By Andrew Laming*

Although it doesn’t cover the entire credit spectrum, it’s fair to say that the agri credit appetite has improved for those in the middle and stronger end of the risk curve.

On the back of better fundamentals in the dairy sector, some lower interest rates in the mix and (maybe) some spillover impact from the parliamentary inquiry into banking competition, we’ve observed a stronger appetite in the agri sector.

These improvements have been threefold: better access to further capital, better terms and better customer lending margins for some farmers.

But are the drivers of this extra appetite really due to better dairy payout and lower interest rates?

We think not.

Firstly, if this year remains at $10/kgms + - it’s a really good payout, but on an inflation adjusted level versus history, 2022 was higher at $~10.50 (inflation adjusted), 2014 was a whopping $11.18 in today’s dollars, and 2011 was $10.45 (inflation adjusted). The last five years have averaged $9.09 (inflation adjusted). So, it’s good, but not massively better than average.

Also, the sheep and beef sector, while improving, still has a wee way to go yet before we can say that we’re back on track.

So, what’s going on then?

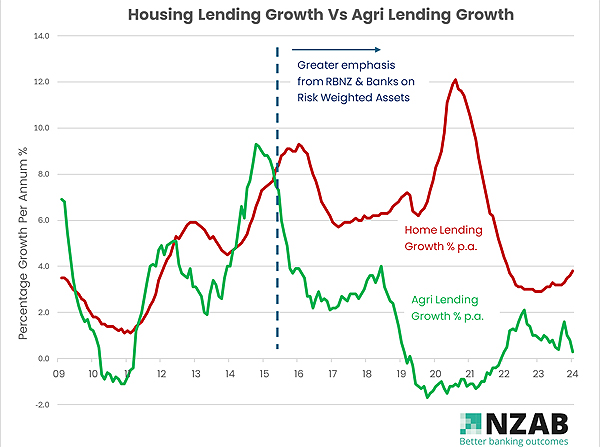

Well, take a look at the below graph, it’s the annual percentage change in main bank lending in housing versus the annual percentage change in agri lending, since 2010.

We’ve put a line through 2015 as this was where banks stepped up a gear (with Reserve Bank “insistence”) on recognising that the agri loans required more bank capital. This had the effect of lowering the returns on these loans (from a “return on equity” perspective) as they sucked up more of the bank’s tier 1 capital. And importantly, much more tier 1 capital than home lending.

Noting that this period also correlated with the “dairy downturn” at the time, we almost overnight we witnessed a massive drop in agri lending growth, despite years of a strong correlation between agri lending growth and other types of lending.

This disparity amplified during Covid when more liquidity (from Reserve Bank & government) was pumped into the banking sector, and fuelled by lower risk weighted capital requirements, banks went ballistic on home lending. The graph above effectively illustrates which sector that growth in home lending was pulled from i.e. agri.

And that brings us back to now.

When New Zealand first went into recession on the back of large interest rate rises in 2022/23, the home lending growth fell considerably to sit well under the long run average. It remains at that low level of demand today.

And the impact? Well, all of a sudden, we’re seeing better appetite in the agri sector, plus also in the business sector as well.

In short, this is a substitution effect. Quite simply, banks want to continue to drive profit (as do most businesses) and a massive section of their portfolio (housing), is not growing as intended, leading to a renewed focus on other parts of their portfolio (i.e agri and business banking) to continue to drive lending volume growth.

So what? This is a good thing, right?

Yes, is the short answer, in the short term. More appetite equals more competition which results in better outcomes for borrowers.

But (and unfortunately this is a massive but!), what happens when the economy swings back into gear and housing gets off the canvas? It's not hard to envisage a swing back to the easier and less capital-intensive home loan borrowing.

Farmers are intergenerational in their thinking and with their investment decisions, they are used to the ups and downs of commodity cycles. However, their investment horizon is decades in length. Volatility of credit appetite (all in or all out) is simply not a good match.

But don’t get frustrated - just make sure you understand the factors at play and use them to your benefit.

For us, this means taking advantage of these periods of better appetite to engage professionally with competition. This means ensuring your farming business is well set up and “owns your credit risk”.

When a farmer “owns their credit risk”, they then have the confidence to create a market for their loan. They can interact quickly with the banking market, get swift outcomes and the best possible rates and terms.

Understanding and presenting credit risk is not simple. Given the range of outcomes and what it means for future business success, it is not a process that you want to DIY. It is also dynamic. The credit tolerance and pricing for a bank was different last year and it will be different next year. Staying abreast of this is challenging.

It is certainly not something you want to simply “leave with the bank”.

What else should you consider right now?

Where your bank allows you to via their product suite, consider fixing your margin for longer periods during this time, but keep a range of maturities – as typically fixing longer costs more.

Also, take care when extending with further debt during times of high bank appetite that might later put your credit risk “outside the box”. This doesn’t mean that expansionary credit at these times is unwise, far from it – but it does reinforce the need for high quality strategic decision making in your business.

Just because the bank now says yes, it doesn’t necessarily mean it’s the right thing to do (nor does it mean its wrong either!). Ensure your strategy and resultant capital structure is fit for cyclical credit appetite so you don’t get knocked out of bed at the bottom.

And this increased appetite from the main New Zealand banks doesn’t solve for the gap in credit risk right across the spectrum.

There is still a significant credit gap versus what banks used to extend to farmers. Have a read of Scott Wishart's article here to get you thinking about this a bit more.

*Andrew Laming is a founding director of NZ Agri Brokers Ltd (NZAB) and is based in Timaru.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.