Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE/LOAN RATE CHANGES

WBS (Wairarapa Building Society) has trimmed its 2 year mortgage rate.

TERM DEPOSIT/SAVINGS RATE CHANGES

Nelson Building Society (NBS) has trimmed its 2 and 3 year TD rates. And we have reviewed the risks that Kiwi Bond interest rates might slip soon. See here.

THE 'GOLDILOCKS' ZONE

The latest NZIER Quarterly Survey of Business Opinion (QSBO) showed a sharp pick-up in business confidence over the final quarter of 2023. While a net 10% of firms are still expecting a worsening in general economic conditions over the coming months on a seasonally adjusted basis, this is a significant decrease from the net 49% in the previous quarter and the net 79% a year ago.

JOB ADS TUMBLING - SUPPLY OUTPACING DEMAND

The BNZ/SEEK Employment Report shows that the number of applications per job advertisement has now hit unprecedented levels.

'UPCOMING GUIDANCE'

RBNZ will break its summer silence to address recent economic developments. Their chief economist will speak on January 30, a month before the first scheduled OCR announcement for the year in a move clearly aimed at guiding the markets after December's shock GDP fall.

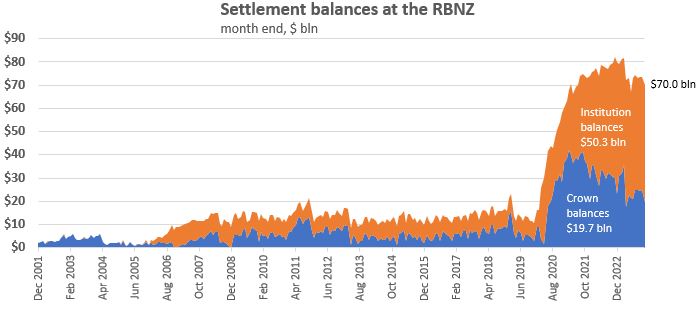

THE COST OF HIGH SHORT TERM INTEREST RATES

Bank settlement balances at the RBNZ rose to $50.3 bln as at the end of 2023, the second highest month-end level of the year. But they were down almost -11% from the same month in 2022. These balances pay the OCR rate, so banks collectively earned $2.6 bln in interest in 2023, up from the $1.2 bln in 2022. Paying interest on these balances is a fundamental monetary policy strategy by the RBNZ." Paying the OCR on all settlement cash balances means that banks with settlement accounts have little incentive to lend settlement cash in the market at interest rates lower than the OCR. The OCR therefore acts as a floor under key short term market interest rates."

ALL-IN ON AI

Microsoft has gone all-in on AI, for both its customers and enterprise partners, releasing its Copilot feature for business customers locally. Juha Saarinen explains.

RUC EXEMPTION TO END

The new Government announced the exemption from road user charges (RUC) for owners of light electric vehicles (EVs) and plug-in hybrids will end from 1 April. They will pass legislation for lower rates for hybrids.

AUSSIE CONSUMER GLOOM

In Australia, the Westpac-Melbourne Institute Consumer Sentiment index fell -1.3% in January from December, remaining in negative territory now for nearly two years. A surge in the cost of living and high interest rates continued to dominate sentiment. The index has been below the 100 mark since February 2022, the longest streak since the early 1990s recession.

SWAPS RISE

Wholesale swap rates may be higher today. However, the key reaction will come at the close. Our chart below records the final positions. The 90 day bank bill rate is unchanged at 5.64% and unchanged from yesterday. The Australian 10 year bond yield is up +7 bps at 4.15%. The China 10 year bond rate is unchanged at 2.54%. And the NZ Government 10 year bond rate is up +6 bps at 4.69%, while the earlier RBNZ fixing was at 4.60% and up +2 bps from yesterday. The UST 10 year yield is now at 4.00% and up +4 bps from this time yesterday. The UST 2yr is at 4.20% and little-changed.

