By Katharine Moody*

It has been two years since I introduced a formula approach for a weekly rent maximum to Parliament’s Petitions Committee. In this time, rental market conditions have improved marginally for both landlords and tenants.

Despite the cooling of rental price increases, many other statistics are going in the wrong direction. Nationally, rent costs are now the highest ever as a proportion of median incomes. Last year nearly 20% of households spent 40% or more of their income on housing costs, up from 18% in 2023. And for the year ended June 2024, 9.4% of households were in material hardship, up from 8.6% in the previous year.

New Zealand also faces additional headwinds in the housing space associated with uncertainty in the global trade environment. We can expect more internal shocks, similar to the wholescale layoffs in timber and paper production markets. Even though many of the individuals laid off in Ruapehu and Tokoroa might be homeowners in these communities, some will now need the Accommodation Supplement from central government, where they might not have qualified previously. And the ‘caps’ on that subsidy, combined with unemployment benefits might not cover existing mortgages.

Even the National government when introducing their Going for Housing Growth plan, admit that all- things-accommodation are dire;

Our housing shortage manifests in different ways; from very high prices for first home and other buyers, poor quality, increasing rents, and growing demand for social housing which has resulted in over 3,500 families living in motels and more than 400 living in their cars.

That is the situation, despite them noting that;

The government spends nearly $4 billion1 each year on housing subsidies. Our housing shortage particularly affects low-income households.

The NZ Property Investors Federation (NZPIF) said to me two years ago when I was formulating my proposal that to fix the housing crisis you have to fix the rental crisis first. And the good news is, a number of the NZPIF requests were implemented with the change of government; (See more here).

The NZPIF also recognises that shortfalls in the current Accommodation Supplement settings are causing tenant hardship, as they also suggest above, that;

Private rental providers should receive all the Government support that social housing providers receive (bullet 8. under Lower Costs, Lower Rents).

What could we have instead of these subsidies?

An optimally functioning housing market requires the full spectrum of offerings from social housing, market rental, rent-to-buy, shared-equity purchase and market purchase at an affordable rent-to-income level.

Given the regulatory changes to improve rental property bottom lines, combined with slow (but seemingly steady) house price declines, I believe now is a good time to claw back some of the $4 billion dollars per annum in government expenditure on housing subsidies.

Bearing in mind, $4 billion in annual savings would buy in any one year:

the full monty Dunedin Hospital upgrade;

more than the entire annual Pharmac budget;

a reinstatement of the Jobs for Nature programme;

more than the entire Early Childhood Education budget before the recent cuts; or

the entirety of the scrapped $3 billion Interisland ferry project.

These are but a few examples of the social cost of allowing our housing market to get so out-of-kilter with median household incomes. Governments the world over are to blame as reluctant regulators of this market, and New Zealand in 2024 was one of the worst.

Further studies on the weekly rent formula model

So, what progress has been made on my formula approach to rental market regulation;

(RV/1000) - x% = weekly rent maximum

The Petitions Committee reported back on the proposal in September 2024. There was no appetite from the Ministry of Housing and Urban Development (MHUD) or Ministry of Business, Innovation & Employment (MBIE) to regulate private sector rent, although that was not unexpected given the election was only two months away.

However, the Social Policy & Parliamentary Unit (SPPU) of the Salvation Army conducted further research on a version of the formula approach as a means to identify;

… a fair rent based on actual median household incomes and house prices… to provide an alternative source of information in the rental sector.

The fair rent information produced based on the formula approach is intended to supplement the market rent information provided by Tenancy Services.

The SSPU report, titled Tackling Rental Affordability in Communities applies the findings of their research. The data is impressively granular, using Community Compass databases. And a fair rent calculator look-up tool (look up by residential address) is currently under development.

