By Peter Dragicevich*

The NZD has had a renewed pep in its step recently with the currency climbing from the bottom end of its 2024 range (i.e. ~$0.5850) to ~$0.6160 (above its two-year average) in a matter of weeks.

This predominantly reflects global forces rather than a turnaround in domestic fundamentals.

The more upbeat risk sentiment as equities have rebounded sharply from their 5 August panic sell-off due to easing US recession fears, and USD depreciation on the back of declining bond yields as the start of the US Federal Reserve’s easing cycle comes into view have been influential. It shouldn’t be forgotten that in FX the USD is in the driver’s seat with other currencies essentially ‘price takers’ of its underlying trends.

That is not to say New Zealand-centric developments don’t have an impact on the NZD. FX is a relative price and macroeconomic under-currents typically shine through more cleanly in the NZD’s performance against other currencies. With this in mind, we think the challenged New Zealand economy and other regional headwinds means the NZD is biased to underperform on the crosses over the period ahead. This relative story can act to cap the NZD’s upside potential versus a weaker USD. Bottom line, we think myopic markets shouldn’t lose sight of the bigger picture. There are still more NZD headwinds than tailwinds manifesting.

The pivot by the RBNZ from ‘inflation fighter’ to ‘growth supporter’ at its August meeting is one reason which we believe should undermine the NZD on the crosses over the medium-term. This is especially the case against currencies like the AUD given Australia’s sticky domestic inflation pulse and resilient labour market point to the RBA holding interest rates steady for a while yet.

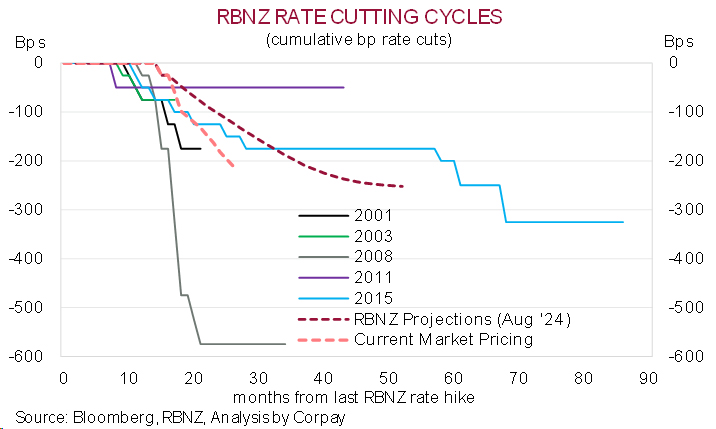

The recent 25bp rate cut by the RBNZ is the first of many to come due to subdued activity, unfolding upswing in unemployment, and positive inflation signals. Below trend New Zealand GDP growth appears set to continue for at least the next year, with constrained kiwi consumers, subpar business sentiment, reduced net overseas migration, and negative feedback loop generated by the lagged effects of the RBNZ’s still ‘restrictive’ settings, a deteriorating labour market, and rising insolvencies rippling through the system.

Arguably the RBNZ’s forecasts looking for the Official Cash Rate to steadily fall from 5.25% to ~3% in H2 2027, which is estimated to be the equilibrium ‘neutral’ level, might prove to be too conservative especially in terms of the anticipated speed of descent.

New Zealand’s dwindling yield advantage should ultimately act as a NZD handbrake. Indeed, in our opinion, various yield spreads already imply the NZD may be too high and that its nascent revival could be on borrowed time.

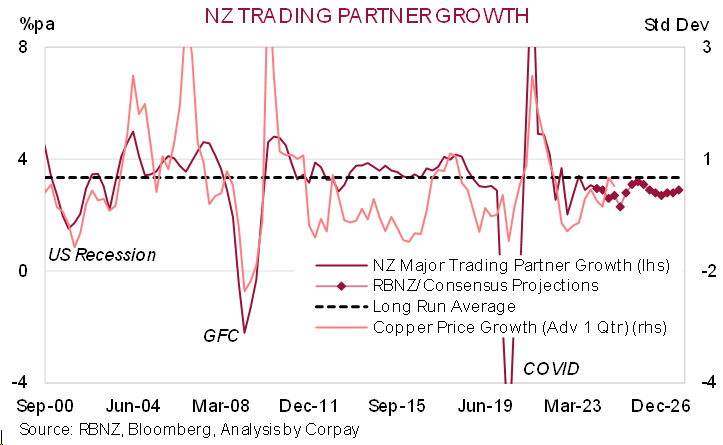

More broadly, the global and regional growth trajectory also isn’t compelling. This has important direct and indirect spillovers for a small open economy like New Zealand and the NZD. China’s stumbling post-COVID cyclical recovery is compounding its unfavourable demographics and protracted property downturn. Importantly, there are few signs a sustainable reversal is on the horizon because of the structural issues at play. Given China’s standing as the major trading partner of ~120 nations this can have far-reaching and long-lasting consequences.

New Zealand is in this boat as it sends ~1/4 of its merchandise exports directly to China, with almost 2/3’s shipped over to broader Asia and Australia. As our chart shows, the RBNZ’s figuring indicates ‘below average’ growth across New Zealand’s major trading partners is expected over coming years as China’s issues cross paths with sluggish momentum in several major nations stemming from higher average interest rates, elevated debt burdens, and/or geopolitical uncertainty.

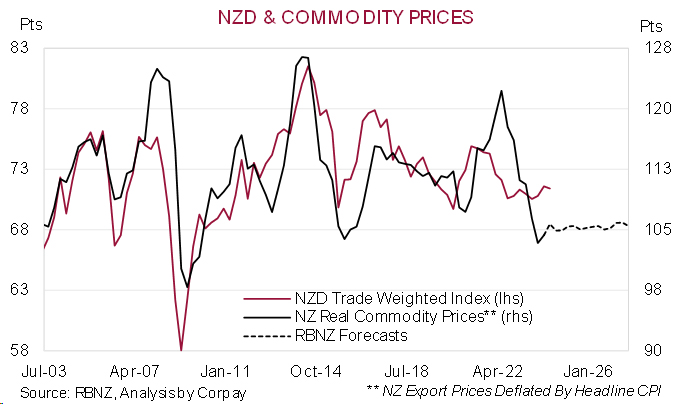

This is also a reason why New Zealand commodity prices, when adjusted for inflation, are projected to only move sideways the next few years. If realised, the flatlining of New Zealand real export prices at lower levels could be a drag on the NZD trade-weighted basket.

Peter Dragicevich is Currency Strategist, APAC, at Corpay, based in Sydney, Australia. This is his Peter’s personal opinions and analysis and does not necessarily reflect the opinion of or endorsement by Corpay. This presentation is provided for general-information only. This presentation is not (and does not include) advice.

2 Comments

I'm surprised how the NZD has held up in recent weeks, and now I expect it to hold its value despite the domestic economic woes.

Currencies from the Middle East and tax havens dominate top performers in 2024

https://www.unbiased.co.uk/discover/personal-finance/savings-investing/…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.