By David Skilling*

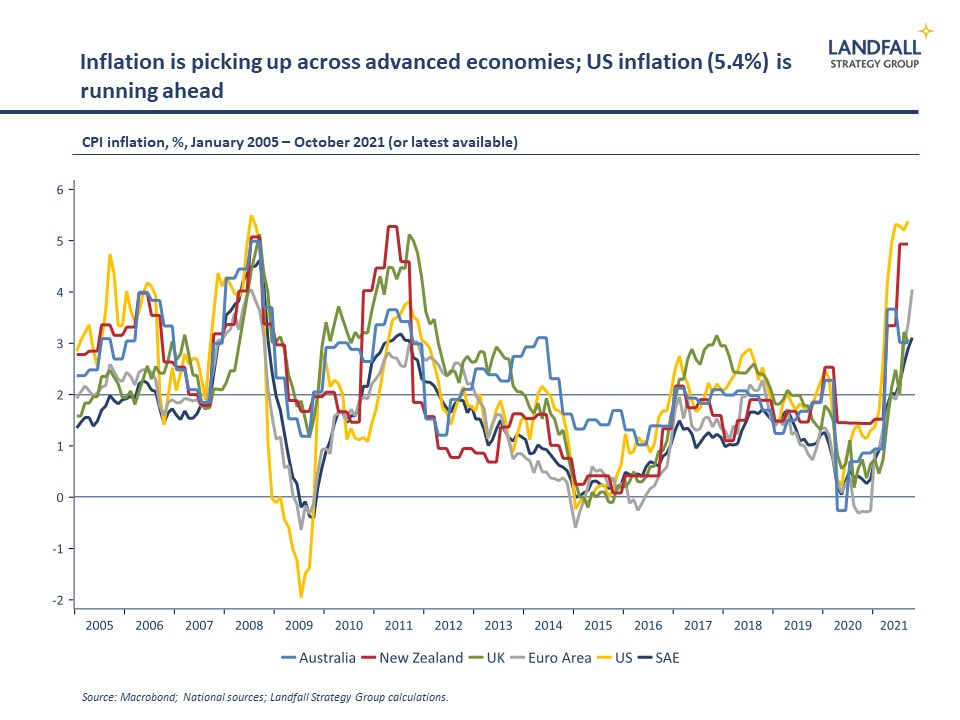

Inflation – and the inflation debate – is heating up. Recent inflation readings in the Eurozone, the US and the UK, as well as Australia and New Zealand, have come in above expectations.

Opinions vary widely on how persistent these inflationary dynamics will be. Some central banks (Norway, New Zealand) have already lifted rates, and bond markets are pricing in rate rises by large economy central banks. But the ECB, the Fed, and the Bank of England remain unpersuaded.

Accelerating from 0 to 100

There are good arguments on both sides of the inflation debate. Resolving the issue is complicated by the unprecedented nature of the Covid shock and the speed of the recovery. The global economy is moving from a hard shutdown in 2020 to a very strong recovery process.

So it is not surprising that pressures and constraints are emerging across the global economy, from supply chains to energy prices and skills shortages. As well as inflation.

But recent data should not be over-interpreted as necessarily a resurgence of broad-based inflation. Inflation will be higher for longer than expected a few months ago, but these pressures may plausibly weaken significantly over the next 12 months.

For example, supply chain disruptions, as well as energy and commodity prices, may ease as bottlenecks are addressed and consumers rotate from buying goods to consuming services; China’s growth may slow markedly; and fiscal policy will become less stimulatory.

However, vigilance on inflation is required. This is particularly so given that many advanced economy governments are likely to continue to run high-pressure economies. Fiscal tightening is likely to be gradual so as not to endanger the recovery – and increased government capex is likely. And on monetary policy, my assessment is that there will be economic and political constraints on lifting interest rates.

Expanding the supply side

More importantly, policy vigilance on inflation will be required over a longer period as price pressures associated with structural changes in areas from labour markets to globalisation and climate change play out – reinforced by relatively expansionary macro policy. Policy instruments beyond monetary policy will be required to manage these medium-term inflationary pressures.