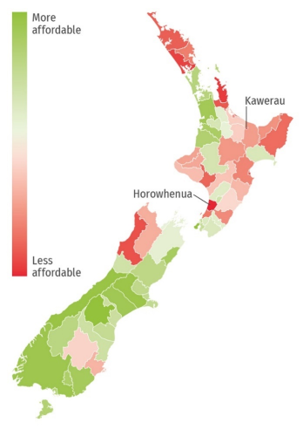

The SPPU results are visualised in the following Rental Affordability by Territorial Local Authority diagram below (see page 5. of the report);

You may want to do a double take on that diagram. I expected our major cities, particularly Auckland, to be the least affordable housing markets. But not so, when you look at median household incomes for each district against the median house price. Where median household incomes are highest – rent as a proportion of income, is lowest. And where median household incomes are the lowest, rent as a proportion of income, is highest.

In other words, despite being geographically located in a lower housing cost district, those renting in those locations suffer more as a percentage of income in making their weekly rent payments.

From a planning perspective, these findings are a concern. Logic would suggest that over time families in the ‘pink’ geographic districts will migrate toward the main centres (i.e., the ‘green’ districts) with higher wages and better rent-to-income ratios.

New Zealand last experienced a domestic urban migration wave and a ‘hollowing out’ of our small urban areas in the decades post-1984. Due to the influx of ‘economic refugees’ from small town New Zealand, infrastructure deficits in our main urban centres started mounting rapidly during these decades.

And if future economic conditions mirror that era, the larger urban centres (already struggling under the pressure of increasing international migration) will experience greater and greater housing stress and homelessness. This is what we see overseas.

Conclusions

Which leads me to conclude that the Going for Housing Growth policy of the National-led government, won’t be enough – not nearly enough.

The government, through their Kainga Ora reset, has made it clear, they aren’t going to be the ones to build our way out of this. Neither does the government make decisions for the residential development sector. A sector already under strain.

So, how might the government begin to claw back on their $4 billion annual rental assistance costs, while also making housing more affordable at the same time for all New Zealanders?

I would suggest, that regulation of the private rental market is a necessary step, and perhaps the only way to avoid the plague of homelessness seen in so many of our OECD counterpart cities.

The sooner they pick up the policy work on an affordable rental market, the better.

1) The National government’s plan does not break this number down into individual line items in the budget, but from HYFU 2024, it is likely made up of $2,495 million in Accommodation Assistance plus $1,619 million in Income-Related Rents.

*Katharine Moody is a senior tutor at Massey University's College of Humanities and Social Sciences in Palmerston North, who comments on interest.co.nz as "Kate". The views expressed in this article are her own and don't necessarily reflect those of Massey University.

75 Comments

Despite the cooling of rental price increases, many other statistics are going in the wrong direction. Nationally, rent costs are now the highest ever as a proportion of median incomes. Last year nearly 20% of households spent 40% or more of their income on housing costs, up from 18% in 2023.

Rising housing cost is not the same as deterioration of rental affordability.

The definition of housing costs in the context of their report refers only to accommodation costs (rent or mortgage) - not utilities etc.

There is only one answer to over-priced private rental homes:

We need a government that will resuscitate the state housing agency Kainga Ora, and have it build, own, and manage 100,000 quality homes for secure, income-moderated lifetime rent by whoever wants them.

Put the landlords out of business.

You are just shifting the subsidy from being a cash payment to a lose making entity. That's not solving the problem for the generations that are paying for it.

Those old houses sitting on quarter acres close to city centres are the problem - plain and simple. Either give councils the power to tax the crap out of land located close to CBD and major transport corridors and ring-fence this revenue for new housing infrastructure delivery or let's keep playing the fiddle while Rome burns to the ground.

give councils the power to tax the crap out of land located close to CBD and major transport corridors

Councils already do have the power to set a targeted rate based on distance to a CBD. Their GIS mapping systems are capable of that kind of search function - just give them a circular perimeter to be covered by the targeted rate - and the GIS will pick up every land parcel within it.

Could do now if they were so inclined.

How many at the council own a property within any proposed targeted rate zone?

none of the councils do that kind of targeted rate to my knowledge. But, yes in many cases those holding up urban development policy progress (and that includes a change to the way properties are rated/taxed) are those with vested interests.