EQUITY WINNERS & LOSERS

The NZX50 is down -0.3% in late trade today. The ASX200 is falling hard in early afternoon trade, down -1.0%. Tokyo has opened down -0.3%. Hong Kong has opened down -0.2%. Shanghai has opened unchanged. Singapore is down -0.4%. The S&P500 futures suggest Wall Street will open tomorrow after its holiday break up +0.4%.

OIL LITTLE-CHANGED

Oil prices unchanged from yesterday at just on US$72.50/bbl in the US while the international Brent price is still at US$78/bbl. That is not to say it is stable; in between, this market has been jittery.

GOLD STILL ON HOLD

In early Asian trade, gold is now at US$2050/oz and unchanged from yesterday, and giving up the interim rises in other markets.

NZD SOFTER

The Kiwi dollar is now at 61.7 USc and down more than -½c from this time yesterday. Against the Aussie we are unchanged at 93.1 AUc. Against the euro we are down nearly -½c at 56.5 euro cents. That means the TWI-5 is now at 70.4 and down another -30 bps

BITCOIN LITTLE-CHANGED

The bitcoin price has firmed today to US$42,624 and up +1.0% from where we were this time yesterday. There's been modest volatility over the past 24 hours of just on +/- 1.4%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

103 Comments

EVs, plug-in hybrids to pay road user charges from 1 April | RNZ News

- Owners of light EVs will pay $76 per 1000km, in line with equivalent diesel-powered vehicles

- Owners of plug-in hybrid vehicles will pay a reduced rate of $53 per 1000km so that they are not double taxed when paying fuel excise duty. The partial rate of $53 per 1000km assumes that on average, a plug-in hybrid will consume petrol at a rate of just under 3 litres per 100km

- Every EV and plug-in hybrid owner will receive a letter before 1 April that will explain the RUC process. The first time an EV owner buys their RUC licence they need to give their odometer reading

- Whenever a warrant of fitness is carried out, a vehicle's odometer will be reviewed. If the odometer exceeds the RUCs purchased by the vehicle's owner, they will be invoiced for any difference

Finally, some fairness...

Hardly fair.

A 1600kg Leaf pays the same as a 3500kg ute.

& the next band is 6000kgs, increasing then to 9000kgs & so on. lines have to be drawn somewhere & sensibly

https://www.nzta.govt.nz/vehicles/road-user-charges/ruc-rates-and-trans…

Most utes in NZ are around 2000 kg (unladen), so it's not really that big a deal.

Double cab utes are more like 2500kgm and have a much larger footprint than small vehicles require larger parking spaces and do more road damage. Are we trying to encourage people to drive large vehicles?

Also forgotten is our emissions reduction target and we will have to purchase offshore mitigation.

Balance of payment. We are 87% renewable with our electricity as opposed to imported fuel.

The wear on the roads goes up exponentially with weight so the difference under 3000kg is negligible.

For things like climate change and balance of payments, there are other things that can incentivise behaviour

How many utes weigh 3500kg ? Most road going utes weigh in at 2 tonne

Hardly fair that a ute has to still pay RUC even when being used on private land unless the driver goes through the hassle of getting exemptions for that private land use

boats pay fuel taxes for roads

Everyone can agree that a cleaner fleet is good for the environment but right now our roads are in dire need of upgrades and repairs. Should those who can't afford EVs be footing the entire bill? No way!

It's interesting, comparing my Leaf to my Prius (non-plugin) - they both weigh basically the same so will do similar amounts of damage to the roads.

Leaf will pay RUC of $76/1000 km including GST.

Prius gets about 5 L/100km so will use around 50 L to travel 1000 km. For this the fuel taxes add up to $41 (70.684 c/L + GST). So I'll pay less tax on my petrol powered vehicle.

Another way of thinking about it, is that the RUC rate is comparable if your vehicle has a fuel economy of 9.3 L/100km. If your vehicle has a better fuel economy than that you're better off on fuel tax, but if it's worse RUC would be better.

They need to move everyone to RUCs. And improve the system so no pre-purchased stickers (it isn't 1970 anymore).

just as well thats exactly what Nact are planning then huh? its even mentioned in the press release.

Transitioning EVs and plug-in hybrids to RUC is the first step in delivering on the National-ACT coalition commitment to bring all vehicles into the RUC system.

