $2000 mobile phones.

So you believe the only way to control the growth of debt is through the OCR?

We are only at more or less the long term average OCR. Its tough to come off the debt drug, but it needs to happen.

So you too believe the only way to control the growth of debt is through the OCR?

Amazing how problematic the OCR is when it’s too high, I never heard this much moaning when it was low and heroin was being pumped freely into the debt junkies / asset holders veins.

Good luck in rehab….

The sky is not falling, it's a storm. It is almost certain that we could remain at this OCR and the economy will eventually grow, after purging the bad debt. That means pain, it means foreclosures, it means business liquidations. The entire outcome is based on stressing everyone and everything until people figure out how to live like this. It might require political change, but the economic pain drives improvements in the efficiency of allocation of resources to satisfy peoples wants.

SKF

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.