They should scrap the accommodation supplement it is a subsidy that raises rents. Without it rents would lower to the level people could afford. Simple supply and demand with force that

The gummit run the accommodation supplement and the Income Related rent system. Why the heck don't the at least combine it into one. Both have huge problems and both get ripped. Accom Supp results in multiple people claiming on the same home, Income related rent disincentives increasing ones income.

Shambles of a system.

Can we at least call it what it actually is “It’s a landlord subsidy” plain and simple

That would be nice if it were paid to the LL however, recent experience shows me they still get into arrears to the point they are evicted, not a cent to the LL but plenty to the meth dealers.

That's the point - at present the AS isn't enough to fully supplement accommodation costs - which is why the NZPIF requested that the supplement be raised to the same level it is for community housing providers. See above linked .pdf file.

In this case supplimented the meth dealer but not paying the LL. If said AS was paid directly to the LL then the meth dealer would miss out.

In a few cases yes. But asup rates are directly related to rent paid. So your rent goes up, asup does as well (to a point)...and is paid to the landlord via the rent increase.

The tenant is the conduit, the beneficiary is the landlord.

Exactly. Personally cant see this being massively unwound by a national Govt. Would be funny in the left had to support a National lead change here though...

When I spoke to the SC last year, it was a National MP chairing it. She and the ACT MP on the panel were the most enthusiastic with the prospect in my opinion. But of course, time for questions is limited in those presentations.

Scrap the AS ... if a landlord is not financially wise enough to by an investment property, relying on a Government handout, they are no better than a dole bludger !

Then introduce a capital gains tax for every second and subsequent property (except the family home) - NZ is the only country in the OECD that does not have some form of capital gains tax. Also no "funny stuff", with putting an investment property in your dog's name or a company in the Cayman Islands etc etc

Yes, let the landlord completely claim back their mortgage interest payments - as they are running a business to make money, so why should I as a taxpayer support your business through the AS, when all it has done is raise rents for tenants and increased house prices for FHB's !

I hear screams of the "over extended" saying "I'll go under" well, who cares - every business has a cycle and it not just about YOU ...it's about the economy for ALL and the overall standard of living.

It may mean, dare I say it, people's incomes being able to afford that first home or renters being "self sufficient" with their accommodation needs.

Then let the "free market" do its thing .... if NZ is a so called "first world economy" can't sort that out, well what hope is there.

It wont just be the landlords that go under. It will be the banks as well. If you havent bothered to read any history, we've already seen what happens when the banks go under due to a housing collapse. It was called the GFC. Go look it up.

No, the effect on local banks would be nothing like the GFC was in the US. Private rental properties make up only a third of our dwellings. And when I looked at it years ago, around 50% of all properties advertised for rent had been purchased more than 10 years ago - so much lower prices, meaning (provided the mortgage has been paid down) early entries to the market would be fine profit-wise. And even if those LLs had borrowed on the uncapitalized gains on other houses in their portfolios, they would still be making money (i.e., that capital gain) in the sale. So, even if they choose to sell because regulations are brought in, you'd find very few people/LLs being foreclosed on.

WTF? Are you suggesting that a collapse in rental property prices will have NO effect on the rest of the housing market? You truly are deluded. Anything you say cant be taken seriously.

Let's assume the cost of housing stayed the same forever for OO's. This would simply mean that the mortgage would inflate away but their access to using the house to access credit would be limited, which would impact the velocity of money in NZ. Is this so bad? Not in my view but I am aware that so much runs on housing debt. IMO it would force people to allocate their time, energy and resources into more productive means instead of being able to keep piling debt (risk) up for investments. We need to ask a serious question of what sort of society we wish to have, one where it is affordable to rent or own without a generational wealth tap, or one where we have a small percentage of the population owning and controlling the bast quantities of assets and resources, while keeping the rest under their thumb.

Firstly, we need a phase out - not a halt - just stop indexing it up.