This matters for economic outcomes. But the politics of higher inflation are also challenging. Periods of high inflation often lead to political turbulence.

Economic policy should focus on expanding supply-side capacity, and raising productivity. This should be based on a coherent economic strategy. Simply asserting that higher wages and costs will deliver productivity without further policy action (as suggested by the UK’s Prime Minister) is not enough.

Consider a few examples where structural changes will require supply side responses to manage price pressures.

First, changes in the nature and location of jobs in the post-Covid economy are creating mismatches between labour supply and demand – leading to skills shortages and wage pressures emerging across the economy (compounded by constraints on migration). In addition to talk of the ‘great resignation’, technology and new business models are creating new jobs and displacing others quickly and at scale. These pressures will endure for some time.

These structural changes in labour markets, accelerated by Covid, could lead to wage and price inflation unless met with policies that enable better matching of labour demand and supply – and support labour productivity growth.

Investing in skills policy, active labour market policy, and in well-judged migration policy, will help alleviate pressures on labour markets. Done well, wages can grow strongly with productivity improvements offsetting any inflationary effects.

Similarly, investment in capital and technology can push out the supply side of the economy – and support the labour market transition. The rapid, at-scale adoption of technology during Covid – and the expectation of a global ‘investment bonanza’ – will contribute to stronger productivity growth over time and contain inflationary pressures.

Governments can support productivity-enhancing investments by firms, and make complementary investments in public infrastructure (from high speed broadband to funding research).

Second, the intensity of globalisation, which has been a deflationary force over the past few decades, is no longer increasing – and the deflationary impulse of large emerging markets like China is weakening/reversing. And there are costs with trade and investment frictions (e.g. US/China), as well as the pressure for localisation and strategic autonomy.

Governments (and firms) should retain a strong bias towards openness, and strengthen resilience in a disciplined manner to manage the risks of higher cost structures.

Third, there are cost pressures associated with the transition to net zero. Although renewable energy prices are reducing sharply, the pricing is not yet always competitive with fossil fuels; and the broader transition to a low emissions economy will involve costs (including carbon taxes). This can be seen as a negative supply side shock, which is likely to have an inflationary impact.

The transition to a low emissions economy will require substantial investments in new capacity. Over time, renewables should be consistently cheaper and productivity enhancing. But in the meantime, governments will need to manage the distribution of the costs of this transition across the population and over time – including funding new low emissions infrastructure, technology, and innovation.

Playing the long game

These structural dynamics across the global economy will shape inflation outcomes beyond the near-term economic reopening. The governments (and firms) that act to strengthen productivity and expand supply side capability are likely to manage inflation pressures relatively well. The policy response needs to extend well beyond monetary policy.

Small advanced economies, which have a bias towards supply side over demand side measures to generate productivity growth, are worth watching in this environment. From Singapore to the Nordics, several have been developing relevant supply-side measures as part of their post-Covid economic strategies.

Many advanced economy governments have used macro policy effectively to exit the Covid crisis. But a new policy emphasis is now required: structural changes require a supply side response. Without this, expect higher trend inflation, weaker economic outcomes, and greater economic and political turbulence.

