Food and agribusiness banking specialist Rabobank New Zealand argues the NZ rural banking market has a high degree of competition, and says farmers should be seeking ways to optimise production whilst operating within planetary boundaries.

Rabobank's CEO Todd Charteris says this in a submission to the parliamentary banking competition inquiry being undertaken by the finance and expenditure and primary production select committees. With the Commerce Commission having recently completed a market study into competition in the personal banking market, the select committee inquiry is expected to take a particular focus on business and rural banking.

As of June 30 this year, Rabobank says it had 21.7% of NZ’s rural lending market, having provided 40% of all new lending to the rural sector over the first six months of 2024. Over the 15 years to 2023 the bank says it has provided 30% of new lending to the agriculture sector.

"Currently, relatively flat growth across rural lending has resulted in what many of our experienced bankers regard as the most competitive market they have seen. All banks have an appetite to increase their market share. Rabobank’s success to date is due largely to our single focus on rural banking, supported by our sector knowledge and networks, together with our long-term access to capital," Charteris says.

"Data compiled by CoreLogic shows that over the past decade, Rabobank has posted positive gains through rural mortgage switches in all but two years, which has contributed to our overall and ongoing business growth."

"As a general observation, Rabobank believes the New Zealand rural banking market has a high degree of competition. It is not dominated by a single bank, with the rural lending market shares of all five of the largest banks ranging from around 14% to 24%," says Charteris.

Rabobank also notes, however, the absolute capital requirements and significant infrastructure investment required to meet increasingly complex regulatory obligations are significant barriers to entry for new entrants.

The big five rural lenders are ANZ NZ, BNZ, Rabobank, ASB and Westpac NZ.

Big 4 banks have a capital advantage

Charteris notes regulatory capital is a function of risk-weighted asset allocations prescribed by the Reserve Bank. Rabobank being mandated as a “standardised bank” means it must have a 100% risk weight to agribusiness exposures, while the other four major rural lenders use the “advanced” rating model, letting them have a lower risk weighting.

"This is reflected in Rabobank’s lower return on equity. Rabobank’s return on equity over the last seven years has ranged between 5% and 7%, which is comparatively lower than our key competitors in the New Zealand market. The key driver of this lower return on equity is the level of capital we hold to meet the Reserve Bank’s capital requirements."

"For Rabobank, our risk weighting for the majority of assets is 100%, compared to competitors using the advanced capital model allowing an 80% to 85% weighting. As we are competing in the same market, Rabobank is unable to extract a premium for this higher capital weighting, which is in turn reflected in our lower return on equity," says Charteris.

Noting the other four banks also have lending exposure to sectors other than agriculture including housing and corporates, the latest quarterly Reserve Bank data has Rabobank's return on equity at 7.4%, versus ANZ's 13.1%, ASB's 12.7%, BNZ's 12.5% and Westpac's 11.4%.

'Very different risk profiles'

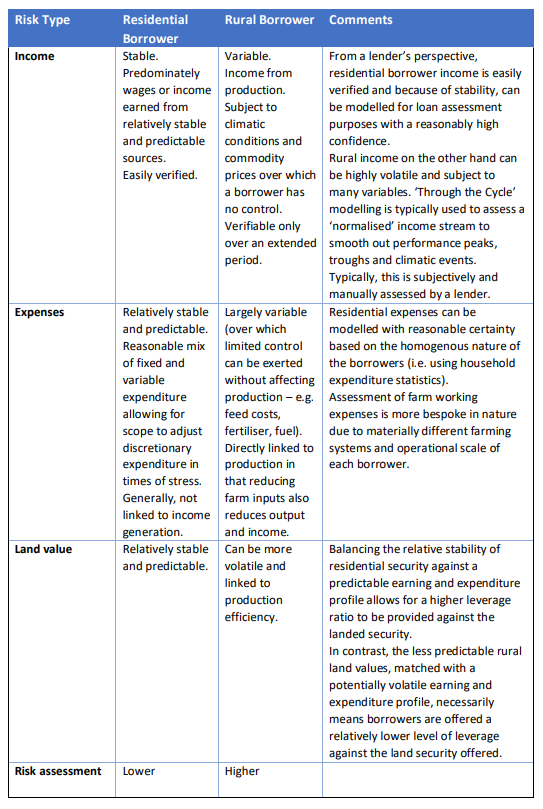

Meanwhile, Charteris says it's important to differentiate risk factors affecting rural clients, given these are distinct from residential borrowers.

"These very different risk profiles are reflected in local regulatory settings for calculating risk-weighted assets, which require New Zealand banks to hold a significantly greater proportion of capital against rural lending than for residential lending. For rural lending, the combination of different risk profiles, the need to apply individualised credit risk assessments and higher risk weightings are all reflected in the interest rates applied to the sector. While the security type (a mortgage over land) may be similar, that is really where the similarity ends, as we have set out in the following table."

'Interest rate margin variability is common'

Charteris says Rabobank sets lending interest rates for rural customers on a case-by-case basis.

"We employ a thorough process that takes account of each client’s circumstances, including sector exposures, entity governance, variability in both income and costs, commodity outlooks, business plan information, the current and forecast financial position and any other relevant risk factor to calculate an individual probability of default. This is combined with an assessment of our ability to recover a loan in default through any collateral provided. As each client’s circumstances are different, interest rate margin variability is common."

On issues of sustainability and climate change, Charteris says; "farmers can and should be looking for ways to optimise production at the same time as operating within planetary boundaries – this is also good for their long-term performance and the creation of intergenerational wealth."

Charteris also says more than 80% of NZ’s exports go to countries with mandatory climate-related disclosures either in force or on the way.

"Another factor is the emergence of Climate Border Adjustment Mechanisms (CBAM). The European Union is requiring all imports into the EU to comply with its soon-to-be-implemented CBAM and the EU Deforestation Regulation."

"Currently, levies apply only to a range of heavy industrial items such as steel and iron. The United Kingdom, Australia and Taiwan are shaping as fast followers in this space. More broadly, as part of a global organisation we want to contribute to feeding the world sustainably, transforming the way we produce and consume energy, and fostering prosperity in the communities in which we are active," says Charteris.

Rabobank NZ, whose ultimate parent is a Dutch co-operative, says its total lending is now at $17.2 billion. It has about 4,000 rural lending customers, 1,600 rural deposit/credit only rural customers and 31 wholesale, or institutional, clients, plus about 54,000 customers in its Rabobank Online Savings business.

"To date, 100% of our profits in New Zealand have remained in this country as retained earnings, financing our ongoing and growing commitment to supporting Kiwi farmers and growers. This is a compelling point of difference for us in the New Zealand market," Charteris says.

*This article was first published in our email for paying subscribers first thing Thursday morning. See here for more details and how to subscribe.

3 Comments

Here is a thought for Rabobank, they say they have 54,000 online savings customers. Rabobank have made the decision that they only want customers who will bank on cellphones or ipads. Other banks seem willing to continue to provide on-line computer friendly services. I am sure I am not the only person who over time will close their savings and term deposits with Rabo and go elsewhere. Very sad as Rabo gave NZers the opportunity to support our rural community. I have no problem using passwords but don't disenfranchise your savings base.

The website isn't scheduled for closure to my knowledge. I agree, though, I use it 90% more than my phone. Having to do two-factor login via cellphone rather than the old DigiPass isn't all that different.

Banking apps can be inherently more secure than using a computer browser, where versioning is mandated, and the operating system's ecosystem is stricter. As a result, their fraud/AML costs would be proportionally lower than the major banks to offset the operating costs.

As someone with a TD it would be unlikely you log into it frequently, like your regular chequing account.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.