Secondly, the issue is that the higher rentals flow onto higher house values - which flow onto higher land costs. There is a case for saying land owners have been the real beneficiares of massive house price increases. The only way to make housing more affordable is to massively increase supply. That doesn't need Government to be building the houses (KiwiBuild built 2.000 in Auckland while the private market build around 75,000). You just need to zone the land. and there is a case for saying you don't even need to build the infrastructure - because if land supply increases it can be reflected in the sale price.

K.W .... did you look this up, as you know everything about the GFC ..... NINJA loan - a type of high-risk loan issued to borrowers with no income, no job, and no assets

While the NZ banks wouldn't go under at all ....they are not practising that type of lending, as in the US pre-GFC, while then Wall St et al would "package up" these loans and sell them as so called "securities" to some unsuspecting school board in Norway.

If house prices crashed, the banks would most certainly go under. They wont be able to recover the money lent, and they wont even be able to sell the houses that they repossess - like the American banks, they'll be sitting owning houses for years. Owners will be bankrupted and unable to buy another house ever (due to credit scores). It would be worse in NZ than in America, as NZ banks have these loans on their books, whereas the US banks at least had the foresight to offload them to other investors via mortgage bonds.

Well then, I'll repeat .... if a landlord is not financially wise enough to by an investment property, relying on a Government handout, they are no better than a dole bludger.

Disclaimer: I was involved in the post GFC housing crisis in the US

A debt/asset reset could be managed quite sensibility if you take the emotional fear out of the equation, it's only numbers on a screen.

There needs to be a change in values across the board.

Accommodation supplement is baked into the housing market now; so many billions in taxpayer money has, in effect, funded the property investment & capital gains of many. Has anyone modelled what would happen to property prices if the accommodation supplement was simply stopped?

It could've easily been removed when interest rates were stupidly low - would've had less effect than the then-raising rates had.

A bigger problem is how to remove it - not everyone gets it. Does the government just declare its removal, telegraph say, 6 months notice, prevent evictions leading up to its effect, and send a letter to all recipients to provide their landlord with a notification the rent must be reduced by that amount? Imagine the workload that will induce at the TT level when landlords refuse.

Also, some properties do have legitimate reasons for multiple tenants receiving AS - student flats and boarding houses. At an individual level removing the AS for each of those isn't a problem, but those landlords may face a world of pain. Luckily there aren't many of them.

And then, if it's implementation was telegraphed far enough, it will simply be cancelled as an election promise!

Re: the student housing, if an investor purchases a rental with their business plan relying on the government handout, which gets changed, they will simply have to try and find tenants who can afford the rent the LL needs to cover the mortgage or they'll have to top up the mortgage or or sell up. This, on a large scale will cause possibly a temporary hike in rents for those desperate to hang on to bad investments, but more likely prices to drop as more and more IP's become bad investments and go on the market. Ultimately this will help.

Has anyone modelled what would happen if the accommodation supplement areas were reversed. Choose to live in over crowded Auckland and get little from the taxpayer but choose to live in a remote rural area and the low-paid would get showered with money from the govt - of course mostly for the posher houses demanding higher rents. Help stop the steady march of zombie towns and villages.

I have done a fair bit on this when I headed an economic development agency.

What has been happening is the accommodation supplement means businesses relocated from the regions to Auckland. In simple terms $600 a week rental in Auckland gets a $100 per week greater subsidy than in provincial centres (ie same rental - bigger supplement). Of course the home for $600 in Auckland is not the same as in a secondary centre - so the Government was actively subsidising poor accommodation over good. It also became a subsidy of the business owner - who could employ people at the same wages as the regions but at lower transport and distribution costs. It also meant a lower relative wage worker in Auckland, so an effective de-skilling in employment - which may be the cause of low productivity growth.

It can be removed by stopping the indexation up - so it slowly becomes less impactful

There's a lot of statistical merit in that thought based on a look at that map figure.

As a girlfriend of mine renting in Whakatāne said, property owners/landlords are charging Tauranga prices. Big difference in median incomes between those two urban areas - and as a proportion of median incomes, the folks in Whakatāne are paying a much higher percentage.