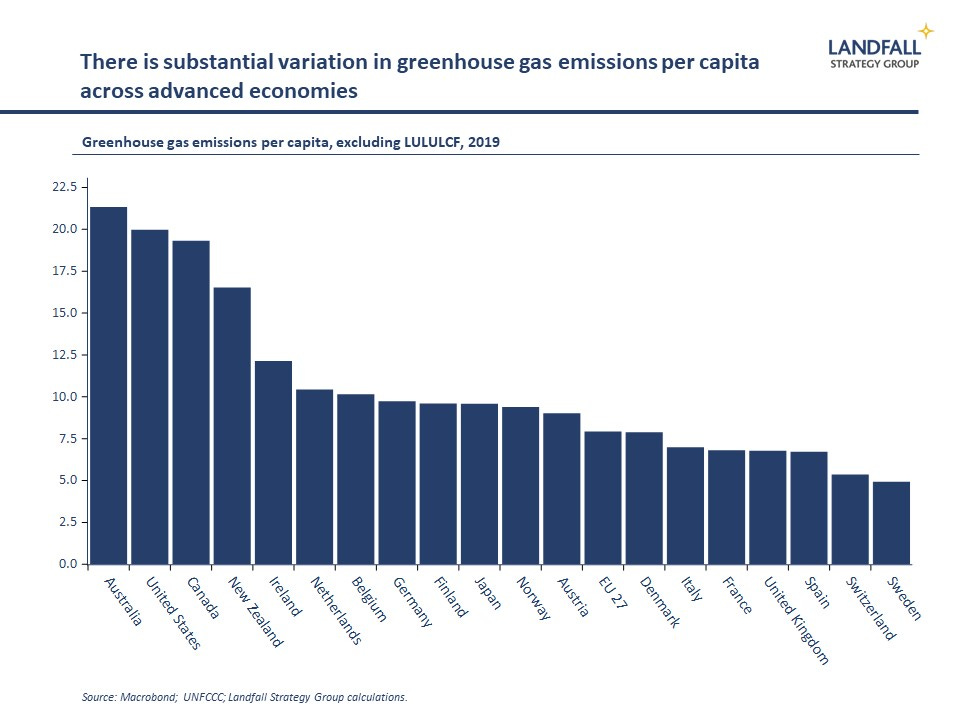

Chart of the week

As the COP26 meetings launch in Glasgow this week, it is striking how much variation in emissions per capita there is across advanced economies. This variation in emissions intensity goes some way to explaining variation in the ambition of national targets: Australia and the US have the worst records, whereas many European countries perform relatively well. The encouraging news is that emissions per capita has been consistently reducing across advanced economies – although not by enough.

*David Skilling ((@dskilling) is director at economic advisory firm Landfall Strategy Group. This article first ran here and is used with permission. Skilling recently spoke to interest.co.nz in a Zoom interview.

29 Comments

"Inflation – and the inflation debate – is heating up."

Why is it heating up !!!!

Has the Reserve Bank Governors parroting Fed not guaranteed that is is Transitory......What is Transitory is different story and topic of discussion

"Recent inflation readings in the Eurozone, the US and the UK, as well as Australia and New Zealand, have come in above expectations"

Everyone should chill as Reserve Bank Governors are always correct and what they say is Gospel Truth or are ready to be hanged, if wrong.......are we correct Mr Orr.

Long game.

We need to have a stable population policy (max 5 million) to avoid the disasters of infrastructure cost and maintainence. And the carbon of course.

The way to achieve that is limiting immigration to high skill (very high) and skill and tech knowledge interchange.

That of course means an end to cheap labour keeping wages down, and limiting process development. (higher incomes are good for New Zealanders, not a market problem)

Could set us up well for the next few hundred years.

Sadly there is no "Next few hundred years". We are at the tipping point and from here life just gets worse for many people and not better. Far to many people for a sustainable planet so it will turn into a fight for resources and what's left to try and maintain our "Current Lifestyle" we have grown to accept. Going forward because lets face it, nobody wants to make the sacrifice of a lower standard of living so things will remain great for the few that can afford it up until the very end. Bit of a bleak outlook I'm afraid but until we address population control, we are doomed to fail.

There aren't far too many people. The lifestyle of the rich is the unsustainable part. The richest 1% use more than double the carbon of the 3.1 billion poorest people on earth.

The way people live isn't something stagnant. We can change and force high carbon consuming activities are inaccessible even to the richest 1%. There is no insane population pressure, we make more than enough food for everyone it's just distributive issues. Sick of people blaming population when it's the structure of their lifestyle that's the problem.

For context credit suisse puts anyone with a networth over $1million USD in the top 1%.

Bugger that's me in the top 1% then, as I'm sure a few others on here are as well. Yeah maybe on a worldwide scale but not in New Zealand alone, that sort of individual net wealth puts you in the top 5% in NZ. You need multimillions here to make the 1%. Feeling a bit guilty now, just put my private jet on Trade-Me. Nope its a population problem, if we had half the current world population or better still even less we wouldn't even be talking about Climate change.