It was always going to happen...and id be surprised if all vehicles are not required to has a linked GPS fpr billing....what else can they do to pay for the infrastructure when an ever increasing portion of the fleet is not paying fuel excise?

Can't see ACT supporting compulsory gps tracking of all vehicles, sometimes their libertarian streak is actually a good thing.

If the revenue source is going to be RUC (road use) rather than fuel excise (due to declining use) then a direct billing from some form of GPS tracking makes efficiency sense...libertarian or not. The alternatives are tolls (also GPS tracked) or the current manual system.....ACT will not stand in the way of 'efficiency'....one way or another vehicle use will be tracked and levied.

Good luck with that.

Their libertarian credentials are fairly soft. Anything to do with Epsom and they become arch-conservatives all of a sudden.

Well why not just move all onto RUC on April 1? EVs are being penalised in the meantime. We all know the transition is necessary

Penalised? Hardly. Finally paying their share.

There is no way they could cope with 2 million vehicles being added to the RUC system in one hit, it's likely to be a cluster F as it is.

Speedmax,

I have an EV and accept that as a road user, I should not be exempt from RUCs.

Great, government and business tracking your every movement. Give me the freedom of 1970 any time thanks.

For now its a simple odometer reading, so they know how far you've gone, but not where or when, so not exactly impinging on your freedom.

Great analysis. I'd hope they address that anomaly by introducing a sub-2000kg class, with lower RUC charges.

This change also does a pretty big job of reducing the cost benefits associated with driving an EV or PHEV.

Current "Per 1000km" nominal costs (assuming $2.50 petrol)

- Average Sedan/Medium SUV - Eg Rav4/Camry - 9l/100km - $225

-Average Hybrid - Eg Prius - 5l/100km - $125

-Average PHEV - Eg Outlander - 3l/100km + $53/1000km - $128

-Average Electric - Eg Tesla 3 - $76

It does cost more up-front to buy electric (or hybrid), and now the benefits are watered down, it will make people more likely to buy a petrol powered (or more petrol powered) vehicle than otherwise.

But it's alright - something something more chargers something

Well, if you only look at the short term maybe, but factor in how much nicer Evs are to drive, the near zero cost of maintenance, and the fact that petrol cars will be on RUCs in a few years you might regret that decision down the line.

Jeepers, my gas guzzling Audi v6 will pay less than a leaf (Most of our driving is highway) - incroyable!

What about the cost of electricity to charge the Leaf?

Its a swings and roundabouts game, my supercharged v8 gets about 25l/100ks around town, weighs in at 1.9T. Rucs would be a win for me.

So you are better off having a PHEV than a BEV if you never use petrol in your PHEV.

The new outlander has like 84km on EV only. I think that would cover a lot of people's daily driving

One MP down and we are only half way through Jan.

Who's next?

I was tiring of greenie hypocrisy well before this affair. This has just heightened that.

A ‘greenie’ who is clearly super materialistic.

ok

Glasshouse and stones ...

Greenhouse

I think he means " most shoplifting is commited by white CIS males ".

No I mean govt coalition supporters may want to think twice before insulting greenies. We already have a alleged assault of a ex mps sister, and a ex mp abusing airline staff this year. I would go back further but I don't have all day.

It would appear we aren't allowed to comment on this topic!!!

Despite one of my responses being "deleted" I'm quite happy to abide by the site's moderators decisions. Its fair enough, we all have a choice to participate or not & it has to be said that we & the site owners usually take a robust view of debate.

Same here (I think it's because I used a word that can also have a naughty meaning, and the double entendre was deliberate based on some recent clangers from our esteemed minister of finance).

It would appear we aren't allowed to comment on this topic!!!

That's unfortunate. I believe entitlement is a problem in NZ, right across the political spectrum and in the public sector in particular.

Partisanship on here exhibited some fairly distasteful extremes during for instance Mr Muller’s & Ms Allen’s personal challenges. Intervention by the moderator, to preclude that recurring, is both welcome and prudent by my count.

Party of benefit fraud , shoplifting and "social justice".