Hi Kate,

Agree that rents are massively far too high.

Rent caps would reduce the return landlords make, reducing rental supply but increasing the relative number of houses for sale. (It would work almost like an invisible capital gains tax and would help push capital towards productive use, rather than being used to bid up land prices.)

Its a good sticking plaster, but somehow we have to deal with the continuous stream of incompetent governments that have got us in this mess in the first place.

I really could not disagree more (I always enjoy reading your work though Kate!).

If you want rent caps, or any other form of rent control, then have the State build and provide housing for rent. Why the obsession with controlling the private rental market? Probably because there is no other viable alternative.

Let's be clear, rents aren't high - they reflect the commercial reality of providing rental accomodation. Rates and insurance on an inner city villa (nothing too flash) in Wellington - $250 p/w. Where do you think the rent should be on that poperty? Do the maths, price up a block of land, price up the cost of actually getting consent to build a dwelling and any contributions required, price up the cost of a build, add in rates and insuranec and tell me what the rent needs to be to break-even. This has almost nothing to do with landlords being greedy and profiteering and everything to do with the marginal cost of providing a unit of accomodation.

The solution is for us as a nation to raise our productivity, upskill and increase GDP per capita.

Where do you think the rent should be on that property?

If you give me an address, I can run the exact property through the model and let you know what it's fair rent would be.

You'll likely be surprised as Wellington being one of the highest median salaries in NZ will mean that the "market rate" (via tenancy.govt.nz) is likely very close to the "fair rent" (the maximum calculated under the formula).

Agree with you that a new build won't likely be a good choice/investment as a rental property, unless you are prepared to wait until the unrealised capital gains start working for you. True of most capital investments - be they buildings and/or equipment/plant.

It looks like presently, LLs are wanting the tenant to pay for all of their outgoings from day one..

I used Welly as I priced that up recently, the costs are absolutely horrendous. It's a multi-headed beast, the building code itself is continuously pushing costs higher, so are councils, so is the weak Kiwi, so is our lack of prductivity, so is our lack of investment in infrastructure, so are our low wages.

As someone said above, try and get a resource consent for anything and the costs are eye-watering.

That's not the point Te Kooti. If you give me an actual address - you would be able to determine whether regulation of the rental market under this proposal would make any difference to the current market rate charge.

The objection you have with my proposal has nothing to do with the objections you have to the building code, the councils, the weak NZD, etc. It doesn't address those things - it only gives you a maximum weekly rent that can be charged for a particular property. And if the market price is in-line with the 'fair rent' - all good. If not, then most of the prospective tenants will need a government subsidy to live there.

Would be interested to see what it comes out at for the unit in the papers that burnt recently. 77E Bordesley Street, Phillips town.

The fair rent estimate on that unit would be $223.00/week.

You would get to see the granularity of the median income data used - if you gave me an address for a one-bed unit in Cashmere as a comparison.

Be happy to look that up for you too.

It's very impressive how the calculator works.

Let's be clear, rents aren't high - they reflect the commercial reality of providing rental accomodation.

Disagree here but there's a spectrum to consider. He who has a low mortgage who purchased 10-15yrs ago and didn't overleverage will be fine with this and creaming the market rent - which when analyzed with median rents is a fairly reasonable way to establish if the average rent is too high. He who has high mortgage and leveraged to get a greater portfolio will be asking the max they can get to maintain cashflow. 4k increase (total) in rates and insurance = approx $80/week over the course of a year. Once again, if the investment isn't profitable or profitable enough, then it is able to be offloaded. Not all costs can be passed on a the market dictates the price more than the landlord.

The commercial reality of residential property has been highly distorted by government and RBNZ policies. In many ways it needs to be unwound. Unfortunately the academic beliefs have become so deeply embedded in the general narrative it'll be hard to implement.

Will productivity, upskilling and GDP per capita really bring home prices back to more reasonable levels, with less influence on the wider economy, and financial stability? It sounds more like a reckon than sound science.

Agree. And a really good point about how incompetent NZ governments (or governments protecting the real estate investors) must go..