COP26 is a total waste of time, every country need electricity and its going to keep coming from Coal. Nothing will change in the developed countries and the climate will continue to warm and begin to control the world population through more and more freak weather events.

Nobody wants to talk population control, China tried it and it went sideways on them. Not a single western politician even wants to talk about it because its political suicide. Everyone thinks its their God given right to keep having kids.

It's pretty obvious there are far too many people, in spite of protestations to the contrary. Countries suffering environmental collapse due to the human population explosion would no doubt experience less human suffering, if there were less people for finite resources to be divided amongst. Madagascar is a current example that comes to mind. 5 million in 1980, 28 million now. Projected out, 100million by 2100. Of course that won't happen because the local environment is already collapsing and won't be supporting anyone by 2100.

World pop gonna cap out 9B by 2070.

All good.

I always wonder about these figures, is it $1m per person if married or if there are 2 people in the household $1m each?

Not hard to work out, its individual net wealth so if your married your partner gets half so you need $2m total. Net wealth is if your SELL EVERYTHING and then pay off the outstanding debt, your not at $1m just because your Auckland house is $1.2 but the bank basically owns it, you would need to be pretty much mortgage free and single. The problem is the perception that everyone's a Millionaire these days but if you did a deep dive many are mortgaged to the eyballs and the car is on tick, they don't actually own bugger all.

I understand your working I am just never sure if the millionaire status is $1m per couple or if because couple $2m.

Bit doom mate and no need to worry. All nations population falling or will be soon. India tips out in 2070 and everywhere else before then. Less population is bigger problem to be concerned about.

Yes life about to get exponentially more expensive but not necessarily worse. People will adjust. Govt will come to rescue bailing people out with benefits and subsidized housing. NZ still land of milk and honey if you don't mind very boring and quite bad weather most of the time. Seems a reasonable tradeoff, expensive and boring and bad weather for safe country to live in.

+1 . I’m continually dumbfounded that we have had 100,000s of immigrants in the last 10 years but we are supposedly facing a labour shortage. Would another 200,000 fix the problem? The mix of arrivals is wrong and I’d love to see a policy that heavily restricts the numbers and raises the caliber of successful applicants.

Disclaimer: I am an immigrant

There are a lot of unemployed around our town, either that or they are early retirees or shift workers.

There is no way NZ can play the long game; it has no capacity to be self-sufficient unlike bigger economies. The accumulation of human capital, technological advances and structural frameworks supporting self-sustainability are just too far from any critical mass required in the long game.

The current inflation picture is misleading as its a matrix of post pandemic recovery, greenflation and international politics.

While the misleading picture is painted by a post recovery economics, under its belly is the real inflation caused by greenflation and political instability.

NZ Inc will need to find its competitive advantage soon before the country turns into an exotic holiday island located in the bottom of the pacific but only for those who can afford it.

It’s that inability to be self sufficient that’s hurting us.

Behind your inflammatory comments is a very intelligent person. Good comment their CWBW.

I agree, good comment.

Less inflammatory trolling, more excellent commentary like this please :)

You have that a about f.

No country is sustainable, as formatted. And the ones closest to it, are being urged to become more unsustainable.

Inflation, from here on in, is probably permanent - except that the system cannot cope with it, so will recoil. But not enough remaining planet ve never-more demand, only goes one way - and we've taken the best; it's gone already.

But interest-rate rises will lead to cascading defaults, so we can't use them overmuch. And we have no other so-called 'tools'.

And even as we write, 2-3 $ of debt are required for every $ of GDP, and there's no physical underwrite for a way back from that, either.

Stagflation? Followed by?

"...before the country turns into an exotic holiday island"

Well at least that's optimistic!

And here's me seeing New Zealand turning into the go-to Retirement Home at the bottom of the Pacific, but only for those who can afford it.