Finally one of my predictions was right! I did predict she would blame mental health. Hard to know how mental health makes you steal high end clothing.

For those who haven't followed it, the case of the UK Post Office prosecuting 700+ of it's sub-post masters based on data from faulty software is yet another sobering reminder of the incompetence of those who hold high office. 700 unlawful criminal convictions, innocent employees going to jail, losing their houses and commiting suicide.

I make no apology for holding the behaviour of Golriz et al to account. Representing the public is a privilege, not a right. If you cannot behave appropriately, do something else.

https://time.com/6552764/uk-post-office-scandal-police-investigate-pote…

And I haven't seen anyone suggest she should do anything less than resign, and face police action. Even those socialists greenies.

Agree, I have been following that for some years. Another blatant example is the Robodebt scandal in Oz.

https://en.m.wikipedia.org/wiki/Robodebt_scheme

Yes, that has many similar qualities to the UK Post Office scandal. The common theme is people in power persecuting the vulnerable for their own self-aggrandisement and with little real consequence if caught.

Representing the public is a privilege, not a right. If you cannot behave appropriately, do something else.

Yes indeed.

Yet wealthy and sometimes famous people get caught shoplifting. If it's not for money, what is it?

If you represent your community, the bar is higher.

You don't understand that mental health problems can cause you to do strange things? Odd. I find it hard to imagine someone in that position stealing unless they have mental health problems.

It's certainly not an excuse, but it may well be a reason. Resignation and dealing with her issues is the right course of action.

Hard to argue with that except suggest that resignation and dealing with it, or any other warning signs for that matter, should have been a lot more prompt. That is, if the event now being reported as occurring in Wellington in October is a fact, then that would have been both the responsible and appropriate time to address the concerns that are only now been explained by the Green Party.

I haven't seen anything to suggest the green party knew about the October incident before today, so hard to say how they could have responded before now.

Any party would have given their Mp a chance to resign, and that couldn't happen till she returned from overseas.

Reportedly the proprietor in Wellington laid a police complaint and provided at that time, the video footage published in the media this morning. If the Green Party were not in the loop about that, then they damn well should have been.

They only emailed other shops about it yesterday, it is unclear when the police complaint was made.

Other than that, on what grounds would the green party be informed legally?. They are not her employer.

Agree solardb. I think the G&T is strong amongst some of her detractors. Mental illness is a curse. Comes out of nowhere. And many of Gloriz generation are poorly equipped and poorly supported when it happens. Calling it 'entitlement' (or similar put-downs) is lazy and ungenerous. She stuck her head above the parapet. She has stuck her neck out for what she believes in. She has been found wanting and acknowledged this. She has my support as she moves forward.

There are people out there that would probably spit on her in the street! I certainly wish her no harm, she will have a pretty rough time from here, I feel quite sorry for her. But on the other hand I do love a bit of gossip and I find the whole thing quite intriguing.

solardb you appear to have a penchant for denial of reality. Try for just one example 1 News website. Timeline of a downfall. October 26 2023 alleged first shoplifting incident at Cre8iveworx in Wellington [police have confirmed a shoplifting report at the shop on this date.]

Chloe was with her in the video footage.. there’s more to this

I have plenty of sympathy and empathy for mental health struggles. At the same time, I think mental health issues are being used too much as an excuse for unacceptable behaviour. The medicalisation of bad behaviour.

Most crime has mental illness as a root cause, the mental health card for shoplifting is the cherry on the cake of this sordid saga.

The sooner the nation is held to account for it's behaviour, the better we will all be. I include Maori in that.

The sooner the nation is held to account for it's behaviour, the better we will all be. I include Maori in that.

Well knock me down with a feather…. Never thought I’d see you say that…you may not be the as biased as I thought.

Hell, I might even invite him over for a beer. Probably a “Pale Ale.”

The woman has MS! It does affect mental acuity! She is an intelligent, well paid individual with social conscience. There will be more than meets the eye.

Its highly unlikely her physical health condition had anything to do with it, considering that she immediately refused to open her bag when challenged by the AKL store.