@KO I get a bit sick of people moaning about rents being to high! Buy some properties and rent them out at what you think they should be. Solve the problem, don't moan about it! Hmm, I guess not huh, to hard?

Exactly, if you think landlords are creaming it, then become a landlord, pool funds with your mates if you have to (public schemes to buy parts of property are called syndicates)

The property prices have already been bid up because of the government subsidy to rents, that's kind of the point. This isn't something an individual can solve.

The real gains have been hoovered up by those who bought property a decade or two ago - there's just scraps left for those buying at today's prices (and especially at 2021's prices).

Regulation of the private housing market just exacerbates the problems. Maybe learn from overseas experience

https://www.telegraph.co.uk/business/2024/10/19/rental-market-catastrop…

The method of regulation is not found anywhere overseas (that I could find). The difference being that this proposal applies universally to all residential rental accommodation.

Logic would suggest that over time families in the ‘pink’ geographic districts will migrate toward the main centres (i.e., the ‘green’ districts) with higher wages and better rent-to-income ratios.

Logic has nothing to do with it. People will stay in the pink districts because they are all on welfare, and its intergenerational now. They do not want to work. They do not want to move to areas where there are jobs. They're quite happy being unemployed, pumping out kids, receiving benefits, and waiting for Kainga Ora to build them a million dollar house for which they will pay peanuts for the rest of their life, and their childrens lives, and their grandchildrens lives .....

Then if they still want more money, they wait for the next Leftist Govt and then demand "reparations" for colonisation, while confiscating other people's money by way of wealth taxes and Expropriation Acts.

And then the transition to South Africa will be complete.

OMG - I hope we lose you on the 1st.

Are you trying to get booted off before then :-).

Looks like he got himself booted off lol.

From what I see the price of houses are as affordable now as they have been for almost 20 years [exempting covid]. In our area today, house prices are not that much higher than what they were pre-covid. Our main rental has gone up & is now back down to about plus 10% from Jan 2020 when we bought it. Which, over that 5 year time frame is still less than inflation. If house prices can stabilize/drift for the rest of this year, then I believe most people will be in a better position this time next year.

Two housing markets to watch are the Australian ones & the USA. Both countries have many multiples of housing markets & both are at all time highs, or thereabouts. I'm expecting moderate price declines in both countries in 2025.

The good news is 'at least we're not as bad as China', although I know I need to tread carefully here. China today reminds me a bit of 2007/9 - in North America particularly, although my view was from the outside looking in.

As for the rent, we have been unable to break even on our rentals. This was true when we began 10 years ago & is true today as well. Capital gains? Up & down with our nose in front as I write this. This time next year[?] who knows. At least interest rates are on the down.

Yes, it would be great if interest rates went down - that too was a very big concern for the NZPIF (property investors federation). I think if you click through the link to that .pdf you'll understand their recommendation regards interest rates on rental housing.

On prices, Wellington City was just revalued - an average 25% drop in price from the 2021 valuations. It's quite a shock for folks who were revalued in the 2021 year peak prices. Things were just so ridiculously inflated then.

I recall German(approach) where the landlord owned the building and nothing else. Entire fit out was with tenant, drapes, carpets, utilities and the like.

Tenant unable to be evicted unless did no pay rent.

Tenant had an asset to sell onsell to a new tenant.

Landlord had no worries about R&M, damage etc.

Why can't we think outside the box?

Yes. We need the whole range of options in our market. That's an excellent suggestion. It's a bit like our current QE II covenant - where it is land that remains in the ownership of the landowner, but rates are not charged on that parcel of land - given the property owner cannot take the land out of 'retirement'.

It's called a lease. (Leasehold)

Because it is household income that is measured how do we know the 'more affordable' rents in higher median multiples is not due to more crowding of income producing people in those houses?

And/or that because the increase in the median multiple has been higher, landlords have been focused on capital gains yield rather than rent yield?

Good question.

Our last rental in NZ, when we took it was 3rd most expensive in the area (the other 2 were honestly mansions - sports courts, cliff-top views etc.).