Queenstown being a prime example. Bunge jump in the morning; ski in the afternoon and go back to your Arrowtown "Shady Acres" $Multi Million Unit in a secure environment to settle down to an exciting evening of Netflix after a home delivered repast from one of the multitude of outlets that provide such. Delivery and preparation provided by a mixture of Island Temporary Workers and European young on their OE.

Sounds great! I love Netflix.

Price increases may be broad and persistent (and I remain to be convinced they are), but they are certainly not uniform. The prices of different goods and services are surging and retreating differently - exploited by speculators (eg commodity traders) and price-setters like the Saudis and Russians. This is where the politics of inflation are felt - when the price of things like petrol or energy bills stress households and wages / benefits do not rise to alleviate that stress. I don't see things settling down anytime soon - not least due to the risk of conflict over natural resources.

When you add a carbon price of $100 - $140 per tonne (compounding fuel price increases), a pandemic with a long tail, and a health system and population ill-prepared for 500 covid patients in ICU and 30 - 50 deaths per week, the next few years are going to be a rollercoaster.

The free marketeers may not like it, but Governments (and their banks) have a role to play in steering economies through tumultuous periods like this. However, I'm not talking about impotent adjustments to interest rates - we need to increase minimum wages to mitigate the impact of inflation, invest in infrastructure that increases our self-sufficiency (sawmills!), introduce a three-year rent freeze to buy us time to regulate and licence our rotten and highly regressive rental market, spend money on supporting dairy farmers to transition away from cows (instead of spending billions on overseas carbon credits), and, as the article recommends, bundle all of this into a strategy for a sustainable 2050.

We may be a tiny island in the south pacific, but we have an endless supply of clean water, an easy route to 100% renewable energy, fertile soils, decent broadband, and a brand that can be easily translated into low-carbon income. If only we had a Government capable of setting out a vision for 2050 (instead of one that can't see beyond the next election).

Went to the supermarket, a good Aussie shiraz like Pepperjack is still only about $20. Hardly changed in the last 7-8 years.

I don't think clothes prices have changed much either.

Inflation has a totally different impact depending on what stage of life your at because of what it is your purchasing. If your sitting mortgage free with cash in the bank its great your Pepperjack is still $20 and all the cheap clothing made in China and that new car is also great value compared to 20 years ago. The cost at your local restaurant really hasn't gone ballistic due to way more competition and same with many other things. At the other end of the scale life now sucks trying to make a buck in this country and house prices going up more in a month than you earn in a year.

Very well put.

Inflation can work positively for many families in some ways:

It shrinks your mortgage size relatively. It boosts your wage levels. It keeps an urgency and velocity on consumer spending (buy before prices rise).

It also provides higher term deposit income for retirees.

And it all relies on "It boosts your wage levels."

What if it doesn't? Or what if employers raise the wage of 75% of their employees and sack the remaining 25%, to keep their wages bill the same, in the face of rising costs elsewhere in their businesses? What does that 25% do? Stimulate the Economy isn't the answer. (NB:They'll probably Work from Home, and undercut their ex-empolyers prices as they have fewer overheads - Deflation creeping in via the backdoor as business seeks out the lowest cost of provision of goods & services)

Answer: Everything else that you suggest falls apart if wages fail to rise. I know - they will; they have to, right?

""It also provides higher term deposit income for retirees"

How? Enlighten me

1919 was the last time Mother Earth was able to sustain the human population at 1.9 billion we're now 6 billion over populated and using resources like never seen before sadly. Resources are the true wealth

No, it's bitcoin. Sorry, kiwisaver. Oops, my savings. Ah, hang on.....

jeez - you're right. Whaddya know?

Answer - more than anyone trained in flat-earth economics.

PDK's tipping point may be here - or may be not. If not, it's probably not far away. So - I'll be getting my solar panels fitted & installing 5,000 litres of water storage. My beautiful back lawn is earmarked for a vege patch which means we will have to move the washing line. Bugger. It's perfect for the sun where it is. Haven't budgeted in killing cats for protein just yet, but have made a note to self for 2023.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.