There were some rather unsavoury episodes and personalities that emerged out of the National Party prior to the 2020 election.. In particular in the odious form of a mp texting youngish females and if I recall correctly a lame attempt at mental illness was proffered as an excuse. Resorting to the convenience of what is a serious and often tragic circumstance is shameful behaviour by any measure to my mind, to use as an escape hatch.

Yes I suspect that will have played a large part. There’s published evidence showing people with degenerative neuro disorders have an increased risk of criminal activity with theft being at the top of the list.

https://www.sciencedaily.com/releases/2015/01/150105125832.htm

from your link: "The medical review showed 204 of the 2,397 patients (8.5 percent) had a history of criminal behavior that emerged during their illness." Hardly convincing:

“Survey estimate that about 29 per cent of New Zealand adults are victims of a crime in a given year, but reporting on those crimes happens only in about 25 per cent of cases.” The Front Page: What’s behind the spike in crime? - NZ Herald

Rubbish

I know of several people with MS (and my mother had it) it’s a big struggle sure but not a reason to shoplift repeatedly

this medicalisation of bad behaviour is really annoying

She was simply carrying out the "Green with Envy" Party tax policy a little too literally, which is to waltz in and thieve from hard working businesses trying hard to be successful.

Is it a very wise excuse though? Imagine if Sam Uffindells excuse was mental health, an uncontrollable urge to hurt people, he wouldn’t have a job now. Probably best to just apologise, people will eventually trust you again.

Agreed, we had a lack of accountability on the highest order with the last government. The public just want honesty ad ownership then to move on

“I find it hard to imagine someone in that position stealing unless they have mental health problems.” - fair enough. Unless she did it for the thrill or to be a bad ass or because she simply wanted the stuff and didn’t want to pay for it. I guess it’s like rich people that commit fraud unnecessarily, are they all mentally unwell?

Something is up with mental health in this country. It’s getting to the point where so many seemingly normal people have significant problems. I think there is so much pressure to do the right thing and eat healthy and not drink alcohol and not do almost anything, then life is so boring your mind starts making things up.

It is the flow on effect of social media and the attention economy enhancing what you suggest as the pressures we face, couple'd with the current financial climate and decrease in community sense and social cohesion that resulted from lockdowns and mandates over the last couple of years. Everyone has a breaking point, and I find is so common that people have ruminating struggles form 2020 onwards that haven't been dealt with, or they have tried and had no luck with a mental health referral from their GP. Mike King is onto it, he sees it daily and is doing something to help.

You don't understand that 'mental health problems' are part of the templated response for shamed public figures?

No MFD. Unless you call attitude mental health.

I am a retired nurse having worked all my nursing career in mental health and it sickens me that when this type of crime takes place they blame mental health

I would put my house on that bounce in confidence being almost entirely down to the election rather than anything deeper than that. All the intel I am seeing and hearing is pretty pessimistic.

Exactly - business leaders are all chipper because they are looking forward to a bonfire of regulations, and better tax breaks... But, given them 6 months and they will be demanding that Govt does something about the dire state of the economy and the lack of demand.

Exactly

A confidence ‘dead cat bounce’

Wait until the govt comes back to them after that 6months and tells them they got their freebie at the start, now they're on their own and should have the capability and business acumen to succeed without further government intervention. Not a big fan of National but if they were to do this then at least they;d command a bit more respect.

I think there is a period of time after the bottom where people adjust accordingly and get over it. In this case for many people the bottom would be the peak of interest rates which started probably six months ago.

I’m certainly sick of holding back financially, time to get back to normal again.

I had a splurge with our Japan trip, back to frugality 😂

I've never heard someone come back form Japan singing anything but the biggest praises for it. Hope you had a great trip :-)

Sickly start to the year for Australasian shares.

Only a few days ago I was considering moving my KS fund from cash to a more aggressive fund, but not so sure now. My cash fund did nearly as well as the more aggressive funds over 2023, despite the big rally in shares in the final quarter, and the risk profile is obviously much lower. Lots of volatility and risk in 2024 I think, might stick with cash, at least until interest rates start falling meaningfully.

Cash funds should pay 5% this year with no risk.