The previous 2 sets of tenants were multi-family, and both tenancies ended due to inability to pay the rent after someone moved out.

The landlord dropped the asking rent 20% before we looked at it, mind.

Can't say I quite understand the question - but I can 'look up' what the fair rent for any specific property or properties would be.

You could then 'test' your question that way.

My point is that the graphics of who pays more rent where is open to other variables that you don't seem to have thought about before making a judgement as to cause effect and solution.

For example, some developers in higher house price areas are building new houses all with ensuites on all bedrooms to enable multiple couple occupancy. This will generate a far higher yield inspite of higher price when compared to regional rentals that are cheaper but of lower occupancy.

This is the longer term rental equivalent of Airbnb.

But God help any Mum, Dad and three kids from needing to live in the area.

Personally I like your solution but just as I would like better and more Ambulances in an emergency.

But all this could be avoided by a better fence at the top of the cliff.

Agree, Dale. But, I don't mind thinking of it as more ambulances in an emergency - given we have been in an emergency for years now - one that costs us $4billion per annum and counting. But the really good thing about this formula approach is once rents reach that 30% of median income level for a given area - the formula result is of no consequence because the market rent (as per tenancy.govt.nz) is equal to or less than the fair rent.

I think the recent initiatives with freeing up land and encouraging intensification are going to solve our accommodation issue in the long term, providing immigration stops running ahead of house building.

But meantime, a 'circuit breaker' is needed as those tax dollars are so extremely important in other areas, such as health and education.

There is misinformation in many comments in this thread. For instance no banks in NZ 'went under' during that mother of all depressions (yes depression, not a piddly recession) from 1929 to WW2.

FACT: a huge number of houses were walked away from by the owners or tenants who repectively couldn't pay their mortgage or their rent.

I've said it before that my mother (about 8-years-old at the time), her sister and parents were renting a villa at 4 Cromwell St, Mt Eden.(I believe the very same house that Helen Clark bought.)

(My mother died just over couple of years ago of the Chinese plague just before her 99th birthday.)

Many of the houses around them were empty and my mother distinctly remembers asking her mother: "where have all the people gone?"

However, people were more resilient those days; my grandfather got the landlord's permission to turn the house into two units so he could sublet one of them and live in the other.

This was definitely the prevailing situation at the time, so I'd like to know from a sociology or an economics historian how it was that no banks went under with so many houses unoccupied.

Streetwise- in the depression the government stepped in and legislated to require debt forgiveness on the underwater portion of mortgages on properties, including farms and family homes. That probably helped banks as while they would have had to accept some losses, it probably averted the wholesale chaos that would have accompanied mass mortgagee sales.

And I recall that up until the 80s many people had to take out second mortgages (with solicitors) as banks would generally only loan around 2/3 of the value of a house.

Thanks....I'll take that. It must have been a huge outlay by the government of the day.

Yes, I remember those 1960s to 1980s. I bought my first home in 1967 for $11,000 and something dollars (pounds were replaced by dollars earlier that year) and I took out a solicitors 1st mortgage for around $8,000 to add to my deposit of around $3,000 and something.

Solicitors' mortgages were very common because some of their clients with spare money to invest had the option of receiving a higher rate of interest from these mortgages to house purchasers funded by the so-called solicitors' trust accounts than from a bank's term deposit.

However, it became apparent over those few decades that an unusually high number of solicitors 'couldn't keep their fingers out of the till' and fairly regularly the Herald would carry the court trials of such solicitors. In fact this malfeasance became so prevalent that the national law society had to make sizeable annual contributions from all solicitors to reimburse the defrauded mortgagees. At one stage the total funds so collected weren't enough to cover the frauds so the annual contributions had to be substantially increased.

So I guess, in the end, this fraudulent activity was such that it was showing the legal profession in a very bad light so the practice just seemed to die a natural death.

There is also a missed issue with Council social housing. In Auckland or Wellington the councils reduced rentals to 'affordable levels'. However, by holding down the rentals by (say) 100 per week then the person's accommodation supplement dropped by (on average) $80 per week.

So Wellington City Council owns around 2,000 social homes. If it charges $200 below market rates per week, this would save the tenant $40 per week and the Government $160 per week. So 2,000 social houses is $16 million per annum subsidy of central Government by Wellington City Council.

The figures Katharine Moody presents should be anylised before jumping to conclusions.

The $2495 Million spent on Accommodation subsidies to private housing providers is spread over the 6044785 private rentals as per the 2023 census. This equates to $4125 subsidy / assistance per dwelling.

The $1619 Million spent on Income Related rent subsidies is spread across the 76271 social houses provided by both the government and CHPs. This equates to $21226 per dwelling.

So the social housing provider's tenants get over 5 times more help than tenants in private rentals even though they are on the same benefits / low wages.

Assistance for tenants should be based on the need of the tenants and not on who their landlord is.

Yes, that was why the NZPIF wanted the same subsidy as the CHPs.

But that's no solution - that's going backwards (i.e., more expense to the general taxpayer)!

We want to aim policy toward a subsidy-free housing market! Just like you nurture your children toward becoming self-sufficient/self-reliant.

Neither should the government be topping up FHB deposits. It's an out-and-out subsidy too!

Housing foundation 'rent to own' model has some merit . I think ownership brings with it a more responsible societal individual and that larger society wins when folk learn to be more responsible. The model we presently have with govt subsidies and supplements leans toward the enriched investor type and tends to erode the ability of those less fortunate to play in the RE sandpit and its really not just about being able to play in the sandpit for 1 in 3 kiwi households , its about watching your hard earned money walk out the door every week into someone elses pocket and being able to set enough aside after clearing all the weekly/monthly costs . Clearly the gaps are widening and with every upward RE cycle that dream just keeps slipping away for many. Sadly we have created an industry that leans on the financially weak and empowers/enriches the strong via capital gains for example . I think we have dug a very deep hole with subsidies and supplements and it will be no easy feat to discard such given the damage it will inflict on those less fortunate. Banks and financial institutions are all for the 'dog eat dog' (Capitalist) mentality and surely must delight when the RE market booms and lets face it even if the market hits the rocks YOY growth is all these institutions focus on. The problem RE and banks ,financial institutions have is the bigger the numbers get the more diluted the newbies pool becomes. So presently we have a market expectant on surging demand with the lowering of mortgage rates but if we consider the fallout from the last surge is still clouding the picture somewhat (inflated prices/costs seemingly now neutral according to the press) I doubt enough newbies have the buy in required to climb on the ladder and bust RE out of the doldrums . With luck this forces an alternative model of ownership to show itself ...something the common renter can participate in perhaps ?... Wait a minute reality tells me the financially strong wont have a bar of ANY it....lol

First, they have scraped the innocent children's free transportation to school. Now they are poisoning the next generation with cheap quality foods. Running a country is not same as running a company. The blood-sucker vampires only work for themselves and not for country. If you cannot run, its better to step down and leverage the opportunity to others to lead this beautiful country. NZers deserve better.

How do such delusional articles make it to print at interest.co.nz

This website has become a bit of a disgrace and dumping ground for left wing drivel.

The rental market is actually soft right now across the whole country and rents are going down.

You dont need more regulation, it is regulation and red tape that has kept rents high, things such as taking away Interest Deductibility, ridiculous rates rises, insurance costs and silly compliance costs.

Letting the market build more houses, stop trying to control and over regulate to death the people of NZ, sack the 1,000's of staff at places like Kainga Ora that earn over 120k each and contribute nothing.

But are you also in favour of the $4 billion pa being spent on housing subsidies?

One could only say we have a functioning market if it didn't need such subsidies to ensure people are housed.

Building at scale takes time and it's not the government that will be doing the building over the next 3 years. We cannot force the private sector to solve the problem overnight.

The main problem is the lack of affordable housing. It's an old recipe, but rather than MORE regulation we need to cut bureaucracy in housing develpment and limit immigration.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.