If you think the risk profile of being in cash is 'obviously lower' you should consider opportunity cost.

History suggests your net risk to retirement finds is higher in a cash fund.

The BNZ/SEEK Employment Report shows that the number of applications per job advertisement has now hit unprecedented levels

Met a couple of recruiters to discuss job roles we're about to advertise shortly. Turns out there is no shortage of candidates applying for jobs that are all talk and no substance.

No wonder the handful of worthy candidates in the market are still demanding big pay hikes.

I questioned the size and depth of the Bank of Mum and Dad in NZ as there doesn't seem to be any definitive data to indicate the reality. Across the ditch, SMH picks it up and comes out with a reckon that a whopping 75% of first home buyers are getting help.

But the reckon is from the RE industry and a survey. It may be true but take it with a grain of salt.

Jarden concluded from surveying mortgage brokers that about 15 per cent of borrowers were using some form of family assistance to buy a home, receiving $92,000 on average from their parents.

“If we assume the majority are first-home buyers, it would imply about 75 per cent of first-home buyers were receiving some form of family assistance,” he said, noting it was up from 60 per cent in 2017 and 12 per cent in 2010.

https://www.smh.com.au/property/news/a-500-000-helping-hand-how-the-ban…

Those settlement balances are interesting - quite a big drop in recent weeks. This seems to in part the result of RBNZ doing some massive FX trades over the Christmas period while nobody was looking - like $44bn worth of buying and selling. Govt spending also outweighed revenue in December meaning settlement balances reduced accordingly (as is typical in December - although Govt better get used to that as it pursues it's dumbass austerity strategy).

National Bureau of Economic Research suggests that 14% of the $2.7 trillion commercial real estate loan market in the US— and 44% of office loans — currently carry outstanding loan balances higher than property values and are at risk of immediate default.

https://commercialobserver.com/2023/12/report-44-office-loans-14-of-all…

When will financial reality apply...?

The sheeple don't pay any attention until the mainstream media of their choice reports it and it becomes accepted reality around the water cooler.

https://www.nzherald.co.nz/nz/politics/national-soars-in-new-poll-as-vo…

"National soars in new poll, as voters agree country is ‘on track’, Chris Hipkins crashes record low...

National hit 41 per cent in January, a massive jump from the 36.5 per cent it scored in the December poll."

Gees it’s a bit worrying that so many people think this coalition is taking us in the right direction. Anyway I’m sick of politics at the moment, let’s get back to talking about the economy and stolen clothes.

Haha exactly. Although the clothes thing is politics right 😂

my interest in, and respect for, politicians has sunk to all time lows. And that’s saying something

hell, I might be on the early path to libertarianism 😂

Or authoritarianism

Don'tcareianism?

Yes although I’m less interested in the politics of the thefts. It would be just as interesting if she was a journalist or celebrity.

The critical race theories behind it are nauseating. TO suggest GG has had anything but a privileged upbringing is delusion. Spent more time in departure lounges than in refugee camps.

Different year, same ole garbage from OneRoof, especially the nonsense spouted by the mortgage advisor:

https://www.oneroof.co.nz/news/nz-property-market-forecast-what-are-the…

he, or just as importantly OneRoof who oversee these articles, need to check the math - good luck covering a 750k mortgage on less than 150k income per annum!

re .. "Bank settlement balances at the RBNZ rose to $50.3 bln as at the end of 2023, the second highest month-end level of the year. But they were down almost -11% from the same month in 2022. These balances pay the OCR rate, so banks collectively earned $2.6 bln in interest in 2023, up from the $1.2 bln in 2022. "

{kind=link}

Corporate welfare? i.e. The RNZ raises the OCR, borrowing from banks falls, banks' profit margins are in danger ... So the RBNZ tops up their profits and ensures their shareholders continue to suck money from the NZ economy? How about using regulation instead RBNZ?

On another note ... Mr Orr needs to be very careful the RBNZ isn't doing a Norman Lamont with their market interventions. If the market decides there's money to be made taking the RBNZ's position apart, the market will have no qualms in rubbing the RBNZ's nose in the mud.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.